BRICS - The Project Of The Century

Authored by Peter Hanseler via VoiceOfRussia.com,

The Western media are prioritizing the Ukraine conflict, the green revolution and the woke revolution. In the shadow of this media coverage, BRICS is changing the world.

We bring you the latest figures and place them in the current geopolitical environment. – An analysis.

Introduction

One of the main topics of this blog is BRICS. We have written numerous articles, followed and analyzed the development of this organization. Significantly, the first independent post on this blog was dedicated to BRICS on November 18, 2022 “The unstoppable rise of the East“.

Our last dedicated BRICS-only article from 24 September 2023 “BRICS will change the world – slowly” gave an overview of the development and summarized the results of the BRICS summit in South Africa in August 2023. This article was published by ZeroHedge, the GloomBoomDoom report by Dr. Marc Faber and Weltwoche (print and online).

From the density of our coverage, it is clear that we ascribe paramount importance to BRICS for the geopolitical and geo-economic development of the world. Based on the facts, we have come to the conclusion that BRICS will change the world more than all other developments of the last 100 years put together. The developments around BRICS have already triggered a tectonic shift in the geopolitical balance of power; the Ukraine conflict and the accelerating crisis in the Middle East are merely pieces of the mosaic by comparison.

The Western media are setting their priorities differently and focusing on topics that we believe are of lesser importance: Mortal enemy Russia, wokeness and green ideology.

Reporting on BRICS in the West, if it takes place at all, is limited to portraying BRICS either as an instrument of China to achieve world power – as the Financial Times put it,

«How the BRICS nations risk becoming satellites of China»

FINANCIAL TIMES – 26 JULY 2023

or to trivialize the success of BRICS – according to the NZZ,

“We explain in the video why this extension only promises limited success.”

NZZ, 14 DECEMBER 2023

Preliminary remarks on the figures

We proceed as we always do and develop a fact-based foundation for a discussion.

Membership doubled as of January 1

Since January 1, Saudi Arabia, Iran, the United Arab Emirates, Egypt and Ethiopia have joined the existing members (Brazil, Russia, India, China and South Africa) as new members.

Argentina not participating

In August 2023, Argentina was invited to become the sixth member. However, the new president of Argentina, Javier Milei, decided not to accept this invitation and to rely on the USA and Donald Trump to rescue his economy.

It is impossible to judge at this point whether this decision will prove to be the right one. For the second largest country in South America, which was once one of the richest countries in the world, it is to be hoped that Milei can pull the cart out of the deep mire. Milei is fighting against the establishment in Argentina, which has driven the country economically to the wall. These former rulers are serious opponents who are fighting for sinecures that Milei must wrest from them if he wants to save Argentina. We hope that Javier Milei can prevail and wish him every success and good luck. The first signs of success appear to be emerging: The country was able to report a positive budget for the first time last month. It seems to be heading in the right direction.

Saudi Arabia

According to Western media reports, Saudi Arabia is not yet fully on board. South African Foreign Minister Naledi Pandor is reported to have told Reuters that “Saudi Arabia has not yet responded to the invitation to join BRICS. It is still being considered”.

Saudi Arabia, or rather the ruling Saud family, has been an ally of the USA since the end of the Second World War, and this relationship has been further strengthened since the agreement of the ” Petrodollar” in 1974.

Since President Biden has been in power, the relationship with the USA has suffered massively, while at the same time cooperation with China and Russia has strengthened to an unprecedented level.

The problem that Saudi Arabia now has is the gigantic investments that the state and private individuals have made, particularly in the USA and the UK. Government investments in the USA alone amount to over USD 35 billion and investments in the UK are said to be around USD 75 billion. Due to the geopolitical situation in the world and the West’s aggressive sanctions policy, the concerns of Saudi Arabia that these investments could be confiscated in the event of a BRICS accession are definitely justified. As Saudi Arabia is important to BRICS and China has overtaken the US as Saudi Arabia’s largest trading partner, we expect Saudi Arabia to join BRICS as soon as China might make commitments to the Saudis in the event of Western expropriation.

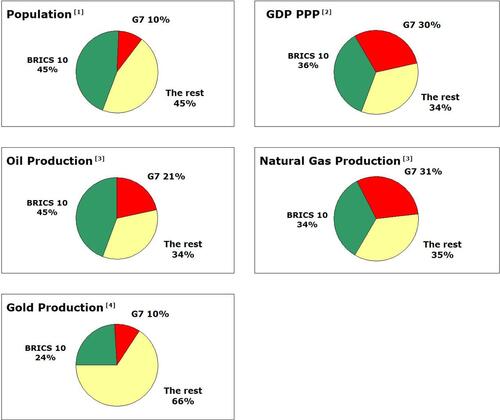

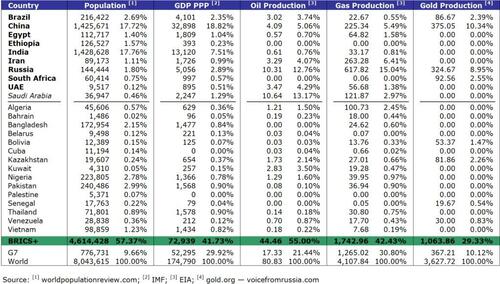

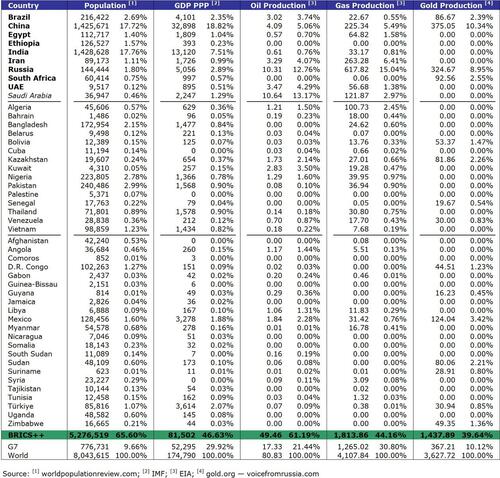

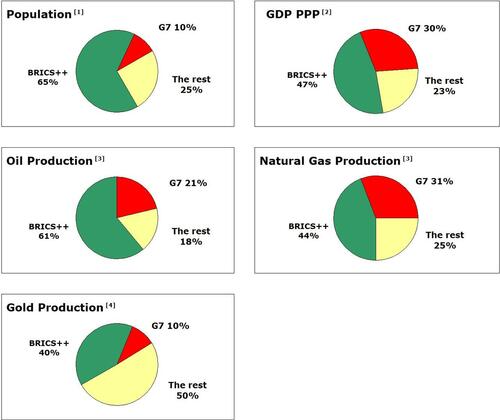

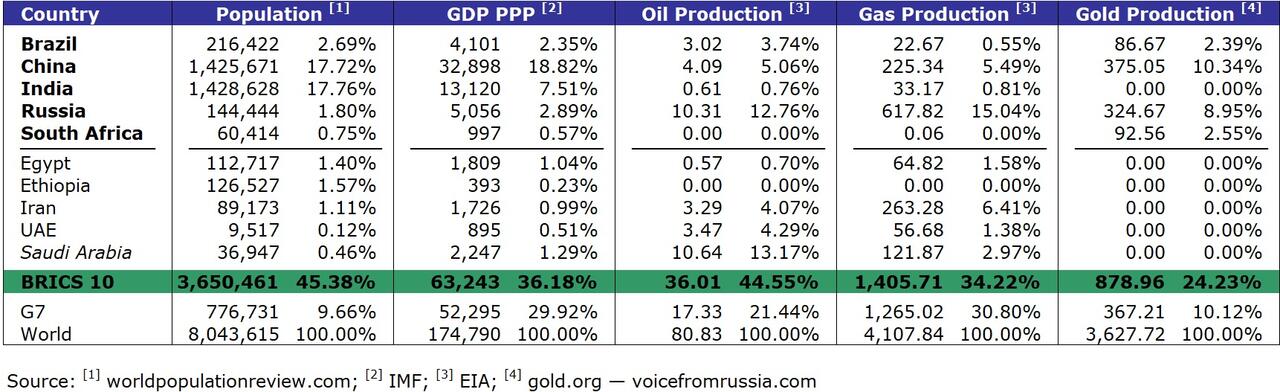

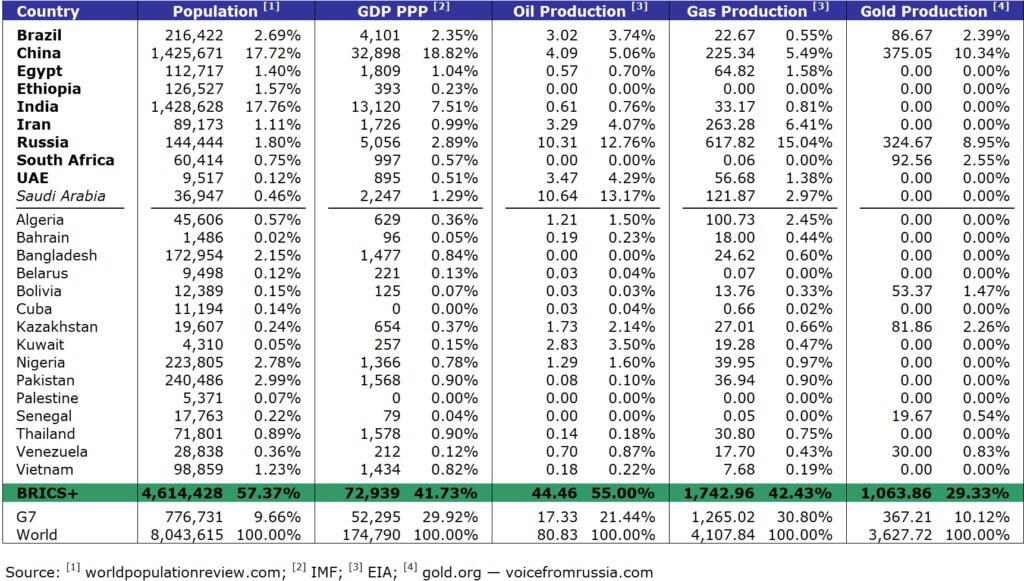

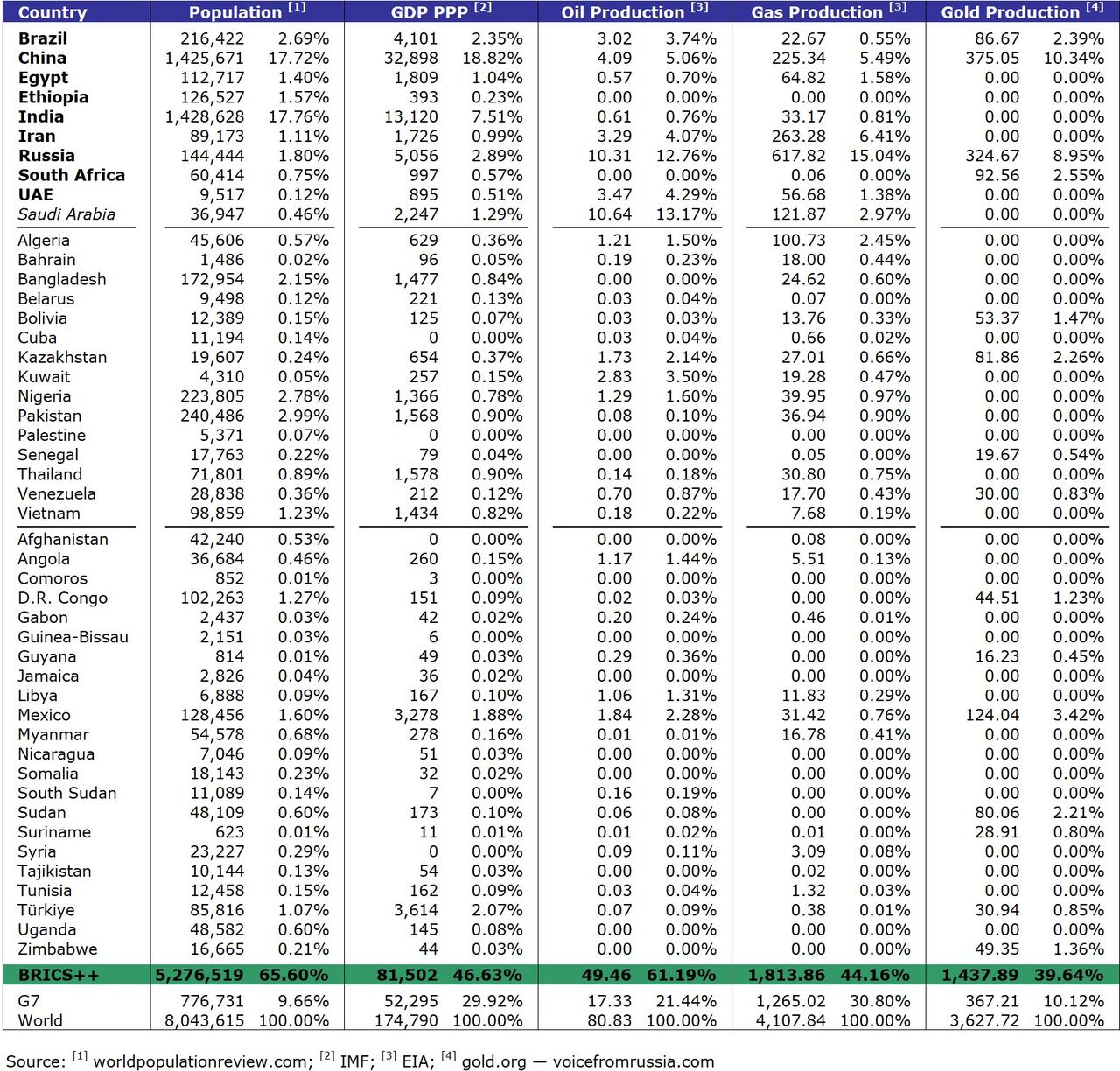

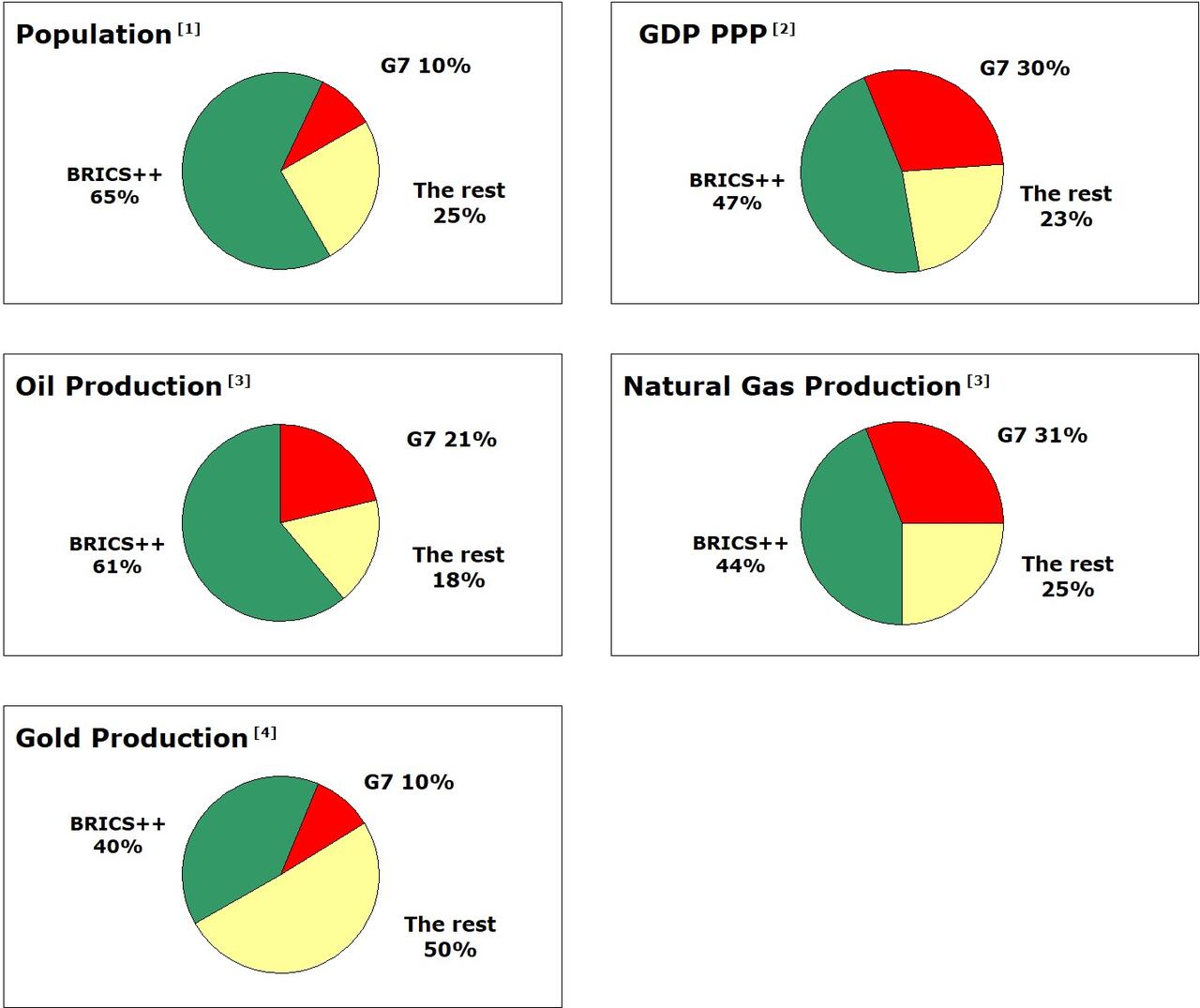

BRICS-10 in numbers

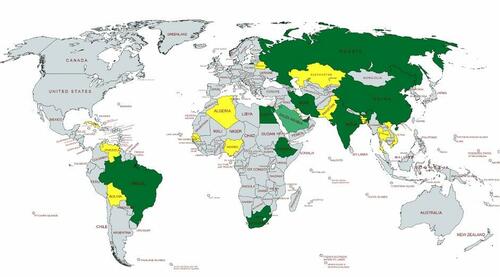

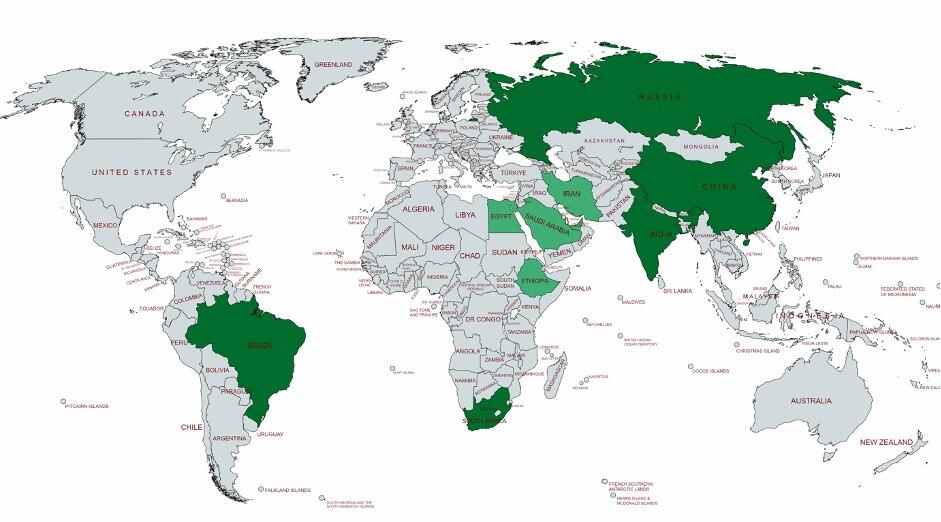

Map

Dark green BRICS until August 2023 – light green – the new BRICS members – Source: VoicefromRussia

Numbers

In our figures, we compare the BRICS-10 with the G7 and the world as a whole to give you a feel for the ratios. The parameters we use are population, GDP (adjusted for purchasing power), oil production, gas production and gold production.

We show the gross national product adjusted for purchasing power. If you use the US dollar as a measure of GDP, the economic power of a country is distorted: if you want to measure financial strength realistically, it makes a big difference whether, for example, a Big Mac in US dollars costs twice as much in one place as elsewhere. The so-called Big Mac Index is reason enough to use purchasing power-adjusted figures when comparing GDP figures. The reason why Western media use the unadjusted figures is pure marketing to disguise the devaluation of the US dollar and make it appear stronger than it is.

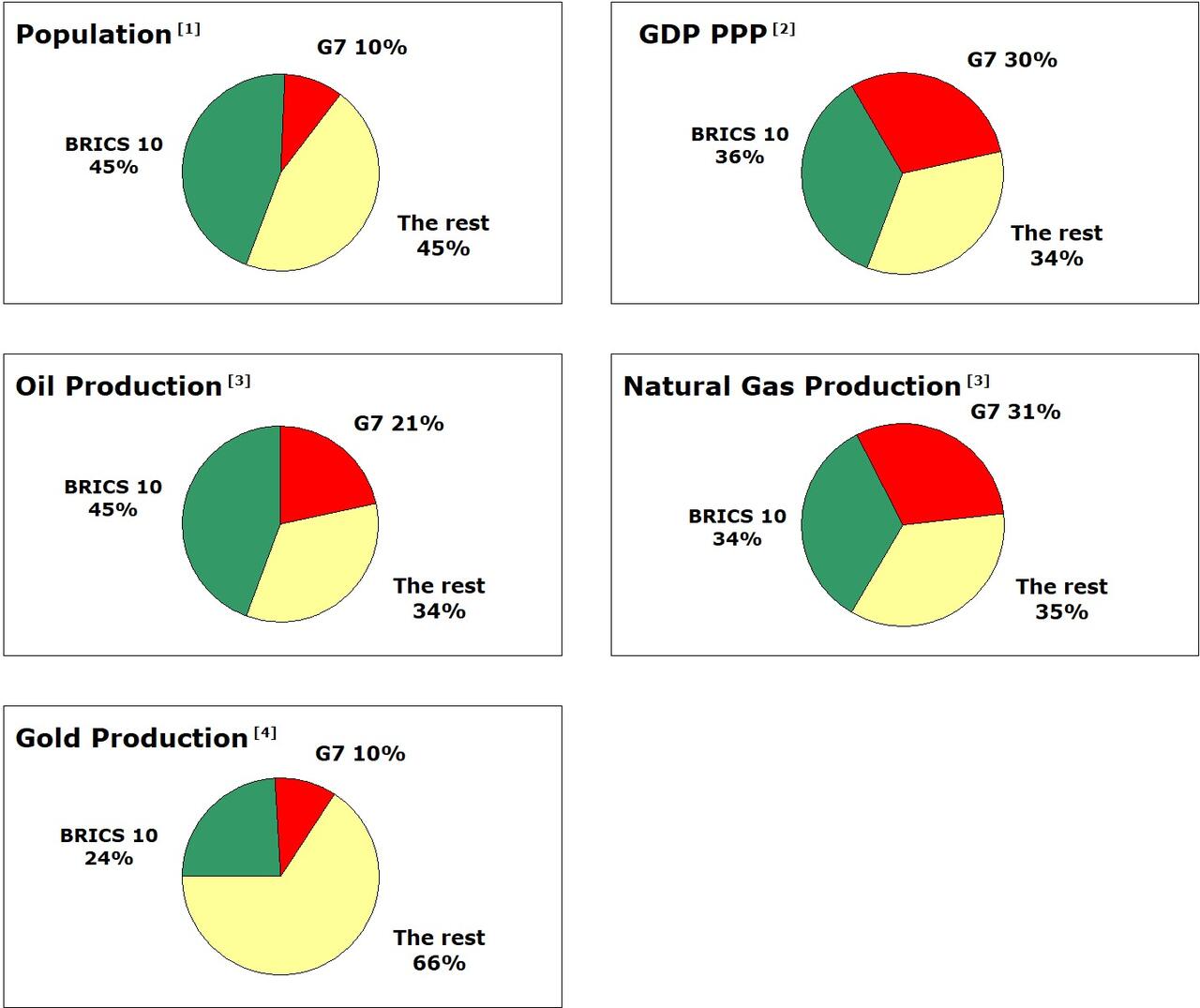

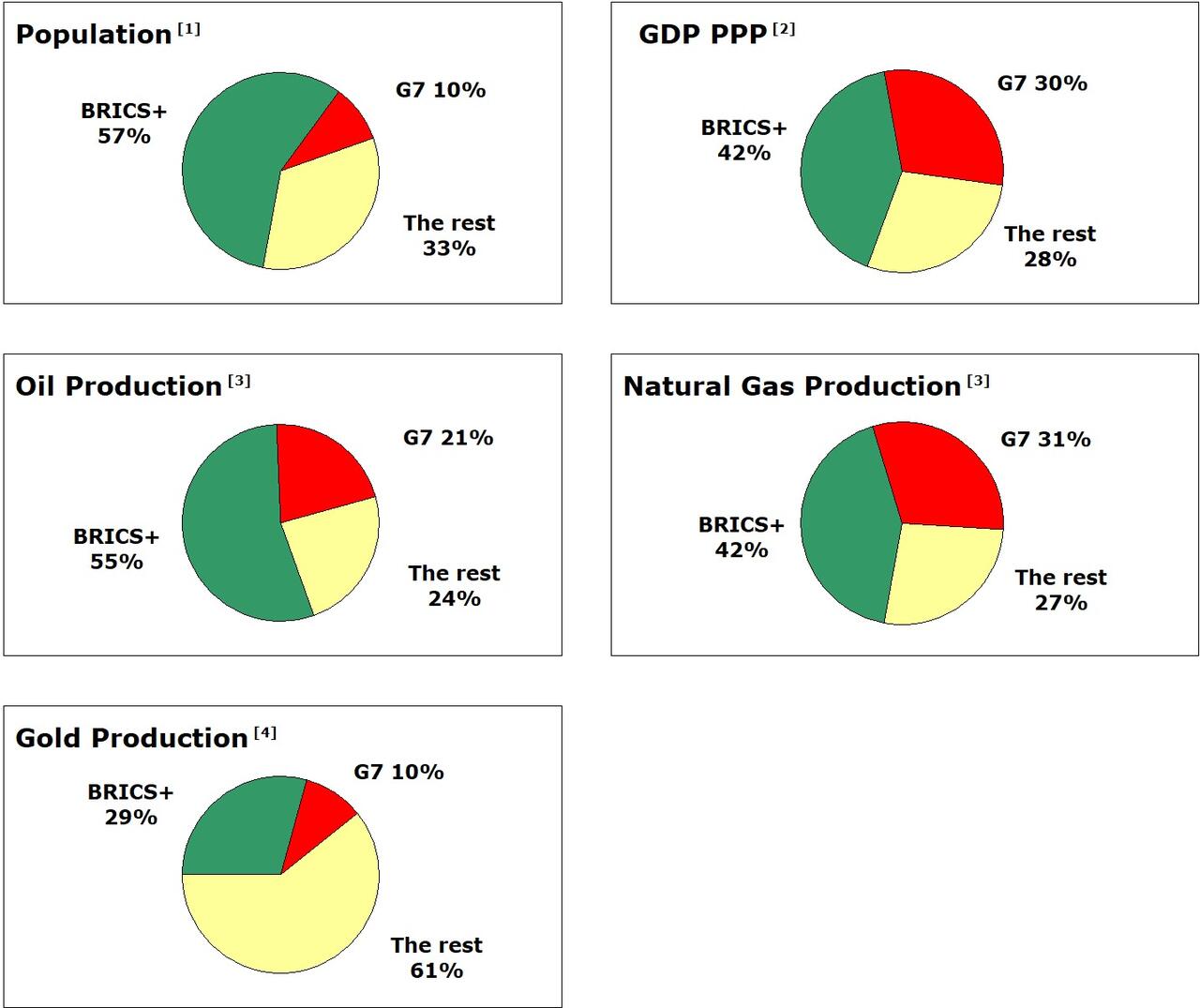

Charts

Graphical representation of the figures – Source: VoicefromRussia.

Interim result

All factors show that the BRICS 10 far outstrip the G7 and it seems incomprehensible that the West is simply suppressing this fact. A look beneath the surface reveals facts that reinforce the impression of the bare figures.

Assessment of these figures

Oil production

The following additional facts should be taken into consideration when evaluating the oil production figures:

Firstly, although the USA is still the largest oil producer in the world, accounting for around 18% of global production, it also consumes the most oil, with a share of over 20%. This means that the USA is currently not even able to cover its own consumption. This fact alone is a compelling reason for the US to pressure Saudi Arabia not to join BRICS.

Secondly, the major oil-producing members of BRICS have a great deal of influence or even control over OPEC. As BRICS thus also controls OPEC and therefore controls the price and distribution of a large proportion of oil, BRICS can be said to have an (indirect) monopoly position.

Thirdly, the production costs for US oil are around 2.5 times higher than the production costs for Saudi oil.

These factors therefore further strengthen the BRICS’ position of power with regard to oil.

Natural gas

With regard to natural gas, it should be noted that with Iran’s accession to BRICS, the two largest natural gas producers in the world are joint members of BRICS: Russia and Iran.

The largest non-BRICS gas producer is Qatar, which is (still) allied with the USA. BRICS is therefore also a real center of power when it comes to natural gas.

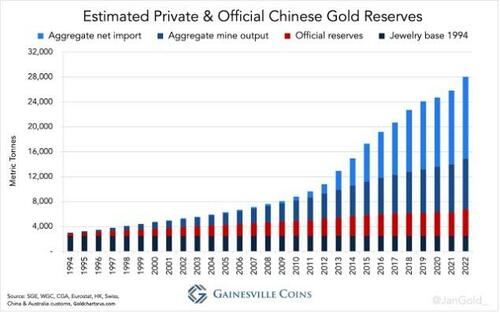

Gold

With regard to gold, it should be briefly mentioned that China and Russia are number 1 and 2 in global gold production respectively. I mention gold here because there is a good chance that gold will again play an important role in future monetary systems at some point – more on this below.

Russia holds the BRICS chairmanship in 2024

Over 220 BRICS conferences will be held in Russia over the course of 2024. The topics are diverse: science, high technology, healthcare, environmental protection, culture, sport, youth exchange and civil society.

President Putin’s statements at the beginning of the year at the opening event of BRICS 2024 in Moscow were interesting. He mentioned several times the closer cooperation between the members on security issues. It seems that BRICS will therefore not only focus on economic aspects, but also on security-related aspects more and more. The apparent coordination of the BRICS states in connection with the Middle East conflict at the UN in New York clearly indicates close cooperation on non-economic issues.

Various non-official sources have reported that the SCO (Shanghai Cooperation Organization) is moving closer to BRICS and may even merge with it. In addition to China, India, Kazakhstan, Kyrgyzstan, Pakistan, Russia, Tajikistan and Uzbekistan, Iran has also been a member of the SCO since July 2023.

This is extremely important due to the heightened geopolitical tensions and the two major conflicts in Ukraine and the Middle East. If these two organizations were to merge, there would be a new counterweight to NATO. NATO is already increasingly being characterized by experts as a mere chattering club, particularly due to its performance in the Ukraine conflict, which was not a success. As a result, NATO has almost lost its threatening potential. If the BRICS-SCO merger becomes a reality, NATO would finally degenerate into an empty shell.

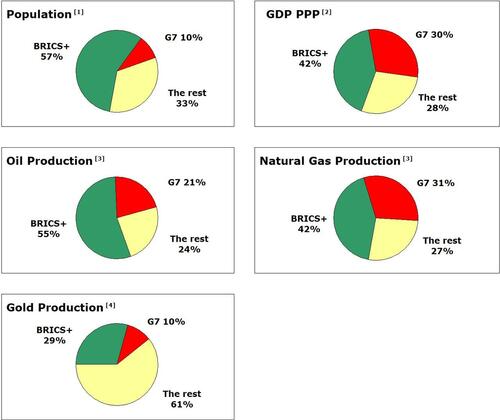

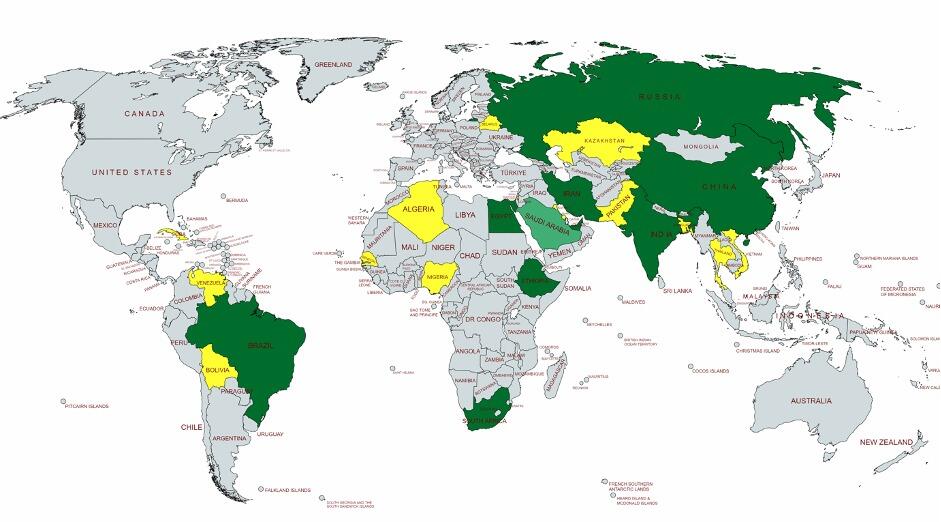

Formal applications for admission – BRICS+

Candidates

Algeria, Bahrain, Bangladesh, Bolivia, Kazakhstan, Cuba, Kuwait, Nigeria, Pakistan, Palestine, Senegal, Thailand, Venezuela, Vietnam and Belarus have formally applied for membership.

Green: BRICS 10 (light green Saudi Arabia) – Yellow: formal membership applications

Figures

Charts

Assessment

It should be noted in this list that the formal applicants will probably not all be admitted in 2024. This illustration shows the maximum and the broad formal interest in this organization. The applications for admission from some countries harbor great potential for conflict with the USA.

In my opinion, the greatest potential for conflict from an American perspective is the possible accession of Mexico, Cuba and Venezuela. Mexico’s membership would be seen by the USA in the same way as the Soviet stationing of nuclear missiles in Cuba in 1962 – “enemy on the doorstep of the USA”. This is probably also the reason why it was reported on March 3 that Mexico had not submitted a formal application for membership. Fear is breathing down the necks of the Mexicans and the USA is exerting pressure in the background.

In Venezuela, the country with the world’s largest oil reserves, the US has been trying for years to overthrow President Maduro and install a puppet.

Last August, it was not enough to gain admission and the USA will do everything in its power to prevent this oil giant from joining. However, the USA has a losing hand with the Venezuelan population, as it is imposing sanctions on the beleaguered country to bring about a collapse and accepting that the Venezuelan people are suffering from hunger.

The list of formal applications for admission could therefore change considerably between now and October, when the decisions on who will be invited to Kazan are made. What is certain, however, is that the G7 – especially the United States – is devoting huge energies to slowing down the development of BRICS. In my opinion, however, this organization is already too powerful to be weakened by the West.

BRICS turns its back on the US dollar

The petrodollar – US dollar as a reserve currency

The greatest danger of this ever stronger community is to the USA. We have discussed many times that the Petrodollar is the real foundation of American supremacy and not the American armed forces.

It is of existential importance for the USA that international trade, especially commodity trade, is conducted in US dollars. We explain why.

The US dollar as a global trading currency means that practically all countries have to hold US dollars in reserve in order to be able to settle their trade invoices. This makes the US dollar a reserve currency.

However, central banks do not hold the US dollar in cash, but in US government securities in order to earn interest. This makes the world’s central banks the biggest buyers of US government securities, regardless of whether they think they are a good investment. As a result, the US can refinance its debt on terms that are not based on the strength of the US economy, but on these systemic purchases. French President Giscard d’Estaing rightly described the petrodollar in the 1970s as an “exorbitant privilege”, as it leads to the automatic refinancing of the USA.

Abuse of this exorbitant privilege

However, the USA has been abusing this privilege for decades. Whenever a country implements something that the US does not like, it is cut off from the US dollar. The US can implement this without any problems, as all US dollar transactions go through the US. The consequences for the country concerned are catastrophic, as it is effectively banned from the commodities trade.

Theft of Russian central bank reserves

However, by blocking the foreign currency reserves of the Russian central bank in March 2023, the US has overstepped the mark, because now the entire Global South is afraid to hold US dollars, as they may suffer the same fate. Although every legal expert declares that the freeze was already carried out without an international legal basis, the West is about to go one step further and prepare the confiscation. This is the unequivocal statement made by Janet Yellen on February 27:

“I also believe it is necessary and urgent for our coalition to find a way to unlock the value of these immobilized assets to support Ukraine’s continued resistance and long-term reconstruction.”

JANET YELLEN AT THE PRESS CONFERENCE BEFORE THE G20 ON FEBRUARY 27, 2024

The EU under Ms. von der Leyen and even exponents in Switzerland are preparing to put this planned raid into practice and thus not only continue to block these funds, but to steal them.

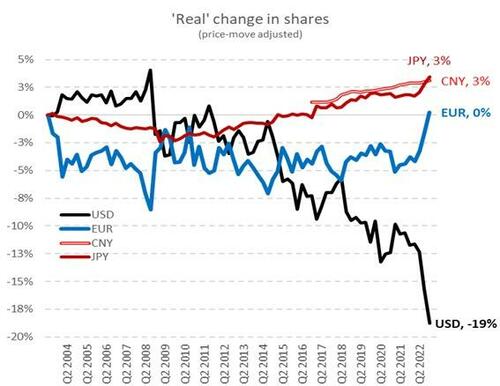

De-dollarization is already here

Until 2022, Russia conducted 80% of its trade in USD and EUR, 50% in US dollars. Today it is only 13%.

In the same period, Russia’s trade activity in roubles and yuan rose from 3% to 34% for both currencies.

These figures are clearly the result of the sanctions against Russia. However, it is a declared goal of all BRICS countries to no longer trade with each other in US dollars, but in the respective local currencies.

If you look at the current size of BRICS – 36% of global GDP – this will herald a tectonic development away from the US dollar; if you add the formal applicants, this figure rises to 42% of global GDP.

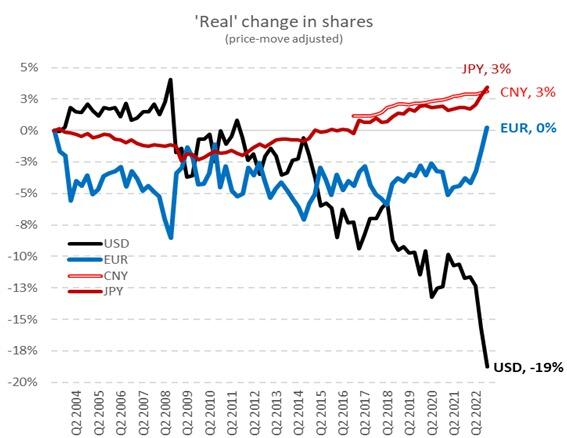

According to Bloomberg, the use of the US dollar as a reserve currency is collapsing.

Source: Bloomberg

Consequences for the US

De-dollarization poses an existential threat to the USA, as it will result in the loss of buyers of US government bonds and thus the USA’s ability to refinance its highly deficit-ridden national budget. As US government bonds are a product like any other, whose price is determined by supply and demand, a collapse in demand also leads to a collapse in the price of US government bonds. As the interest rate on bonds moves inversely to the price, the interest rate on bonds and therefore inflation will rise.

Debt in the USA is currently accelerating at an unprecedented rate. Debt currently amounts to over USD 34 trillion. It will soon take just one month to accumulate the next trillion in debt – apocalyptic. When President Reagan was in power, the total US debt amounted to less than one trillion. It therefore took just under 200 years to build up the first trillion in debt; soon this amount of debt will be a reality within a month.

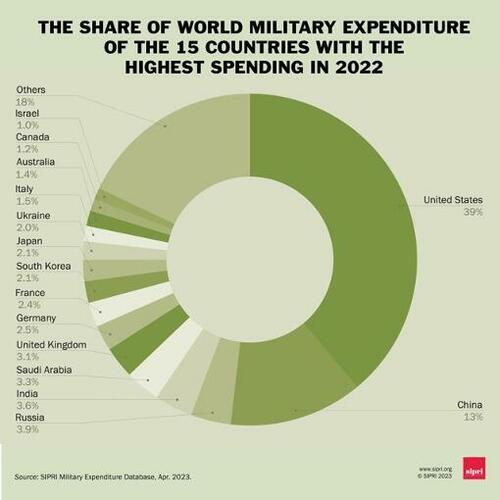

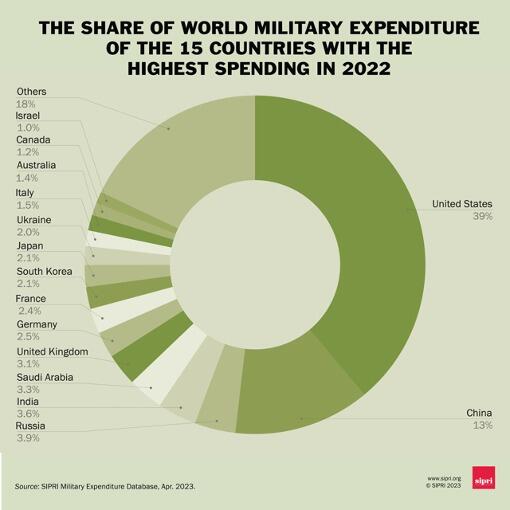

One of the reasons for this is that the USA will already have to pay one trillion US dollars (1,000,000,000,000) in interest payments on its own debt this year alone. This is more than the USA spends on its entire military expenditure, which is gigantic in itself, as the USA spends more money on its military than the next 13 countries combined.

Source: Wikipedia

If the willingness of the countries of the Global South, and in particular the BRICS members, to buy decreases, the USA will sooner or later find itself in an existentially dangerous situation.

BRICS’ own currency

Trading currency

There is a lot of talk about a new currency that would serve as a payment and financing instrument for the BRICS. There were voices – including James Rickards – who were convinced last August that a BRICS single currency would be created as early as 2023. We were skeptical about this timing and took the view that it would take longer, and we were right. However, this does not mean that James Rickards was wrong, he was just a little early.

We have seen above that the BRICS countries are in fact hardly using the US dollar among themselves any more, instead using their local currencies.

Use of local currencies

The consequence of this is that the BRICS members accumulate currencies of their trading partners over the course of a trading year if they sell more goods than they buy. Example: Russia and India use Roubles and Rupees in their trade. Since Russia sells more to India (especially raw materials) than India sells to Russia, the Russians are sitting on large amounts of Rupees at the end of the year. This problem arises regularly throughout the BRICS region among the various members in bilateral trade when deficits or surpluses build up.

Settlement with gold

I believe that the bilateral use of national currencies will continue for the time being, but that the first step will be to look for a mechanism to balance these surpluses or deficits at the end of a trading year.

Gold is an obvious choice here, not gold calculated in US dollars, Rupees or Roubles, but gold in units of weight. The trade differences at the end of a year or month would be settled in gold (kg or tons). Whether in this case the gold is actually physically delivered or merely recorded in a ledger depends on the trust between the parties. I also assume that in such a case, gold warehouses would be opened in various locations in the BRICS region, where the member countries would store their gold and their holdings would be confirmed by a BRICS auditing company.

A final issue would then be to determine the exchange rate of the local currencies. This seems to be one of the major sticking points so far.

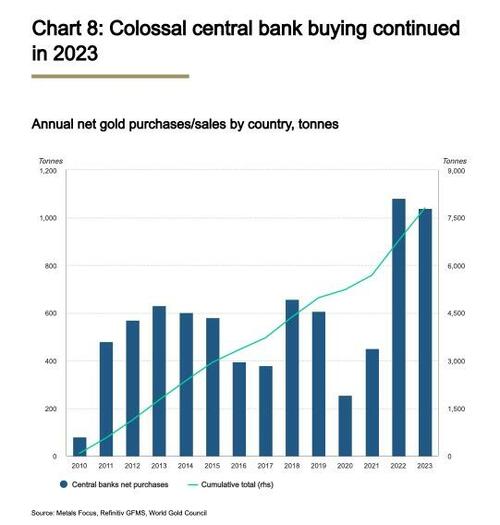

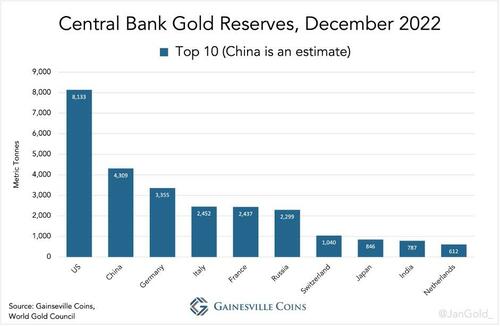

Indications that the trend is towards gold

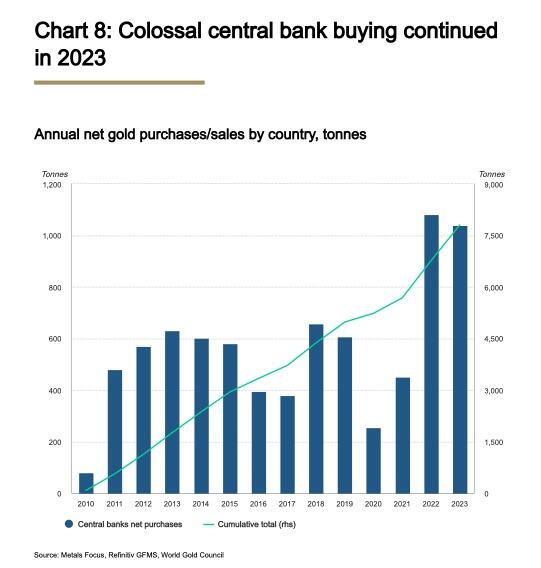

Evidence always comes from the facts. The world produces around 3,000 tons of gold per year.

According to the World Gold Council, central banks have been net buyers of gold since 2010 and the trend in gold purchases has increased steadily in recent years.

The Chinese bought the most gold (225 tons).

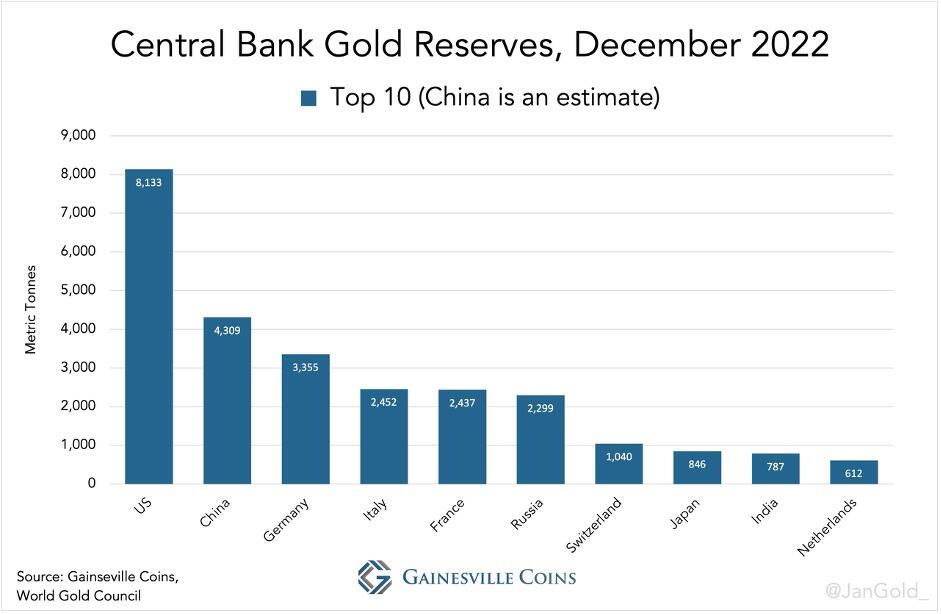

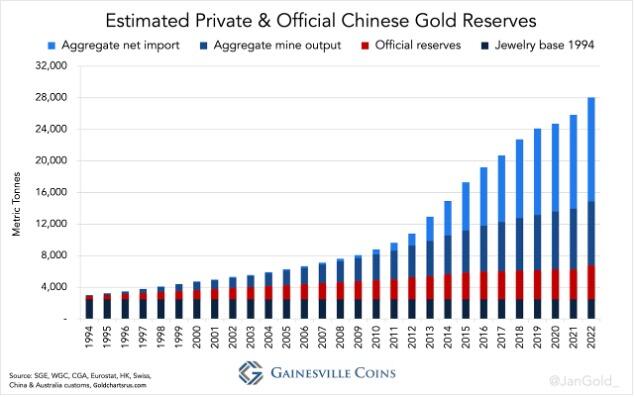

Caution is advised with regard to the official reported gold reserves.

It is very possible – and in my opinion probable – that the gold reserves of China and Russia are much larger than officially reported.

It is clear that central banks are buying more gold than they have since the 1960s. This is an indication that they are not only arming themselves against inflation, but also for the settlement of commodities.

It will be interesting to see what exactly will happen this year, but I assume that at the next BRICS summit, which will take place in Kazan in October, announcements will be made that will surprise the West. In addition to new members, I believe that a trade clearing system as described above or even more is within the realm of possibility.

Future of BRICS – many new members

Preliminary remarks

Looking to the future, BRICS has the potential to unite many countries of the Global South and completely eclipse the Collective West.

We have compiled the data of those countries that are interested in joining. This is for the future, but in times of geopolitical tensions and military conflicts, history teaches us that a lot can happen in a short time, especially after decades, without major changes. For this reason, we are merely providing a framework below and are not making any predictions regarding the timeline, but rather letting the figures speak for themselves and refraining from commenting at this stage.

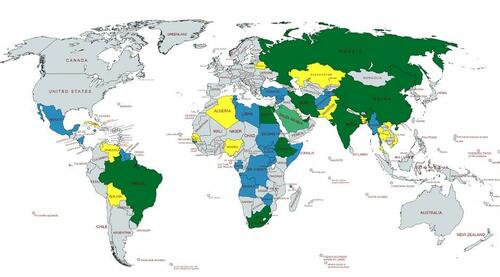

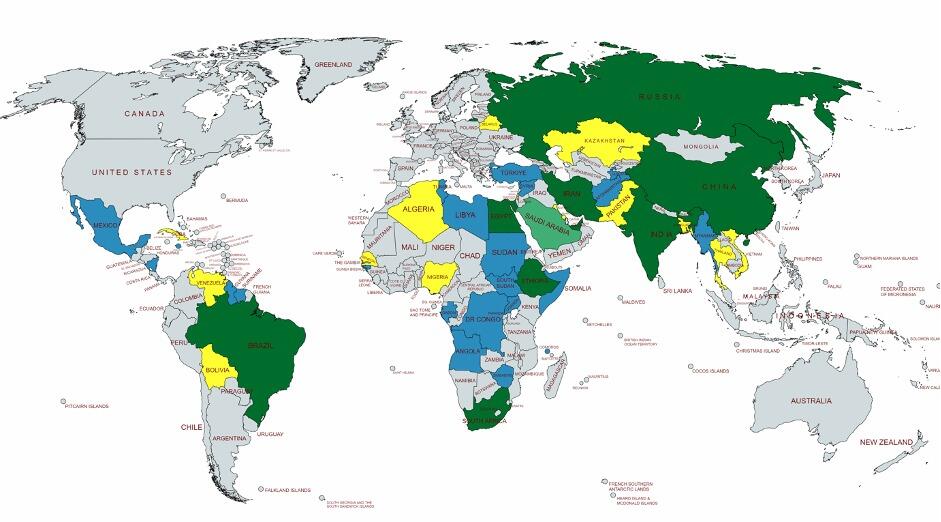

Map

Green: BRICS 10 – Yellow: formal requests for membership – Blue: countries that show interest

Numbers

Charts

Conclusion

After BRICS became BRICS-10 last August by doubling its membership and thus far outstripping the previous economic colossus G7, the current year is set to continue in giant strides. The gap to the G7 will definitely widen further at the BRICS summit in Kazan. It is still uncertain which of the formal applicants will actually be invited and thus become new members on January 1, 2025.

In my opinion, however, one thing is already a fact: the hegemony of the USA will come to an end as a result of de-dollarization. The combination of astronomical debts, rampant new borrowing and the fact that more and more countries in the Global South are turning away from the US dollar is accelerating the demise of the hegemon that ascended to the throne in 1945 and is increasingly harming itself through its aggressive geopolitics.

No world power has ever left voluntarily and peacefully. The aggressive stance of the USA towards Russia and China and its adherence to the alliance with Israel are de facto proof of the aggressive behavior of the sick hegemon.

This attitude could lead to a war between Russia and NATO in Ukraine, where a local conflict is still taking place, all the more so as the Americans have so far been on the way to inciting France, Great Britain and Germany to wage war against the giant empire.

In the Middle East, the attitude is downright perverse. In order not to alienate the Jewish lobbies in the USA, which traditionally have a major influence on presidential elections, the USA is supporting a genocide that has been clearly designated as such by the International Court of Justice. In addition to purely electoral considerations in the USA, the USA also supports Israel in order not to lose its last power base in the Middle East. These two ends obviously justify the means – and the means is genocide. The Israeli attack on Hezbollah in Lebanon has already begun and so there is ever less in the way of a burning Middle East.

Finally, they are also trying to provoke a conflict over Taiwan – a conflict that would be fought between Chinese and would therefore be a civil war. China’s intention to reach a diplomatic agreement with Taiwan in the next 20 to 30 years – that was the plan – is in jeopardy due to Washington’s aggressive stance.

The behavior of the US is unfortunately typical – the downfall is predetermined, the facts and figures in this article prove it. Whether the smouldering fires already blazing in American society will bring about a change and whether they will be aggressive or more balanced cannot yet be guessed. We will have to wait for the presidential elections in the USA, but a lot can still happen between now and November.

For a geopolitician, the world could hardly be more exciting – but for humanity, a little less tension and pressure would be a blessing. After all, people under pressure, especially politicians, have a tendency to make big mistakes.

Tyler Durden

Fri, 04/19/2024 - 02:00

President Joe Biden speaks during a campaign event at Martin Luther King Recreation Center in Philadelphia, Penn., on April 18, 2024. (Drew Hallowell/Getty Images)

President Joe Biden speaks during a campaign event at Martin Luther King Recreation Center in Philadelphia, Penn., on April 18, 2024. (Drew Hallowell/Getty Images)

Former President Donald Trump gestures as he returns from a recess in his trial for allegedly covering up hush money payments linked to extramarital affairs, at Manhattan Criminal Court in New York City on April 18, 2024. (Brendan McDermid/Pool/AFP via Getty Images)

Former President Donald Trump gestures as he returns from a recess in his trial for allegedly covering up hush money payments linked to extramarital affairs, at Manhattan Criminal Court in New York City on April 18, 2024. (Brendan McDermid/Pool/AFP via Getty Images){kind=link}

Recent comments