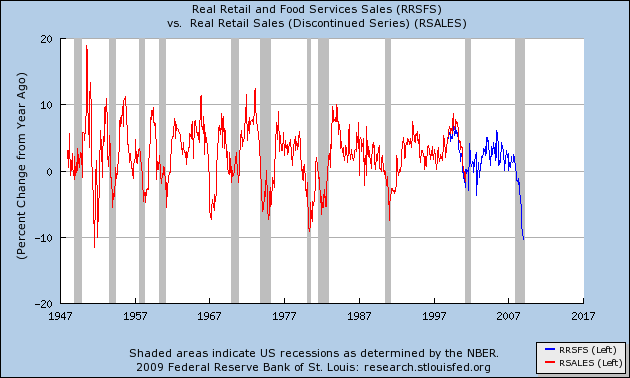

We all know by now that the economy is cliff-diving. Many bloggers can ably describe the dive in progress. One of the distinguishing things I have been trying to do over the last year is to look ahead to determine, "Where is the bottom of the cliff, and When do we get there?" Unlike most recessions, which might be described as bungee-jumps, where you get to the bottom and rebound quickly, this recession heralds a secular change, as housing and financial bubbles burst. In those circumstances, typically there is a crash or cliff-diving stage (also described by Russ Winter as the "guillotine" phase) followed by a slower, more sideways, grinding stage (described by Russ Winter as the "sandpaper" stage). Or, as I've described it many times, a Slow Motion Bust.

A more visual depiction of such crashes is to liken them to going over the American falls. First there is the free-fall, then the bouncing to the bottom of the rubble. For example, in my last blog, I noted how new home sales almost had to be nearing the bottom of the cliff. Or, visually:

might be wearing off somewhat. Like Freddy Kreuger, Michael Myers, or Jason Voorhees, it appears that American consumer simply refuses to stay dead, but instead is rising, zombie-like, from the grave to spend another day.

might be wearing off somewhat. Like Freddy Kreuger, Michael Myers, or Jason Voorhees, it appears that American consumer simply refuses to stay dead, but instead is rising, zombie-like, from the grave to spend another day. Despite the perfectly correct mantra that new home sales continued to cliff-dive, and that, as my friend Bonddad said not once but Twice(!) yesterday,

Despite the perfectly correct mantra that new home sales continued to cliff-dive, and that, as my friend Bonddad said not once but Twice(!) yesterday,

Recent comments