AIG's Joe Cassano - An American Tragedy

By Numerian

What’s a capitalist to do when he loses $500 billion and almost single-handedly destroys the global economy? In Japan you would bow deeply in public and express the deepest possible remorse and shame, that is if you already had not committed seppuku. In America, where the Ayn Rand ethos of objectivism reigns supreme, you weasel your way out of any explanation or regret, while riding off in the sunset with your undeserved fortune.

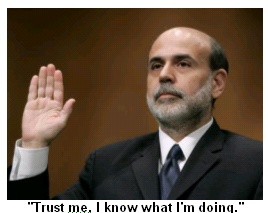

Joe Cassano, former CEO of AIG Financial Products, could have chosen the Ronald Reagan Alzheimers defense: “I have forgotten everything that happened.” That was the route taken by AIG Chief Risk Officer Robert Lewis, when he along with Cassano appeared yesterday before the Financial Crisis Inquiry Commission. Lewis, unlike Reagan, had to act like he actually had Alzheimers to make this defense plausible.

Cassano could have used the “I was too dumb to know what I was doing” defense, which would have at least have been plausible. Instead he chose to brazen it out in front of the Commission, arguing that everything he did was perfectly correct and legal, and any losses were the fault of somebody else.

We know everything he did was perfectly legal, because both the SEC and the FBI have dropped any plans to charge Cassano with criminal activity, which was one reason he was able to appear before the Commission and be so openly unrepentant for what happened. We also know that nothing he did was correct, which even a cursory reading of the public record will reveal. Cassano built an untenable portfolio of credit default swaps, selling these insurance contracts to banks around the world anxious to protect themselves if the US housing market tanked. He earned billions in fees for AIG and $300 million in bonuses for himself, but when the housing market did indeed tank, his losses totaled half a trillion dollars and destroyed AIG in the process. AIG was taken into the bosom of the US Treasury, and the American taxpayer made good all the losses the banks would have experienced had AIG been thrown into the bankruptcy courts.

Chances are if you are a typical American consumer you have purchased something made by Foxconn Technology Group. This giant Taiwanese-owned company is under contract to make Sony’s Playstation, the Xbox 360, the Wii, motherboards for Intel, routers for Cisco, and Apple’s iPhone, iPod, and iPad. As profitable as Foxconn is, it is in a fundamental sense a failure of capitalism. At a time when machine tools and robotics are available to make these products at high speeds, Foxconn uses manual labor to craft tens of thousands of electronic devices each hour, 24 hours a day. (

Chances are if you are a typical American consumer you have purchased something made by Foxconn Technology Group. This giant Taiwanese-owned company is under contract to make Sony’s Playstation, the Xbox 360, the Wii, motherboards for Intel, routers for Cisco, and Apple’s iPhone, iPod, and iPad. As profitable as Foxconn is, it is in a fundamental sense a failure of capitalism. At a time when machine tools and robotics are available to make these products at high speeds, Foxconn uses manual labor to craft tens of thousands of electronic devices each hour, 24 hours a day. (

Recent comments