More quantitative easing is here. The Federal Reserve will increase purchases of mortgage-backed securities and agency debt by $340 billion by December 31st, 2012. From the FOMC statement:

The Committee agreed today to increase policy accommodation by purchasing additional agency mortgage-backed securities at a pace of $40 billion per month.

The Committee also will continue through the end of the year its program to extend the average maturity of its holdings of securities as announced in June, and it is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities. These actions, which together will increase the Committee’s holdings of longer-term securities by about $85 billion each month through the end of the year

More astounding is the promise to continue to make MBS purchases until the employment rate is acceptable.

If the outlook for the labor market does not improve substantially, the Committee will continue its purchases of agency mortgage-backed securities, undertake additional asset purchases, and employ its other policy tools as appropriate until such improvement is achieved in a context of price stability. In determining the size, pace, and composition of its asset purchases, the Committee will, as always, take appropriate account of the likely efficacy and costs of such purchases.

Anyone find these economic stimulus packages put out by the government and the Federal Reserve ridiculous at this point? The reality is a direct jobs program would be much cheaper and much more effective to get the economy moving. Yet, magically that idea has been dismissed and worse since 2008.

Fire in the Jackson Hole - Bombastic Stimulus Claims

Federal Reserve Chair Ben Bernanke will do more quantitative easing. That's the consensus from his Jackson Hole speech. As usual, the utterances on labor are ignored by Wall Street or in this case, used to justify Wall Street's crack addict quantitative easing fix.

The stagnation of the labor market in particular is a grave concern not only because of the enormous suffering and waste of human talent it entails, but also because persistently high levels of unemployment will wreak structural damage on our economy that could last for many years.

Taking due account of the uncertainties and limits of its policy tools, the Federal Reserve will provide additional policy accommodation as needed to promote a stronger economic recovery and sustained improvement in labor market conditions in a context of price stability.

Bernanke is justifying this action through various studies claiming quantitative easing generated jobs.

For those once again thinking they were getting their crack cocaine, quantitative easing, once again they are disappointed.

The FOMC statement showed no change in policy from the Federal Reserve. For the rest of us, the FOMC statement acknowledges our crappy economy.

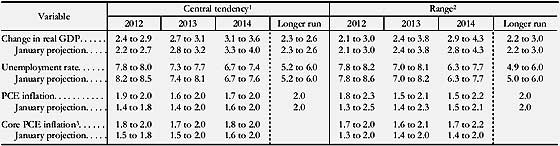

Information received since the Federal Open Market Committee met in June suggests that economic activity decelerated somewhat over the first half of this year. Growth in employment has been slow in recent months, and the unemployment rate remains elevated. Business fixed investment has continued to advance. Household spending has been rising at a somewhat slower pace than earlier in the year. Despite some further signs of improvement, the housing sector remains depressed. Inflation has declined since earlier this year, mainly reflecting lower prices of crude oil and gasoline, and longer-term inflation expectations have remained stable.

Additionally the Fed doesn't expect things to really improve:

The planets are aligning for another round of debt monetization in Europe, backed up by the United States. Mario Draghi, the president of the European Central Bank, is reportedly looking at expanding the amount of Spanish government debt he can buy. He is also said to be considering another LTRO – Long Term Refinancing Operation, which is the mechanism the central bank uses to buy debt from private sector banks.

That Spain needs help is beyond doubt. The global bond market has been fleeing Spanish government debt as rapidly as it can, forcing yields to the 7.3% area, which is beyond the point where the Spanish government can continue to pay interest from its own revenues without severely cutting back on domestic expenditures. The same situation is playing out at the local level in Spain: Andalusia and other provinces have been besieging Madrid for help in meeting the interest burden on their own debts. There is also talk that medium to small size Spanish commercial banks are out of liquid collateral, and are unable to meet further collateral calls on the global markets.

Congressman Ron Paul has been after the Federal Reserve for decades. His last great act before retirement, to audit the Fed, just passed the House of Representatives. All but one Republican voted for the bill with Democrats split down the middle. Our more corporate Democrats voted against the bill. Now the Senate has vowed to not take up the bill.

A senior Democratic Senate leadership aide said there are no plans to bring the bill up in the Senate, but didn’t rule out an attempt by Republicans to seek a vote on the measure as part of another piece of legislation. The Senate would be almost certain to defeat it given the Democratic majority in the chamber.

"This bill would instead jeopardize the Fed's independence by subjecting its decisions on interest rates and monetary policy to GAO audit," said House Minority Whip Steny Hoyer (D-Md.). "I agree with [Fed] Chairman [Ben] Bernanke that congressional review of the Fed's monetary policy decisions would be a 'nightmare scenario,' especially judging by the track record of this Congress when it comes to governing effectively.

The Federal Reserve will extend their Operation Twist past the June 2012 deadline and downgraded the economic outlook. Originally Operation Twist was $400 billion in Treasuries that were maturity dates of 3 years of less turned into T-bills with maturity dates of 6 to 30 years.

The Federal Reserve released a report, the 2010 Survey of Consumer Finances. This is a report on household wealth from 2007-2010, removing effects of inflation. No surprise, median net worth declined by 38.8% from 2007 to 2010 and is down to 1992 levels. Why this should be no surprise is due to the housing bubble and declining home values. A home is the largest asset many people have.

Federal Reserve Chair Ben Bernanke gave testimony before the Joint Economic Committee and the doves fell from the sky. Bernanke cut short Wall Street's addict like demand for more quantitative easing and instead suggested a host of policies to boost hiring and real economic output.

More-rapid gains in economic activity will be required to achieve significant further improvement in labor market conditions.

In fact, Bernanke suggested the next FOMC meeting discussion question will ask: Will there be enough growth going forward to make material progress on the unemployment rate? This is good, Bernanke realizes the #1 threat to the U.S. economy is the jobs crisis.

The Fed Chair also warned on the ongoing sovereign debt crisis in the Eurozone:

Welcome to the weekly roundup of great articles, facts and figures. These are the weekly finds that made our eyes pop.

53.6% of New College Grads are Jobless or Underemployed in 2011

Dr. Andrew Sum crunched the numbers and for those graduating from college with a Bachelors we have some startling news. A whopping 53.6% of those under the age of 25 who have a college degree are either unemployed or unable to land a job in a field associated with their college major. Associated Press:

More quantitative easing is here. The Federal Reserve will increase purchases of mortgage-backed securities and agency debt by $340 billion by December 31st, 2012. From the

More quantitative easing is here. The Federal Reserve will increase purchases of mortgage-backed securities and agency debt by $340 billion by December 31st, 2012. From the  Anyone find these economic stimulus packages put out by the government and the Federal Reserve ridiculous at this point? The reality is a direct jobs program would be much cheaper and much more effective to get the economy moving. Yet, magically that idea has been dismissed and worse since 2008.

Anyone find these economic stimulus packages put out by the government and the Federal Reserve ridiculous at this point? The reality is a direct jobs program would be much cheaper and much more effective to get the economy moving. Yet, magically that idea has been dismissed and worse since 2008.  For those once again thinking they were getting their crack cocaine,

For those once again thinking they were getting their crack cocaine,  The planets are aligning for another round of debt monetization in Europe, backed up by the United States. Mario Draghi, the president of the European Central Bank, is reportedly looking at expanding the amount of Spanish government debt he can buy. He is also said to be considering another LTRO – Long Term Refinancing Operation, which is the mechanism the central bank uses to buy debt from private sector banks.

The planets are aligning for another round of debt monetization in Europe, backed up by the United States. Mario Draghi, the president of the European Central Bank, is reportedly looking at expanding the amount of Spanish government debt he can buy. He is also said to be considering another LTRO – Long Term Refinancing Operation, which is the mechanism the central bank uses to buy debt from private sector banks. Congressman Ron Paul has been after the Federal Reserve for decades. His last great act before retirement, to audit the Fed, just

Congressman Ron Paul has been after the Federal Reserve for decades. His last great act before retirement, to audit the Fed, just  The Federal Reserve will

The Federal Reserve will  Welcome to the weekly roundup of great articles, facts and figures. These are the weekly finds that made our eyes pop.

Welcome to the weekly roundup of great articles, facts and figures. These are the weekly finds that made our eyes pop.

Recent comments