We all know the story of the three little pigs and the big, bad wolf.

We all know the story of the three little pigs and the big, bad wolf.

Little pig, little pig, let me come in.

No, no, not by the hair on my chinny chin chin.

Then I'll huff, and I'll puff, and I'll blow your house in.

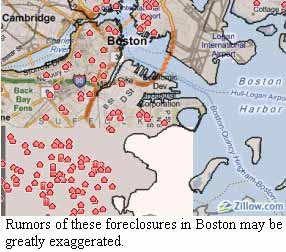

To date that's been the story of the banks as the big bad wolf, blowing houses down all over America with fraudulent foreclosures, viewing home owners as tasty piglet snacks of profit.

Will we ever see role reversal in this never ending grim tale? Will the big bad wolf finally be our government, blowing down the Banks' house of mortgage and foreclosure fraud? Can the government at least hand Americans just a few bricks at least? It's yet to be seen.

The latest seems to be dueling events. One the one hand, there is a foreclosure fraud settlement in the works for all 50 States, which supposedly gives banks immunity and waves all future legal actions. Yet at the same time, the New York Attorney General filed a civil fraud lawsuit against three major banks over MERS.

Welcome to the weekly roundup of great articles, facts and figures. These are the economic and financial finds that made our eyes pop.

Welcome to the weekly roundup of great articles, facts and figures. These are the economic and financial finds that made our eyes pop.  The

The  With much fanfare and headline buzz, Obama announced a

With much fanfare and headline buzz, Obama announced a  We have a name, HARP, for this program. Yet another mnemonic, similar to hopeless

We have a name, HARP, for this program. Yet another mnemonic, similar to hopeless

Recent comments