You may have missed it. Fannie Mae released their Q3 2011 earnings report and announced more losses due to derivatives.

Chart: The Atlantic

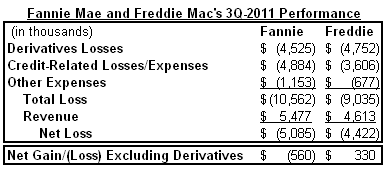

Fannie Mae (FNMA/OTC) today reported a net loss of $5.1 billion in the third quarter of 2011, compared to a net loss of $2.9 billion in the second quarter of the year. The company’s third-quarter loss was driven primarily by two factors: $4.9 billion in credit-related expenses, the substantial majority of which were related to its legacy (pre-2009) book of business; and $4.5 billion in fair value losses driven primarily by losses on risk management derivatives due to a significant decline in swap interest rates during the quarter. These losses were partially offset by $5.5 billion in net revenues.

That's right, it's bad enough we have the foreclosure, underwater mortgage and toxic mortgage backed securities mess. Now we have bad bets on interest rates, which went to record lows, and this is supposed to be paid for by taxpayers in more bail out funds. Reuters:

The government-controlled firm also attributed the deeper cash drain to losses on derivatives used to hedge its exposure to interest-rate swings and on expenses related to home loans made prior to the 2008 financial collapse. In the year-earlier quarter it had a loss of a $1.3 billion.

Mortgage backed securities are still around as well:

In the first nine months of 2011, Fannie Mae purchased or guaranteed approximately $445 billion in loans, measured by unpaid principal balance, which included approximately $51 billion in delinquent loans purchased from its single-family mortgage-backed securities (“MBS”) trusts.

Worse, Fannie Mae are asking for $7.8 billion of additional funds from the Treasury. That's us.

The Atlantic caught this derivative debacle as well and reports Freddie lost $4.8 billion, and Fannie lost $4.5 billion -- on derivatives alone.

Earlier Freddie Mac ask for $6 billion more from the Treasury. That's $9.3 billion in derivative losses in one quarter.

Meanwhile Fannie Mae and Freddie Mac are paying out bonuses and of course Congress is shaking it's rattle over that one:

Lawmakers on Wednesday ramped up efforts to block multimillion-dollar bonuses for executives at Fannie Mae (FNMA.OB) and Freddie Mac (FMCC.OB), the government-controlled mortgage finance firms that just this month have sought billions more in taxpayer-funded assistance.

Lawmakers in both chambers and in both parties have expressed shock at revelations the firms, which have been already propped up with about $169 billion in taxpayer aid, were paying out $12.79 million in bonuses for 10 executives.

How do you lose over $9.3 billion dollars by betting on interest rates? Think about how many people in the United States could get a house for free with $9.3 billion bucks. What's that joke about how many financial executives does it take to screw in a light bulb?

Hedging or gambling?

According to Daniel Indiviglio article (The Atlantic.com, 9 November 2011), losses were incurred in hedges against interest rate risk as long term interest rates declined more than Fannie and Freddie anticipated in 3Q 2011.

First comment at that article makes distinction between hedging and betting:

Second comment there analyzes events this way

All of this begs the question: "What happened to cause long-term rates to decline beyond reasonable expectation?" I associate that question with another question: "What happened in 3rd Q 2011?" As we all know, Boehner held up raising the debt ceiling to send US credit rating down for the first time in history. That would take funds out of long-term Treasurys which then ended up in insured long-term mortgages, pushing interest rates down in the housing market. This may seem illogical, since the ultimate reliance is still on the USD and the "full faith and credit" of the US government -- but think about it. If you are interested in a steady stream of dollars from your investment, you might well consider your chances better when backed by real estate than when backed by the tarnished rating of Treasurys.

I am suggesting that Fannie and Freddie were caught off guard by Boehner's chicanery, as were many other institutional investors. That's my take on this news story, but I am certainly open to criticism.

Cross-posted this comment at Daniel Indiviglio's blog at TheAtlantic.com

that' doesn't make sense

they knew the Fed promised to keep interest rates at max. low for 2 years, announced earlier. and this is become interest rates dropped, not rose that they lost.

Finally, it a beyond huge amount of money here, how can that possibly be less than what they would lose on mortgages if interest rates rose?

Trying to make sense of F & F's losses

Robert Oak,

Thanks for your reply. Considering the size of the losses, I share your doubt about the second comment (at Indiviglio's blog) that F & F "would do even worse whenever interest rates rose."

I am trying to make sense of this story myself, and I'd like to strip away at least some of the devilish details. Major questions remain about the hedging. The story is a puzzlement that could use more research -- digging deep into F & F's books -- than I will be giving it, although I am going to search around for a more detailed explanation.

As you note, F & F took losses because of falling rates, not because of rising rates. But it's unclear what that means, since no one has yet clearly stated that F & F were gambling that long-term rates would actually rise (notwithstanding assurances from the Fed). The claim may be rather that the losses were mostly because of a greater absolute drop in interest rates than F & F anticipated ("as long-term interest rates declined more in the third quarter than in the second"). It seems likely that the hedging was all about Treasurys, but Treasurys do not equate to 'derivatives'. Maybe the losses reduce to that F & F were obligated somehow to purchase Treasurys at above-market.

I am not saying that F & F made judicious calls, because obviously they didn't. All I am saying is that there is probably some connection to the 3rd Quarter budget/debt limit games. In other words, F & F may have gambled that rates would continue low as guaranteed by the Fed, but missed how low rates would drop for their index of interest (as distinguished from index of effective Treasury rates, which were rising), at least in part because they failed to anticipate the extremes reached in the budget/debt limit battles.

No one makes losses anymore

I think a more disturbing aspect is that no one seems to make a loss anymore and this determines behaviors. Does not matter how you view it....a bad investment, gambling, etc, the outcome is that there is no penalty or consequences to change behaviors. The bottom line is that any financial services investment seems to be bailed out at the taxpayers expense. The short term let alone the medium term to long term outcome of this is not a positive one (understatement).

I'd love to run a business where everyone of my actions is back stopped by the government....if I do well I make profits or if a screw up my losses are also covered.

Bad bets are being made on

Bad bets are being made on purpose as a way to transfer taxpayer money into the hands of the parties who are cashing out. Follow the money. It's more criminal racketeering. As long as we don't storm DC and New York and the private estates of the crooks and their minions (prosecutors who grant immunity to the scammers, politicians, etc), it will continue. I suppose that would be trespassing. And since were a nation of laws .....