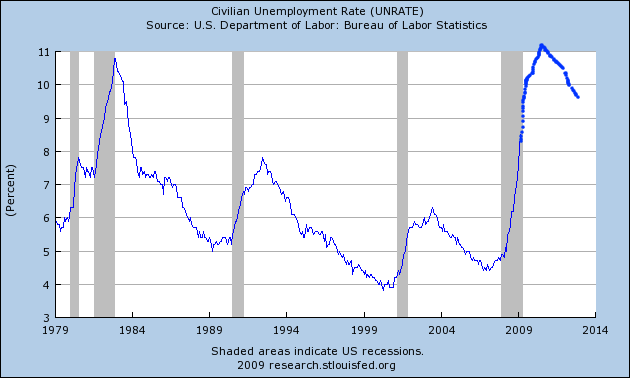

It is almost universally received wisdom that when the turn comes, we will have a "jobless recovery" where GDP turns up anemically, but unemployment stubbornly rises. Indeed the most controversial notion in some parts of the econoblogosphere is that of the "jobless recovery." as in, can it truly be a "recovery" if the number of jobless Americans continues to increase? Much moreso than dry GDP figures, wages and employment are what matter to the average American. I too have generally accepted the idea that any GDP recovery would be jobless, such that in April I made a graph showing what an unemployment spike will look like if the recession bottoms this summer, but a "jobless recovery" similar to 1991 and 2001 ensues:

This post originally began as an examination of whether trends in the leading indicator of new jobless claims could give us useful information to predict when the number of unemployed will peak -- and then took several totally unexpected turns.

Ultimately what I discovered -- and I'm not saying it will happen, only that there is a surprisingly decent case to be made that it might -- is that contrary to the accepted wisdom, the recovery from this recession may not be "jobless" at all, but particularly in its earlier portion may feature quite robust job growth. There are three separate metrics supporting such an outcome: (1) "jobless" recoveries have only happened when manufacturing hours have not slipped significantly below full time employment; (2) the steeper the inventory correction, the more robust the snap-back; and (3) pent-up consumer demand can support a very robust snap-back recovery.

Let's take the arguments in order:

I. Offshoring and Recovery: Slack manufacturing employment has in the past snapped back quickly

In the course of researching the relationship between declines in initial jobless claims and peaks in unemployment, I found that (1) in those recessions and recoveries where jobless claims fell steeply, peak unemployment occurred within 2 months of the point where jobless claims fell 12% from the peak; but (2) in those recessions and recoveries where jobless claims fell slowly, peak unemployment occurred not at the 12% mark, but only when new jobless claims were more than 16% less than peak claims, and stayed more than 16% off for at least 3 months thereafter. What was totally unexpected, was that in both the 1991 and 2001 recessions, as soon as the 16% marker was reached, the recovery in jobs stalled. Something was happening that was interfering with the hiring of more workers exactly at the point where new hiring, and plant expansion, should have kicked in. I suspected, and still do, that what was really happening was that once the economy began to pick up -- and only then -- employers took advantage of the situation not to hire more Americans, but instead to offshore jobs and plants to low wage countries.

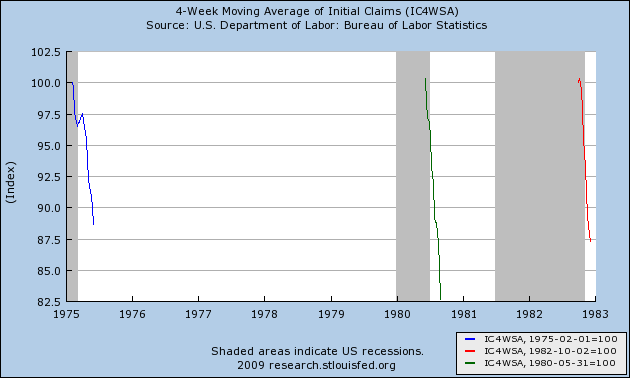

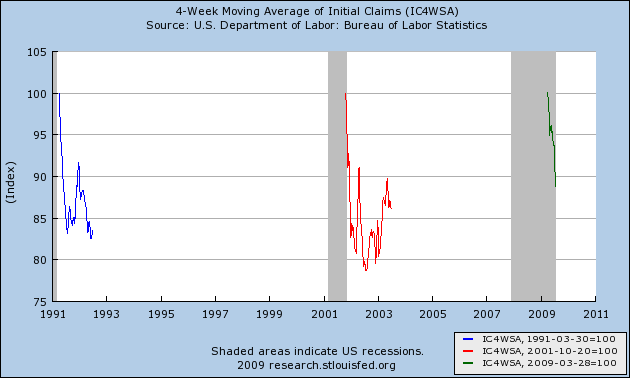

Here's the chart, showing the year, and months from the peak in initial jobless claims that they retreated 12%, 16%, and the month of peak unemployment. In the case of the two "jobless recoveries" I also show the range from peak of initial jobless claims during the time of +GDP with increasing unemployment:

| Year | Mo./-12% | Mo./-16% | Mo./peak unemployment |

range/ jobless claims |

|---|---|---|---|---|

| 1970-71 | 1/71 | 2/71 | 11/70 | n/a |

| 1974-75 | 5/75 | 7/75 | 5/75 | n/a |

| 1980 | 7/80 | 8/80 | 7/80 | n/a |

| 1982 | 10/82 | 11/82 | 12/82 | n/a |

| 1991-92 | 9/91 | 7/91, 6/92 | 6/92 | -8% to -16% |

| 2001-03 | 12/01 | 2/02, 6/03 | 6/03 | -7% to -21% |

For those who prefer visual aids, here is the graph showing the quick falloff in jobless claims until unemployment peaked in the 1974, 1980, and 1982 recessions:

and the second one showing the very long "jobless recoveries" just as the falloff hit the 16% mark at the end of the 1991 and 2001 recession, as well as the most recent data from the April 2009 high in initial jobless claims:

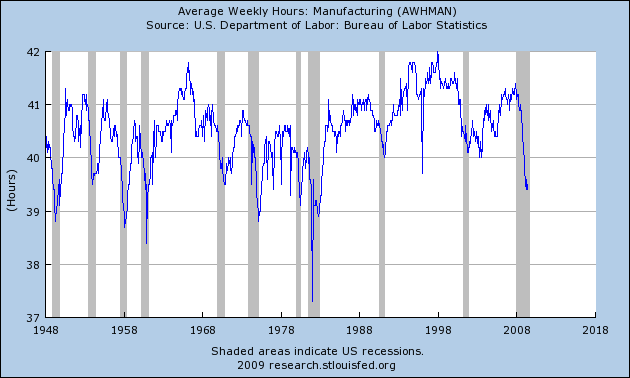

Since there is no "smoking gun" of data from manufacturers' advertising their intent to offshore jobs, I looked at one place where it might show up -- in the statistic for average weekly hours in manufacturing. In other words, rather than increase hours, employees' hours worked would be flat, as offshoring occurred instead of rehiring and expansion. What I found was more complex. Here's a graph of manufacturing hours since 1949:

In general, over that entire time period, the deeper the "V" in hours (i.e., more than a 1.5 hour decline, to a level below 39.5 hours), the quicker the snap-back in hours worked once the recession ended. (The one ambiguous case is the tepid hours recovery from the 1970 recession, during which time not only were the mass of baby boomers for the first time entering the full-time job market, but 500,000 of them were being withdrawn from Vietnam for an extra surge of workers.) In the above graph, the 1991 and 2001 recessions stand out like a sore thumb: In neither case did hours worked ever fall below 40! Once the recession ended, there was no slack to be picked up by rehiring laid off workers and increasing production at the plant. Instead, the offshoring (I hypothesize) began immediately.

Let's return to jobless claims and our current recession. Right now, 3 1/2 months after peak initial jobless claims, we are just at 12% off from the peak. Should our present rate of decline be sustained after the midsummer anomalies -- not a sure thing of course -- we will cross the 16% mark (~550,000 new claims per week) in one more more month. If we are to have a "jobless recovery", the number should quickly (with a couple of months) stall there and increase again. If, on the other hand, we will have a "V" shaped recovery, the marked decline in new unemployment claims should continue. If past patterns are prologue, then what the graph of average hours worked in manufacturing argues is that at least over a substantial period thereafter, we will have a quick snap-back in hiring as opposed to a "jobless recovery."

In addition to the pattern of recoveries from past sharp manufacturing employment slumps, there are two other reasons why a "V" shaped jobs recovery might occur.

II. Rapid inventory reduction can give rise to a rapid snap-back. Dr. James Hamilton has laid out this aspect of the case for a V Shaped Recovery. I encourage you to read the entire article, but it can be summarized as follows:

"[O]ften a sharp economic downturn is followed by an equally sharp economic recovery. One reason for that is the liquidation of inventories that accompanies any recession and restocking that takes place in recovery.

"The typical pattern is for inventory investment to fall well below trend during an economic downturn. ...[S]ince the current recession began in 2007:Q4 ... the level of inventories is lower than you would have expected in the absence of a recession by about ... 0.91% of one year's GDP. Add that restocking to the normal [ ] inventory investment that we'd expect ..., and you get a possible contribution of inventory investment of ... 1.12% of GDP during the first year of the recovery.

"If we are looking at the growth rate of real GDP, which is how we usually think about these numbers, the potential contribution of inventory investment is even more dramatic. If inventory investment goes from subtracting 0.49% from GDP (as it did over the last 4 quarters) to adding 1.12% to GDP ..., the contribution to the growth rate of real GDP would be 1.12 - -0.49 = 1.61%."

In layperson's terms, "just-in-time" inventory systems will jump start any recovery just as they accelerated the 2008 downturn. Interestingly, Dr. Hamilton supplies a chart indicating that inventory replenishing was significantly higher during the recoveries after 1974, 1980, and 1982, than it was for those after 1970, 1991, and 2001 -- in other words, correlating exactly with the graphic support from average manufacturing hours during and post recessions I laid out above in Part I.

III. This leads us to the third and final argument in favor of a "V" shaped jobs recovery: pent-up consumer demand, especially for durable goods.

In the same article above, Dr. Hamilton further notes that

"similar dynamics also apply to a number of other components of GDP. For example, recent sales levels for motor vehicle appear to be significantly below normal scrappage rates, and this is another area where a big rebound effect is quite possible."

Similarly, Calculated Risk has noted that the

"turnover ratio for the U.S. fleet [of cars] ... for January [2009] is 27 years, by far the highest ever. The actual in December was close to 24 years. This is an unsustainable level...."

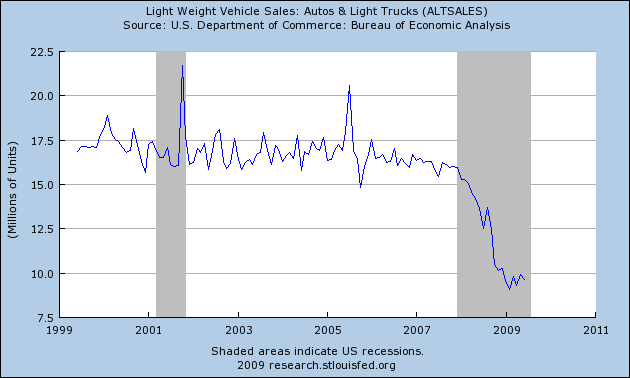

Here is the graph of auto sales for the last 10 years:

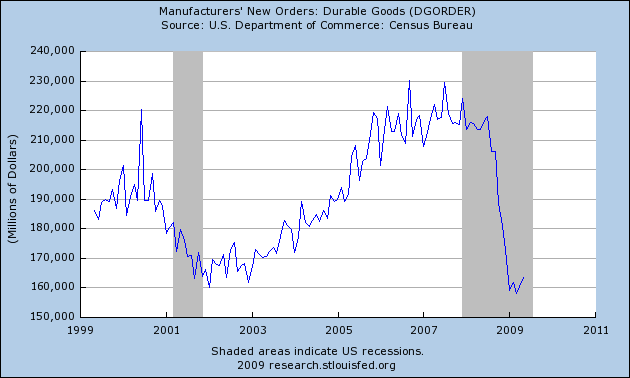

And here is the same graph for durable goods produced:

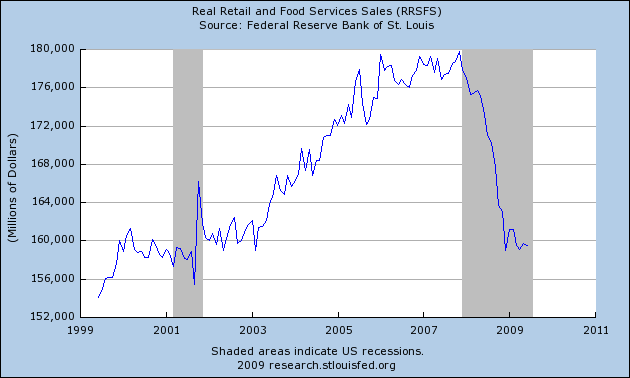

And finally for real retail sales:

You can see that auto sales have fallen from 16m to 9m, or roughly 40%. Durable goods have fallen off 30%. Retail sales in general fell over 10% in the last year. Compare that with the complete non-event of the 2001 recession.

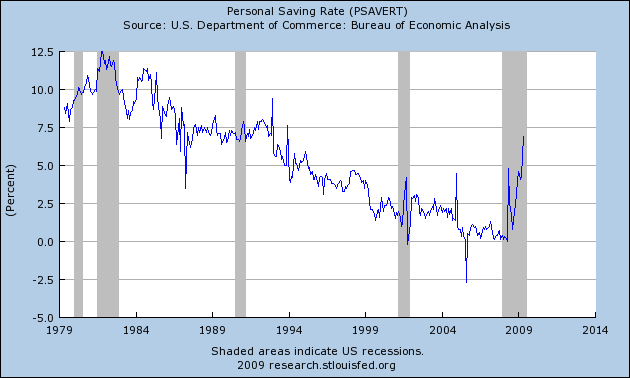

Yet, despite the steep fall in all kinds of sales, as late as April 2008, the unemployment rate was only 5%. Even with a 10% unemployment rate, that means that American consumers have roughly 94%-95% of the purchasing power from their income that they had a year ago. We know where the missing 5% has gone -- into savings, as shown by the personal savings graph below:

I pointed out in my essay, "Black September", how much of the free-fall of late last year was due to the complete destruction of confidence accomplished by Paulson, Bernanke, Bush and Congress last September, when Americans were warned that the economic world faced Armageddon in only a matter of days. What happened then was typified by this quote from a prominent auto dealer:

on about September 10, we saw our business fall off 30-35%.

As Calculated Risk said at the time, after one particularly panicky speech by George Bush,

it might motivate people that haven't been paying attention to say: "Wow, this is bad. Let's make sure our money is safe, and watch our expenditures." And that could lead to a deeper recession."

And indeed American families abruptly and severely cut spending.

As a result, while Americans as a whole only lost 5%-6% of their income, but car sales did not go down 6% -- they went down 40%! In short, fearful of losing their jobs, and fearful of the future, Americans panicked and started to save, much more in the aggregate than the immediate risks called for (because no individual or family knew if they were going to be among the ones thrown out of jobs or not). Once that fear passes -- once Americans feel confident that the economy is growing instead of contracting -- there is a 5% boost to consumer spending that is immediately available (I'm not advocating for a 0% savings rate, merely pointing out that some of that savings can in fact be released). There is no necessary reason that such a boost cannot happen very quickly. In other words, a mirror image increase in demand to the "Black September" plunge of last year cannot be ruled out.

Compare again with the 2001 recession. Consumers sailed through that recession, so there was no snap-back of increased consumer spending once it ended.

If auto sales, durable goods sales, and general retail sales begin to pick up quickly, the above discussion of manufacturing hours suggests that, unlike the jobless recoveries of 1991 and 2001, there could be a very robust rehiring of workers in the residential, auto, and other durable goods producing industries, at least until such point as plants are operating at full capacity.

Putting the three points above together, and to summarize, if there is a relatively rapid uptick in consumer demand, that coincides with relatively depleted inventories of durables and consumer goods, and factories have cut employees to the bone, then employees in all sorts of industries might be hired back quickly, causing a "V" shaped Jobs Recovery.

How will we know if a "V" shaped jobs recovery is occurring? First, I would want to see Year over Year Leading Economic Indicators turn positive. Barring another sudden downdraft, this is likely to happen no later than September. Once that happens then I suggest that 4 series -- all of which have the virtue of being released within a week after the end of the month on which they report -- will tell us pretty quickly whether we are having a "V" shaped or "jobless" recovery:

- (1) monthly nonfarm payrolls: a gain of under 50,000 a month means a jobless recovery, gains over 100,000 within 3 months support a more "V" shaped recovery.

- (2) monthly auto sales: annual sales rising less than 125,000 a month means lackluster consumer durables spending, over 200,000 supports a "V" shaped recovery.

- (3) monthly manufacturing hours worked: an average rise of only 0.1 hours per month means a lackluster increase in plant use, over 0.15 supports a "V" shaped recovery.

- (4) the ISM manufacturing index: a quick expansion of manufacturing should be supported by the index rising to at least 60.

I still believe the government should move to create a new WPA. Additionally, so long as wage growth remains weak, any recovery will not be robust in the longer term. Let me repeat that I am not saying that we will have a "V"-shaped jobs recovery -- only that a surprisingly substantial case can be made in favor of one If so, I have set forth a road map in this essay to test whether fortune might favor us.

Comments

Grasping at straws

I think you are taking a way to optimistic approach and are thus ignoring several important factors:

1) I doubt offshoring is to blame for any jobless recovery, as efficiency and automation are much more likely culprits (once a company lays people off, it quickly realizes that jobs could get done without them).

2) The savings rate is unlikely to come back down, as this move up was a reversion to the mean of the savings rate. I see the rate settling out between 6-8% for quite some time.

3) Consumer demand will not lead us into any recovery, as consumer's balance sheets are in terrible shape and they have no access to home equity and little access to credit in most cases even if they wanted to spend. Cash purchases aren't going to jumpstart anything.

My bet is that the unemployment rate stays quite elevated over the 2009-2011 period with a gradual move towards a new higher full employment rate sometime after that.

disagree, offshore outsourcing was/is EXTENSIVE

the numbers of jobs lost is in the millions, the projected losses higher.

Corporations hid the data but verified are > 500k in tech jobs (GS) and 2.5 million manufacturing jobs (EPI) from 2001-2003.

Corporations hide the data plus the DOL and Congress refused to do anything about obtaining data (and put out a very bogus report). Even with a bogus report the House Science Committee had to go to war to even get the copy (they refused to release it).

In the "reads" section of EP, go to "studies" and read Alan Blinder's estimates, it's very objective. Then Haas School U.S. Berkley estimated 14M jobs offshored by 2015, Forester Research had 3.5M in white collar jobs alone offshore outsourced.

And if you don't believe that, look at India's GDP, which is now about ~3.7% from pure labor arbitrage, that's the BPO sector, i.e. offshore outsourcing....direct job transfer.

NDD, I appreciate you offering this argument

for "V" recovery but as I have stated before this not a normal recession. Prof. Kenneth Rogoff, who I rarely agree with, has offered with Prof. Carmen Reinhart a very good comparison to past financial crises and based on these past comparisons suggest the following:

Here is part of their conclusion:

Based on comparison to past financial crises it would not be a "V" jobs recovery. Just offering this up as a point of discussion.

As for what I think, I agree with SilverOz above. If the "Great De-Leveraging" continues than we will see anemic growth certainly not enough to create enough jobs to lower unemployment.

RebelCapitalist.com - Financial Information for the Rest of Us.

Outstanding rebuttal

Your comeback is most excellent! Anyone who suggests we can look forward to any "recovery" is simply either ignoring or grossly ignorant of how the present economy is structured, along with any knowledge of the securitization and derivatives involved.

Those who use the term "Great De-Leveraging" comprehend this. We have yet to experience the coming meltdown from CLOs going south (although perhaps those missing trillions from the Fed might be involved in postponing this) from commercial real estate vacancy increases. Also, those CLOs and CFOs that private equity firms have coming due.

And lastly, I've been tracking the jobs offshoring process since I belonged to an activist group which fought against the tax break legislation (for laying off American workers and offshoring their jobs) in the latter part of the Carter Administration, and believe we've reached that critical mass point when there are simply no jobs left which can be offshored (the last bastion, the health care industry, is involved in this latest wave of jobs offshoring).

asdf

"Anyone who suggests we can look forward to any "recovery" is simply either ignoring or grossly ignorant of how the present economy is structured,"

thank you for your substantive, factual, conribution to the discussion.

FYI

ok, one element I think can reduce friction going on is keyword "recovery".

An anonymous poster (with lots of rage beyond the above I might add) suggested we need new terminology for "jobless recovery".

I think this is a good idea. But what?

EI cyclical upswing?

Macro economic data upturn?

insourcing, job creation

I basically said something similar but they still are offshore outsourcing jobs, as evidenced by the many reports. IBM being the most outrageous, 5k jobs where they told U.S. workers to keep their job they need to move to India and work for India level salaries, in one shot.

So, they are going after the high end jobs but even on in sourcing, use of guest worker Visas to further displace U.S. workers, labor arbitrage, this is going on in masse but these offshore outsourcers, those workers, who have been stealing the jobs....are also getting training experience and these countries are determined to move up the food chain...so now jobs are plain being created abroad by U.S. corporations instead of first creating them here, forcing Americans to train their replacements and then moving the jobs offshore...

It's very difficult to track too. Finding out job creation overseas by U.S. corporations and then determining if those jobs are labor arbitrage.

On the rest of the indicators, come on folks, this is beyond complex. We have the Zombie Banks, derivatives still out there, no real oversight and then we have the real economy, massive deficits, a housing sector (which I was shocked to see it was contributing > 3.5% to GDP! at one point), we have the entire consumer debt economy coming to a dry well....

so many elements, so little data so we really need to stay analytical to figure this out. I do believe we have an abby normal situation in many respects, which is why you see NDD returning to the S&L crisis as well as the Great Depression for historical data...

the problem is....this ain't the S&L crisis in terms of policy prescriptions, or the Great Depression, in terms of FDR administration policy prescriptions...

this is also in this globalization shit hole where we have wealth transfer (IMHO) going to "emerging" economies (how can China be labeled a EE????)

Thanks for the Rogoff link

I have read his paper and have a few comments:

1. He uses mean rather than median for much of the data, causing the 1929 depression to skew it somewhat. Using median would have shortened some estimates.

2. Using his unemployment metric, in the last cycle unemployment bottomed at 4.4% at the end of 2006-early 2007, which per mean data takes us to about the end of 2010 or so for the peak, consistent with a "jobless recovery." If you use the median, the peak is a few months shorter and certainly in over 1/3 of the crises, the peak was hit in 3 years or less. So a "V" jobs recovery starting by the end of this year wouldn't be an outlier.

3. I don't know why they didn't include 1938. We certainly had housing data for that recession as well, and our current downturn bears a number of resemblences to that one.

But again, thanks.

offshore outsourcing, insourcing

In the 2001 time frame, 50% of all tech workers in Silicon valley were pushed out of their careers, permanently.

In 2000, it's no surprise either we had a mass exodus of manufacturing jobs to China since the China PNTR trade agreement kicked in.

Now, in terms of offshore outsourcing, the focus is on advanced skill set jobs, i.e. R&D. The pharmaceutical companies massively fired their U.S. researchers and offshore outsourced R&D, happened in 2006 period extensively. The same is true in advanced technology.

While GM hemorrhaged money, few noticed the billions they had spent in R&D facilities, plants in India, China, Brazil.

It's so incredible, it didn't even make a blip that as Citigroup received $25 B in U.S. taxpayer funds, they signed a $2 billion offshore outsourcing deal to take to India what was left of jobs inside Citigroup. That's every single tech job that wasn't nailed down (and if anyone notices, we're having some funky stuff pop up on financial trading software now, just wait! that's only going to get worse!)

On the other hand, some corporations are seeing data come in from their "offshore outsource every division as fast as you can" internal corporate mantras/memos and are discovering it's not the "bang for the buck" they thought, productivity is much lower, the quality is lower, costs have additional layers.

That said, as we speak the outsourcers are talking with Hillary Clinton and believe me, they are after even more U.S. jobs to be traded. (Hillary has delivered for them too!)

So, I do not believe we will have a mass exodus of more jobs at this point, they already offshore outsourced them...

I think what is left of U.S. manufacturing is the unpicked fruit, left to rot on the vine.

Now they are not firing Americans, but simply starting new divisions, new plants, new research centers abroad, so those invisible "lost" jobs never come under the U.S. radar for they were never in the U.S. in the first place....

i.e. MNCs are still in the business of selling to Americans and moving Americans ability to earn a living offshore.

But that cash cow, funneling middle class income out of the country, might be a well run dry.

What we get from Obama is the same crap we heard from Clinton and Bush II, somehow Americans need education and training. It's pure bunk. There are plenty of Americans available with advanced training and skills working at Wal-mart or way below their skill levels. Also, in the past firms themselves trained workers and that is from manufacturing to PhD level training and investment.

Now corporations just want a fresh boatload of "immigrants" where all of that worker investment, i.e. education, training has been done offshore plus they want to throw workers away once a particular project or whatever is completed.

Training, education now (like many hidden expenses, i.e. retirement) is dumped onto the worker, they are supposed to pay out of pocket when it used to be the corporations cost and responsibility.

So, with that....I don't see any "V" because we do not have a housing bubble, or the ability to take on even more consumer debt to generate low paying construction and retail jobs....we do not have anything to replace the lost jobs with.

Until the Obama administration gets serious, as well as Congress about manufacturing policy, incentives for advanced manufacturing to be started in this country, for U.S. corporations to hire U.S. workers first and foremost and doing something about bad trade policy...

I hypothesize that the economy will just drivel along...

Their great green jobs are a case in point. They were immediately offshore outsourced, as I warned on EP.

IBM just as an example, should be plain banned from having any state, federal contract for they do not create local jobs....and are gutting their workforce, offshore outsourcing as fast as they can (or creating jobs in India)...G.E. also does this...

yet these sorts of companies are getting the Stimulus contracts PLUS are getting these "green jobs" initiatives.

Other countries, all over, put their workers first, U.S. policy puts U.S. workers last. We're even up for trade via Hillary Clinton.

We need much more than a WPA in other words, we need a host of policy changes and legislation, esp. focused on manufacturing, trade. We have right now VCs in Silicon valley who are more Patriotic in what they are doing than the Obama administration (and they also happen to know advanced innovation isn't something to labor arbitrage on! but even so, you can bet the manufacturing of that innovation will be offshore outsourced, i.e. fabless startup).

Sorry but the Obama administration has a day trader mentality when it comes to real economic growth.

But as much as I wish we would see a "V", I don't see anything that is going to create real jobs with real middle class income and benefits happening. Even worse, our taxpayer dollars are being used to create jobs.....offshore....so until I see some sort of activity, something, some sector that would create real job growth...

I'm a sideways "L", i.e. |________.

(note, all of this comment needs to be packed up with labor, occupational stats, graphs, i.e. what is the percentage of GDP of the housing boom, the occupational areas of jobs from 2001-2008 created, the occupational areas of jobs lost now (it's across the board last I saw but in 2008 was finance, construction, i.e. affiliated housing bubble jobs), then also how many of those jobs were held by illegal labor, guest workers, etc. who get counted along with Americans in the unemployment stats)

IF word "recovery" is used, THEN fascists cut

everything that can help us peeee-ons weather the fucking depression they created.

whether things will improve, whether things did improve, whether things are improving, how we define "improve" - there is a lot of debate over that stuff, and there has been a lot of debate over it since I started reading Time magazine when I was 10 in 1970... or before?

(btw, I haven't read the rag in decades. it is like the NYT or WAPO, once in a while I skim it to see what the lying m'therf'kers are telling me to think)

HOWEVER, as I've commented on kos in bondad's diaries, the use of the word '_ecovery' has become tied with the implementation of MORE goddam fascist policies in the last 30 years - cut this and that and anything that levels the playing field, don't fix a goddam thing systemically, and shovel MORE wealth at the fucking pigs in the front of the line.

you need a new word - you're enabling the lying fuckers by using THEIR lying ass terminology.

rmm.

Regarding Second Point.

Professor Eileen Applebaum argued that we can't rely on the inventory cycle for recovery: Link.

Her argument is that we no longer manufacture most of the goods needed to replenish inventories so we will need to turn to imports to restock inventories. Any gains from inventory may be offset by increases in imports.

Very interesting argument.

RebelCapitalist.com - Financial Information for the Rest of Us.

Good for China & India, but

not so good for US workers. Without an industrial policy that supports American manufacturing, this country will never have a strong middle class again. Without a strong middle class, there are not enough consumers for the piggish US consumer based economy to flourish. Wall Street will recover, but the rest of us will not.