Surfing around I came across this little noticed post over at the Wall Street Pit. Consumer lending hit an all time high in March . Literally I couldn't believe their graphs posted. But, it's true! Firstly, here is the Federal Reserve data release, H8: Selected Assets and Liabilities of Commercial Banks in the United States. Secondly, here are the graphs on Consumer Lending by Commercial Banks.

Check out that all time monthly change in consumer loans. What the hell happened?

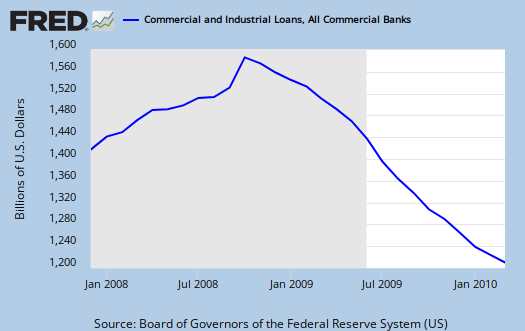

Yet on all Business Loans, the main graphs shows credit is still tight:

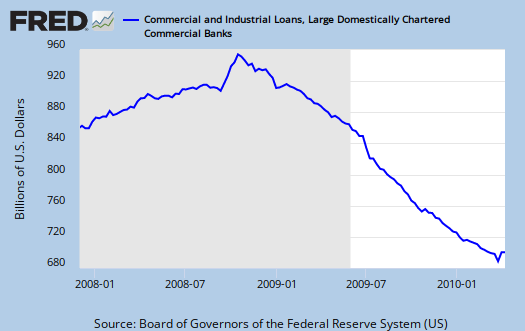

But at large banks, there is a slight increase in business loans:

I scratched my head, wondering what is happening here and then it dawned on me. I got an automatic credit limit increase on a bunch of credit cards. I didn't ask for it, they just did it! Sure enough, from the Federal Reserve data, revolving credit went from $321.1 billion $396.7 billion in a month. That's a 19% increase in just one month on revolving credit. All consumer loans, which includes revolving credit (credit cards), had a similar jump, 9.22%.

So, who wants to bet we're going to have a larger C, consumer spending, in GDP real soon, brought to you by Visa and MasterCard? (ignore that D funding it, we'll just sweep that one under the rug with all of the other debt).

Consumer lending: look closer

There was a change of accounting rules. Actual lending fell.

Skeptic, do you have the details?

I saw a change in accounting rules which moved loans from bonds back on the balance sheets, but those were January, but I cannot find any correlation to the above in terms of percentages.

Nothing would surprise me on this but the jump is so dramatic I would like to find the references where they moved a host of loans on the books.

Also, it's just credit cards, consumer loans, so do you have any intel on why this would explode almost 20% in a month by just accounting and making them put these onto the books?

I did dig around and have yet to find any overall industry wide changes, in March, that account.

Yup, it's accounting

"Financial Accounting Statements (FAS) 166 and 167 have implications for how banks treat off-balance-sheet special purpose...Larger banks took advantage of secondary markets as destinations for their securitized products, but smaller banks, especially community and regional banks, did not engage actively in securitization vehicles (SPVs)...For instance, for commercial banks with more than $50 billion in total assets, consumer loan portfolios grew 42 percent from the fourth quarter of 2009 to the first quarter of 2010."

http://research.stlouisfed.com/publications/es/10/ES1018.pdf

Most intersting: "A broader issue for the banking sector is how the consolidation of these assets on bank balance sheets will affect bank capital. The purpose of off-balance-sheet SPVs was to give banks smaller balance sheets and to remove assets, which allowed them to hold less capital to defend against the risk of losses. Thus, these banking institutions may need to increase risk-based capital levels in upcoming years to accommodate this increase in assets."

Great find BTN

Wow, I missed that completely and the Fed itself is saying these are just accounting rule changes, consumer credit in practice did not increase dramatically as a result.

Please consider getting an account for we could use some good forensics like that research paper.