The National Bureau of Economic Research declared this week that the Great Recession ended over a year ago. Yet, for some reason, the average American isn't ready to break out the champagne.

"Every single one of the individuals who wrote the report needs a serious reality check," said Bob Johnson of the Queens borough of New York, who is 46, had worked in communications and has been looking for a job for more than three years.

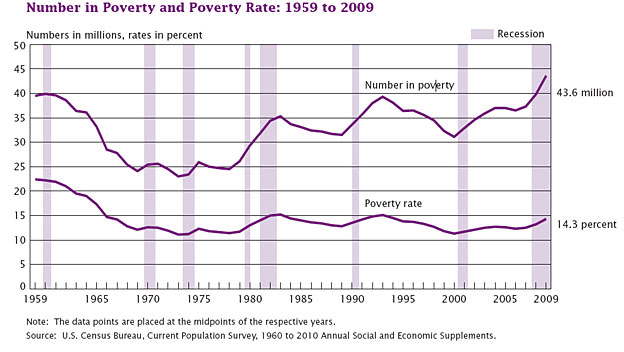

The American working class is hurting. The unemployment rate is only marginally down from the peak and the economy has been losing jobs over the last three months. Households were $1.5 Trillion poorer last quarter, and $12.3 Trillion poorer than three years ago. Most of this is reflected in the crushed dreams of retirement. The poverty rate is at a 15-year high.

Nevertheless, the economy is improving, right? That depends on who you ask.

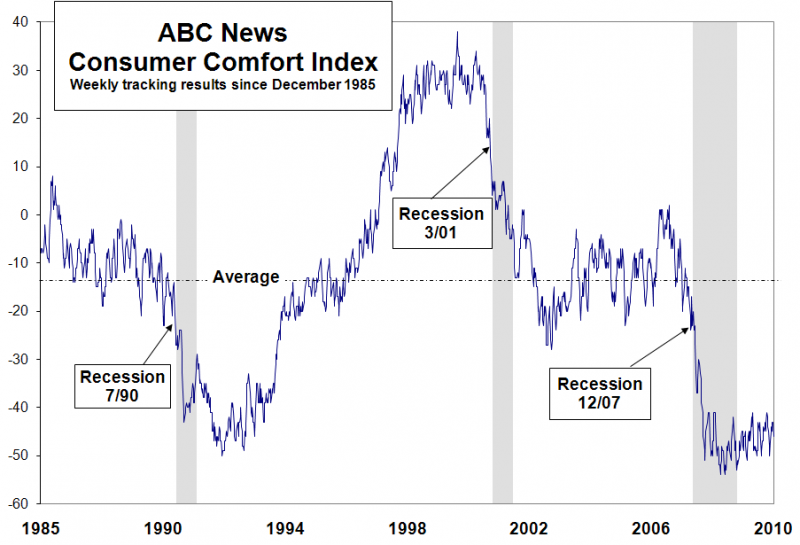

Clearly the American consumer doesn't believe that the recession is over.

This week 89 percent of Americans rate the economy negatively, 75 percent say it’s a bad time to spend money and 55 percent rate their own finances negatively.

The Gallup poll showed very similar findings.

So what does this mean? Economists, the financial media, politicians and industry leaders think that it means nothing. They consider the consumer, and thus +90% of the population, either a lagging indicator or irrelevant.

Of course they aren't going to tell you that because, well, it sounds so darn elitist. They have their numbers and charts, and, you see, you just aren't as smart as them.

That's what they honestly believe.

The idea that they aren't as smart as they think they are, hasn't occurred to them. The idea that their charts don't accurately represent reality is not something they will ever consider.

In reality, they are prisoners in a cave of their own making.

Allegory of the Economic Cave

Around 2,400 years ago Plato created an allegory of prisoners chained for life in a cave. All they could see was shadows on a wall. Thus the shadows became their reality.

"And if they were in the habit of conferring honors among themselves on those who were quickest to observe the passing shadows and to remark which of them went before, and which followed after, and which were together; and who were therefore best able to draw conclusions as to the future, do you think that he would care for such honors and glories, or envy the possessors of them?"

The charts and reports that economists present to us are only shadows of reality. They are mere representations and caricatures of a slice of the real economy that is distorted by interpretation and dogma.

The economist who can more quickly draw conclusions and predict the next shadow gets honors and glories from his peers.

Of course the economist who gets the honors and glories isn't one who predicts recessions. Any economist who predicts bad news either doesn't exist, or is held up for ridicule.

In fact there were economists that predicted what happened.

Nouriel Roubini in 2006, Peter Schiff in 2005, Fred Harrison in 1997, and Hyman Minsky in the 1980's all predicted scenario's that were far too accurate to be considered just luck.

The same economists that didn't listen to these cassandra's before the crisis are now embracing the recovery that most Americans say doesn't exist. What could they be missing?

For starters, economists generally don't look at how wealth is distributed. They have conscientiously decided to not consider class in their calculations. By doing so they are missing an monumental change in the economy.

As Andrew Sum and Joseph McLaughlin of Northeastern University's Center for Labor Market Studies have documented, pretax corporate profits increased $388 billion from the low point of the current recession, the second quarter of 2009, to the third quarter thereafter, while wages increased just $68 billion. At a comparable point in the 1981-82 recession, corporate profits came to just 10 percent of the combined uptick in profits and wages. This time around, they amount to 85 percent.

A similar tale can be told about employers and health insurance, the costs of which have continued to rise. It's not the employers, however, who have borne those increases. A survey, released Thursday by the Kaiser Family Foundation and the Health Research & Educational Trust, shows that employee premiums rose 13.7 percent over last year, while the amount that employers contributed dropped -- dropped! -- 0.9 percent.

Only a purblind ideologue could miss the pattern here. American employers -- more than employers in other nations and more than American employers in earlier downturns -- have imposed the costs of the recession and, increasingly, the costs of doing business, on their workers, and kept for themselves damn near all the proceeds from doing business.

All of the economic models are based on a system in which people and businesses will "trickle down" the wealth. When profits go up, businesses will hire. That's a basic premise that economists simply won't question, even when the facts show otherwise.

That's why economists always support tax cuts for the wealthy - because they are supposed to spend it and "trickle down" the wealth. Once again, the facts show otherwise, but economists won't update their models. And why should they update those models, when they don't even acknowledge the fact that class influences spending and consumption patterns?

Which brings us back to the current economic conditions, which are the worst since the Great Depression.

Has the economy made some progress since the summer of 2009? Yes, but only at the expense of unprecedented amounts of deficit spending. Between the wars, the bailouts, and the stimulus packages, we've run up a deficit of nearly 10% of GDP. This is unsustainable.

The really disturbing part is how little we have to show for this increased debt burden.

What we've seen is a cyclical upturn in a larger secular downturn (as witnessed by the large percentage of GDP growth coming from inventory build-up), just like we saw in the 1930's. But we can't call this a Depression because there is no accepted definition of what a Depression is.

That's not to say that some aren't trying to define it.

This is what a depression is all about — an economy that 33 months after a recession begins, with zero policy rates, a stuffed central bank sheet, and a 10% deficit-to-GDP ratio, is still in need of government help for its sustenance.

A depression usually involved a liquidity trap. In other words, expunging the debt excesses of the previous cycle leads to an ongoing contraction of credit where the demand and supply of loan-able funds is basically non-existent. This is why Libor (three-month interbank) rates are down to five-month lows of under 0.3%.

You know it’s a depression when, 33 months after the onset of recession...* Wages & salaries are still down 3.7% from the prior peak;

* Corporate profits are still down 20% from the peak;

* Real GDP is still down 1.3% from the peak;

* Industrial production is still down 7.2% from the peak;

* Employment is still down 5.5% from the peak;

* Retail sales are still down 4.5% from the peak;

* Manufacturing orders are still down 22.1% from the peak;

* Manufacturing shipments are still down 12.5% from the peak;

* Exports are still down 9.2% from the peak;

* Housing starts are still down 63.5% from the peak;

* New home sales are still down 68.9% from the peak;

* Existing home sales are still down 41.2% from the peak;

* Non-residential construction is still down 35.7% from the peakIn a normal recession-recovery cycle, practically all these indicators are making new highs at this juncture of the business cycle.

The reason is because this isn't a business cycle recession. This is a secular Depression. The reason for that is because the wealth has been increasingly distributed up to the top 1% who are saving the money rather than spending it like the working class would.

Asset prices, like stocks and bonds, rise because of this is where the rich save their money. However, real final sales decline because most of the population is hurting.

While this statistical "recovery" can continue for years to come, the working class will continue to struggle. As long as we continue to embrace these failed economic policies, the jobless recovery that no one but a statistician can see, will become the "new normal" - a permanent lowering of living standards for the working class. The jobless recovery will become the homeless recovery.

If this is to change, it must come from below. We must accept that class does make a difference, and that the wealthy elite do not have our best interests at heart.

It's not class warfare to say this. It's simply a matter of recognizing shadows from reality.

Comments

NBER cycle dating

I was actually surprised they dated it. That said, in their press release they clearly seem to be gunning for a "double dip" definition and I think it's political, because a recession going on 3 years, technically, is a Depression.

Those folks are extreme economics geeks, so I have a hard time implying that...

because I'm with you, and said so, when I overviewed the NBER declaration.

We are also getting some very serious bullshit on cable noise, including Dylan Ratigan on "solutions".

It's scary. Many are recognizing "the problem" and then we get "solutions" that are even more middle class squeeze disaster!

So, they are using the economic despair to twist in the wind and try to convince people to endorse bogus and incredibly corporate driven, god awful agendas that will hurt working America even more!

Deficit is unsustainable ...

I really enjoy your musings and share your disillusion about mainstream economists. Unfortunately you seem to fall for one economics fairy tale hook, line and sinker. The government budget constraint mythology.

On August 15, 1971, the United States unilaterally terminated Bretton Woods. Since then the US government is the monopoly issuer of its non-convertible, FX free-floating FIAT currency. By definition the US federal government is not revenue-constrained and faces no solvency risk. It can run deficits nonstop and indefinitely. The only constraint on federal spending is what real resources are available in the economy both to the private and the government sector. And I hope you agree, that given a capacity utilization of 75% and unemployment a lot larger than 10% there are plenty of idle resources available for government spending without any danger of inflation.

Too many people and not enough jobs

"American employers -- more than employers in other nations and more than American employers in earlier downturns -- have imposed the costs of the recession and, increasingly, the costs of doing business, on their workers, and kept for themselves damn near all the proceeds from doing business."

This continues a trend of transferring risks from the corporation to the individual worker (e.g. from pensions to 401Ks).

This is exactly what most employers want. A desperate workforce, an economy with too many workers and not enough jobs, so that employees can be lowballed into accepting whatever the employer chooses.

Most employers despise having to COMPETE for labor. Offshore outsourcing and H-1B visas are tools in their arsenal for ensuring an oversupply of labor ... and United States Congress is their facilitator in this scheme to undermine working people.

The problem with the economy in the United States is simple. There are too many people and not enough jobs.

Correct in all respects except...

...your conclusion which is, frankly, a tautology.

If our greatly esteemed President or our Congre$$ was responsive to the people's needs we'd see a vastly different landscape. That landscape will follow a massive earthquake in this nation. An earthquake that will destroy the crumbling, croney capitalism we are seemingly stuck with. But the ruling class has never in history given up it's greed and lust for power in order to keep on ruling. Nope, they always push it that one step to far. Obama is that one step. His 'policies' are absolute lunacy; especially if you are in the top 2%.

Things are about to get so bad that 'Change you can believe in...' will come. On a wave of violence not seen since...oh, say...

...the 1930s.

'When you see a rattlesnake poised to strike, you do not wait until he has struck to crush him.'

You're right to lead with poverty data Excellent post

And the graph, "Recession at Work," is telling. This is exactly what propels the rise in corporate profits. It's not just a jobless recovery, it's a continuation of the great wealth transfer.

The Republicans are absolutely overjoyed by this and they've hoodwinked enough of their supporters to show some degree of structural integrity as a party, although it is an illusion. The Democrats use the Republican craziness to move the "moderate" position evermore to the right. There is no hope with the current cast of characters.

Michael Collins

No sure how you can do such

No sure how you can do such an analysis and leave out (apologies if I missed it) the word "Federal" next to the word "Reserve." It has been the Federal Reserve that is juicing up the rich. The two huge jumps in the top 1% are the dot com bubbles and the housing bubbles.

Pumping cheap money always has 2 effects - huge debt in the bottom, funneling of wealth to the top.

The second villain is the global elites who offshored our industry. Again the Federal Reserve is the enabler - flood the masses with credit to replace wages.

We don't need higher taxes on the wealthy. We need the Fed torn down, brick by brick.

Recession is going to continue until America is realigned

It is clear that the rise in poverty seems systemic based on the laws and infrastructure that are still in place from 2001.

We need a system that creates opportunities for the producers of America, those that make and provide goods or services and decreases the incentives for the hedge fund managers of for people to trade.

In my estimation, it all comes down to a simple math problem.

Capital Gains are only taxed at 15% whereas worker's income is usually taxed at 28%

If we inverted the two perhaps we would make trading currency and timing the market less profitable and production of goods and services more profitable.

Until America is aligned with growing the GDP, poverty will continue because there is no economic infrastructure which benefits the lower and middle classes.