THROW THE BUMS OUT - ALL OF THEM

Senate Millionaires Kill Mortgage Assistance for Citizens

The United States Senate took a swipe at the spirit of May Day in a spectacular show of callous indifference when it voted down a bill to provide limited assistance to citizens at risk for losing their homes. The final vote was 45 in favor, 51 opposed to Senator Richard Durbin's (D-IL) mortgage assistance bill. The original version of the bill covered some but not all of those requiring assistance. The final version was even more restricted. It applied to only homeowners currently in foreclosure as a result of actions prior to the start of 2009.

The denial of assistance to citizens by Senators is ironic given the fact that the origins of the current economic crisis came from Senate legislative actions in 1999 and 2000.

While their avarice knows no bounds, their memory suffers.

Apparently these multimillionaire aristocrats of the Senate "gentlemen's club" haven't been watching the news. The International Monetary Fund declared that the United States is in a depression almost three months ago. Delinquency and foreclosure rates around the country are rising at spectacular rates. Unemployment has jumped by 3.3 million in the last five months. Economic growth has declined at a rate of 6.3% in the first quarter of 2009.

What part of economic crisis can't they understand? Apparently all of it.

Memo to stingy Senators: Workers and their families are in serious trouble or about to be in trouble. That means they lack the money to pay for their homes (also known as shelter, a basic human need). These citizens did nothing to bring on this crisis.

You, the members of the Senate, are largely to blame and you know it.

One of the most revealing remarks came from Democrat Ben Nelson (D-NE) who said:

“Do I want to have my rate go up so that somebody else might be able to cram down” their mortgage payment?" asked Sen. Ben Nelson, D-Neb., who voted against the bill. Associated Press, Apr. 30, 2009

Nelson has never been regarded as the sharpest tool in the shed but he's set a new standard for ignorance with this remark. Nelson was worth at least $7.0 million as of reporting in 2008. Obviously he needs to skimp on every penny to stay afloat. He'll offer no breaks for financially strapped citizens on the brink of ruin even if they are in trouble as a result of his support of Wall Street welfare. The bill would have no impact on his or anybody else's mortgage rate unless they qualified for help. In those cases, the rate would go down.

The Durbin bill offered a reasonable change in bankruptcy law that would allow those in foreclosure to ask (simply ask) bankruptcy judges to invoke a "cramdown." In that process, the bankruptcy court would set a lower interest rates and longer terms on loans. This takes the case out of foreclosure and allows citizens to keep their homes and the lets banks collect the money owed at a lower rate over an extended period. (See this for a real cramdown to benefit all citizens)

The Durbin bill provided limited options since it presumed that homeowners at risk had the money to get in bankruptcy court; that the courts would be able to handle all those in need; and that the judge would accept the request for a cramdown to keep people in their homes. But the bill might have helped as many as 1.7 million homeowners.

Even with those limitations, Sen. Durbin was forced against the wall and had to negotiate the bill to a lower level of protection. The final bill rejected by the Senate. Associated Press reported: "The latest proposal would have restricted eligibility to homeowners already in foreclosure whose lender had not offered better terms. Homes would also have to be worth less than $729,000 and apply to mortgage loans originated before 2009." Apr 30, 2009

Durbin's last stand would have provided protection some homeowners but now there's no protection for anyone.

William K. Black is the chief fraud investigator who untangled the 1980's Savings and Loan fiasco. His comments on the current economic meltdown are instructive and assign blame:

William K. Black: 'We need some chairmen or chairwomen … in Congress, to hold the necessary hearings (on banking fraud) and we can blast this out. But if you leave the failed CEOs in place, it isn't just that they're terrible business people, though they are. It isn't just that they lack integrity, though they do. Because they were engaged in these frauds … they're not going to disclose the truth about the assets." Bill Moyers Journal, Apr 3, 2009

Senators, you allowed changes in banking regulations that turned Wall Street in to a big casino for the "in crowd" and wiped out millions of small investors and retirement funds.

You failed to monitor the new freedoms you gave the banks and Wall Street after you stripped away citizen protections in law since the Great Depression.

You created the current depression.

And now, you're so stingy you won't even help a few of the many people victimized by the massive corporate fraud schemes, Ponzi schemes according to Black.

Is there any reason why even one single Senator of the 51 who voted down this assistance should remain in office to complete his or her term?

Is there any reason to hold back from recalling them where allowed or demanding their resignations in every state that they represent?

I can't think of one. Can you?

END

Permission to reproduce this article in whole or part with attribution of authorship to Michael Collins and a link to this article

Appendices: Hall of Shame, Things to Come, and Resources

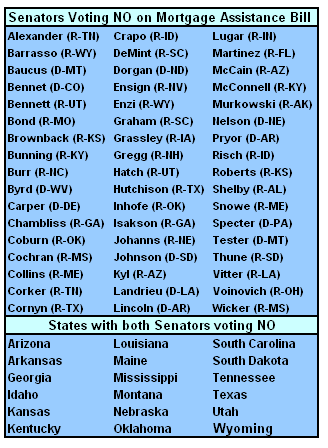

Hall of Shame

The votes lined up in the usual way, with the majority of citizens losing out on positive action. Of note, the "moderate" Republicans Collins and Snow of Maine both opposed the bill. The new Senator from Montana, Democrat Tester, voted no. And Democrat "changling" Specter said no also.

Things to Come

See: Too Little Too Late - The Money Party at Work Feb. 18, 2009

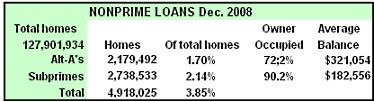

There are 4.9 million Alt-A and subprime loans. Alt-A's are loans to those with higher credit ratings that have special introductory features. Subprimes are loans to people with marginal credit.

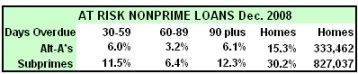

15% of Alt-A loans were at risk in at the start of the year. 30% of subprimes were at risk.

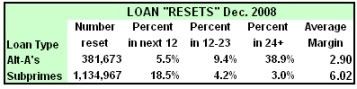

A majority of Alt-A loans will "reset," increase interest, in the next 2 plus years. 25% of subprimes will do the same at a much higher rate. That spells disaster since the "resets" are a major trigger for bankruptcy.

Some Resources

Bill Moyers Journal - Interview with William K Black Bill Moyers Journal, Apr 3, 2009 (Transcripts: PBS pdf Word.doc)

Stiglitz: Capitalist Fools (Essential Reading"

Economic Disaster -- Are You Next? Feb. 5, 2009

Too Little Too Late - The Money Party at Work Feb. 18, 2009

Enough of Everything But Dollars Mar. 2, 2009

Enabling Acts for an Era of Greed - The Money Party at Work Apr. 14, 2009

Comments

I'm not sure of this vote yet

and the reason is Dorgan is well known to be a strong middle class advocate, legislator. Tester ain't bad either.

I just read through the amendment and I did see a clause which stated bankruptcy judges could reduce the principle to 31% of a person's income, as calculated at the time of bankruptcy.

Unless I am mistaken, this could give someone a house basically for free, while in bankruptcy.

I'm not saying this for sure yet, I need to see the objections of Dorgan, Tester for I know Dorgan especially is not one of our "bought and paid for" finance corporate representatives and Tester is not either. I also need to read the actual amendment more. I found it here.

Seriously we might have one of those devil in details going on.

Not saying this is bad, I have believed for some time, they need to let people out of those bad mortgages, refinance them and due to the housing bubble crash, also reduce principle in hardship, especially those second mortgages...

but I want to know more first.

But in terms of rage, hey, you go, I'm all for Populist outrage on EP! ;)

The details are important

But the general picture is even more revealing.

One thing I gathered after publishing this is that there was strong opposition from the community banks. They loan their own money, it's not securities a go go. They were going to take a big hit if this passed.

Now, what does that tell us. There wasn't a serious plan to make this work. I'm not criticizing Durbin who showed a real trooper's spirit. It's the White House, which made no big secret that it had abandoned this task.

After all, it would only benefit 1.7 million homeowners and their families. That's the source of the populist energy on this one.

This could have worked, not as well as a national cramdown. The basis for that proposal, linked in the article and published here, is that the financial services industry has engaged in fraud, as per William K. Black's most thorough outline, and we need to achieve some equitable solution to the whole mess.

But ultimately, it's all about Geithner and Summers, the lurking presence of The Money Party in what is supposed to be our capitol. Great site, pleasure posting here always.

Michael Collins

told ya

I had a feeling it was one of those "look good but really don't support it" pieces of legislation that one tends to see.

baseline scenario agrees with you

James Kwak agrees with you.

I'm still hesitant in spite of all of the oligarch lobbying simply because I know Dorgan's voting record so well. Why the hell did he vote against it and it's not due to lobbyists, I'm positive.

Dorgan thinks that the 31% is an arbitrary

number. I don't thinks so - a lot of time and effort went into drafting and negotiating this amendment.

RebelCapitalist.com - Financial Information for the Rest of Us.

I have to agree with that

I read the amendment and that's what popped out at me immediately. I could see, easily, one walking into bankruptcy court with no income or very little and walking away with basically a free house.

That didn't seem right at all and I was wondering why it was there. Loaded for abuse.

I don't understand why they would do that for it was an obvious manipulation to me.

i.e. I quit my job, I just plain default on my credit cards, I don't make my house payment....I file...

bam, the court could literally wipe out my debts and also give me a house for free..

Once the case is closed (I think it's about 60 days from filiing), I get a new job, so now I am with a new job and also got a free house.

considering the value of houses (still, even with them slowly becoming valued to where a wage can afford one), that's an obvious "optimization" in our temporary employment world.

Seriously, I would do that. Living with a bankruptcy on your record just doesn't hurt that much and for a free house...it would be more than worth it in total amount I would actually get.

I can't think of the senator's name

But there was major senator, who under the old bankruptcy system, had a mansion in Florida who would do something similar. He would do this every couple of years.

exactly

Florida was a place you could keep a McMansion and basically get it for free through Ch. 7, never mind 11.

Psycho ex-wife killer O.J. Simpson did the same thing, he even bought a huge house, established residency there in order to do it to avoid the payout on the civil suit.

So I got my fundraising letter from the Democrats today

I couldn't fill it out. This morning confirmed what I have been feeling for a while now, that I'm no longer a Democrat. Today, I'm an independent. Reading this, and amen to Michael Collins for putting this up, all I can say is that the failure to pass is really a shame. The argument has been that you can't change a business contract, that there is the rule of law. And for the most part, they are right. But I also know that deals can change if conditions do.

The Democrats knew this was a dead deal. If they really wanted to pass this, they could have. I'm sorry, but I fail to see how they could not. This was one of those "make us look good" bills for the Democrats. They know that certain conservative party members, without any arm twisting the other way, would vote against this. Honestly, did the Senate leadership really attempt to lobby with their dissident members? My suspicions think they did nothing. Durbin was probably told "yeah go ahead, it sounds great" but then behind his back they snickered. Frankly, a lot of these peope, both parties, are bought and paid for.

But we really need to have a serious discussion about homeownership and the things that entail such. We know there was fraud, hell I was almost part of such an operation back in '05! The banks don't want to own these homes. A lot of folks purchased homes that many KNEW they could NOT afford but felt entitled to own that big house. We had an industry pumping out messages that led to that entitlement, I mean how many of you have seen those mortage commercials or those late-night infomercials with Carlton Sheets? This was a perverse version of pump and dumb on a biblical scale! A lote of these people who are facing foreclosure who, despite how many cramdowns or financial assistances, must realize that if they can't afford it they will lose it. But for those that can, the best we can do is help them keep that home. For those that lose out, well we really need to help them up with rental assistance and dammit we need to do something...something about affordable housing!

We need the regular folk party

or the middle class lobby. Seriously, let's abolish all taxes and put all of our money to buying our government back from the hands of corporations.

I don't blame you on that one....

I think about how hard I worked on the Kerry campaign in '04 and I look at his voting record now and say to myself, "what was I thinking"...

Even ones I believe in during the campaigns, I get hoodwinked.

Jeff Merkley (OR) ran on "no bail outs period" and looked like a really good Progressive/Populist Dem..

first vote in the Senate...bam, voted for more bail out money, no conditions, walking lock step with DLC Dem leadership. I mean he ran on this issue and he also surged in the polls when he did....huge, major campaign promise.

I have a lead on some of those conservatives....but they just don't get it in my view, these are the conservatives who are flipping out on the TARP, Stimulus as much as we are...but they want to also make these things that clearly do not work, the neoconservative sort of rhetoric back.

They don't seem to get the difference between corporatism and think it's socialism. I wish they would wake up and stop spinning the machine. They know something is really wrong but they can't get out of some rhetoric to understand what exactly is wrong.

These are my personal opinions, impressions.

IF so I think maybe I'd agree

I think I'd have to agree with their vote if this is in the Act "bankruptcy judges could reduce the principle to 31% of a person's income, as calculated at the time of bankruptcy".

Damn, why did I pay off my mortgage in 15 years? I put off those fancy vacations, that my wife so openly pointed out, that our friends were taking.

So with such an Act / Bill it would have allowed me to take the moral hazard route and to have gone on nice vacations and now with an income downturn....I could have had my principle reduced to 31% of income. The problem is that my working class morals, pay your bills mentality wouldn't let me game the system. But on a daily basis I see a ton of people that would have no problem gaming the system.

But we can allow the same modification

on vacation homes and luxury yachts. The only way to game the system is if loan originated before 2009 and 60 days delinquent. This doesn't go off in the future.

I believe that most people have learned a valuable lesson from this particularly when they may be losing their homes and destroying their credit history. I don't think there is a risk of moral hazard for most people.

If we are going to prevent more destruction of middle class wealth we have to stem foreclosures. Foreclosures in neighborhoods hurts everybody in that neighborhood. It sucks that we have bail out people who made really bad decisions but I would rather bail struggling people out then the financial oligarchy.

RebelCapitalist.com - Financial Information for the Rest of Us.

There's just one problem .

The people in their primary residence, with no other place to go, didn't get there by "gaming the system". As JV explained, they are likely victims of circumstance. The speculators who bought 2,3,4 or more "other" residences are qualified to cramdown those loans. They are the ones who really knew how to "game the system". That's what the "system" is all about. Poor people are more apt to pay their bills, it's a matter of pride and ethics. "System gamers" find the loopholes and cry rule of law, all the way to the bank. By the way, don't you think you're going to pay one helluva premium for bailing out the banksters? If 10%, even 20% of prime residences are crammed down, the cost pales in comparison. The banksters are the guys who are quick to point out that a contract is a legal, binding agreement, unless it applies to them. We need to get off this Reaganite way of looking at each other. Dog eat dog capitalism just can't work, we need to look out for each other.

Most speculators are out by now.

They took their loses and got out - the carrying cost would be too huge to hold properties.

RebelCapitalist.com - Financial Information for the Rest of Us.