There is a limited window of opportunity, when an economic crisis evolves from a manageable event to an out-of-control monster. The current economic crisis is getting rather long in the tooth, and yet the global political and economic leaders still show no ability to fully grasp the depth and complexity of the situation.

As of this moment there are two evolving problems that are only a few months away from being out of anyone's control. One of the problems is domestic, the other lies on the other side of the Atlantic. Both of them have the potential for catastrophic consequences.

The Domestic Problem

It's more symbolic than anything else. When the state of Kansas can't make tax refunds then something seriously is wrong in the state of...well, you know.

Of course something is also wrong in the state of California as well, where 20,000 layoff notices are being sent out. California has $41 Billion shortfall (and counting) to cover and no realistic way of doing it.

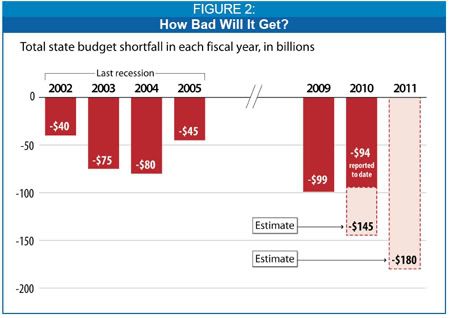

Kansas and California are far from being alone. 46 states have budget shortfalls of a combined total of $350 Billion. Nine of those states have deficits of over 10% of their budgets already.

Over half the states had already cut spending, used reserves, or raised revenues in order to adopt a balanced budget for the current fiscal year — which started July 1 in most states. Now, their budgets have fallen out of balance again. New gaps of $51 billion (over 10% of state budgets) have opened up in the budgets of at least 42 states plus the District of Columbia. These budget gaps are in addition to the $48 billion shortfalls that these and other states faced as they adopted their budgets for the current fiscal year, bringing total gaps for the year to 15 percent of budgets.For example, at least 28 states have implemented or are considering cuts that will affect low-income children’s or families’ eligibility for health insurance or reduce their access to health care services. Programs for the elderly and disabled are also being cut. At least 22 states and the District of Columbia are cutting medical, rehabilitative, home care, or other services needed by low-income people who are elderly or have disabilities, or significantly increasing the cost of these services.

At least 26 states are cutting or proposing to cut K-12 and early education; several of them are also reducing access to child care and early education, and at least 32 states have implemented or proposed cuts to public colleges and universities.

Reduced health care coverage, reduced child care, reduced education, reduced services nationwide. What's more, 37 states are following California's example and slashing payrolls in the face of rising joblessness.

Many of these states never fully recovered from the 2001 recession. Now they are being hit even worse. This has the potential to undo all the good that the federal stimulus package will do.

Without serious help there are good odds that cities, counties, and even states will default on their debts in the coming years.

The Overseas Problem

Ireland has a problem.

"Fears are mounting that Ireland could default on its soaring national debt pile, amid continuing worries about its troubled banking sector," Britain’s Sunday Times reported.The Times noted that pledges made by Ireland to support its crumbled banking sector amount to 220% of the country’s annual economic output. Loans outstanding at Irish banks are more than 11 times the size of the economy.

Home prices in Ireland fell at a 9% rate last year. So far the Irish government has seized one of the three major banks in the country and leaning towards doing the same with the other two.

Credit default swaps on Irish debt is running at 355 basis points, the highest rate in Europe and almost half way to Iceland's rate (which has already defaulted).

That sounds pretty disastrous until you realize that Ireland is not the basket case of Europe - the entire swath of eastern Europe is.

Bartosz Pawlowski, from TD Securities, said the recent plunge in currencies across Eastern Europe had come as a brutal shock. "The rout could potentially lead to substantial problems, if not an outright collapse of the financial system," he said, citing the rising real burden of debt taken out in euros and Swiss francs.

Eastern European countries have borrowed heavily from western European banks. Banks from Sweden, Italy, Austria, France, Belgium, and Germany account for 84% of all of those loans. The debt is denominated in western European currencies, so when the currencies of eastern Europe collapse the debt burden becomes almost unpayable. If the debt burden of eastern Europe goes into default then that means trouble for even the strongest of western European nations.

Swiss banks have given billions of credit to Eastern Europe - now the customers cannot pay back the money. Switzerland is threatened with the fate of Iceland, says economist Arthur P. Schmidt.

...

Yes, the system has only worked as long as the exchange rate between the franc and the currencies were reasonably stable. But that is not currently the case. For example, the Hungarian forint and Polish zloty have lost over a third of their value against the Swiss franc in recent weeks. Because of the devaluations of the national currencies, the debt to Switzerland has increased by more than one-third. Many of the Eastern European countries have serious payment difficulties, and are virtually bankrupt.

The unemployment rate in Spain has reached 14.4% while ndustrial production has plunged by 20% from a year ago. Some are openly questioned whether British banks can be saved at all.

But it is to the east where the financial crisis appears to be centered. Athens has ordered Greek banks to pull out of the Balkans.

“The outlook for the global and the Euro-area economy in 2009 appears dismal. The current crisis is the biggest since the 1930’s and exiting from it will not be easy or quick.”

- Greek central banker George Provopoulos

Meanwhile the former Soviet states are melting down. The Ukraine, which the IMF recently bailed out for $16 Billion appears to be ready to default anyway. The Ukrainian PM has officially denied it...which is always a bad sign. The Latvian central bank governor called his economy "clinically dead". In Bulgaria, the police are staging a sort-of "silent strike" over wages.

The currency crisis in eastern Europe has gotten so bad that people are turning to gold as faith in paper currencies recedes.

The most dramatic surge was in Europe, where bar and coin demand increased from just 9 tonnes in Q4 2007 to 114 tonnes in Q4 2008, a 1,170% increase.

Lack of vision and leadership

The other day Lindsey Graham actually came out in favor of nationalizing banks. Imagine that. Even a Republican has seen the light and endorsed a progressive move to stabilize our financial system.

So why the F*CK isn't the Obama Administration doing it?!?

Instead the Obama Administration is going down the same road that the Bush Administration just led us.

And for all of its boldness, the plan largely repeats the Bush administration’s approach of deferring to many of the same companies and executives who had peddled risky loans and investments at the heart of the crisis and failed to foresee many of the problems plaguing the markets.

Instead of cleaning up Wall Street, the administration is forming a partnership with the largest speculators there, giving them free loans to speculate further. For all of the grand speeches, we are making the same mistakes that others have made before.

"I thought America had studied Japan’s failures," said Hirofumi Gomi, a top official at Japan’s Financial Services Agency during the crisis. "Why is it making the same mistakes?""I think they know how big it is, but they don’t want to say how big it is. It’s so big they can’t acknowledge it," said John H.Makin, an economist at the American Enterprise Institute, referring to administration officials. "The lesson from Japan in the 1990s was that they should have stepped up and nationalized the banks."

Instead, the Japanese first tried many of the same remedies that the Bush administration tried and the Obama administration is trying — ultra-low interest rates, fiscal stimulus and ineffective cash infusions, among other things. The Japanese even tried to tap private capital to buy some of the bad assets from banks, as Mr. Geithner proposed.

The problem doesn't appear to be so much corruption as a distinct lack of understanding of how we got here, and a lack of vision for where to go. Instead of moving ahead, the Obama Administration appears to be trying to get the economy back to where it was a few years ago.

For instance, they are trying to reinflate the housing bubble by lowering mortgage standards and subsidizing borrowers that have gotten in over their heads.

This is a useless waste of time and resources that should be directed on moving us ahead, not trying to get back to a place where we can never, and should never, return to - an unsustainable credit bubble.

We've lost precious time trying to get back to what we know, afraid of what is to come. What we know was a lie and it deserves to die. What is to come is the truth - the post-credit bubble world. It may not be pretty, but it is real. I'll take the real over the lie every time. If we can't form enough courage to face reality then perhaps we deserve the punishment that this hopeless and futile denial will bring down upon us.

Reality is going to intrude upon our lives one way or another. We can either embrace it and work with it, or we can be beaten down by it. An economy based on buying things that we don't need with money we don't have is a lie. Getting "rich" by selling each other McMansions is a scam.

Producing goods by hard work and savings and living within our means is reality. The world is returning to the historic mean. The dysfunction of the world financial system of the last 30 years is dying. We can use this as a historic opportunity to change the world for the better, or we can try to take the easy way out, which will only lead us to a dead-end and more suffering.

Comments

TALF

That is one hell of a find. I had no idea they were trying to use U.S. taxpayer money as ante to play in the great Ponzi Hot Potato derivatives market.

We need a national manufacturing policy. A real crafted, analysis, specific and pointed U.S. agenda to revitalize U.S. manufacturing.

Hey ... didn't I read this somewhere else already? ;o)

It has always been about class warfare

Great minds think alike!

Ok, who is going to write the nasty blast post on Obama and his NAFTA promises vs. what just happened today?

I'm out of my daily outrage quota.

When you're Right, you're Right On

"The problem doesn't appear to be so much corruption as a distinct lack of understanding of how we got here, and a lack of vision for where to go."

Ed McMahon couldn't have said it better, "You are CORRECT, sir!" Neoclassical approaches may not work at this stage.