This morning Mish has an entry entitled

Huge Demand For Treasuries As Banks Refuse To Lend in which he cites bank reserves and a sluggish M1 multiplier in support of the conclusion that:

Look at the Base Money chart and the Reserve Bank Credit chart. Base money is soaring but all of it is sitting in bank reserves. In other words, banks are not lending. Clearly we have a huge monetary distortion, but banks seem to understand that lending money in this environment would do nothing but increase losses

Of course, Mish's article is simply received wisdom at this point. There can be no recovery until banks start lending, and they are refusing to lend.

There's just one problem with this argument: it isn't true.

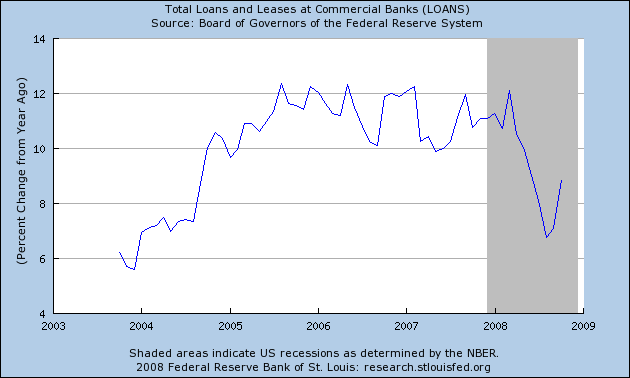

Here is the Federal Reserve graph of Commercial Bank loans and leases through October 2008:

Here is a good description of that statistic:

Interest and fees that banks earn on loans and leases also are a major source of the revenues they report on their income statements. Besides commercial and industrial loans, or “business loans” as they are often called, other key categories of loans reported by banks and savings institutions include loans secured by real estate, loans to finance agricultural production, and loans to individuals—including credit card loans.

As can be easily seen, commercial loans have been made at an increasing rate since August!

To be fair, the idea that banks are sitting on most of that new cash has obvious merit, per Mish's post. But far from hoarding all their cash, banks are in fact beginning to lend out more money!

So much for the meme that "banks aren't lending".

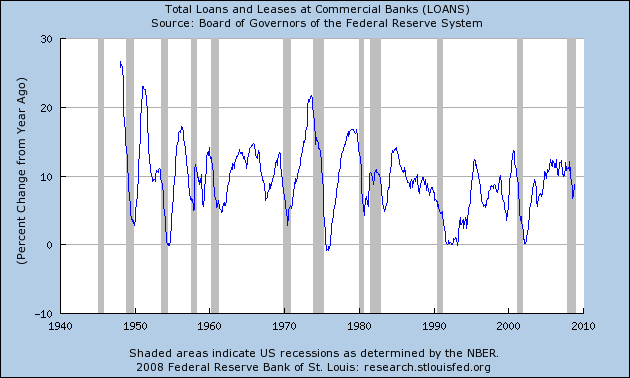

Curious as to whether or not the upturn in lending might have in the past proven a portent of the end to a recession, I looked at past cycles since the series was begun back in 1949. Interestingly, with the exception of two recessions (1957 and 1970), loans actually continued to decline until after the recession's end, i.e., for the other 9 recessions, the statistic was a lagging incidator:

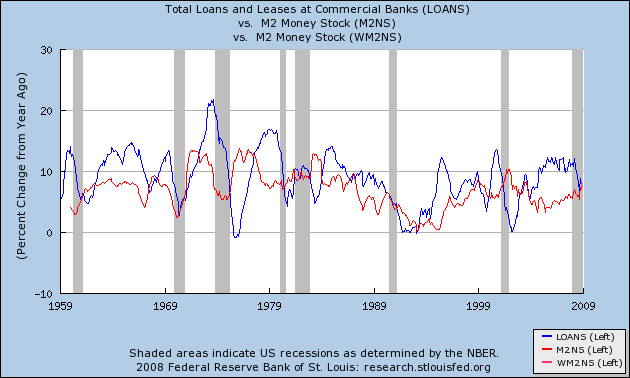

After cross-referencing with items like base money supply, M1, and inflation, and finding no particular relationship, I put Commercial Loans together with the M2 money supply and lo and behold, the graph showed that after a recession starts, M2 has in 10 of the 11 instances started to grow at a rate exceeding commercial loans within a month, give or take, of the end of the recession:

(The 2001 recession is anomalous in that there was an interim period of growth that was ended by the 9/11 attacks. Take away that exogenous event, and the indicator has a perfect record of 11 for 11).

It seems that when the rate of growth of funds available to banks to loan exceeds the rate at which banks have been making loans, that is a signal of the beginning of an expansion.

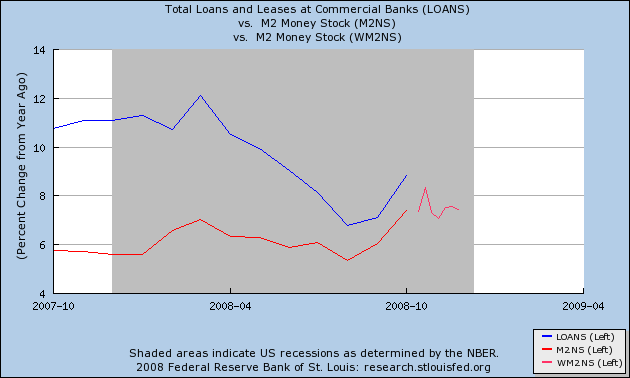

So, where are we now? Here is a graph of this year with the weekly M2 updates through November:

Although M2 has turned up, it does not exceed the loan rate. I will keep an eye on this relationship going forward.

But can we please stop saying "Banks aren't lending?" They are lending, and they are lending at an increasing rate. They are just not lending enough to overcome the other forces in this downturn.

Comments

Excellent work!

Another myth blown up by someone bothering to look at the data. Nice job!

I hope this post gets a lot of readers, for the current religion is banks are refusing to lend and this should make a few faces blush.

This may actually be bad news

I figure the entire US economy is overleveraged at least 13:1, just based on the ratio of M1:M2.

That's what got us into trouble in the first place.

Taking on more debt won't help, it will only delay the inevitable.

-------------------------------------

Maximum jobs, not maximum profits.

correctamundo

google ... stephen roach "America’s inflated asset prices must fall" head of M.Stanley Asia, or:

http://www.ft.com/cms/s/0/5a5419aa-bd47-11dc-b7e6-0000779fd2ac.html

This is a tectonic shift. Bigger than any new President or the ideas of the "geniuses" that got us here. It's just arithmetic, all you M1-M2 Heads.

May I offer these I made up (but may contain prior aphorisms inadvertently)...

"It's the beliefs that die last."

"The truth cannot be fully understood until all the foundations of the lies are excavated and examined without preconceptions (those beliefs)."

The excavations shall commence once enough of the beliefs are dead. It's what the future is made of; always has been. And the beliefs will die once we finally pick up the mirror.

Some financials

were leveraged as much as 40:1. But yes, we got a long way to go.

I was figuring on average

And NOT just financials, but in fact the whole shebang, comparing available M1 to GDP there's a hell of a lot of credit out there.

If we were to try to run an economy this size on cash-only basis, we'd need $13.5 trillion changing hands annually, in real money (as opposed to bits in a computer accessed by an ID card). That's a heck of a lot more cash than we currently have in circulation.

-------------------------------------

Maximum jobs, not maximum profits.

We are constrained by post WW2 statistics

Debt deflations are nothing new. Unfortunately, our in-depth statistics do not include any of those past periods. I have finally found a graph that includes monthly M1 and M2 statistics from the 1920s on, but no cite as to where the data came from, and too noisy to be of much help.

One hopes that on Wall Street, in Washington, and in academia there are many hours being spent creating that data. I would like to know how those debt deflations were resolved "by the numbers."

What is the lending for?

The first question that comes to my mind: What about auto loans? Since that would impact what to do about the auto industry. If auto loans are getting back to normal, then the automakers just need enough to tide them over.

What I think is more likely is that banks are applying more critical analysis, and a lot of people who were able to qualify for an auto loan two years ago, no longer do. This would indicate a more fundamental problem: the stagnation of income for working and middle classes. In which case, loan standards either have to be lowered, or we have to back the auto industry for a very long haul, and begin to frontally attack the conservatives' anti-labor ideas.

Secondly, what are these loans for? Are businesses buying money to purchase new equipment (good) or to buy other companies (bad)? I believe the fundamental problem of the past three decades has been lack of investment into industry and infrastructure; the loss of good paying jobs is largely a consequence of that.

Curious

How much of the data is revolving credit or turnover of old debt? I'm not one looking for an argument here, and perhaps NDD has something here. Yet, listening to companies and their earnings announcements, one gets a different picture.

Now, saying that, I'm going to assume that New Deal Democrat right and that these companies are not. What does that tell us? Now for me, one thing that springs into my mind is that the heads of these companies are using the credit crises as an excuse. Which in turn, leads me to believe that many of these executives actually don't have a clue as to what is going on in their own companies. For what its worth, I think NDD is spot on with M2 and loans in regards to recessions.

Once more, I'm not disagreeing with NDD, I'm just iffy when I see treasury yields go into near-to-negative territory.

Let me add one last thing

Now Tony Wikrent asked an excellent question. Is the credit for capital investment or buyouts of companies. Now it could be, just possible, that both NDD and I are correct. That in reality, banks are loaning out money for consumers and businesses for goods (though I suspect using stricter guidelines for acceptance). Yet, when it comes to M&A, that's when we see things start to dry up. Banks figure assets or companies outright are worth even less or that any debt issuance as the result of such activities are right now born as too risky.

And you know, it makes sense, now that I think about it (or it's the Scotch). Who has been complaining most about the credit crisis? Sure some manufacturers (well really, more than just them), I mean we can all agree that for a few weeks a couple months back, it looked like the entire system was going to come to a complete standstill. Yet, that now it seems it was fear gripping the market, something Hank Paulson managed to utilize in pimping for the TARP.

But now, well people are, sadly, still using their credit cards as a substitute for a paycheck. That companies are making sales. Yet on the Mergers & Acquisitions front, it's as if someone dropped a neutron bomb. And, it isn't just the M&A desk who has been squiling on networks like CNBC, so have companies whose business is that of trading or providing liquidity to markets. Listen to folks like Art Cashin who is on most mornings on CNBC or Bloomberg. So what we have here is a dichotomy on credit.

Further information on the bank loans

If you click on the link where I quote the description of the Fed statistic, that will lead you to a page that gives a detailed breakdown of the historical percentages. Also if you go to the St. Louis Fred and search for "loans", that should pull up all the subcategories that were also reported on December 5. Iirc, every single one of them was up similarly.

Since this is an October statistic, of course it's possible that the number declined in November. But more likely, as I wrote elsewhere, the dramatic collapse of treasury rates to 0 is not inconsistent with this diary. Rather, banks have been the recipient of such a firehouse of money that they have enough to both stuff the proverbial mattresses full of the cash, and also loan some of it out.

Had the banks already loaned out most or all of the bailout money they received, somehow I doubt people would find that reassuring. Better to dole it out in small slices.

Very interesting stuff

The "reflation" has begun.

Of course that begs the question of why credit is so tight? Could it be simply because the entire nation is insolvent?

Mish is at it again

with a new post;

He reruns the same "monetary base" graphs, and adds a graph on banks' holdlngs of reserves. The banks held about $2 billion in reserves at the beginning of September and held ~$300 billion by the end of October (it's about double that now). During the same time, loans increased from $6,9T to $7.2T, a 4% increase.

Is there anyone who thinks that because banks didn't suddenly double their loans in the last two months as the monetary base doubled, that qualifies as "refusing to lend"? If the banks had suddenly made double the loans as they ever had before in the last 70 days, would Mish have considered that a good thing?