By now all of America has heard about BoA's $5 dollar a month fee to use a debit card, or $60 dollars a year just to use a standard feature of any checking account in the digital age.

The question becomes, why would anyone keep their money with Bank of America? Switch! It's easy! There are all sorts of online banks, credit unions which offer free checking, assuredly free debit card use, free ATMs and even offer interest on low balance checking.

America, vote with your consumer power and leave BoA, Wells Fargo or any other financial institution nickel and diming you to death. All these banks care about is keeping their executive bonuses rolling in.

Today we've heard from the 2008 TARP bank bail out inspector general, SIGTARP, that banks left TARP early, not because they wanted to pay back the taxpayer, or because they were financially stable....they left the bank bail out early in order to increase executive pay. The terms of TARP limited executive pay so banks were hell bent on getting out of it, despite their flimsy financial footing.

Guess who was at the top of that list? Bank of America.

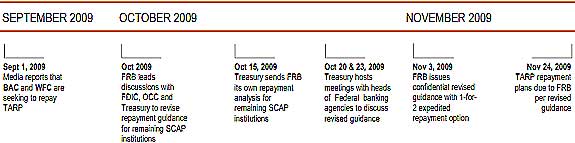

In a new report (large pdf), Exiting TARP: Repayment by the Largest Financial Institutions, we find, literally, a group of banks who could not pass financial stress tests, supposedly designed to tell if a financial institution was healthy or not, were demanding out of TARP so they could once again issue their outrageous executive bonuses and continue pretending or increasing investor confidence. What did Treasury do per the demands of these behemoth banks? Relaxed the rules and requirements for bank financial stability just two months later. Remember, supposedly these banks were going to implode and the entire justification of TARP was to stabilize the financial system.

Federal banking regulators relaxed the November 2009 repayment criteria only weeks after they were established, bowing at least in part to a desire to ramp back the Government’s stake in financial institutions and to pressure by institutions seeking a swift TARP exit to avoid executive compensation restrictions and the stigma associated with TARP participation.

When Bank of America, Citigroup, and Wells Fargo repaid Treasury in December 2009, only Citigroup met the 1-for-2 minimum established by the guidance, combining new common stock and other types of capital to meet a more stringent requirement.

Because the regulators failed to adhere to FRB’s (Federal Reserve Bank) clearly and recently established requirements, the process to review a TARP bank’s exit proposal was ad hoc and inconsistent.

So, who were these regulators relaxing the requirements to exit TARP? Why Tim Geithner and the Treasury, of course, in cahoots with the Federal Reserve. From the report:

Treasury’s involvement was also more extensive than previously understood publicly. While regulators negotiated the terms of repayment with individual institutions, Treasury hosted and participated in critical meetings about the repayment guidance, commented on individual TARP recipient’s repayment proposals, and in at least one instance urged the bank (Wells Fargo) to expedite its repayment plan. The result was a nearly simultaneous exit by Bank of America, Wells Fargo, and Citigroup, involving offerings of a combined total of $49.1 billion in new common stock in an already fragile market, despite warnings that large and contemporaneous equity offerings might be too much for the market to bear.

Below is the timeline where Treasury clearly pressured the Federal Reserve, the ultimate TARP regulator, to relax the requirements for banks to exit from TARP.

As you can see, two banks, now trying to nickel and dime their customers to death, Bank of America and Wells Fargo, also lobbied, successfully, to skirt the rules and exit TARP. It was all about getting their executive bonuses and the Treasury Department along with the Federal Reserve, were more than happy to accommodate them.

Bank of America was adamant that it needed to repay in full and immediately exit TARP, citing concerns including market perception and restrictions established by the Special Master for TARP Executive Compensation. As the negotiations progressed, FRB, OCC, and Treasury became increasingly more comfortable with permitting other sources of capital as a substitute for meeting the 1-for-2 provision in the repayment guidance, while FDIC pushed hard to maintain the strict requirement, as originally established, that the 1-for-2 provision apply only to new common stock.

In yet another rip-off, questionable legal fees were paid by the Treasury Department, surrounding TARP legal issues.

SIGTARP issued another audit report, Legal Fees Paid Under the Troubled Asset Relief Program. Four law firms were paid $25.5 million bucks from a U.S. Treasury department contract related to legal issues surrounding TARP, or the bank bail outs. One law firm bill, Simpson Thacher, all of their billed hours are questions by SIGTARP.

SIGTARP questioned $8.1 million of the $9.1 million (89%) of legal fee bills reviewed. The most striking example of fees questioned by SIGTARP is from the law firm Simpson Thacher. Simpson Thacher billed OFS $5.8 million in fees and expenses with bills that provided no detail whatsoever as to the work performed.

RealtyTrack reported a 33% increase in foreclosure notices in August from July and most of it is attributed to....you guessed it, Bank of America.

Bank of America is officially the biggest loser of the DOW for the quarter, down 42% and was the dunce cap award winner for the previous quarter as well. Bank of America is also one of the largest holders of derivatives and was downgraded along with Wells Fargo.

As Yves Smith puts it, Quelle Surprise the rules were thrown out the window the minute Bank of America, Wells Fargo demanded it and shall we say Too Big To Fail should really be redefined to mean Too Predatory to Exist.

Comments

moving your accounts

I personally move/close out accounts based on new fees or changes in interest rates and so on. What you do is just open a new one with some funds and some Internet banks, credit unions, you can open with nothing or $5 bucks, wait for all checks to clear in the old one and set up payments and so on in the new one. Then, close out the old one.

These financial institutions bank on people not closing out their accounts. But truly, if you want a vote, use your consumer choice one and it's also plain smart.

Another example are trading fees. People will pay $20 buck trades when you can find $5 buck, $7 buck trades all over, with the same execution speed, same features and so on.

I have interest bearing accounts with debit cards which gives cash back and free perks on top of it.

Why anyone would stay at these banks which offer nothing and even suck more money from consumers is beyond me.

Excessive Executive Compensation is the Heart of the Bank Crisis

Goldman Sachs has a problem. 50 Percent of the banks expenses are compensation and 80 percent of that compensation half is executive. Goldman is about to announce a loss. GS is not atypical. What feeds the current crisis is that almost all of Blankfein's income is deferred compensation in the form of Common Shares. Blankfein is one of the many overfed managment class at the banks worldwide.

Common Stock and profits are almost all of what makes up Tier I Capital under Basel II. The more the banks lose due to excessive executive compensation, the less bank capital. At the same time, banks need to issue more common, and participating preferred shares to bolster capital so the banks can lend.

The Fed? These idiots push more and more liability reserves into the banks causing the equity percentage to fall and the ability to lend decrease over time.

But banks cannot issue more common equity because levels of common shares (from executive compensation) are dilutive of primary earnings per share. The more the executives take in the form of common shares, the bigger the financial losses and because the compensation expense reduces earnings and creates EPS dilution.

Europe desparately needs to recapitalize its banks, America too. Recapitalization will not happen because the oxygen of earnings and equity is all sucked out of the collective economic room. Yes, there is class warfare and one class is the aggressor.

Burton Leed

reference, citation, link?

*that* is most interesting and I do not believe an article on the ratio of exec. comp to quarterly earnings has been done, at least I cannot recall one. I'd love to run some macro data on this one, but need some data references.

Agreed

I completely agree. I think it's partially out of fear. A lot of people are talking about bank collapses in general and I feel that many people believe that if large national chain banks can't survive what's going on with the economy then how is their money safe with the credit union?

Little do they know that credit unions are a better deal. The Wall Street Journal did a report on this last month:

http://online.wsj.com/article/SB1000142405311190392720457657718304922442...