First it was Bear Stearns. Then it was the Countrywide and the mortgage lenders. Then it was Lehman and AIG.

Now we have another banking crisis brewing, but this one is different because it's not from America. This one is from the other side of the Pond.

Jim Rogers, chairman of Singapore-based Rogers Holdings, said the “U.K. is finished” and investors should sell the currency.

...

“I would urge you to sell any sterling you might have,” said Rogers. “It’s finished. I hate to say it, but I would not put any money in the U.K.”

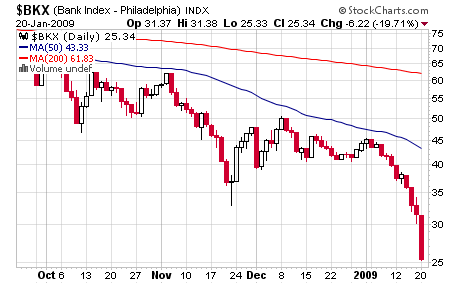

That's not to say that America isn't looking at another round of banking crisis as well. Bank of America is going to need another $80 Billion bailout or go under. The bank stock index has collapsed in the last few weeks.

New York University Professor Nouriel Roubini comes to some disturbing conclusions.

U.S. financial losses from the credit crisis may reach $3.6 trillion, suggesting the banking system is “effectively insolvent,” said New York University Professor Nouriel Roubini, who predicted last year’s economic crisis.“I’ve found that credit losses could peak at a level of $3.6 trillion for U.S. institutions, half of them by banks and broker dealers,” Roubini said at a conference in Dubai today. “If that’s true, it means the U.S. banking system is effectively insolvent because it starts with a capital of $1.4 trillion. This is a systemic banking crisis...

And yet the real source of the latest banking trouble doesn't come from Wall Street. It comes from the other side of the Atlantic Ocean.

Royal Bank of Scotland announced the biggest loss in British corporate history yesterday. The news triggered fears the bank would be nationalised and caused a bloodbath in shares across the sector, overshadowing the Government's latest financial bailout.Although some Labour MPs called for full state ownership, ministers insisted that was not their goal. But the Chancellor, Alistair Darling, did not rule out the move as a last resort, saying: "The Government has to continue to do whatever is necessary to get credit flowing."

The Lloyds Banking Group also took a beating in the last few days.

Britain has a limitation of size. Nationalization may not be an option.

Britain has foreign reserves of under $61bn dollars (£43.7bn), less than Malaysia or Thailand. The foreign liabilities of the UK banks are $4.4 trillion – or twice annual GDP – according to the Bank of England. The mismatch is perilous.

...

"If Spain can get downgraded, then the risks for the UK are self-evident," said Graham Turner, of GFC Economics. "The increase in the UK gross public debt burden – 11.8 percentage points in just one year – is troubling. The market rightly fears the long-term fiscal costs of a collapsing banking system. Rising Gilt yields are the main impact of the botched move from the UK Treasury."

That $4.4 Trillion in liabilities is 8 times the size of Lehman Brothers.

So the situation is thus:

* Major British banks are either insolvent or close to it

* Britain doesn't have the foreign reserves to cover the losses of these banks. If the government nationalizes the banks and it doesn't stop the crisis then it could easily collapse the entire currency

* The banks are too large to go bankrupt without creating a whole new worldwide banking crisis

Meanwhile the sufferings of Britain are being felt twice as hard in Ireland, where Irish bank stocks got massacred in the wake of the Anglo Irish Bank nationalization.

Ireland's own real estate bust, combined with the collapsing global economy, is threatening to force Ireland to pull out of the Euro currency.

"This is war: countries have to defend themselves," said David McWilliams, a former official at the Irish central bank."It is essential that we go to Europe and say we have a serious problem. We say, either we default or we pull out of Europe," he told RTE radio.

"If Ireland continues hurtling down this road, which is close to default, the whole of Europe will be badly affected. The credibility of the euro will be badly affected. Then Spain might default, Italy and Greece," he said.

There is almost nothing that Obama can do about this situation, other than take measures to make sure that our financial system is better run and more accountable to regulators.

Comments

Britain on the edge of bankruptcy

The realization is finally dawning on people.

This is what a post-nationalization problem looks like. What will our nationalization of Fannie Mae and Freddie Mac look like in two years?

I saw a post on the now defunct Technocrat.net

Way back at the beginning, last August, I saw a post from somebody who was well connected, if a bit strange, that British Banks were overleveraged 200:1 into the CDS market. It appears that assessment was right....

-------------------------------------

Maximum jobs, not maximum profits.

I hope they realize the fault begins with Thatcher

George Will does us the inestimable favor of affirming where the problems began, when he writes mournfully today,

Let's start analyzing

The possibility of nationalization and if it is indeed the path of least pain for the U.S.

While you are reporting the U.K. cannot nationalize I am seeing instead they will not.

Was Sweden with total liabilities in this level of boat in 1992? There they just said to the shareholders to any bank executive, sorry, bummer, you just lost all of your money and set the toxic assets to zero and they did not suffer any major collapse.

So, this is the next question, how to make worthless publicly that which is worthless and not collapse one's entire economy?