The May 2011 ISM Manufacturing Survey has some bad news. PMI plunged -6.9 percent points to 53.5%, from 60.4% in April. This is the lowest PMI since September 2009. PMI dropped 11.4% by percentages and this is worse than October 2008. This is the worst monthly drop in PMI since January 1984 by percent points.

New orders is even worse. It dropped -10.7 percentage points in a month to 51.0%.

Production, which is the current we're makin' stuff now meter, cliff dived -9.8 percentage points to 54.0%. Production correlates to the Federal Reserve's industrial production, which the May figures will be out mid-June.

Below is the ISM table data, reprinted, for a quick view. It's a blood bath of declines this month.

| MANUFACTURING AT A GLANCE May 2011 | ||||||

|---|---|---|---|---|---|---|

|

Index |

Series Index May |

Series Index April |

Percentage Point Change |

Direction |

Rate of Change |

Trend* (Months) |

| PMI | 53.5 | 60.4 | -6.9 | Growing | Slower | 22 |

| New Orders | 51.0 | 61.7 | -10.7 | Growing | Slower | 23 |

| Production | 54.0 | 63.8 | -9.8 | Growing | Slower | 24 |

| Employment | 58.2 | 62.7 | -4.5 | Growing | Slower | 20 |

| Supplier Deliveries | 55.7 | 60.2 | -4.5 | Slowing | Slower | 24 |

| Inventories | 48.7 | 53.6 | -4.9 | Contracting | From Growing | 1 |

| Customers' Inventories | 39.5 | 40.5 | -1.0 | Too Low | Faster | 26 |

| Prices | 76.5 | 85.5 | -9.0 | Increasing | Slower | 23 |

| Backlog of Orders | 50.5 | 61.0 | -10.5 | Growing | Slower | 5 |

| Exports | 55.0 | 62.0 | -7.0 | Growing | Slower | 23 |

| Imports | 54.5 | 55.5 | -1.0 | Growing | Slower | 21 |

| OVERALL ECONOMY | Growing | Slower | 24 | |||

| Manufacturing Sector | Growing | Slower | 22 | |||

Now we come to employment. where are the damn jobs? According to the ISM, anything about 50.1 correlates to an increase in manufacturing employment as reported by the BLS and we now have the best ISM manufacturing showing in 38 years. The unemployment report will be released June 3rd.

The manufacturing ISM employment index also dropped -4.5 percentage points, which correlates to an increase in initial unemployment claims and doesn't bode well for the unemployment report.

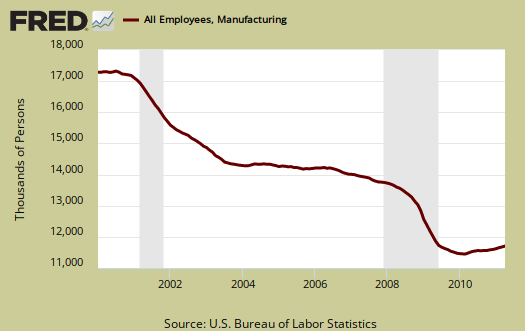

Below is the BLS manufacturing non-farm payrolls (jobs) for the past decade on the left (May's numbers are not released yet), graphed against the ISM manufacturing employment index on the right. The BLS number is simply raw manufacturing jobs tally, not taking into account population growth or overall sector shrinkage as well as time lag. One can eyeball a slight correlation in the middle of the decade, yet note the divergence this recovery, starting late 2008, to date. We're going to need a massive spike up from the BLS on Friday to correct this divergence.

Inventories contracted -4.9 to 48.7%. The ISM says inventories above 42.7% indicate expansion, but this is not a positive for Q2 GDP, which was 66% changes in private inventories for Q1 2011.

Exports dropped -7.0 percentage points to 55.0%.

Prices declined -9.0 percentage points to 76.5% and if the first time prices have dropped below 80 since December 2010.

In terms of which industries are officially contracting, the ISM lists Printing & Related Support Activities; Furniture & Related Products; and Food, Beverage & Tobacco Products.

The ISM has a correlation formula to annualized GDP, but they are now noting the past correlation, versus current, probably due to the meager 1.8% annualized GDP growth for Q1 2011.

A PMI in excess of 42.5 percent, over a period of time, generally indicates an expansion of the overall economy. Therefore, the PMI indicates growth for the 24th consecutive month in the overall economy, as well as expansion in the manufacturing sector for the 22nd consecutive month. Holcomb stated, "The past relationship between the PMI and the overall economy indicates that the average PMI for January through May (59.5 percent) corresponds to a 5.9 percent increase in real gross domestic product (GDP). In addition, if the PMI for May (53.5 percent) is annualized, it corresponds to a 3.8 percent increase in real GDP annually."

The ISM neutral point is 50. Above is growth, below is contraction, although the ISM is this report is noting some variance in the individual indexes. For example, A PMI above 42, over time, also indicates growth.

The ISM has much more data, tables and analysis on their website. For more graphs, see St. Louis Federal Reserve Fred database and graphing system.

folks you should scan these graphs, slowing economy!

I'll try to do a "big picture" of a lot of these recent economic reports as well as oil.

For now, high oil prices are strongly correlated to recessions and this report is astoundingly horrific in terms of change. We might very well be in for a "double dip", although, I think by any real world person, the "Great recession" never ended. Makes me also think the NBER should reconsider their "business cycle" classifications for those "long term downward trends".