While everyone has been focusing on the housing bubble bust, the commercial real estate market is collapsing at a record rate.

Commercial real-estate prices fell 7.6% in May, according to Moody's Investors Service, as both dollar volume and transaction count reached record lows in the nine-year history of the firm's Commercial Property Price Indices...The indexes are down 29% from a year ago and 35% from their October 2007 peak.

That 7.6% drop wasn't a year-over-year drop. It dropped 7.6% in just May.

In April it dropped 8.6%, thus making a two month decline of 16%.

Of course not everyone sees this as a bad thing. This near-Armageddon news for the commercial real estate market could still bring out bottom callers.

The index covering all property types is down 34.8 percent from its peak in October 2007, nearing the range of forecasts of total declines expected by many analysts. The acceleration of recent price drops could mean that the market will soon find a bottom, Moody's analysts said.

Translation: Things are getting worse at an accelerating rate, and have already equaled our worst-case scenario, thus it can't get much worse.

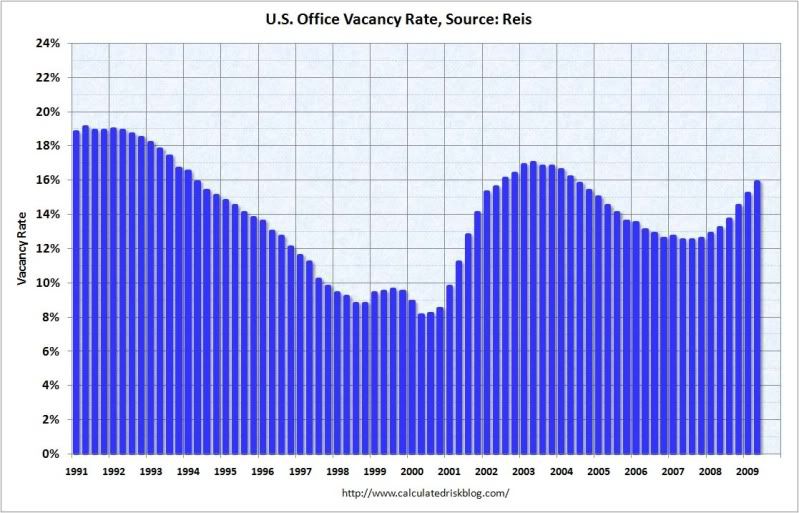

Office vacancy rates hit 15.9% in the second quarter of this year, while rents from office space fell by the most in seven years.

This implosion in the CRE market is filtering into the mortgage loan market with similar effects - near record losses.

U.S. banks have been charging off soured commercial mortgages at the fastest pace in nearly 20 years, according to an analysis by The Wall Street Journal. At that rate, losses on loans used to finance offices, shopping malls, hotels, apartments and other commercial property could reach about $30 billion by the end of 2009.

...

In contrast to home loans, the majority of which were made by about 10 lenders, thousands of U.S. banks, especially regional and community banks, loaded up on commercial-property debt.

The CRE bust, unlike the housing bust, is striking small regional banks. So far this year 57 banks have failed, more than all of last year.

Now I guess we know what Joint Economic Committee Chairwoman Carolyn Maloney meant when she said the CRE market was a "ticking time bomb".

5,315 commercial properties were in either default, foreclosure or bankruptcy by the end of June. Losses in the commercial mortgage-backed securities market is expected to peak at between 9 and 12 percent of the entire market.

So what is the government doing about it? The Fed's TALF program was designed to address this, but its effect has been minimal at best.

Investors only applied for $669 million of loans using old, or legacy, CMBS, as collateral, Reuters is reporting. No one requested loans from the New York Fed using new CMBS, but that’s hardly a surprise since the market has been frozen since last year.

...

Considering the amount of commercial loans estimated to mature this year - between $300 and $500 billion - TALF hardly looks like it’s going to save the day.

Comments

This is a problem for pension funds.

Obviously, these crashes don't happen in a vacuum. I am trying to find their exposure. I heard it could be at least $200 billion in CRE exposure.

RebelCapitalist.com - Financial Information for the Rest of Us.

it can't get much worse

in terms of labeling, perhaps this is the new terminology which should be used.

In watching the weekend flame out on calling a bottom (or not, with various insults flurrying about in bit land) on housing, this is the question I didn't see addressed (which you just did) CRE.

How big, overall, of a market is CRE in comparison to residential real estate?

Good question

I did a quick search and found this:

It's about 3 times the size it was after the S&L Crisis finished.

I can't find the size of residential, but I know that it is more than $10 Trillion

Excellent work

Midtown. Keep it up. And please crosspost to Big Orange.

I don't know if you've seen this, but thanks to the magic of globalization our less than stellar CRE market (and other casinos) are starting to rub of on European banks that invested during the bubble. Germany is facing the possibility of a credit crunch.

I know it isn't the market, but perhaps the Good Germans are about to show us a way the destructive power of big finance can be broke. Let the bad banks die, and raise up the functioning local credit unions (Sparkassen) in order to create credit for the real economy.

FYI on cross posting

we don't want all posts on EP over on agent orange, also it's kind of a "select" audience.

FYI in terms of reads, per post, believe this or not, but unless you get a the top of the recommended list, EP usually gets more reads per post than DK, probably because we're all econ. Even on the rec list, we've gotten more reads. We just have more lurkers, won't venture out to comment.

More pick off the other economics people (who are in depth, fact based, analytical) and get them over here! ;)

Maybe

you are right in page read terms, but I honestly think that in terms of impact that's probably not true.

And I honestly, there's a problem with preaching to the choir. You aren't going to save any souls that way.....

I crosspost because if I'm going to write something that's in depth, I want to spread it widely. I'm not going to do that for something I tag for instapopulist, but if I spend 3-4 hours on something I want to try to get it out to as many people as possible.

And if you don't have commenters you don't see that it's being read. Is there a way to put a page view count at the bottom of posts?

If you want to have a real impact, you can't stay in a bubble.

The problem with the blogosphere is that a division of labor has been established. You have to post at those places that have a broader focus if you want to have an impact.

I always post first at Economic Populist, and try to tweak the title so Technorati doesn't ring it up for daily kos.

impact, widely read

Yeah, that's a major goal here too, but another way to do that is to submit the post to share engines (see all of those buttons) and yet another way is to post a reference in a comment on other sites(has to have relevance, part of discussion) and even in article comment sections.

For in "preaching to the choir" EP has a pretty varied audience but DK is a world onto itself. I mean nothing wrong with it but DK is is one of those sites "onto itself" in terms of community whereas the financial blogosphere and others are more widespread....then things can travel viral, which has happened with some posts on EP. Other posts are referenced as articles. i.e. NDD's Great Depression series is in the reference section of Business Week. We have numerous of those.

Also, I think I need to incorporate twitter, this seems to be so popular.

Anyway, I see the stats and DK publishes the stats in a "high impact diary" section plus there are other ways of getting to them, so, I'm just letting you know. DK is massive but that's because there are so many posts on a daily basis, but most posts also have a shelf life of 24 hours max. EP shelf life is long lasting, at least 1 year and that's because of all of the search SEO I have.

I'm always working on ideas for building up the EP community (which we need more of) SEO, getting more traffic reads.

More Ratings Shenanigans?

Talk about very strange: S&P Restores Top-Rating to Commercial Mortgages

As early as just a few weeks ago S&P downgraded three commercial backed mortgage bonds. This made these securities ineligible for the Fed's Term Asset-backed Securities Loan Facility (TALF). But suddenly they reverse course today and restored the top rating for these bonds. Amazing how that works. This quote is from the article:

Wow. So now the market really opens up for these bonds. It is like "deju vu all over again".

RebelCapitalist.com - Financial Information for the Rest of Us.

why we're here

if you can track down what the truth is, esp. considering the midtowng blog post just showing all sorts of horrific reports on the commerical mortgage market, if you can dig out some facts, details, you may be very right.

I just saw a Bloomberg claim that Americans are "paying off their debts" and increasing savings. That is pure bullshit. The increase in savings I believe can be traced to the rebates and tax breaks, esp. to Senior citizens from the Stimulus bill. I don't have time to verify this with references, citations....

and that's what happens, when bloggers lay off, when the public spotlight turns off, out comes the snow job in masse. The shit gets piled high and deep and it really takes a lot of digging from a lot of people who aren't getting paid to do so!

Great Devastating Graph

Its really a depressed graph is showing on above, this was an really a historical fall on Real Estate agencies.