The Senate Subcommittee on Investigations held a hearing, Offshore Profit Shifting and the U.S. Tax Code. Did you know U.S. Multinational Corporations have more than $1.7 trillion in untaxed profits stashed as undistributed foreign earnings and keep at least 60% of their cash overseas? That these earnings have increased 400% in the last decade? That corporate tax as a percentage of total Federal revenues has dropped to only 8.9%?

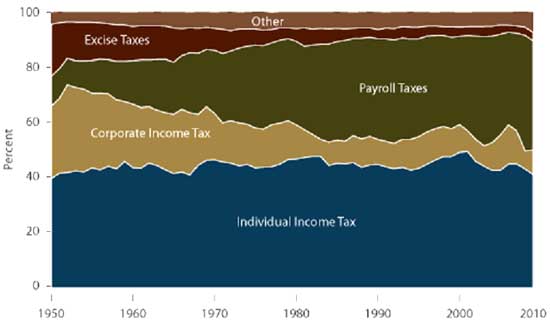

At its post-WWI peak in 1952, the corporate tax generated 32.1% of all federal tax revenue. In that same year the individual tax accounted for 42.2% of federal revenue, and the payroll tax accounted for 9.7% of revenue. Today, the corporate tax accounts for 8.9% of federal tax revenue, whereas the individual and payroll taxes generate 41.5% and 40.0%, respectively, of federal revenue.

These and other damning facts make the committee hearing exhibits a must read. On the Senate hearing hot seat was Microsoft and Hewlett Packard. Both of these tech companies have fired thousands of U.S. workers, offshore outsourced thousands of jobs and to this day spend millions lobbying Congress to import more foreign workers. In the midst of their never ending layoff bloodbath, Microsoft and HP claim they cannot find tech workers, a very obvious lie.

The hearing exhibits has some real gems to show how these two companies are more in the business of manipulating the international corporate tax code than designing much. No surprise since both corporations slashed and burned their U.S. citizen R&D staff, which shows in their products and declining market share.

Microsoft Corporation has used aggressive transfer pricing transactions to shift its intellectual property, a mobile asset, to subsidiaries in Puerto Rico, Ireland, and Singapore, which are low or no tax jurisdictions, in part to avoid or reduce its U.S. taxes on the profits generated by assets sold by its offshore entities.

While America needed jobs, Microsoft was busy shifting profits offshore from 2009-2011.

From 2009 to 2011, by transferring certain rights to its intellectual property to a Puerto Rican subsidiary, Microsoft was able to shift offshore nearly $21 billion, or almost half of its U.S. retail sales net revenue, saving up to $4.5 billion in taxes on goods sold in the United States, or just over $4 million in U.S. taxes each day.

Not to be outdone, HP has been busy transferring profits back into the United States, untaxed through another corporate tax code rig up.

Since at least 2008, Hewlett Packard Co. has used billions of dollars of intercompany offshore loans to effectively repatriate untaxed foreign profits back to the United States to run their U.S. operations, contrary to the intent of U.S. tax policy.

Subcommittee hearing chair Carl Levin pulled no punches in his opening hearing statement:

The share of federal tax revenue contributed by corporations has plummeted in recent decades. That places an additional burden on other taxpayers. The massive offshore profit shifting that is taking place today is doubly problematic in an era of dire fiscal crisis. Budget experts across the ideological spectrum are unified in their belief than any serious attempt to address the deficit must include additional federal revenue. Federal revenue, as a share of our economy, has plummeted to historic lows – about 15 percent of GDP, compared to a historic average of roughly 19 percent. The Simpson-Bowles report sets a goal for federal revenue at 21 percent of GDP. The fact that we are today so far short of that goal is, in part, due to multinational corporations avoiding U.S. taxes by shifting their profits offshore.

In other words, America is broke and multinational corporations continue to blood suck the United States dry. This is a great hearing, loaded with facts and figures on the corporate tax code. The pattern becomes clear, U.S. Multinational corporations are out to not pay taxes,

All of this is perfectly legal. Microsoft and HP along with a host of other companies manipulate the U.S. tax code through transfer pricing and loopholes. The tax law in question is subpart F, section 956 and FASB accounting standard, APB 23.

Sounds like something out of the Hitchhiker's Guide to the Galaxy and in a way it is. Corporations only pay tax on active income, but it is called deferred income if left offshore. Passive income from royalties, patents, intellectual property though, the tax is supposed to be paid, offshore or not.

Subpart F is often referred to as an “anti-deferral” regime. It is only active income of a CFC that may be deferred until repatriated, but passive income earned by a CFC such as royalties, dividends and interest is currently subject to U.S. tax and reportable under Subpart F regardless of whether the earnings have been repatriated

Deferral is why multinational corporations leave profits in other countries, offshore, so they don't have to pay U.S. tax. Corporations are literally shifting income (and people) offshore, in part, to avoid paying their taxes. This is what they mean by undistributed foreign earnings. The list of corporations keeping profits offshore is a who's who of multinational giants. Cisco, G.E., Apple, Google, Pfizer, Qualcomm, Walmart, Ebay, Dell, even Coca-Cola. Apple, for example, has $74 billion in profits parked offshore.

The U.S. Treasury found it was not sales causing foreign profits parked offshore to swell, instead it was their manipulation of international corporate tax codes.

The differential between a company’s U.S. and foreign effective tax rates exerts a significant effect on the share of its income abroad, largely through changes in foreign and domestic profit margins rather than a shift in sales.

Transfer Pricing

Transfer pricing is a fancy way of saying multinational corporations "sell" something to their foreign affiliates and to make profits look real good they set the price on these "sales" to absurdly low levels. Imagine a corporation "sells" to their offshore outsourced R&D unit in India services they provide. But instead of the retail price of $200,000, the U.S. multinational "sells" those services to their affiliate for 1¢ It's much more complex than that, all sorts of services, patents, intellectual property and licensing rights are "sold" to their foreign affiliate oompany, all to move profits offshore. From the exhibit (MNC means multinational corporation, CFC is the foreign affiliate of that MNC):

One way that income shifting occurs is when a MNC sells or licenses the foreign rights to intangible assets developed in the U.S. to its subsidiary in a low-tax country. For example, a U.S. parent may license the economic rights of its intellectual property to a subsidiary located in Bermuda, a subsidiary which, in many cases, was created for that purpose. Once the foreign subsidiary owns the rights, the profits derived from the technology become those of the subsidiary, not the parent.

The license payment made by the subsidiary to its parent is taxable income, but the parent has an incentive to set the price as low as possible. If the price paid is low compared to future profits generated by the license rights, less income is taxable to the parent and the subsidiary’s expenses are lower. Thus, the U.S. parent has successfully shifted taxable profits out of the United States to Bermuda, where no corporate taxes apply.

Let's say one holds a critical patent on the iPhone. Apple would then sell that patent to some special purpose company they had set up in the Cayman Islands for licensing rights. Then that PO BOX tax haven affiliate in the Cayman's would reap all of the profits associated with licensing those patent rights to others as well as Apple themselves. Slick trick huh?

Loaning Back to the Parent Company

This one is a classic. There is a loophole in the tax code which allows foreign subsidiaries, like the one above, created in the Cayman's, to offer a short term loan to the U.S. parent company without paying tax. It's all done by timing these loans, issued one after another to avoid a tax time window and is, in effect, a way to transfer foreign profits back into the United States without paying taxes.

Uncle Sam Helps Offshore Outsource Jobs

The tax code gives a permanent tax break to corporations if they invest their offshore profits in foreign countries. I kid you not.

Another incentive to shift or keep profits offshore is provided by an accounting standard known as APB 23, recently renamed ASC 740-30-25.

APB 23 permits U.S. multinationals to defer recognition of tax liability on foreign earnings for financial reporting purposes so that earnings are not reduced by the tax liability if they affirmatively assert that their foreign earnings are permanently or indefinitely reinvested. In 2011, more than 1,000 U.S. multinationals made such an assertion in their SEC filings, reporting in total that more than $1.5 trillion is or is intended to be reinvested offshore.

Gets worse than that. Of these funds declared permanently reinvested offshore, a study found that 46% of it was sitting in U.S. bank accounts, buying up stocks in other U.S. companies or U.S. treasuries.

Reforms

Now the above are clearly no brainer corporate tax code problems that should be fixed. Wouldn't it be much better to give corporations a 0% tax if they invested their profits in America? How about a 0% tax for every U.S. citizen they hire and retain? How about even a tax credit for every worker they offer on the job training to? When it comes to R&D, that's a permanent, long term tax credit!

Yet, Congress cannot get it together and do the practical and the obvious. Plug up these loopholes and use the corporate tax code to get these companies to hire U.S. citizens. Why? In part because multinational corporations with their lobbyists demand their crack cocaine tax loopholes and will stop at nothing to keep them. Damn logic, damn spreadsheets and damn America, these MNCs want their global international tax code stupid hat tricks. Here are the reform recommendations from the exhibit.

- Reform Tax Provisions that Encourage Offshoring of Profits. Reform tax code Sections 482 and 956 regarding transfer pricing and offshore loan practices, and the check-the-box and CFC look-through rules, that encourage U.S. multinationals to transfer and keep profits offshore and untaxed.

- Issue APB 23 Guidance. FASB should re-evaluate whether the indefinite reversal exception to ABP 23 is being used by multinationals to manipulate their earnings reports, and issue additional guidance or restrictions to clarify how the standard should be applied.

- Use Anti-Abuse Rules. The IRS should make greater use of its anti-abuse rules to stop offshore schemes and transactions that substantively violate the intent of the code, but are structured to appear to meet the most technical reading of, the tax code rules governing the taxation of offshore income.

Think any of them will get done? Not a prayer's chance unless you, dear public, start studying documents such as the ones presented at this hearing, write to your Congressional representatives, raise hell and don't stop until these loopholes are plugged, once and for all.

Comments

Enjoy benefits of US incorporation - you must pay fair share

Real simple solution in a sane world (not the one where the corporate criminals get to write the laws because they own the lawmakers) - if you want to enjoy the benefits of being incorporated in the USA, then you must pay your fair share of taxes. This report obviously shows the average American is picking up the burden that corporations have shifted to us by crony capitalism, despite the endless ramblings by "news" shows telling us corporations are so overburdened with taxes and regulations (despite their records profits recently and the Forbes list showing the well-to-do are actually getting richer) they simply cannot cope. We get the greater tax burden, the middle class is disappearing as a result of greater taxes and fewer opportunities to pay those taxes also because of corporate actions and laws (e.g., outsourcing and visas), but corporations with no taxes, greater subsidies, are prospering?

Pretty obvious we're being screwed left and right.

If corporations continue to refuse to bear their fair share in the US where they enjoy our federal, state, and local governments' protection and lobbying for them here and abroad, by all means, incorporate where the majority of operations take place, whether that is in Communist Corporate China, or the Philippines, or Bangladesh, or somewhere else. You want to take advantage of our Commerce Dept. flying out with you to lobby for megacontracts with other nations (e.g., Boeing fighting for contracts over Airbus with US Govt. assistance vs. EU), or take advantage of our FBI pursuing IP theft cases in US courts, or the State Dept. lobbying for you in the WTO with our Trade Rep., or oil companies relying on our State Dept. and DOD to protect them in places like the Middle East and Nigeria when things go bad, then you owe the tax burden of that government assistance. Same as a barely surviving family has to pay property taxes for schools and police and fire, and payroll taxes (which this article shows we are paying more than our fair share of), etc., then the big boys and girls that own our government can pay their fair share for those services even fellow Americans don't get (no average citizen has the access or power to even communicate with our federal govt. on a regular basis, let alone get our govt. to represent us in international bodies, build roads for us, give us tax abatements solely for us, or anything else megacorporations get).

If these companies simply refuse to pay for the services they receive at our expense, then they really need to incorporate overseas and see how well do without our govt. backing them up. Let's see how the courts treat them in Beijing or Algiers or Lagos or Islamabad when a crowd of workers demand justice and the local courts demand the CEO appear in court - imagine Bill Gates (back when he was CEO) or Jamie Dimon or an oil exec pissing their pants because that's what would happen. Those places are no joke when things go wrong or the local government wants to send a message, and when folks like that step out to see what the real world is like, boy will they be in for a shock when the US Govt. isn't there to protect them.

Hit the links

On purpose, the corporate tax code is impossible to navigate, even overview without people getting confused and falling asleep. That's on purpose. Lobbyists hide the most egregious things with obscure semi-colons and opaque rules. I strongly recommend at least reading the exhibit linked above. They do a pretty good job in making the issue clear without over simplification.

I find it very interesting our favor "worker shortage" whiners are the ones who have really labor arbitraged the shit out of America. That's Cisco, Microsoft, HP, Oracle and they are some of the worst offenders here.

Tax code is just a tool for the thieves to obfuscate the theft

It's the same old cast of characters hard at work, megalaw firms, the same old accounting firms, etc. Megacorps. hire the lobbying and law firms to write the laws, the laws get passed by the same politicians they just lobbied and provided with the laws they wrote, and then the politicians go straight to the law firms and lobbyists to help "interpret" the same laws they just passed because damn it, working for money and as a "public servant" is so leech-like, and real geniuses don't work for the public's money, they get their money for nothing. Same with the tax code, law firms and lobbyists help write the laws/insert the breaks and subsidies targeted to their specific clients, the firms help the politicians interpret the tax laws, and on and on it goes. This ain't capitalism and democracy, it's a system we're purposely left out of.

My neighbors and I just lobbied for our own tax code and tax abatements in our own state capital and DC that we got passed by the same politicians we got elected with Super PACs, and when the politicians can't figure out what they just passed and why there's a fiscal cliff when the middle class simply can't bleed anymore, my neighbors and I will step up and explain to the politicians in closed door meetings why the middle class needs to bleed, like a stone, because damn it, STONES WILL BLEED when oligarchs demand it. Just kidding, I'm not an oligarch, but I've seen them on TV when they come out of the shadows and kids will dress up like them next month.

Anyway, check out accounting firms and law firms and consulting and lobbying firms still loving that corruption and tax crap in 2012 like it was Enron back in the day using shell companies, nightmarish tax havens, and blacking out the State of California while energy traders were laughing about screwing over "grandma Millie": "Yeah, grandma Millie, man. But she's the one who couldn't figure out how to fuckin' vote on the butterfly ballot." Yuppers, we're all Grandma Millie now. And the money laundering, aiding terrorists and drug cartels, market manipulation, tax evasion, and full-blown destruction continues full speed ahead, democracy and America be damned.

Starbucks - Venti tax evasion, please, and a venti F U

Saw someone say Starbucks had an obligation to find every way possible to not pay taxes - and it's all legal because big corporations and their political puppets allow it. Ethical? Come on, 2012, ethics are so antiquated. The same rules apply to the 99% too, right? Gosh, officer and IRS Agent, it's my obligation to avoid paying my fair share, following the laws the "peons" must follow, and on and on and on. These people love the American politicans that serve their interests and are rented for a very low price, but bearing their fair share and helping finance schools, roads, airports, law enforcement, the infrastructure they use every single day to make their profits and the people that buy their overpriced crap daily, well, they apparently don't matter too much. Venti tax bill, Starbucks, no foam with that you asshats.

Taxes? Fair share? Poppycock!

The only fair share is no taxes for anyone at all.....for now. The system is broken. It can not be fixed. we need to start over. The only thing the Banksters, corporate criminals and Washington thieves understand is money. If we all stop giving it to them maybe we can get some stuff done.

The only reason we pay taxes at all is because we think we have to. We give our own authority to tax collectors. They work for us people. What if we just don't authorize them to collect taxes anymore?

Why do they hate us?

"The tax code gives a permanent tax break to corporations if they invest their offshore profits in foreign countries. I kid you not. "

Seriously how corrupt is our congress? Who passed this kind of crap tax dodge? Why do they hate their own citizens. Gosh I hope their patents are protected in these wonderful countries loved by our corporations. So much for the enlightenment of our founding fathers. Entitlements my ass. We are entitled to nothing here. A job? No. Food? Sorry. Social Security? Ha, Ha stolen.

I remember a book "Snow Crash" when we all make the same as a pizza delivery boy in Pakistan this will end. I don't doubt tipping is a sin there too. We can burn movie theaters while we hang out in the streets.

that tax break is temporary but it's for "permanent" investment

Good question and I strongly suggest reading the exhibit and watching this hearing.

Also, Citizens for Tax Justice has some posts which break down the tax code is easier to understand terms (but still detailed).

I have Snow Crash on my shelf, I'll have to go crack it now.

I feel the way you do, it seems it's "anybody but the U.S. citizen", "anybody but the U.S. worker" and it does feel like hatred towards Americans and by those in power in this country no less.

Sure seems that way, why anyone would put this in the tax code, either a liberal wanting to play games with foreign policy through corporate dominance or yet another lobbyist, corporate favor.

Look at stadium/arena names to show who owns us

Just for kicks, quickly examine who now owns the stadiums and arenas where the increasingly poor American can no longer afford to take his family. A really bad/good example: Barclays Center in Brooklyn, yes, the same Barclays busted for LIBOR fixing. The new home of the Brooklyn Nets (formerly NJ Nets). Remember families could go have fun watching their local teams in stadiums or arenas named only after the city or franchise and not a corporate sponsor? And it was affordable? But now it's impossible to attend a game just because of the ticket prices (not even including food, souvenirs, tolls, and parking). And the corporate boxes get more and more luxurious, the arenas carry the names of banks or other corporations, and the arenas get big tax breaks that the local communities have to fund through bond sales or other means (while also having to take care of traffic, police, and other issues). It's just another symptom, but one people can see whenever they watch a game from home.

folks, help out, share this article on other sites please

We all know Romney claimed there is no tax break for offshore outsourcing jobs. There indeed is and then some, but because the corporate tax code is so complex, one has to follow the details to understand how the trick works.

This article overviews some of those tricks. Obama is right, Romney is not only wrong, he wants to give tax loopholes to offshore outsourcing jobs an absurd increase in tax breaks by changing the status of territories outside the U.S., known tax havens, to be defacto U.S. lands for tax purposes! Major disaster in terms of trying to keep jobs in America.

Anyway, this post overviews the details on how the corporate tax code rewards offshore outsourcers and if you do not like this overview, the actual hearing exhibit does a good job in boiling down the complex so we all can follow along at home.

Seriously, the press with their "fact check" is burying this fact!

Truly,the Fool Has Said in His Heart:No Foreign Tax Credit

Here it is for the record. As an attachment. The I.R.C. Section 4.6.10. My dad and I worked in this stuff, even though he was a Libertarian Republican, he like many patriots despised the FTC. This is the work of the Chamber of Commerce and the Jack Welchs of this country. This is the world and substance of the outsourcers who have ruined this country's industrial base. Liberals like Matthews are

far to kind to the predators.

Take a look in the mirror Jack(W), you like conspiracies. Here is your favorite and that of your buddies in the Chamber of Commerce have used to keep your foot on the necks of the American worker and send our jobs offshore.

You say the USDOL Unemployment numbers are a conspiracy? Take a look at your conspiracy to gut GE and the rest of the Industrial Base. The double taxation in the Code Section refers to the ability to get a credit for U.S. Corporate tax for paying taxes to foreign countries, say China. In other words, when you box a factory in Ohio and send it to China, you get a credit on your U.S 1120 for the

tax you pay in China. The Chinese will also give you credit, land, water, labor and innumerable other subsidies that you and the rest of the U.S. corporate Pond Scum will

be delighte to accept.

What many refer to a "Free Trade".

"

4.61.10.1 (05-01-2006)

Foreign Tax Credit Audit Guidelines

The purpose of the Foreign Tax Credit (FTC) is to provide relief from double taxation. Double taxation may occur, for example, when the U.S. taxes foreign sourced income. FTC limits the overall tax rate on foreign sourced income to the higher of the taxpayer's foreign or U.S. tax rate. The United States does not impose additional tax on foreign income when the foreign tax rate is higher than

the U.S. rate. Conversely, if the tax rate on the foreign sourced income is lower than the U.S. tax rate, the FTC causes the overall tax on the foreign income to approximate the U.S. rate.

This table summarizes the Code sections that authorize and limit the FTC:

Summary of IRC Sections Authorizing and Limiting the FTC

Code Section Description

901 Allows direct credit for taxes paid to a foreign country by a U.S. taxpayer based on realized net income.

902 Allows deemed paid or indirect credit for foreign taxes based on the proportion of taxes paid by a corporation on its distributed earnings and profits.

903 Allows direct credit for taxes (typically foreign withholding taxes based on gross receipts) and paid "in lieu of" the generally imposed net income tax.

904 Limits the amount of credit available in each year, including carryovers of credit.

905 Provides guidelines on foreign tax adjustments, redeterminations and proof of credits.

906 Allows the foreign tax credit for nonresident alien individuals and foreign corporations engaged in a trade or business in the United States.

907 Contains credit limitation for foreign oil and gas income.

960 Allows an indirect credit for deemed distributions.

There are two types of FTCs.

Direct credits are for taxes withheld or taxes paid on the profits of a foreign branch.

Indirect or deemed paid credits are for taxes paid by foreign corporations with 10 percent U.S. shareholders.

There are two types of FTCs.

Direct credits are for taxes withheld or taxes paid on the profits of a foreign branch.

Indirect or deemed paid credits are for taxes paid by foreign corporations with 10 percent U.S. shareholders.

4.61.10.1.1 (05-01-2006)

1986 Law Changes

The FTC regime changed in 1986. For tax years after 1986, taxpayers must:

Maintain multi-year pools for undistributed earnings and taxes of foreign subsidiaries for purposes of calculating indirect credits

Categorize income into nine or more baskets, each with a separate limitation

The foreign source income categories are:

Passive income

High withholding tax interest

Financial services income

Shipping income

Dividends from each noncontrolled IRC section 902 corporation [See IRM 4.61.10.9.1(5).]

Dividends from a DISC or former DISC

Taxable income attributable to foreign trade income

Certain FSC distributions

All other income (general limitation)

Note:

The taxpayer may have certain types of income segregated into additional baskets such as income from blacklisted countries and income treated as foreign sourced under a tax treaty. [See IRC section 901(j), IRC section 904(g)(10), 246(a)(10), and IRC section 865(h)(1)(B). ]

IRC section 904(d) provides that the FTC limitation of IRC section 904(a)–(c) applies separately to the income in each basket.

If a distribution is from pre-1987 earnings, the old rules apply. Pre-1987 earnings and profits and taxes use a separate calculation for each year. After the 1986 Act, taxpayers main Eligible Taxpayers

The first step in an FTC examination is to assess the taxpayer’s eligibility for the credit. Taxpayers subject to U.S. taxation on foreign sourced income are generally entitled to the FTC.

US. citizens and domestic corporations may generally claim a credit for the eligible foreign taxes they pay or accrue. Foreign taxes paid on the following types of income, that are generally exempt from U.S. taxation in the hand of U.S. citizens, are not eligible for a FTC.

Income from sources within possessions of the United States by certain bona fide residents of the possession [see IRC sections 931, 932, and 933]

All excluded foreign earned income [See IRC section 911(d)(6)]

Foreign corporations and Individuals and corporations residing in a U.S. possession (except Puerto Rico) that are not otherwise citizens and not residents of the United States are generally not subject to tax on non-US source income and so are not entitled to the FTC .

4.61.10.2.1 (05-01-2006)

Resident Aliens

Resident aliens in the United States are subject to U.S. taxation and are, therefore, eligible for the FTC. The following limitations apply:

The general rules applicable to U.S. citizens apply to this category of taxpayers.

Only those foreign taxes on income earned while in the status of a resident are eligible for credit (consult the specific treaty involved).

Aliens residing in U.S. possessions (excluding those in Puerto Rico for the entire year) do not get the benefit of the FTC since they are not generally subject to U.S. taxation on non-U.S. source income.

4.61.10.2.2 (05-01-2006)

Other Taxpayers

Nonresident aliens and foreign corporations are eligible for FTC relating to qualified taxes paid on foreign source income effectively connected with a U.S. trade or business (See IRC section 906). A flat 30 percent tax (or lower treaty rate) applies to investment and other fixed or determinable periodical income whether or not the recipient engages in a trade or business in the United States.

Burton Leed

The Way Around the FTC

The reason for an impassioned plea for a tax holiday putting the money back onshore. The Foreign Tax Credit, the name of the Beast, is not temporary.

Obama and the Democrats lost the battle to repeal the FTC. If there is one reason, and one reason only to re-elect the President, in spite of his flaws and weaknesses, it is his unflinching opposition (expressed in the Presidential Debate) against the Foreign Tax Credit.

If there is only one reason to oppose Romney, it is his denial that there is a problem with the Foreign Tax Credit.

Burton Leed

The Way Around the FTC is Move Money to Industrial Assets

The option to rebuild America industry, must not be an option.

In 2008, we made the historical case for success vs. failure,

for economic systems which could not support industrial activity.

To move money to fixed investments means create the incentives

to move the offshore money back directly to Fixed investment

as we said in "Back to the Future". All fixed personal property (IRC Section 167) are the appropriate targets of all tax incentives. In other words, no 167 property you pay tax, corporate or personal.

Burton Leed

Foreign Source Income of Manufacturers - The Shell Companies

The empirical case for outsourcing is on the tax returns of the remaining onshore shell companies who continue to designate themselves "domestic", for the IRS. We Know these companies are the provinces of their offhore masters.

http://www.irs.gov/pub/irs-soi/10intertax.pdf

Burton Leed

Burton Leed

I'm saying submit this post to other sites in the comments, use the share buttons, put on Facebook and so on. You're right about Jack Welsh but most people do not understand how the corporate tax code is rigged to offshore outsource jobs, or how the corporate tax code is rigged generally.

Posting some FTC stuff doesn't help because people need to have this stuff explained in very simple English to understand.

Hell, to write up this overview I had to study some tax code plus review the hearing documents and exhibit. It ain't easy to boil it down.

No, Not a Prayer's Chance for Soft Regulation

I learned from experience in the 70's

and that of academic superiors that soft regulation,driven by industry, is regulation controlled by industry. Hard regulation, controlled by an agency with 3 letters works, for a while. That means you do what I had to do in the 80's: work for a prosecutor like Rudy, under a powerful bureau, and an use the rules to bust the worst of the worst. Like Brad Pitt in "Fight Club", you learn you can upset the establishment for a little while, before they regain control.

Try to listen to a guy who was the point of the spear for busting the worst of the worst. Those soldiers are like Patton. They win battles but never rise to the political power. in this system, of an Eisenhower.

The powers shot down Occupy in New York and elsewhere, they behaved just like the 3rd Reich

by destroying books and computers. Local governments are more corrupt than those who existed in the days of Boss Tweed. with greater transfers of wealth from municipalities to MNCs.

The one answer left is the one we must dread the most. The one answer that they cannot co-opt: violent revolutions, worldwide.

Burton Leed