Two years ago Friday the financial crisis started.

Most financial media pundits and politicians didn't recognize that we had a problem until Lehman Brothers went under on September 15, 2008. The official start of the recession is marked at December 2007.

But the real start of the financial crisis was July 31, 2007, when Bear Stearns filed for Chapter 15 bankruptcy protection on its two major hedge funds (High-Grade Structured Credit Fund and High-Grade Structured Credit Enhanced Leveraged Fund).

And yet 24 months later, after all the job and capital losses, after all the heartbreak and stress on the average Americans, the financial media, the politicians, Wall Street, and most of the blogosphere still refuses to even acknowledge, much less address the root causes of our economic problems.

Of course the Bear Stearns hedge fund bankruptcy filing wasn't out of the blue - more than a month earlier Bear Stearns tried bailing out the funds. In fact the stress in the credit markets had been building since March of 2007 when New Century Financial went under.

However, the Bear Stearns crisis was different for a very basic reason - the assets of the funds would have to be liquidated because of the bankruptcy filing.

A sale would give banks, brokerages and investors the one thing they want to avoid: a real price on the bonds in the fund that could serve as a benchmark. The securities are known as collateralized debt obligations, which exceed $1 trillion and comprise the fastest-growing part of the bond market.

Because there is little trading in the securities, prices may not reflect the highest rate of mortgage delinquencies in 13 years. An auction that confirms concerns that CDOs are overvalued may spark a chain reaction of writedowns that causes billions of dollars in losses for everyone from hedge funds to pension funds to foreign banks....

"Nobody wants to look at the truth right now because the truth is pretty ugly," Castillo said. "Where people are willing to bid and where people have them marked are two different places."

The credit markets almost immediately froze up.

The market for mortgage bonds has become "very panicked and illiquid," CEO Michael Perry wrote in e-mail to employees yesterday..."Unlike past private secondary mortgage market disruptions, which have lasted a few weeks or so, our industry and IndyMac have to be prudent and assume that this present disruption, which appears broader and more serious, might take longer to correct itself," Perry wrote.

And that, in a nutshell, was the reason for the worldwide financial crisis - the mispricing of assets, mostly mortgage-backed securities, based on fictional financial models.

The reason for all this economic hardship wasn't because the government taxed too much or spent too much.

It wasn't because the Federal Reserve raised interest rates or contracted the money supply.

It wasn't because the American consumer stopped spending.

It was because the financial system knowingly overpriced a major financial asset class, and then leveraged itself against that asset class in the vain hope that the Day of Reckoning never came.

It's really quite simple when you break it all down.

And yet every policy response to the financial crisis, without a single exception, has been designed to:

a) cut taxes and interest rates,

b) boost the money supply, as well as government and consumer spending, and most of all,

c) to prevent the asset class in question from returning to real market prices.

It's insanity. Plain and simple.

The Elephant In The Room

It is technically possible that the economy might produce some very weak growth in the next few quarters. I wouldn't bet on it, but with the unprecedented government bailouts and deficit spending all over the world, I can't rule it out.

These bailouts, designed to prop up the financial institutions that caused this mess, and the deficit spending, designed to mortgage our future in the hopes of a quick economic boost now, are a fool's hope.

Why? Because the sources of all our economic problems remain in place - debt levels and the prices of it.

To use an analogy that is easy to understand, when you catch a cold you will have several symptoms. You will run a temperature. Your head and chest may become congested. Your eyes may get scratchy.

These are all symptoms, but not the disease. If you got rid of all the symptoms would you be healthy? No. You would still be infected. Your body uses these methods to rid itself of the disease - the cold virus.

The same thing applies to the economy today.

Consumers need to cut back on their spending and pay down their outstanding debt (or default on it), after decades of living beyond their means, so their balance sheets can be healthy again. Banks need to write off hundreds of billions of dollars of bad loans so that their balance sheets can be repaired and they can afford to loan money again.

These are painful symptoms, but they are necessary for the economy to become healthy again. Without these symptoms the economy will still be burdened by mountains of non-productive debt and unable to move forward.

If Some Is Good, More Is Better?

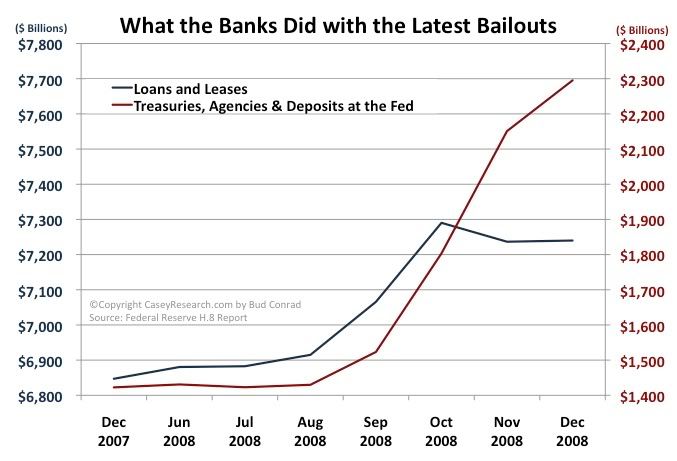

On April Fools Day, the Financial Accounting Standards Board bowed to Wall Street pressure and agreed to revoke Mark-to-Market accounting rules for the banks. Thus the banks returned to the Mark-to-Fantasy accounting rules that existed back in 2007, the same rules that got us into so much trouble to begin with.

You may have noticed the blow-out profits by the big Wall Street banks this past quarter. Were those profits real? No, they were fake.

It’s hard not to be skeptical after the financial community made the choices it did last week. Rather than come clean with the brutal truth that the banking business stinks and the investment banking business isn’t much better, the biggest firms chose to obfuscate, be dim, mislead and camouflage what in reality was the kind of crummy quarter one would expect in the middle of the worst recession since World War II.

To make a simple analogy, let's say you purchase a used car for $10,000. Afterward you discover that the transmission is shot, the engine needs to be rebuilt, and there is rust under the paint.

You then try to sell the car to someone else, but no one will pay more than $2,000 for it. "But I paid $10,000 for it. Therefore that is what it is worth," you say. You then take the car off the market and announce on your income tax forms that it is still worth $10,000. Meanwhile the car continues to rust in your driveway.

That's what the Wall Street banks are doing with toxic mortgage-backed securities on (and off) their books. They then claim that their investments haven't lost any money so they can claim large profits, which in turn become large bonuses for the executives.

Even more important, keeping all that bad debt has its consequences. The banks must hoard capital, much of it taxpayer bailout money, to pay for the real losses that one day will need to be addressed. It can't afford to take chances on loans. That's what happened in Japan in the 1990's, and is being copied here in America today.

"I thought America had studied Japan’s failures," said Hirofumi Gomi, a top official at Japan’s Financial Services Agency during the crisis. "Why is it making the same mistakes?"

There's been a lot of talk about Green Shoots recently, and even a bottom in housing. Before we all start singing "Happy Days are here again" we should all take a step back and remember that the guys pushing the Green Shoots are the same guys who lied to us before.

So let's look past the spin and take a look at the real numbers and see what they tell us. Since the housing market is what got us into this mess, we need not look any further than that.

In particular, foreclosures soared to new record highs in June, LPS found: The national foreclosure inventory rate during June was 2.86%, up 2.5% from one month earlier and a huge increase of 86.1% from year ago levels. Total delinquencies rose as well, to 8.58%, up 44% from one year earlier.

...

New foreclosures are on the rise, as well. “Foreclosure starts in June increased 1.6 percent to the second highest level on record, while reinstatement and recidivism rates are not yet showing signs of improvement,” LPS said in a statement.

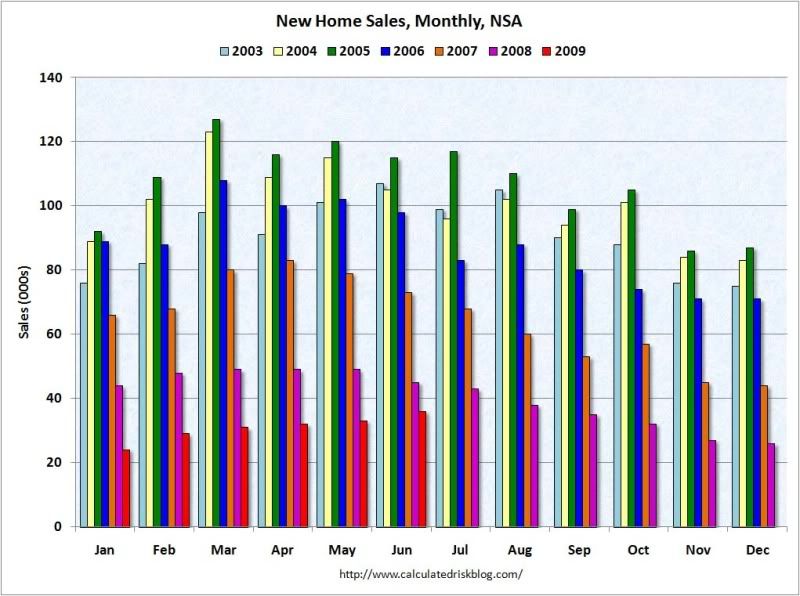

OK, so foreclosures are as bad as ever, but what about home sales? You probably heard some good news about new home sales recently.

New-home sales soared in June from the previous month, the third increase in a row and supplying fresh evidence the housing market is beginning to recover from its long crisis.

It sounds good, but there are several extremely dishonest items about this news article. For starters, they wait to mention that homes sales year-over-year are down 21.3% and that prices are down both year-over-year and monthly as well.

The increase was the fourth in six months, as buyers take advantage of falling prices. It appears new-home sales reached a bottom in January, at a level of 329,000, and that the market is beginning to recover slowly.

The next dishonest thing about this article is that they are using non-seasonally adjusted numbers. The fact is that the home sales market is very seasonal, with the majority of sales happening during the spring and summer months. When you take a look at the month by month seasonal chart you get a very different picture.

You have to think that the WSJ is going to go back to using seasonally-adjusted numbers in the fall.

The other thing to keep in mind is the long lag-time between a pickup in home building/sales and the the bottom in home prices. Take a look what happened after the much smaller 1980's housing bubble.

Falling home prices are important because negative equity is the most important factor in foreclosures, according to the Boston Federal Reserve.

There is little question that we are many years away from the day the housing market, the key source of our economic problems today, can be considered healthy again.

Meanwhile, the government is doing everything it can to stop home prices from falling back to their historical norm.

It's an understandable attempt at mitigating pain, but at the same time it is a waste of effort.

The Boston Fed’s findings suggest the Obama administration’s major effort to solve the foreclosure crisis by giving the lending industry $75 billion to rewrite delinquent loans to more affordable levels is not likely to work.One of the study’s coauthors, Boston Fed senior economist Paul S. Willen, said the government would be better off giving the money directly to struggling borrowers to help them with their payments, rather than to lenders that are averse to working out the troubled loans.

"Loan modification is not profitable for lenders," Willen said. "If it were profitable, they would go out and hire staff."

...

The Fed’s study found that only 3 percent of seriously delinquent borrowers - those more than 60 days behind - had their loans modified to lower monthly payments; about 5.5 percent received loan modifications that did not result in lower payments.

Almost every economist out there, including the Fed, thinks that the "recovery", when it finally gets here, will be weak and slow. No one bothers to really explain to us why that is.

Well, I'll tell you why it is - it's because we haven't addressed the root cause of our economic problems. We continue to only treat the symptoms and ignore the fact that our economy is sick. It has long-term structural problems, problems that defy quick, easy solutions, that need to be addressed.

What is likely to happen is that the "recovery" will be indistinguishable from the "recession" to the average person on Main Street.

Comments

right on!

and what I find even more frightening is the public focus, the public demand for those policy changes, for those deep structural changes is flying off of the radar screen.

and they are right there, for any analysis to view, the growing income inequality, the fact very few are prepared for retirement (and they will not, absolutely will not acknowledge that retirement was raided and this is the real reason why, plus getting fired/laid off all of the time, careers cut short may have something to do with the ability to save)...

I mean we even have Stimulus jobs being offshore outsourced. Yet we still cannot get the focus on this and even worse, the entire blogosphere has become bogged down in calling a recession bottom or the "green shoots/yellow weeds" argument?

No one bothers to really explain

what this weak and slow growth means. This means long and high structural unemployment. This means that people may be unemployed a lot longer than their unemployment compensation. This means that any emergency savings will be exhausted. This means more people will be tapping into retirement savings just to survive. This means that if people are lucky to get a job it will be for much less money.

This is the "New Normal". Unfortunately, we are not ready for it.

RebelCapitalist.com - Financial Information for the Rest of Us.

RebelCapitalist.com - Financial Information for the Rest of Us.

it doesn't have to be that way

Right now it seems policy makers are more busy trying to get the public to accept the rape of the middle class instead of really doing something about it.

I mean in all seriousness, if anyone who goes to D.C. where their focus is on manufacturing, trade, jobs....

if they get a seat at the table....is that the kiddie table in the kitchen?

It's almost like segregation in terms of the enormous blow off on the entire manufacturing (production) economy, including the corporations who contribute.

(If you want to call putting some green kid in charge of GM who supposedly is going to offshore outsource to China attention).

Friday should be spin city, from every direction

Friday the GDP numbers will be released. Now I am seeing the build up to claim the Stimulus worked, but that's if GDP comes in a a -1.5% but be prepared for them to claim it still worked if it's lower.

Most amusing is I'm seeing "22k jobs created" and then claims of 750k jobs saved...

well, I'm sorry but this is all "thumb in the air" spin trying to claim that there is a hard fast correlation between GDP vs. actual jobs....which obviously has broken this recession.

More assuredly but I thought I'd give a heads up because various groups are already releasing their spin pregame.

Jez, can we get some accuracy here?

Given all of the fundamental

Given all of the fundamental problems in the economy I am amazed that gold is still well below $1,000, as explained here http://www.bloomberg.com/apps/news?pid=20601116&sid=aA3eLD2EZ5CM

Echos of a 1930 stock market rally

Ya all gotta read this one. Echoes Of 1930 In Current Market Rally:

No offense, but I really do not want to see midtowng validated. Unfortunately this blog is from the Dow Jones wires.