Double, double toil and trouble; Fire burn, and cauldron bubble. – Macbeth, by William Shakespeare

The financialization of the American economy certainly represents a bubbling cauldron, and the cauldron has bubbled over quite recently, and we sadly can look forward to further overflows.

This post is meant to build upon my previous post on healthcare cost drivers, as well as building upon a recent Instapopulist post by Robert Oak on the pension funds shortfall.

Previously, I had stated the premise of the rise in healthcare costs due to private equity firms' leveraged buyouts of health sector companies together with any and all speculation by healthcare hedge funds.

As can be observed by this chart from a Government Accountability Office report to congress (GAO-08-885):

CLICK FOR READABILITY

there was considerable amount of structured loans afforded private equity firms for their various funds for acquisitions and leveraged buyouts during 2005 to 2007 period approximately $633.8 billion).

According to a white paper from Integrated Corporate Relations (titled: Special Purpose Acquisition Company), between 1999 to 2005, more money was invested in leveraged buyout transactions ($358 billion) than in venture capital transactions ($257 billion). When one reflects upon those funds which may have been bled from some of those companies involved in the leveraged buyouts, due to loans taken against the victim company's collateral and the resulting debt heaped upon said companies, the actual amount of damage probably far exceeds that $358 billion figure.

It is crucial to understand some of the causes of the previously mentioned pension funds' shortfall.

A considerable amount of those private equity (PE) firms funds for leveraged buyouts derives from pension fund investments.

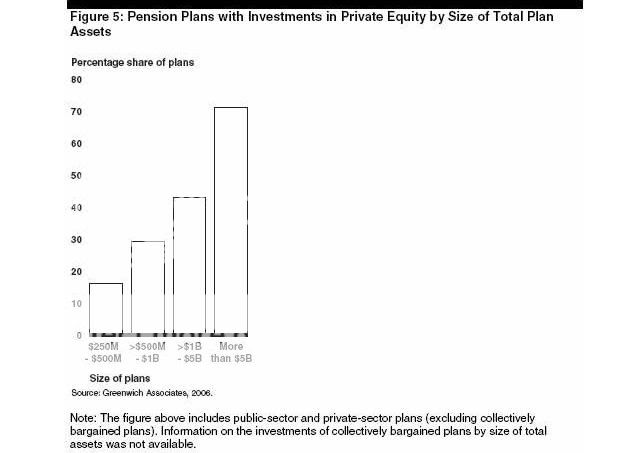

A graphic below, from a GAO report (GAO-08-885) explains this situation.

CLICK FOR READABILITY

As can be observed from this GAO graph, over 70 percent of pension funds with $5 billion or more on hand (often referred to as superannuation funds) were invested in private equity.

Quite a telling figure!

And these structured loans from those banks previously displayed in the GAO chart, along with these pension fund investments, are designed as various securitizations, and securitized financial instruments such as collateralized debt obligations (CDOs), collateralized fund obligations (CFOs), collateralized loan obligations (CLOs), as well as including the involvement of various and sundry credit default swaps (CDS).

Lehman Bros. downfall was linked to billions of defaulted credit derivatives and brought down some major insurance securitizations. The external economic circumstances are always correlated. While many of those Lehman credit derivatives were stretched through money market funds, undoubtedly, some of those defaulted credit derivatives were also involved in those pension fund investments.

An even more illustrative chart of the financial interrelationships between private equity firms and pension funds comes from the 2007 Private Equity Council report titled, Public Value: A Primer on Private Equity below.

CLICK FOR READABILITY

On p. 10, from Nicholas Hildyard’s white paper titled, The (Crumbling) Wall of Money(The Corner House, UK), comes this most salient of quotes:

The Afro-American community has been worst affected (52 per cent of “subprime” loans in 2005 were made to Afro-Americans), causing what has been described as “the largest loss of African-American wealth in American history.” Workers’ savings and retired peoples’ pensions have also been put at increased risk (and, in some cases, lost) as a result of pension funds and government insurance schemes investing directly in risky derivative trades or indirectly via hedge funds. In Florida, the state’s $14 billion Local Government Investment Pool lost so much money in the derivative-fuelled financial turmoil of recent years that withdrawals were frozen and local towns were left with insufficient cash to pay teachers and other staff. One municipality – the City of Vallejo in California – has already been forced into bankruptcy by the subprime crisis, while Jefferson County in Alabama teeters on the verge after a municipal bond to raise money to repair the local sewage system run into difficulties, leaving the county $4.6 billion in debt. [Bold emphasis mine - JW]

And on p. 21, from that same report:

Billions of dollars worth of CDSs have also been taken out by hedge funds and pension funds seeking to hedge their investments.

One other quote, from p. 36 of that report, which bares reflection:

Attracted by the high returns, pension funds have invested heavily in hedge funds, as have other institutional investors, notably university endowments – in 2007, Yale University had one quarter of its endowment money in hedge funds while Harvard University was also a major investor.

And, circling back to healthcare costs, those PE leveraged buyouts in the health sector, loading down many of those companies (and some private hospitals) with debt upon debt, surely has a negative impact on any cost reduction.

To better understand the widespread effect of various LBOs on the health sector, one should understand what this sector encompasses. A short list below is highly enlightening.

Private hospitals

Medical Devices

Analytical Instruments, Anesthesia Products, Biomaterials, OB-GYN Products, Cardiovascular Devices, Catheters, Dental Products, Diagnostic Imaging, Drug Delivery, In Vitro Diagnostics, Endoscopy and Minimally Invasive Surgery Products, Ophthalmic Devices, Orthotic and Prosthetics, Packaging Products and Equipment, Pulmonary Devices, Specimen Collection Disposables, Women's Health, Surgical Instruments, Wound Care Items.

Pharmaceuticals

Anti-infectives, Blood Substitutes, Cancer Therapies, Cardio-Vascular Drugs, Contrast Agents, Dermatologicals, Drug Delivery Systems, Generics, Natural Products, Nutraceuticals, OTC Products, Pharmaceutical Packaging, Proteins, Vaccines, Veterinary, Wound Care.

Healthcare Information Systems

Billing Systems, Clinical Information Systems, Electronic Medical Records, Hospital Information Systems, Outcome Measurement Systems, Physician Practice Management Systems, Pictorial Archiving Communication Systems, Radiology Information Systems, Surgical Treatment Systems.

Biotechnology

Biochemical Products, Biotech Instruments, Human Diagnostics, Human Therapeutics.

Distribution

Dental Distribution, Direct Marketing (Catalog, Mail Order, On-Line Systems), Hospital Distribution, Private Practice Distribution, Specialty Distribution.

Medical Services

Clinical Laboratories, Diagnostic Imaging, Independent Medical Exams, Managed Care, Utilization Review.

So, there is a highly probable correlation between the present state of pension funds and PE leveraged buyouts, as well as a possible, if not probable, correlation between rising healthcare costs and financialization and speculation in that sector.

But leveraged buyouts aren't the only financial event impacting upon the health sector, as can be noted by this item from the previously mentioned GAO report on private equity (GAO-08-885).

On page 14, the GAO offers the methods below as the principal ways that private equity firms exit their LBOs and acquisitions:

make an IPO of stock;

sell to a “strategic” buyer, or a corporation (as opposed to a financial firm);

sell to another private equity firm; or

sell to a “special purpose acquisition company,” which is a publicly traded “shell” company that allows its sponsor to raise capital through an IPO for use in seeking to acquire an operating company within a fixed time frame

Please note the mention above of a "special purpose acquisition company" or SPAC (occasionally referred to as a SPAV).

I have read voluminous amounts of documents and find some different definitions of this financial vehicle term. After some of those reports and documents have presented their definition of SPAC, their further information and data described something somewhat different.

Therefore, I am going with the definition below, from the Vernimmen site on corporate finance definitions.

DEFINITION:

*SPAC: Special purpose acquisition vehicles are companies with no asset which are IPOed on the Stock Market through a share issue. They are in fact shell companies with cash. they wait for opportunities to buy assets or other companies using the cash raised during the IPO and debt raised on the acquisition date.They then usually go largely into debt and are equivalent to a listed firm under LBO.

Please note the inclusion of the phrases "..usually go largely into debt.." and "..are equivalent to a listed firm under LBO." (LBO, as in leveraged buyout.)

A more interesting quote is to be found in a very fascinating and exhaustively researched study on the aspects of private equity, hedge funds, SPACs and sundry other constructs as pertains to black market capital by Steven M. Davidoff, an Assistant Professor of Law, Wayne State University Law School.

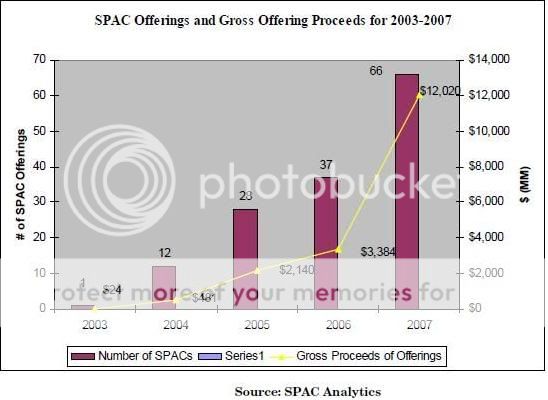

The result is an unwelcome distortion to the structure of our capital markets. Another example of this comes from special purpose acquisition companies (“SPACs”). A SPAC is a public derivative form of private equity which has been touted to investors on this basis. In 2007, there were sixty-six initial public offerings raising $12.02 billion by SPACs comprising twenty-five percent of all U.S. initial public offerings for that year and twenty percent of the aggregate money raised. The recent popularity of SPACs, which are a controversial investment class due to their high risk characteristics, again appears due almost wholly to investor demand for “private equity-type” investment.

An excellent graph from Prof. Davidoff's report illustrates the state of SPACs, to some degree.

CLICK FOR READABILITY

While another more recent chart from the SPAC Analytics site shows a more current status.

CLICK FOR READABILITY

I have gathered by some research in the matter of SPACs, that while the numbers may be lower than the super-sized funds of PE leveraged buyout funds, the effect of SPACs on the health of companies involved with them, in general, and specifically those companies in the health sector, shouldn't be overlooked -- but added to the financial mix.

SPACs afford individuals the opportunity to be involved in the takeover of private operating companies; individuals who would normally be excluded from hedge fund or private equity fund participation.

Lesser money requirements usually pertain to individual SPAC investment.

Of course, a serious problem in ascertaining the negative effects of SPAC upon the state of healthcare sector costs is that they are listed as SPAC transactions, not leveraged buyouts when, in fact, they may actually replicate a leveraged buyout.

From an online Businessweek profile of Healthcare SPAC (accessed February 18, 2010):

HealthSPAC, LLC engages in the business of incubating special purpose acquisition companies (SPACs) focused on healthcare opportunities. The company operates as an incubator for SPACs, which are blank check companies that go public with the intention of merging or acquiring a company with the proceeds of an initial public offering. It undertakes market research to identify specific industry opportunities within the healthcare sector that can thrive under a SPAC financing model; recruits stellar management teams to operate proposed SPACs; offers documentation services to meet regulatory requirements and support the investment model; raises the required investment capital for SPACs; and works ...

Also, a short list of some SPACs I came across, although their status may have changed since I copied them down.

Health Sector SPAC listing:

Apex Bioventures

Echo Healthcare Acquisition Corp.

Golden Pond Healthcare

Healthcare Acquisition

HealthSPAC, LLC

Highlands Acquisition Corp

KBL Healthcare Acquisition II

MBF Healthcare

NationsHealth

Oracle Healthcare Acquisition

Paramount Acquisition

And some very interesting remarks from from a hedge fund report (p. 16) from the Incisive Media site.

A Special Purpose Acquisition Company is another form of private equity investment vehicle which is attractive to investors. Jose Santos, a senior associate in Maples and Calder, says “they’ve been growing in popularity over the last couple of years.

“We’re seeing more and more Special Purpose Acquisition Companies (SPACs) being set up in the offshore jurisdictions.”

A Special Purpose Acquisition Company is a company that is a “publicly listed shell company that has no operating history”, says Maples & Calder’s Santos.

So, another difficulty in what might have appeared to be more transparency than hedge funds and private equity firms is dashed due to the nature of their possible and probable offshore locales. (One might assume tax avoidance figures into this matter.)

It is important to note that SPACs are intimately tied to hedge funds as historically hedge funds have been their largest buyer. (Although Citigroup and Deutsche Bank have been known to purchase one or two of them.)

So, hedge funds are buyers of SPACs, and SPACs can be operated as alternative leveraged buyouts (LBO), so healthcare hedge funds are not only guilty of inventing new methods of speculation (by way of securitizations and leveraging various credit derivatives mixes) but can also do stealth LBOs when the opportunity arises.

Can't you just feel that cauldron bubbling?

And, to tediously repeat again, the SPAC vehicles, PE leveraged buyouts, pension funds and the health sector are all intimately interlocked atop a layer of securitized financial instruments, which are highly susceptible to present and future meltdowns (as we've yet witnessed any real financial regulation to date).

The one bright note in this entire picture: when Goldman Sachs, a little over a year ago, attempted to enter the SPAC market they met with little success.

Evidently even the Vampire Squid sometimes stumbles in the pursuit of limitless greed!

*Please also see BDCs, STACs, and ETFs.

To further add to the bubbling caldron, an item known as PIKs, or payment-in-kind, better understood as trading debt for more debt, is about to come due.

From an excellent article awhile back by Geoffrey Parnass at the Private Equity Law Review site, we learn that private equity firms had issued these PIK notes when the economy went sour to forestall paying the requisite cash interest payments.

These PIK notes aren't simple penalty payments, but incur much higher basis point levels, along with compounding, so when they are due the amounts are far greater (more in the exponential vicinity) than the original cash amounts.

A number of these PIK toggles come due this 2010 summer, so let's hope, for the sake of those plutocrats at the private equity firms, that the word "default" isn't in their and our futures! (If there are large-scale defaults, one can't help but ponder their effect on the present employment situation.)

SUMMATION

We should gravely consider whether these financialization investment vehicles (such as SPACs) are nothing more than massive cost drivers and artificial market expanders.

We should also reflect upon those much vaunted "economies of scale" and whether they are truly just economies of de-scaling.

Of course, the obvious answer is to watch the prices in the health sector. Have they been rising? Or have they been falling?

Has that "wall of money," as Mr. Hildyard describes the monumental securitizations of private equity firms, hedge funds and the Wall Street bankers, been spreading progress across the land or responsible for the regression of the economy?

Have these shadow banking processes simply been used to privatize and buy everything?

Has employment been rising and enriched? Or has unemployment usually resulted? (A little known tactic of private equity acquisitions is to count their new purchases as job growth, when it is simply a company with existing jobs which will in many cases either be offshored or cease to exist in the aftermath of their leveraged buyouts.)

Today we witness people laid off, their pension funds disappeared or in jeopardy, their property taxes rising while the foreclosures continue apace and their actual property value shrink.

Today in America we see Rube Goldberg-style engineering at the city and state level, while suffering from fantasy financial engineering at the federal, corporate and multinational level.

And to those of us who have been curious and paying attention, we have witnessed securitization as a financial force multiplier, acting as the foundation and underpinning of a shadow banking system (including those hedge funds and private equity firms) which allows for more and more concentration of wealth at the top, while negating the utterly valuable free enterprise concept of amortization.

Meet the new boss; same as the old boss – The Who

I would strongly recommend to any and all further interested in hedge funds, private equity LBOs, and securitizations and credit derivatives to read Prof. Davidoff's outstanding report on black market capital, as well as Nicholas Hildyard's highly enlightening white paper.

REFERENCES

Businessweek Profile: HealthSPAC, LLC, Feb. 18, 2010 accessed.

http://investing.businessweek.com/research/stocks/private/snapshot.asp?p...

Davidoff, Steven M. “Black Market Capital.” Columbia Business Law Review, March 2008.

http://works.bepress.com/cgi/viewcontent.cgi?article=1004&context=steven...

Duff & Phelps. SPAC Market Overview. First Quarter 2009. (Duff & Phelps Corporation)

http://www.duffandphelps.com/sitecollectiondocuments/spac_nwsltr_1q09.pdf

Ehrenberg, Roger. “Does SPAC Really Spell SCAM?” Information Arbitrage, May 17,2008.

http://www.informationarbitrage.com/2008/05/does-spac-reall.html

Government Accountability Office (GAO-08-885). “PRIVATE EQUITY Recent Growth in Leveraged Buyouts Exposed Risks That Warrant Continued Attention.” September 2008.

Hildyard, Nicholas. “A (Crumbling) Wall of Money, Financial Bricolage, Derivatives and Power.” The Corner House, UK, Oct. 8, 2008.

http://www.thecornerhouse.org.uk/pdf/document/WallMoneyOct08.pdf

Integrated Corporate Solutions, “Special Purpose Acquisition Company.” White Paper Series, 2006.

Parnass, Geoffrey. “High-Yield Deb Issuers Trigger “PIK” Options.” Private Equity Law Review, April 19, 2009.

http://www.privateequitylawreview.com/tags/pik/

Private Equity Council. "Public Value: A Primer on Private Equity, 2007.

http://www.privateequitycouncil.org/wordpress/wp-content/uploads/pec_pri...

Vernimmen.com. “Corporate Finance by Vernimmen.com, Definition of SPAC

http://www.vernimmen.com/html/glossary/definition_spac.html

Wikipedia.

http://en.wikipedia.org/wiki/Special-purpose_acquisition_company

Comments

Not to nickpick.

James,

You meant cauldron did you not? Sorry to be the word police, but now I can go back to reading the entire article.

Peace!

My bad.

Didn't realize it is one of those English/American words that have double spellings.

I did my due diligence on this

I really wanted to use "cauldron" but in checking into the spelling during Shakespearian times, found that it had actually been "caldron" as well as the modern usage was also "caldron."

The 19th century English spelling was "cauldron" -- so that was a very brief time for that spelling (although I prefer that spelling, myself).

If nothing else, I do know my orthography.

Not that it means much...

My understanding is that 17th century spelling was variable, depending on what spacing was needed and how many and which letters were left in the typesetter's tray. Thus, you might find alternate spellings in the same document, and one might fall on one's sord or sword or whatever. The devil was in the details.

Frank T.

Frank T.

Rats! I knew I should have used "cauldron"

You've spoiled my entire day, Frank!

editing your blog titles

You can change a blog title, esp. if you believe there is a spelling error, after publication.

Just click edit, change it and hit preview, then save.

I have URL creations set up it will not break the links...

(links are created out of post titles).

Gotta have it, esp. for the spelling and grammar disabled.

(I cannot tell you how many times I found a typo, spelling error, including prominent economics, political figures names....after I wrote up the piece and I'd like to get some sort of spell check on the titles which currently I don't have!).

I think you should change it because I'm used to seeing Cauldron but hey, what do I know.

Gez

I had no idea that private equity had such a hand in medical costs. Just great. It would be nice to see a percentage estimate on the additions.

I'm also wondering if they should make it a law, mandatory that all health care sector businesses must convert to non-profit and also taken off the markets.

I'm sure that would be met with a war, but I'm wondering if that's a way to deal with all of the "Wall Street of Death" march.

I mean we have debt warnings all over hell on the debt hitting 100% GDP and a huge part of that is Medicare/Medicaid....so how much of this is part of that?

A non-profit healthcare sector is the way to go!

The damnable problem with those private equity guys, and hedge fund guys, of course, is zero transparency (even now that Blackstone Group has gone public).

While the uppermost usage of all those SIVs (structured investment vehicles, created at Citigroup in 1988), and SPVs, and SPEs, and SPACs, etc., is to hide debt (and all too frequently, hide offshore capital as well), they work equally well in hiding ownership (the original, and still existing, purpose of the holding company).

So the hedge fund ownership of SPACs, as well as those other financial vehicles, acts to make this extraordinarily difficult to ascertain.

Even with several supercomputers and time to model it all, only a fallible percentage could be achieved, I strongly suspect.

But I would definitely re-posit that they are the major cost drivers in the health sector (private equity and hedge funds, that is).

I agree that in a culture or society that hadn't reached the level of complete and total corruption which American has, the health sector would be completely non-profit.

That is the only solution.

imagine if fire and police were for profit

Can you see that? Torched buildings to help their quarterly bottom lines, a few people shot to assist in marketing, shadow created crime to help out..

one has to wonder if those private prisons have thought of this yet to keep up their supply of prisoners. They get money per head and also use those prisoners at slave labor wages to work for all sorts of companies.

So, why, on this huge overriding concept that health care is a service for the public good....is it ok to peddle the latest drugs with God knows what side effects to people on TV and no one blinks an eye?

Vioxx anyone? (or just pick a drug here, I mean this is unacceptable, if it was an individual killing people it would be front page news, but death by Vioxx, which was about 45,000 people, gets just a lawsuit?)

Funny you should mention private prisons....

...as I believe Corrections Corporation of America (subsidiary: Prison Realty, Inc.) is owned by private equity firms, as are most of the private prison corps.

And I do believe in the worst where private equity combines with private prisons. (And as to those rumors that they have ready access to psychos who they then train and use for their own nefarious prupose....well, I don't have any evidence as of yet, but have found some fairly interesting rumors on it.--- Yeah, I know I'm mentioning hearsay, but think of it as a probable future instead.)

And to add to that non-profit healthcare mix

Interesting news article just came across (actually tipoff from Mr. Kosman -- thanks!):

Long-Term Care Hospitals Face Little Scrutiny

We really need a public debate on the social benefits

of the financialization and "financial innovation". IMO, there has been no social benefit from the most recent "financial innovations".

RebelCapitalist.com - Financial Information for the Rest of Us.

RebelCapitalist.com - Financial Information for the Rest of Us.

A very subtle point

Excellent point, sir.

An argument I've been making for awhile now, and a really subtle and almost abstract argument it is, is that the entire securitization process is what has been the artificial price driver driving up all the costs of just about everything, from college education to housing prices, to...you name it! (As well as establishing a slew of artificial markets.)

A close examination of the historical data, and that privatization-securitzation scam process, should be verification enough.

Abolutely right, RC!

I will be attending a dinner this week where our speaker (guest of honor) is Alan Grayson. I may get to ask questions, so give me a couple of talking points so I don't look (sound) like the complete financial Luddite I am becoming, thanks to all this "innovation."

I would start with MERS. except it sounds like a French expletive.

rank T.

Frank T.

Questions for Frank T.

Question 1:

Germany has altered their tax laws to prevent predatory leveraged buyouts by private equity firms. (Taxing debt payments, etc.)

Why hasn't America done the same? (Since those predatory leveraged buyout "pump-and-dumps" -- along with various other types of commercial financial vehicles, SPACs, STACs, BDOs, etc. -- have severely driven up the cost of healthcare, at all levels, in North America.)

Question 2:

From Elizabeth Warren's COP report, as well as Neil Barofsky's SIGTARP report, we find that almost virtually nothing has changed with regard to all those "toxic assets."

What gives? How come? Is anybody doing anything in D.C.?

Question 3:

Why is the pharmaceutical industry allowed their very own price-fixing cartel? Anyone ever heard about the concept of economic competition?

Question 4:

Rep. Grayson, how come there's only one of you in congress?

Zerohedge on LBO bubble

Zerohedge has a great piece on the coming LBO bubble.

How to Capitalize on the Upcoming, Irrationally Exuberant LBO Bubble. Good follow up on this piece.