The Federal Reserve Industrial Production & Capacity Utilization report shows industrial production decreased -0.6% while January was revised downward to a -0.4% decline. February showed a measly 0.1% increase, so overall the first quarter looks bleak Annualized Q1 showed a -1.0% decline and such a contraction has not happened since Q2 2009. The G.17 industrial production statistical release is also known as output for factories and mines.

Total industrial production has now increased 2.0% from a year ago and this yearly gain is much lower than last month. Currently industrial production is 5.2 percentage points above the 2007 average. Below is graph of overall industrial production's percent change from a year ago.

Here are the major industry groups industrial production percentage changes from a year ago.

- Manufacturing: +2.4%

- Mining: +3.7%

- Utilities: -3.6%

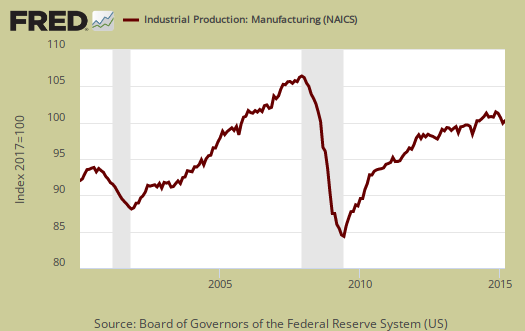

The worst news of this report is January manufacturing was revised downward from -0.3% to -0.6%, that's quite a revision downward. Annualized, manufacturing dropped -1.2% for Q1, another decline not seen since Q2 2009. Manufacturing output is 1.2 percentage points above it's 2007 Levels.

Within manufacturing, durable goods rebounded, increasing 0.2% for the month. Motor vehicles & parts increased 3.2%, reversing last month's drop. Primary metals dropped -3.2%.

Nondurable goods manufacturing showed a 0.1% gain for the month as food, textiles and petroleum all gained 0.6%. Nondurable manufacturing has increased 2.3% for the year.

Mining showed a -0.7% monthly decrease, but has grown 3.7% for the year. Mining includes gas and electricity production and the Fed have a special aggregate index for oil and gas well drilling. Oil and gas well drilling dropped a whopping -17.7% and for the year is down -36.6%. What a collapse this is.

Utilities nose dived -5.9% for the month. Utilities are volatile due to weather and why the below graph shows the wild swings. One can track the polar vortexes and heat waves in the below graph.

There are two reporting methodologies in the industrial production statistical release, market groups and industry groups. Market groups is output bundled together by market categories, such as business equipment or consumer goods and shown below:

Business equipment was the only major market group to post a gain in production for March; its increase of 0.2 percent was mostly due to higher output of transit equipment. The index for consumer goods moved down 0.6 percent, with the decrease due to a drop of 5.0 percent in consumer energy products. The index for non-energy nondurable consumer goods moved up 0.2 percent. The output of durable consumer goods increased 1.7 percent, as a gain of 3.0 percent in automotive products outweighed declines in home electronics and in appliances, furniture, and carpeting. The index for materials fell 0.5 percent, with decreases in the output of both non-energy and energy materials.

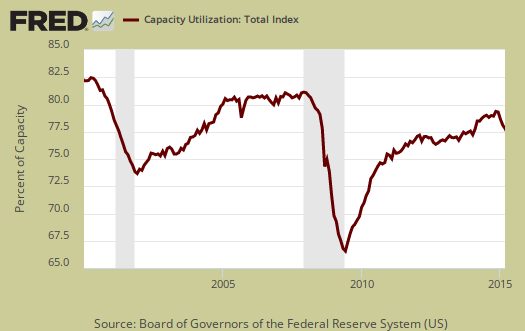

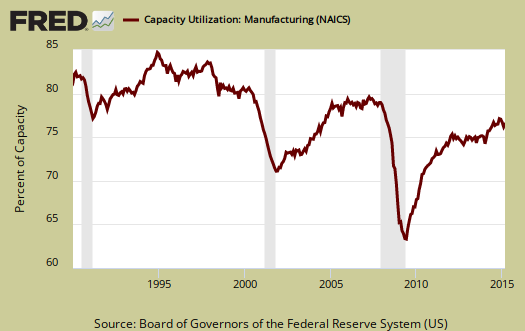

Capacity utilization, or of raw capacity, how much is being used, for total industry is 78.4%, a decline of -0.6 percentage points from last month. . Capacity utilization has decreased -0.7 percentage points from a year ago and is -1.7 percentage points below the long run average. Manufacturing capacity utilization is 77.1% and is 0.3 percentage points higher than a year ago. Manufacturing capacity utilization showed no change for the month. Mining capacity utilization is 84.4% and is down -3.9 percentage points from a year ago. and -1.0 percentage point for the month. Utilities use of it's capacity is 80.0% and has down -3.7 percentage points from a year ago.

Capacity utilization is how much can we make vs. how much are we currently using, of what capacity is available now, or output rate. Capacity utilization is also called the operating rate. Capacity utilization is industrial production divided by raw capacity.

Capacity growth is raw capacity and not to be confused what what is being utilized. Instead, this is the actual growth or potential to produce. Capacity is the overall level of plants, production facilities, and ability to make stuff, that we currently have in the United States. Capacity growth overall has increased 3.0 percentage points from a year ago and the same as last month. Below is the capacity growth increase from a year ago of the subcategories which make up industrial production.

- Manufacturing: +2.1%

- Mining: +8.5%

- Utilities: +0.9%

Below is the Manufacturing capacity utilization graph, normalized to 2007 raw capacity levels, going back to the 1990's. Here is where offshore outsourcing really shows up. Pay particular attention to the 2001-2003 as manufacturing had a mass exodus to China after passage of the bad trade deal in 2000.

This report just gives another data point that Q1 is going to be a very bad economic quarter. Some will try to blame gas prices but there is clearly something else going on as manufacturing growth continues to be stunted.

Here are our previous overviews, only graphs revised. The Federal Reserve releases detailed tables for more data, metrics not mentioned in this overview.

Recent comments