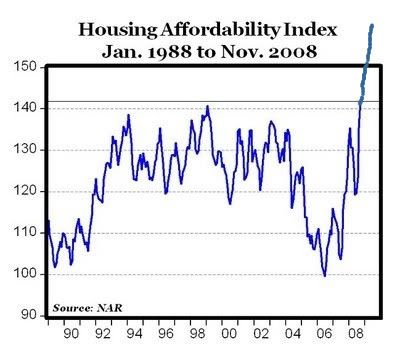

The NAR released its Housing Affordability Index for February this morning:

NAR’s Housing Affordability Index rose 0.9 percentage points to a record high of 173.5 in February from an upwardly revised index of 172.6 in January, and is 36.3 percentage points higher than a year ago. The HAI, a broad measure of housing affordability using consistent values and assumptions over time, shows that the relationship between home prices, mortgage interest rates and family income is the most favorable since tracking began in 1970.

A median-income family, earning $59,700, could afford a home costing $285,600 in February with a 20 percent downpayment, assuming 25 percent of gross income is devoted to mortgage principal and interest. Affordability conditions for first-time buyers with the same income and small downpayments are roughly 80 percent of that amount. The affordable price is considerably higher the median existing single-family home price in February, which was only $164,600.

This literally takes the index "off the chart". Here's the continuation I posted for January:

Calculated Risk thinks the HAI is "nonsense" and just tells you that mortgage rates are low. I think he's wrong here. The bottom for sales in housing will be driven by conservative buyers (vultures, even) with good cash reserves and good credit scores stepping up to buy.

And as further evidence of that, I give you the following Bloomberg report of mortgage applications for the last week in March:

Mortgage applications in the U.S. rose for a fourth consecutive week as a decline in borrowing costs prompted more refinancing.

The Mortgage Bankers Association’s index of applications to purchase a home or refinance a loan rose 3 percent to 1,194.4 in the week ended March 27 from 1,159.4 the prior week. The group’s refinancing gauge gained 3.7 percent, following a 41 percent gain the prior week, and its purchase index rose 0.1 percent.

Refinancing is good not just for housing, but for the entire economy.

In short, lower prices + lower financing costs = greater demand. So it shouldn't surprise us that others are surprised by the uptick in pending home sales.

Comments

the day someone on $10/hr can afford a mortgage

is the day I know they bottomed out. After all, the way the U.S. is busy ignoring global labor arbitrage, I expect that to be about the final median wage.....assuredly is heading this way for most with good jobs.

You'd have to show the link to CR on HAI being nonsense, although intuitively that doesn't make a lot of sense to me as well.

Don't forget: volume vs. prices

You may be right about prices!