Note: this is a cross-post from The Realignment Project. Follow us on Facebook!

Introduction:

In about two years of blogging at TRP (and another two years’ policy-blogging elsewhere), I’ve never discussed trade. It’s not because it’s unimportant, because trade is clearly a major issue within economic policy and politics, but rather because of when I came of age politically. In 2001 student politics, the free trade vs. anti-globalization/protectionism debate seemed remarkably deadlocked and somewhat sterile. Twin camps of policy contenders required allegiance with either side, and I found myself unhappy with the analysis and debate and more drawn to questions of domestic economic policy.

However, in the wake of the Great Recession and the increasingly-urgent need to reassess the structure of the U.S economy, I can’t avoid it any longer. The trade question isn’t the whole of our economic problems, I think it can be exaggerated in a way that obscures a more important class conflict inside nations. And yet, the global balance of trade – between Germany and the rest of Europe, between China and the U.S, and so on – is clearly out of whack.

Historical Background:

To begin with,we have to understand how we have gotten to the present imbalance.

Especially because the dominant narrative presents the decline of American manufacturing and exports as the inevitable result of natural economic forces, we need to turn back to history. The transformation of the American economy from industrial to post-industrial (as much as those terms are overly broad) was recent – taking place largely in the 1970s and 1980s with many starts and stops – and it was not the result of blind economic forces, but rather the result of economic policy, both accidental and intentional, the result of drift and radical intervention. (Note: this narrative is largely drawn from Judith Stein’s new book, Pivotal Decade, which you should all buy – so if you’re looking for citations, search within.)

In 1970, America’s industrial core was within sight of its post-war zenith – the U.S economy accounted for 50% of world GDP (down from 60% in 1945), and exports and imports together made up only 8-9% of our domestic-market-based system of capitalism. There had been trouble – U.S economic growth in the 1950s lagged behind Europe by a wide factor (despite reconstruction from the devastation of WWII giving a bit of extra boost to European growth), American investment overseas in the 1960s had been 50% faster than American domestic investment, the emergence of U.S companies shifting production overseas to get under European tariff walls – but this trouble was understood as the intention of U.S policymakers looking to bolster the capitalist world in the Cold War.

State Department officials argued that it was in “the broader national self-interest to reduce tariffs and increase United States imports even though some domestic industry may suffer,” because “we Americans could afford to pay some economic price for a a strong Europe.” U.S policymakers were not fools, they knew what the consequences of GATT would be, but it was a question of policy priorities. The Cold War trumped domestic industry, and besides we had so much industrial wealth that we would hardly notice a few percentage points here and there. And importantly, the trend of industrial decline was slow - the U.S enjoyed a trade surplus for thirteen years between 1945 and 1968, with the gap between import and export growth expanding at just 4% a year.

While the breakdown of the Bretton Woods system and the removal of the U.S from the gold standard (which if we couldn’t maintain when we were the undisputed world economic titan, why going onto it now would be a good idea is beyond me) was initially unrelated to trade, the international negotiations over what would come after mark the first missed opportunity to rescue American manufacturing. Under the old system, the U.S dollar had been fixed at 1945 levels – leading the dollar to become overvalued when Europe and Japan recovered. However, when the U.S devalued the dollar, the major OECD nations refused to coordinate revaluation. Instead of the 15-20% shift needed to rebalance U.S trade, the Nixon administration only managed a 8.6% shift that was soon completely undone by the world currency markets. Critically, at this this moment, the U.S chose against establishing capital controls that could have prevented speculative runs of this kind.

The oil crisis-induced world recession from 1973-4 further delayed any kind of international agreement on trade. 1975 saw the first G7 summit, where the U.S failed to persuade Germany and Japan to stimulate their domestic economies instead of exporting their way out of recession – instead, the U.S would act as the “market of last resort,” with the Ford administration explicitly agreeing that bolstering the capitalist world market was more important than protecting domestic industry when push came to shove. The parallel Tokyo Round of GATT trade negotiations saw the U.S attempt to reduce tariff and non-tariff barriers, reduce subsidies to domestic industries, and increase dumping penalties fail. Instead, the U.S gave up its existing “countervailing duties” (automatic tariffs set at the level of the tariffs laid on American goods), our Buy American government purchasing requirement, and ultimately reduce tariff rates to below 5%. Again and again in this period, we see the U.S forced to choose between economic priorities and choosing against trade – first in favor of world capitalism, and second in favor of anti-inflation.

By 1976, the trouble signs in American export manufacturing had become so clear that major interest groups (especially the AFL-CIO) broke with conventional wisdom – U.S economic growth had recovered from the recession but exports hadn’t; the gradual decline had crossed an invisible line of viability. U.S steel had dropped from 50% of the world market in 1950 down to 20% in 1976, our exports dropped from 32% of the world market to 11%, and our trade deficit had grown threefold in 1977 alone. If any time was ripe for a rescue, for a “switch in time,” this was it. The recession of 1975 had brought in enormous Democratic majorities, a Democratic president for the first time in eight years, and U.S labor was increasingly militant and well-organized politically – so the way seemed clear.

Instead, the Carter administration decided against rescue.

In the recession of 1975, U.S steel had fallen to 50% capacity and had reduced employment by 25%; a brief recovery had brought it up to only 78% capacity and below pre-recession levels of employment. The recession that began in late 1979 would bring them back down to half capacity. In 1980, U.S auto manufacturing was down to 58% capacity and had shed 800,000 jobs. Both industries were competing against nationalized or subsidized companies – as Europe and Japan made the policy decision to protect manufacturing employment at the price of inflation – but found no support from the American state.

In 1975, the Ford Administration refused to invoke the “escape clause” in GATT that would have allowed tariffs against imported steel and instead pursued a weak voluntary agreement with Japan, the European Community, and Sweden. When Carter came into office, he rejected both tariffs and industrial policy (tax credits, investment incentives, modernization of transportation and power infrastructure) and actively sought to use steel imports as a means of reducing inflation – let that last point sink in. In dealing with the U.S auto industry, Carter refused to establish domestic content legislation (despite the widespread practice of domestic content throughout the industrial world) – again because of inflation fears – and botched the “escape clause” suit in front of the ITC.

This change of priorities from preserving employment to fighting inflation happened at the worst possible time; U.S manufacturing was still savable (in fact, would see a 5% increase in productivity per year in 1984-5), but the U.S was about to slide into a massive recession.

While some economic slowdown in 1979 was bound to occur due to the Iranian Revolution’s impact on oil markets (although in both the ’73 and ’79 oil crises, the actual increase in prices was much greater than the actual shortfall of supply), the depth and breadth of the recession was very much within the power of Fed Chairman Paul Volcker. In order to tackle double-digit inflation, Volcker raised interest rates to 12%, then 17%, then 20% and basically held them there (with one brief letup) until 1982. People are largely familiar with the domestic impact of the Volcker recession – unemployment peaking at 10.8%, nearly two straight years of GDP decline- the international implications were harder to track.

Record interest rates boosted the U.S dollar to record heights, which created the monetary equivalent of a 63% tariff on U.S goods between 1980-1985. In the wake of this, U.S exports shrank from 9% to 7.2% of GDP, while imports rose to 7.5% – the U.S had developed a persistent trade deficit which only grew. The back of American manufacturing and American exports was broken.

The point of all this economic history is that this decline wasn’t an accident – it was a matter of trade, monetary, and domestic economic policy. Some administrations accepted and promoted the decline in exports as a Cold War measure, others struggled to reverse it; finally, it was simply replaced by inflation as an policy goal.

Policy:

Thirty years later, how do we begin to deal with the legacy of a lost decade, especially when this would involve dealing with nations like China and Germany who enjoy large trade surpluses? Ironically, this might be one area in which the Great Recession has actually made things easier. China’s experience of galloping inflation and Germany’s deep frustration with bailing out European nations (who actually are their major customers, and who were lent huge sums by German banks to keep the good times rolling) might show the downsides of imbalanced trade even for exporters.

So, let’s begin to sketch out at least an outline of a rebalanced economic system:

- As I’ve argued before in other contexts, one of the dangers of narrowly focusing on policy in terms of discussion to industries, goods traded, and shares of GDP is that we lose focus on workers and employment levels. Trade can easily play this role – we talk about protecting American steel, not steelworkers (even when we don’t mean to). Indeed, in the 19th century, the Republican Party used its support for tariffs as a shield against demands for the eight-hour day, the minimum wage, or the right to unionize, on the grounds that trade policy would automatically result in a fair division of profit between capital and labor. Therefore, I think we have to start with the idea of nations adopting “labor market insurance” (their trading partners can think of this as “consumer base insurance”) in the sense of a suite of policies that ensure a high level of employment and consumption regardless of the balance of payments. This suite of policies should include both immediate protections against unemployment and loss of income (job insurance, labor market policy, and an improved social insurance system), but also long-term measures for building industries.

- Once we’ve provided national labor markets with an “immune system,” one of the many lost policy tools of history can begin to re-balance the world economy is the International Clearing Union advocated by John Maynard Keynes at Bretton Woods. The clearing union would essentially act like a central bank for trading that would even out the balance between exporters and importers: nations with too high a trace surplus would be taxed and the taxes put into a Reserve Fund, which would provide loans for nations with trade deficits (on the condition of inflating their currency to boost their exports). Intellectually, this is a totally rational mechanism for balancing world trade; it has always run aground on the shoals of national self-interest. However, exporting nations are faced with the reality that they are already doing this – China’s purchase of U.S bonds, Germany’s bailout of the so-called “PIGS” nations – and might as well establish a permanent system that can operate at lower levels without damaging their own economies.

- Next, a backstop is necessary. As we saw above, the U.S spent most of the 1970s fruitlessly chasing international compromise, only to be undone by efforts at national protection without doing the same itself. So to avoid that fate, many have suggested establishing a VAT tax (Europe, Japan, China, and most other nations have established VAT systems to replace tariffs – exported goods are “rebated” against the tax, which reduces their price in relation to competitors’ goods). I personally have been vehemently opposed to a VAT system on domestic grounds, but I can see the argument for what I would call a “double-rebated” VAT, whereby consumers are completely rebated the cost of the VAT they pay and where the rate is tied to the average VAT in trading partners’ economies (hence creating an option to lower VAT rates), as a potential plan B for readdressing America’s trade imbalance.

- Finally, a pragmatic approach to trade involves assessing things as they stand. For example – free trade agreements by this point are mostly an annoyance rather than a dramatic injury; for the most part whatever damage can be done has been done. The Korea trade pact recently negotiated won’t make the U.S dramatically more open to Korean imports (we’ve been that way for a long time) but the boost to our auto industry is a significant departure from the trend. There’s nothing wrong with this approach – even hardline McKinley Republicans pursued “reciprocal tariff reduction” in areas in which they thought the U.S could benefit from it – as long as we give ourselves a plan B to avoid the problems we saw in the 1970s where the U.S was using all carrot and no stick.

Conclusion:

The larger point here is that we should treat no reverse in public policy as inevitable or foreordained, and thus implicitly something we should refrain from trying to counteract. The depth and speed of decline in American manufacturing was largely the result in policy and policy can be the solution.

Comments

Ok, Robert, you finally got me to write about trade

I hope you're happy. ;)

good post, but on Korea

One must find out the nitty gritty. It is another offshore outsourcing deal.

Scott ran the numbers and we're going to lose at least 160k jobs if it's signed.

But yes, the real damage, as evident from the trade deficit monthly reports is China. It's 71% and over of the goods, non-oil trade deficit.

On the VAT, I'm glad to see you're open to it as modifications. The only reason I'm interested in it is because it's legal under the WTO and can be used as a dynamic tariff per good/service de facto. Figuring out a way to make it progressive instead of regressive is a must, and if that could be done I think it's a good idea.

But this attitude that people, labor is something to trade, disposable, that labor arbitrage is a grand idea....

if one looks at the theory, the actual equations, people are not interchangeable, at least not and expect any good results.

Instead, that's what we're getting, trading people instead of goods and final services.

While one can clearly see how trade subtracts from overall economic growth, and Q4 GDP advance is released this Friday (see past GDP reports on EP), it affects more than that in reality. Things like investment, PCE are also affected. When people are stuck in jobs which cannot even make rent, obviously they don't have too much disposable income to consume.

Oil, on the other hand is a real negative drag on the economy, much more than is realized and here come blasting oil prices once again.

I've read different things on Korea

At least in terms of autos, it seems to be ok.

But look at the levels we're talking about: 22k jobs a year, compared to say, NAFTA.

Regarding VAT, the difficulty with progressivism is counter-acting the "marginal propensity to consume." My preference is simply to rebate to consumers on the spot for the vast majority of purchases (anything under...$1k, $10k?) and to just accept that it won't be a huge revenue source (you'll still get some from manufacturers and the supply chain). What I've worried about in the past is folks like Matt Yglesias and Ezra Klein saying we should use a VAT to replace the income tax.

The income tax is one of the most distinctive American economic policies, and one of the few things we can boast of internationally in inequality terms.

this is a lot of BS on trade, in particular the White House

Sorry but we've seen fictional numbers, that usually goes along with yet another bad trade agreement.

Consider the source and esp. consider reading the actual agreement. I don't think it looks good on autos because I believe that's yet another JV,which is not real exports, although propagandists like to portray them as exports.

Well, it's pretty clear the income tax is also becoming fairly regressive. then, this massive underground economy not being taxed is another truth.

Any tax, whether it is income, sales, tariffs or corporate seemingly is never ending manipulated to take from the poor and give to the rich these days, as we just saw...

what worries me more is we just saw pure lobbyist agenda on income taxes endorsed by the white house, so if any other tax comes up, no doubt it would be a corporate lobbyist pig fest.

Fair enough

No need to be hostile on the Korea thing; UAW at least is happy about it, so maybe they got fooled.

The income tax is capturing less income, and it's less progressive than it used to be - but it's still on balance progressive, and it's one of the few progressive taxes we have, and makes a big difference in our tax system's profile.

The UAW

also settled for $14/hr to start at skilled manufacturing, and sure didn't get bailed out along with GM. So, I really don't know what they are smokin', if you look at the overall agreement it's not going to do that much for them and most unions are opposed.

Forgetting organized labor, from a pure macro view, it is projected to lose more jobs.

I think more to the point is to really analyze these. I've already written many posts some some credible data, and there is so much spin, including the White house, hardly ever the facts get out there on trade, the data.

On income, sure, but maybe we need to look a this more for I did a median, wage wage and really above about 500,000 I think a strong case could be made the income tax code is regressive.

It's "progressive" up to that point, or lower if you will, but when 50% of Americans made below 26k, how progressive is that really when the superrich are paying 15% and less?

getting hostile....

It's because I pour over BEA and Census data every day, plus watch the China deals, write them up, read the reports. Obama has so many offshore outsourcers in his administration and it's clearly showing up in policy agenda. To me, it's like I am in a time warp. Now that financial reform is dead, it's just returned to the same ole garbage that destroys the economy as it has the last 20 years. At this point, there are few economists in denial over China and that's because the statistics, data is brazen, you'd have to really be drinking and not take econ 101 to see it. Yet, this administration, just like Bush, refuses to do anything about it. Instead, we're heading straight to the same corporate agenda of the Bush administration, which was the agenda of the Clinton administration.

You just wrote up some of the seeds (missed a little Nixon in there) where the real innovation this country needs is to get economic policy, trade policy based on actual statistical results and the theory, not manipulated, the real theory, with the most important element being the U.S. worker, the U.S. middle class.

It's just incredible, 50% make less than 26k a year, 50 million people at official poverty levels (which are way below real poverty), people losing any retirement, getting fired like disposable diapers....

this has been going on for over 3 years and it's critical, a crisis and instead we get more of the same.

It's infuriating and maybe this site should advertise blood pressure medication because it's going to be a real blow out when this FCIC report comes out Thurs which shows financial Armageddon could have been easily avoided.

Free Trade is Based on Flawed 19th Century Theory

Our enormous trade deficit is rightly of growing concern to Americans. Since leading the global drive toward trade liberalization by signing the Global Agreement on Tariffs and Trade in 1947, America has been transformed from the wealthiest nation on earth - its preeminent industrial power - into a skid row bum, literally begging the rest of the world for cash to keep us afloat. It's a disgusting spectacle. Our cumulative trade deficit since 1976, financed by a sell-off of American assets, exceeds $10 trillion. What will happen when those assets are depleted? Today's recession is the answer.

Why? The American work force is the most productive on earth. Our product quality, though it may have fallen short at one time, is now on a par with the Japanese. Our workers have labored tirelessly to improve our competitiveness. Yet our deficit remains as large as ever. Our median wages and net worth have declined for decades. Our debt has soared.

Clearly, there is something amiss with "free trade." The concept is rooted in Ricardo's principle of comparative advantage. In 1817 Ricardo hypothesized that every nation benefits when it trades what it makes best for products made best by other nations. On the surface, it seems to make sense. But is it possible that this theory is flawed in some way? Is there something that Ricardo didn't consider?

I am author of a book titled "Five Short Blasts: A New Economic Theory Exposes The Fatal Flaw in Globalization and Its Consequences for America." My theory is that, as population density rises beyond a critical level, per capita consumption begins to decline. This occurs because, as people are forced to crowd together and conserve space, it becomes ever more impractical to own many products. Falling per capita consumption, in the face of rising productivity (per capita output, which always rises), inevitably yields rising unemployment and poverty.

This theory has huge ramifications for U.S. policy toward population management (especially immigration policy) and trade. The implications for population policy may be obvious, but why trade? It's because these effects of an excessive population density - rising unemployment and poverty - are actually imported when we attempt to engage in free trade in manufactured goods with a nation that is much more densely populated. Our economies combine. The work of manufacturing is spread evenly across the combined labor force. But, while the more densely populated nation gets free access to a healthy market, all we get in return is access to a market emaciated by over-crowding and low per capita consumption. The result is an automatic, irreversible trade deficit and loss of jobs, tantamount to economic suicide.

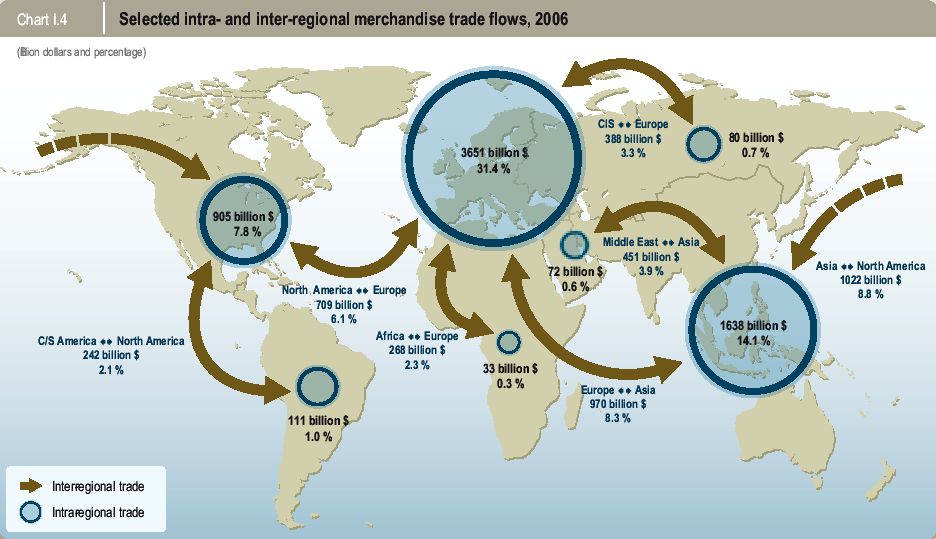

One need look no further than the U.S.'s trade data for proof of this effect. Using 2006 data, an in-depth analysis reveals that, of our top twenty per capita trade deficits in manufactured goods (the trade deficit divided by the population of the country in question), eighteen are with nations much more densely populated than our own. Even more revealing, if the nations of the world are divided equally around the median population density, the U.S. had a trade surplus in manufactured goods of $17 billion with the half of nations below the median population density. With the half above the median, we had a $480 billion deficit!

Our trade deficit with China is getting all of the attention these days. But, when expressed in per capita terms, our deficit with China in manufactured goods is rather unremarkable - nineteenth on the list. Our per capita deficit with other nations such as Japan, Germany, Mexico, Korea and others (all much more densely populated than the U.S.) is worse. My point is not that our deficit with China isn't a problem, but rather that it's exactly what we should have expected when we suddenly applied a trade policy that was a proven failure around the world to a country with one fifth of the world's population.

Ricardo's principle of comparative advantage is overly simplistic and flawed because it does not take into consideration this population density effect and what happens when two nations grossly disparate in population density attempt to trade freely in manufactured goods. While free trade in natural resources and free trade in manufactured goods between nations of roughly equal population density is indeed beneficial, just as Ricardo predicts, it’s a sure-fire loser when attempting to trade freely in manufactured goods with a nation with an excessive population density.

If you‘re interested in learning more about this important new economic theory, then I invite you to visit my web site at http://PeteMurphy.wordpress.com.

Pete Murphy

Author, "Five Short Blasts"

not "grossly flawed"

The problem is in Ricardo's theory, the means of production are assumed static, i.e. not mobile. In other words, it's only the finished good traded and instead they are trading people, they are trading labor forces.

Not supposed to do that for this infamous "win-win", but even so, there it also shows it's not always this win win.

That said, yeah, it's it amazing how population is ignored. They have made it political poison, when so much theory and statistics rest of the baseline of population, workforce.

I beg to differ that the trade deficit with China isn't a problem, uh, it ranges from 70-80% of the total goods, non-oil trade deficit! Bottom line fact there are 1.6 billion people over there, a never ending cheap labor supply, is a real problem, esp. when there is no "domestic consumption" despite all of the wishes, myths and agenda to make it so. Even if they do, so what, unlike China's goods, U.S. goods are .....made in China, so that does nothing for the American people, U.S. economy, it's only good for multinational corporations and "if" they pay any U.S. taxes, which most do not.

Most Productive

Weren't these stats inflated by using the productivity of the overseas labor that work was sourced to as if it was US labor?

I'm pretty sure I read that here.

Nothing hurt the US more than NAFTA and the transfer of jobs to Mexico.

still chasing it down but probably phantom GDP

I reference those in the outsourcing post. I'm becoming more exact in the accounting methods, scope of data but this is driving me nuts. We know China is killing us, the trade deficit is killing us, U.S. multinationals moved to China, millions of jobs lost, 5.6 million manufacturing jobs lost this decade, a decline in total STEM jobs, India body shops growing in profits and numbers, where their #1 customer is the U.S., yet extrapolating out from these metrics which is offshore outsourcing is a major exercise, if you can do it at all and claim it's valid.

Prodcutivity is in a way an indirect measure, notice output is real GDP for the nonfarm business.