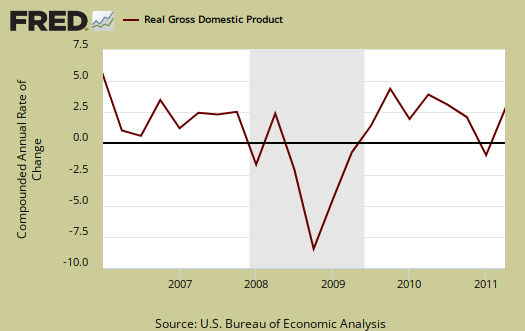

Q2 GDP 2011 2nd revision is in at 1.0%. This is a -0.3% revision from the Q2 advance report, which reported a 1.3% Q2 GDP. Here is the original BEA GDP report. Q1 2011 GDP was 0.4%. The BEA reports real GDP by one decimal place of accuracy. Not rounded, real Q2 GDP was 0.98%.

The Q2 GDP 2nd revision had a downward revision in exports, offset by an upward revision to personal consumption. As expected, imports were revised upward. Investment was the largest contribution by percent points.

As a reminder, GDP is made up of:

where

Y=GDP, C=Consumption, I=Investment, G=Government Spending, (X-M)=Net Exports, X=Exports, M=Imports*.

Here is the Q2 2011 second revision report breakdown of GDP by percentage point contributions:

- C = +0.30

- I = +0.78

- G = –0.18

- X = +0.41

- M = –0.33

Here is the Q2 2011 advance report breakdown of GDP by percentage point contributions:

- C = +0.07

- I = +0.87

- G = –0.23

- X = +0.81

- M = –0.23

Below are the percentage point differences, or spread between the Q2 2nd revision and Q2 advance 2011 GDP report components. As we can see personal consumption was significantly revised upward, imports upward, exports by half.

- C = +0.23

- I = -0.09

- G = +0.05

- X = -0.40

- M = -0.10

Here is the Q1 2011 report breakdown of GDP by percentage point contributions:

- C = +1.47

- I = +0.47

- G = –1.23

- X = +1.01

- M = –1.35

Below is the spread between Q1 and Q2 by percentage point contributions to GDP. As we can see the contribution change was a dramatic drop on personal consumption counter-balanced by a large drop in imports. Spread in the change to GDP point contributions are not the same as percentage changes. Percentage changes are listed further down in this article.

- C = -1.17

- I = +0.31

- G = +1.05

- X = -0.60

- M = +1.02

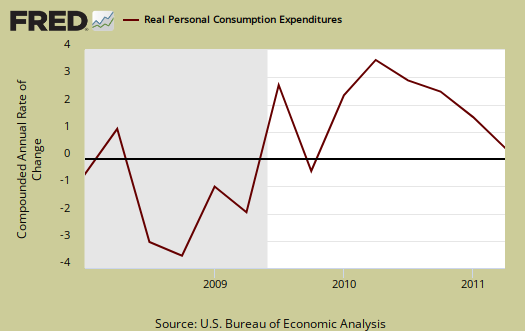

Below the the St. Louis FRED graph for C, or real personal consumption expenditures of the above GDP equation. As we can see from the above, while PCE, or C was revised upward, it is still quite repressed.

Below is the breakdown in C or real PCE annualized change. Notice when times are tough, durable goods (bright red) consumption drops. Notice the drop in durable goods this quarter. Durable goods has a –0.34 percentage point contribution in Q2, or a –5.1% decrease, in comparison to a 1.10 point contribution last quarter.

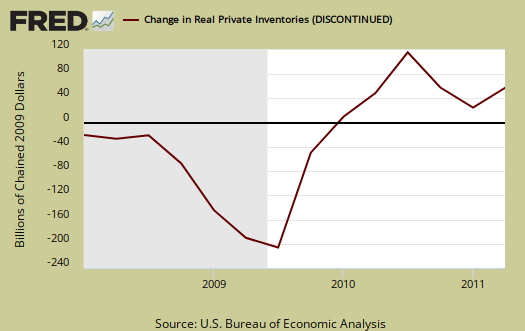

Changes in private inventories subtracted –0.23 percentage points to Q2 2011 0.98% GDP. Last quarter changes in private inventories contributed a +0.32 percentage point change. Seems the great inventory build up, recovering from the slash and burn of 2009 is over.

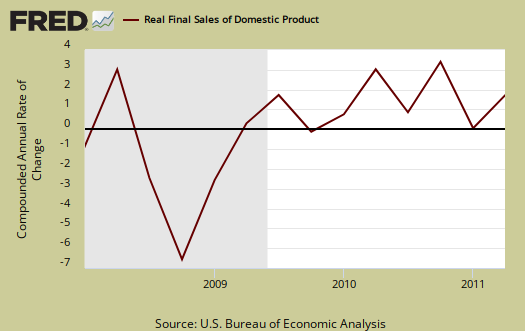

Below are real final sales of domestic product, or GDP - inventories change. This gives a better feel for real demand in the economy. This is slightly better news. Real demand increased 1.2%, versus a flat line or 0.0% for Q1. This is percentage change, not point contribution, so one might interpret real demand as barely breathing.

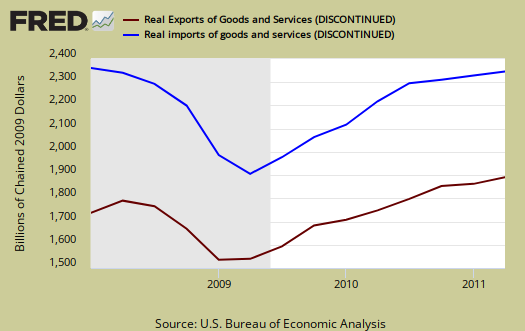

Below are net exports, or trade deficit, in real chained dollars, for Q2 2011.

The below graph shows real imports vs. exports. While exports increased 3.1% from last quarter, we have a deceleration of trade generally for Q1 exports increased 7.9%. Q2 imports increased 1.9% versus a 8.3% change for Q1. Bottom line, it is the trade deficit that matters for GDP, although volume of trade implies a slower global economy as well. Q2 trade deceleration in imports, actually helped overall Q2 GDP.

Below are the percentage changes of Q2 2011 GDP components in comparison to Q1. Realize there is a difference between percentage change and percentage point change. Point change adds up to the total GDP percentage change and is reported above. The below is the individual quarterly percentage change, against themselves, of each component.

- C = +0.4%

- I = +6.4%

- G = –0.9%

- X = +3.1%

- M = +1.9%

The BEA's comparisons in percentage change breakdown of 2nd quarter GDP components are below. Changes to private inventories is a component of I.

C: Real personal consumption expenditures increased increased 0.4% in Q2, compared with an increase of 2.1% in Q1. Durable goods decreased –5.1%, compared with an increase of 11.7%. Nondurable goods increased -0.4%, compared with an increase of 1.6%. Services increased 1.4%, revised from 0.8%.

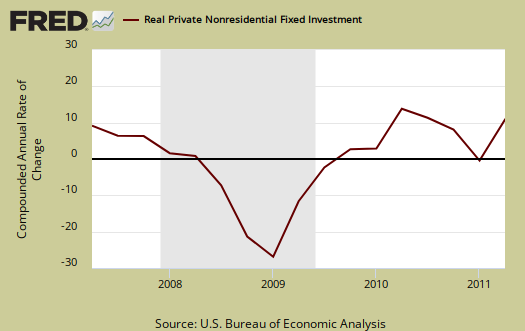

I: Real nonresidential fixed investment increased increased 8.7% in the Q2, compared with an increase of 2.1% in Q1. Nonresidential structures increased 15.7%, in contrast to a decrease of -14.3%. Equipment and software increased 7.9%, compared with an increase of 8.7%. Real residential fixed investment increased 3.4%, in contrast to a decrease of -2.4%.

X & M: Real exports of goods and services increased 3.1% in Q2, compared with an increase of 7.9% in Q1. Real imports of goods and services increased 1.9%, in contrast to a increase of 8.3% in Q1.

G: Real federal government consumption expenditures and gross investment increased 2.0% in the Q2, in contrast to a decrease of -9.4% in Q1. National defense increased 7.1%, in contrast to a decrease of -12.6%. Nondefense decreased -7.5%, compared with a Q1 decrease of -2.7%. Real state and local government consumption expenditures and gross investment decreased -2.8%, Q1 dropped by -3.4%.

Motor Vehicles subtracted -0.15 percentage points to Q2 real GDP while computer final sales added +0.11 percentage point changes. This is different from personal consumption, or C auto & parts. Motor vehicles are bought as investment, as fleets by the government and so forth and in Q2, they bought less.

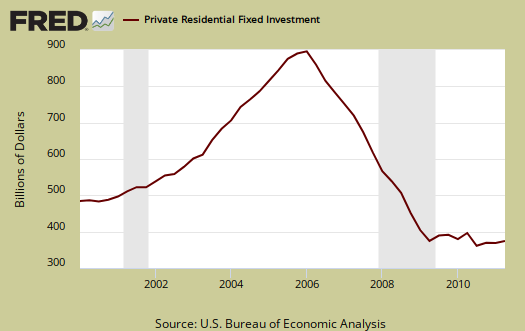

Residential fixed investment added +0.08 percentage points to Q2 GDP after subtracting a paltry -0.06 percentage points in Q1. Below is the raw totals on residential investment. If one could ever see the housing bubble and then it's collapse in terms of economic contributions, the below graph is it. Residential fixed investment changed +3.4% from Q1 2011.

Private, or not from the government nonresidential investment improved, with a 9.9% change from last quarter and a 0.94 percentage point contribution to Q2 GDP. Structures was a 0.38 percent point contribution, or a 15.7% percentage change from Q1 to Q2. Keep those technology changes and updates coming, for equipment and software were a 0.55 percentage point Q2 GDP contribution and a 7.9% increase from Q1.

To have enough economic growth to generate enough jobs to keep up with population, as a multiplier, GDP needs to be at least 2.5%, annualized, per quarter.

* In Table 2, the BEA reports GDP contribution components with their equation sign. If durable goods for example, decreased over the quarter or year, it is reported as a negative number. Imports, from the GDP equation, are already a negative for that is not something produced domestically. A negative sign implies imports increased for the time period and a + sign means the change in imports decreased. Or, from the GDP equation: . Confusing but bottom line exports add to economic growth, imports subtract.

percent point contribution spreads

I like looking at percent point contribution spreads because it tells me exactly what changes in terms of overall GDP change, or growth, specific to GDP. Kind of a mini metric within a metric.

That said, it might be confusing to some. What is useful, understandable in this overview to people? What is not?

I might change the format on point percentage change to a table for easier reading, but what else do people want amplified and clarified from the nitty gritty BEA numbers tables?

Also, much of this report we actually gave some reasonable estimates on this revision. I still expect imports are low balled, but the revisions do match the various monthly economic reports and their revisions.

Remember, the advance GDP report has to estimate some values because the actual raw data hasn't come in or been aggregated yet.

It's the 3rd revision that really matters, which is another month away.

Overall excellent, some questions

The article is outstanding for publication of analyses of econometric data -- very helpful and understandable explanatory notes.

Really excellent -- ALL useful and understandable.

Specific questions and comments --

What was the recent much-touted increase in durable goods orders? Just depleted inventories in need of restocking? It's weird to see steady increases in inventories (although down from peaking in 2010) with rate of change in final sales numbers bouncing around like a stumbling drunk. Are these graphs based on seasonal adjusted numbers?

I note pessimism in Asia (Eddie Tam in Hong Kong) as to USA Christmas orders.

Also, I think that I have been seeing some relation between inventories and liquidity problems lately, but I have no published sources for that.

Anyway, who cares about durable goods orders unless they are broken down into how much has been ordered out of China (always standing for more than just China) and how much within USA?

Mainly, what I wonder about is how is foreign investment handled relative to imports and exports? To what extent is "investment" a euphemism for the "selling of America"?

(I hope there is no such thing as "a stupid question"!)

durable goods inventories w.r.t. GDP

Durable goods, July is here, are wholesale orders, or orders to manufacturers to make more stuff.

What matters in the durable goods report are shipments, which June was revised significantly up so and the above link has some intel on it's approximation and relationship to investment GDP component.

PCE, is what is actually bought, retail and is more correlated to retail sales, June here, which is anemic, at best.

I'm actually surprised that PCE was revised upward as much as it was here from the other reports....

That said, I don't have all of the pieces to go from monthly reports to BEA NIPA accounting methods. I get messed up on price deflators #1, import/export prices....but I think if I did have the ability to calculate exact GDP estimates from monitoring monthly reports...then large multinationals would be using me as a consultant (hey, maybe I need to write some code to do just that!), instead of a niche site writer.

So, wholesale new orders implies more manufacturing business activity and should in part translate to new sales down the road (but this is for everything, exports, inventories, restocking). Shipments means it's "out the door" and when going from wholesale to wholesale implies investment if that makes more sense.

Dunno about inventories vs. liquidity but inventories are at record highs. Business inventories for June is here, so it's the change of inventories and by how much. it's slope vs. quantities.

In Q4 2008/Q1 2009 inventories were slashed and burned next to nothing so the fact we have all of this inventory sitting around well, to me it's not that great, I'd like to see more of it sold.

That's where that sales to inventories ratio number comes in and why people look at that alot to see which way the wind is blowing (business cycles).

Although these days, that entire "business cycle" theory, I'm kind of like...hmmm....

those are the local dips in the long slide down the mountain here. ;)

All of these reports are domestic only, only the U.S. economy. That said, with crazy global supply chains and offshore outsourcing, importing of foreign workers on guest worker Visas, I don't believe they catch everything on this.

There is research into globalization and it's shadow component to GDP (wrongly attributed).

This is something I think gov. statistics agencies need much more data, more information to really ascertain how badly are these global supply chains, offshore outsourcing, MNCs hurting the U.S. by macro economics...

but at the moment, they deny it's even hurting labor, so, sigh.

Seems to me I need to create tables for percent point contribution, plus add a few more bridges from the equation to the description of what that component is. I think that will help, those lists are too long to be comprehensible unless you're a numbers person. The point of these is to translate BEA numbers into visuals and descriptive and implications but show the path to connect all of those dots.

Thanks for answers

Okay, durable goods orders are for domestic manufacturing. That's only indirectly about ordering stuff from Asia or Mexico or wherever. Only indirectly about inventories. Really an index of business activity for the manufacturing sector.

Of course, durable goods orders are going to be related to investment in manufacturing as well as to productivity. That's why NYSE reacted favorably! So that was rational behavior.

Since increases in durable goods orders are presumably linked to marginally larger pay checks, durable goods orders are related to PCE. Of course, PCE must also be related to government payouts and (at least in 2008) such things as MEW. See, CalculatedRisk (2008)

About inventories, I understand "slope versus quantity" -- slope is the first derivative of a graph, so continuous positive slope means steady increase, even if second derivative is flat. That's why I am puzzled by "steady increases in inventories (although down from peaking in 2010) with rate of change in final sales numbers bouncing around like a stumbling drunk."

I would assume, given population growth, that inventories, sales and PCE would all steadily if slowly increase over time. Durable goods orders, however, would be subject to things like fluctuation in exchange rates (although not in the case of China). Similarly, although inversely, percent changes in PCE for durable goods (red bar in the graph) would also be sensitive to fluctuation in exchange rates.

I suppose retailers are just going to say "that month was good, this month not so good." No real trend, so keep doing what we have been doing, using annualized estimates.

By liquidity problems, I mean suppliers vs. retailers as to when or how soon goods are delivered vs. payment received in the supplier's bank account -- in other words, availability of goods at the retail level as payments are worked out. The result isn't failure to meet demand but it could be failure to meet demand until next month's payday. I notice lack of some items on shelves more often than used to be, also demand for payment up front before ordering parts ... and maybe that reflects some kind of liquidity problem. But there are many possibilities.

Sales come up a little, then flat for the next month. Up a little, then flat again. No trend except "could be worse" -- puzzling, especially considering population growth.

But there are many possibilities. Retailers are more competitive some months than others? Customers are more flush one month than the next? Relation of sales to price of gas or diesel fuel? Presumably, it's all based on inventory numbers in Cost of Goods Sold ... but there is the infamous transportation factor, with a delayed effect.

Probably, steady inventory growth is just that retailers are ordering based on annualized estimates and assuming growth.

It appears that you are 100% correct on the global supply chain thing, at least if we can believe the business-school kind of thing. "Supply chain management" is the bee's buzz these days. To me, that's an argument for a tariff -- or, since you prefer, VAT.

Trying to tax MNC corporate profits or net income on an 1120, although the international stuff is very complex, is like trying to measure flow of a river with a gauge set into a tube in the river. Sure you can measure the flow for the tube and that means you could estimate the flow for the river ... making many assumptions or having a whole lot of other data. But why not try the old dam approach? Water will still flow and you can estimate it closely. And since we have no choice but to maintain a dam anyway ....

I am still and have long been wondering about 'national accounts' and how foreign investment is handled there. You can sure get arguments on that subject! It seems like the media and even the academia spin is "those bad over-consuming lazy Americans, but they should quit complaining, they are lucky -- imagine year after year of negative exports, what a wonderful life!"

My thinking is that every negative export is one more nail in the 'For Sale' sign posted at our borders -- with a 'Sold' sticker now pasted over it.

BTW: A niche these days is good. That's what everybody is looking for. Of course, if some MNC offers the big bucks ... study the contract carefully!