Trump And Iran Sign MOU Deal Ahead Of Schedule

Summary:

- The US and Iran have remotely signed their memorandum of understanding to end the war and open the Strait of Hormuz ahead of schedule, and the agreement is now in effect, Axios reports.

- Trump admits energy stockpiles "run out in about four weeks"

- MoU signing could be As Early As Today

- Trump Says Will "Drop Bombs" If Bad Final Deal

- 14-Point US-Iran Draft Deal Released, Set For Friday Signing

Trump Signs Iran Deal Remotely Ahead Of Schedule

Confirming earlier speculation, Axios reports that the U.S. and Iran have remotely signed their memorandum of understanding to end the war and open the Strait of Hormuz, and the agreement is now in effect. The signing - which took place electronically between Trump, Vance and Ghalibaf - reportedly took place at dinner in France alongside President Emmanuel Macron.

The signing was supposed to happen in Switzerland on Friday, but a diplomat from a mediating country and a second source familiar told Axios earlier on Wednesday that there had been discussions about signing and implementing it earlier

The diplomatic source said the discussions around accelerating the timetable were intended to open the strait sooner than Friday, as both parties were in agreement on that issue. Another factor may have been the political pressure on the White House to release the text of the MOU, which it sitll hasn't done officially. The source familiar with the discussions claimed it was Iran that demanded the text not be published until the formal signing, and denied the White House was responding to political pressure.

The only "public release" so far consisted of a senior administration official reading the agreement to reporters in a briefing call on Wednesday, after days of confusion about what was in it.

Ahead of the signing, Iran's foreign ministry said the sides had agreed that the MOU should be signed electronically by both presidents. For Iran, the signing represents a major victory as it now stands to receive billions in unfrozen (and other) funds from the US and Gulf sources.

While it's now just a formality, the meeting between the U.S. and Iranian delegations headed by Vice President Vance and Iranian parliamentary speaker Mohammad-Bagher Ghalibaf is still expected to take place as planned on Friday in Switzerland. They are expected to discuss the launching of negotiations on Iran's nuclear program.

The signing took place after this remarkable press conference earlier in the day in which Trump tried to justify conceding to Iran's terms:

As BBC's Siavash Ardalan writes, Trump's responses to the reporters' questions to justify the agreement with Iran were bizarre and unprecedented in their own way:

They asked him how he could allow $300 billion in investment in Iran. He said, "We've already inflicted $2 trillion in damage on Iran; $300 billion is nothing in comparison."

They asked why he's giving Iran tens of billions of dollars. He said, "If we don't return their own money to them, other countries will be afraid to put their money in our banks, and then the dollar's position will weaken."

They asked why the missile issue isn't in the agreement. He said, "We've already destroyed 85% of their missiles anyway; the rest are buried underground, and besides, we sell air defense systems to the countries in the region so they won't worry about Iran's missiles."

They asked if he's not worried that Iran will say, "We're only producing nuclear energy for civilian purposes." He said, "You can't tell everyone else to produce electricity with nuclear power while only Iran can't."

Finally, he said, "If we continue sanctioning Iran, 91 million Iranians will die of hunger—what's the point of that, really?"

Oh, and he joked that "If [the Iran deal] works out, I'm going to take the credit; if it doesn't work out, I'm blaming [Vance]."

Meanwhile, in the aftermath of the signing, Iranian Foreign Ministry spokesman said Israel's continued attacks on Lebanon would be regarded as a breach of commitments, and adds that the US is responsible to force Israel to abide by the deal; the official also said the 60-day period starts today.

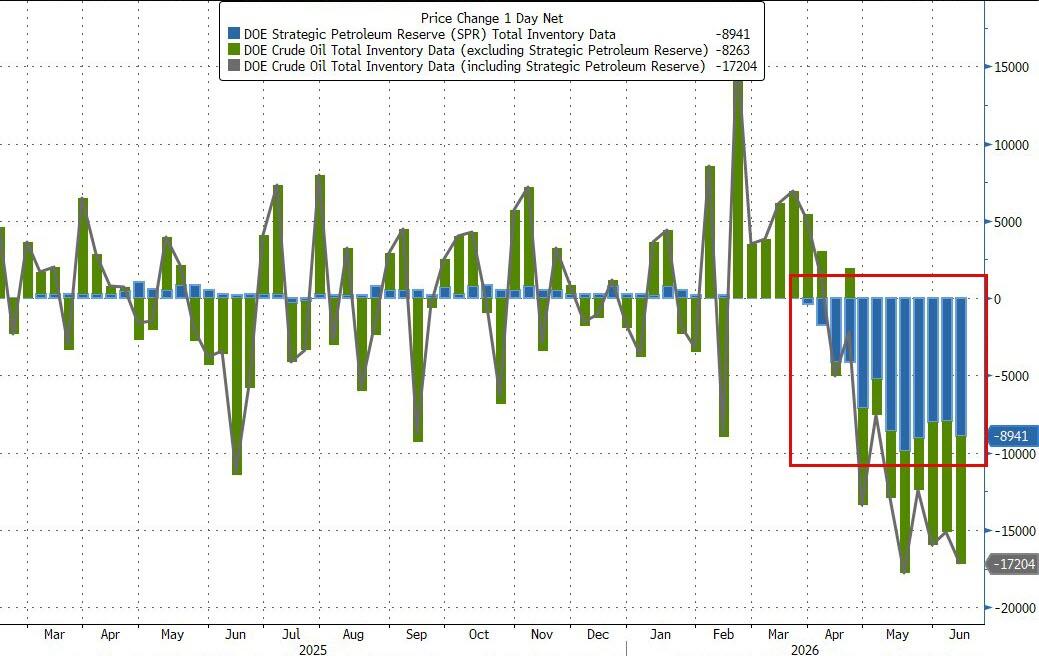

Trump Admits

President Trump's comment at the tail end of the G7 press conference about rapidly depleting crude reserves may have been the clearest admission yet of what is really driving the urgent push for an MoU with Iran to reopen the Strait of Hormuz.

"We run out of reserves in about four weeks," Trump told reporters.

View data here.

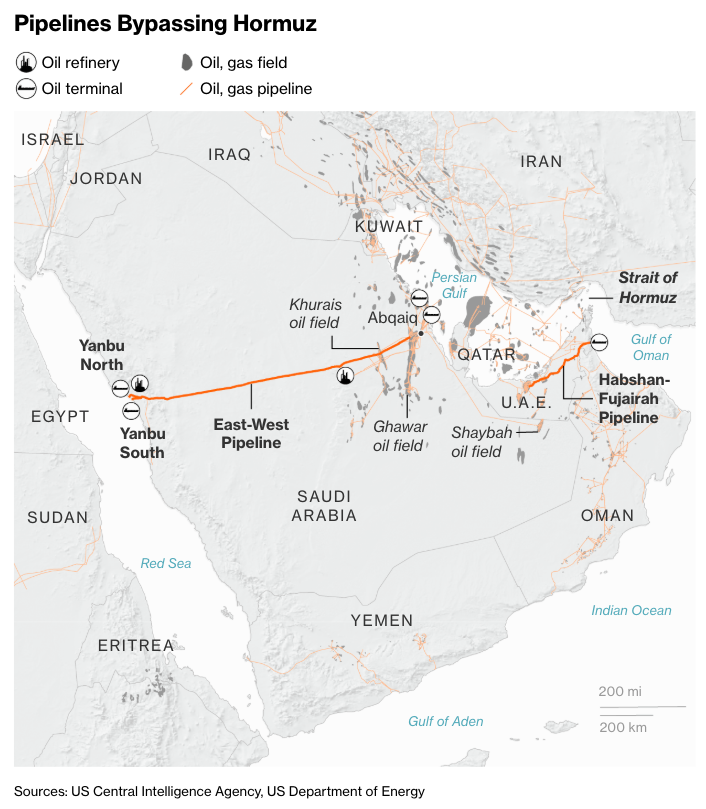

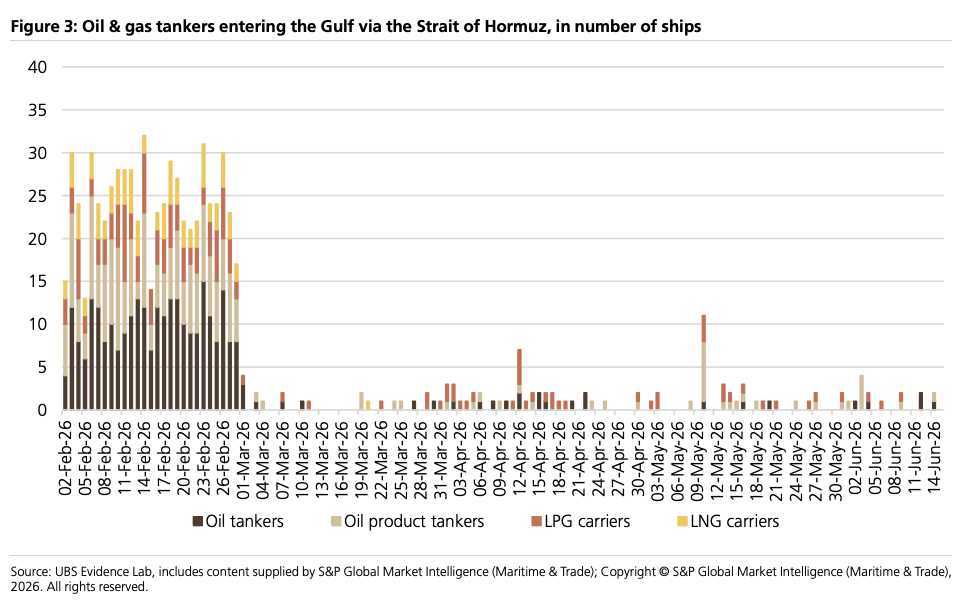

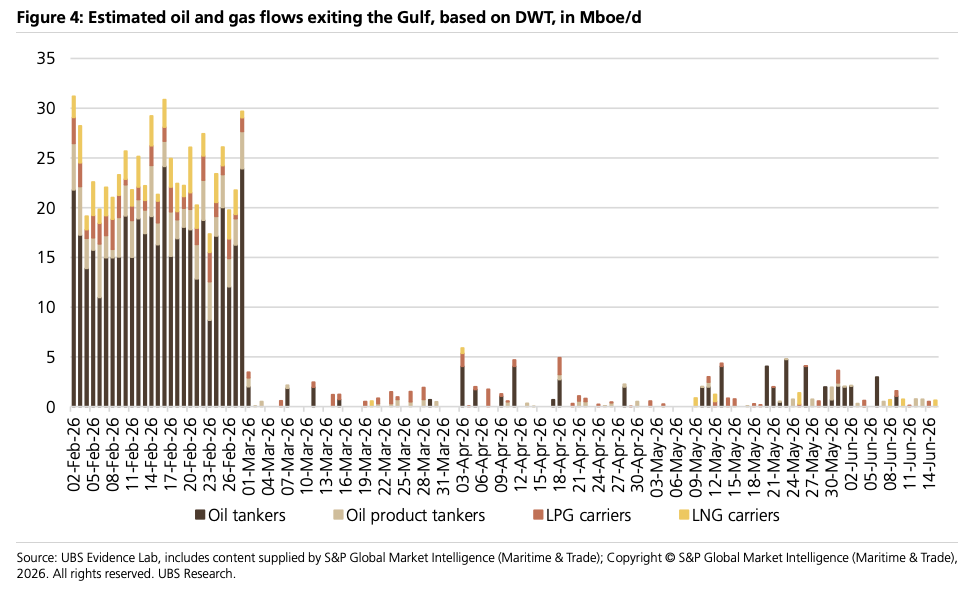

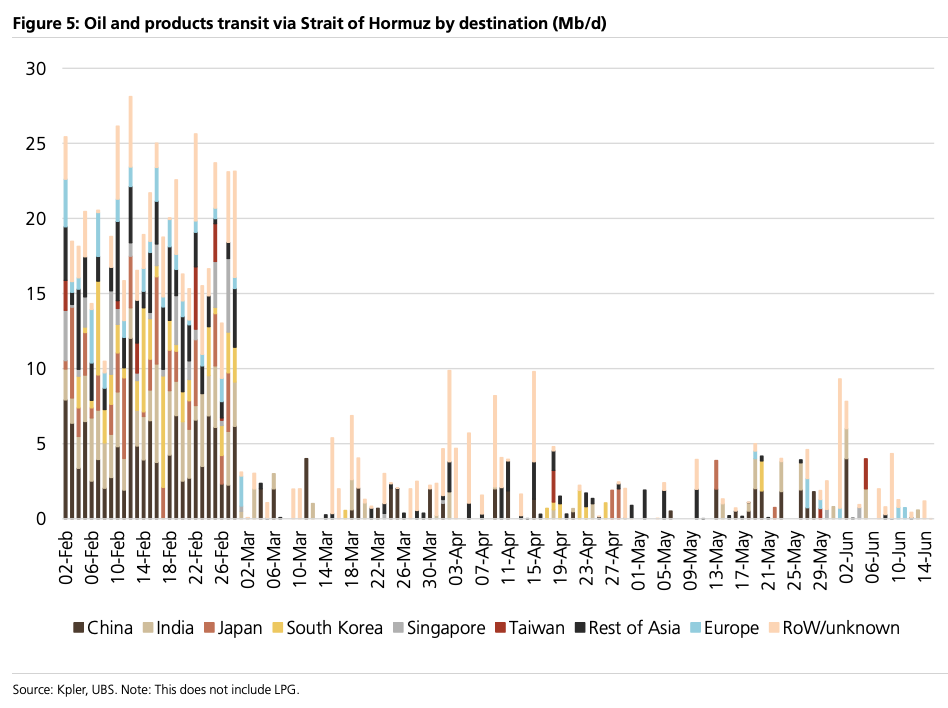

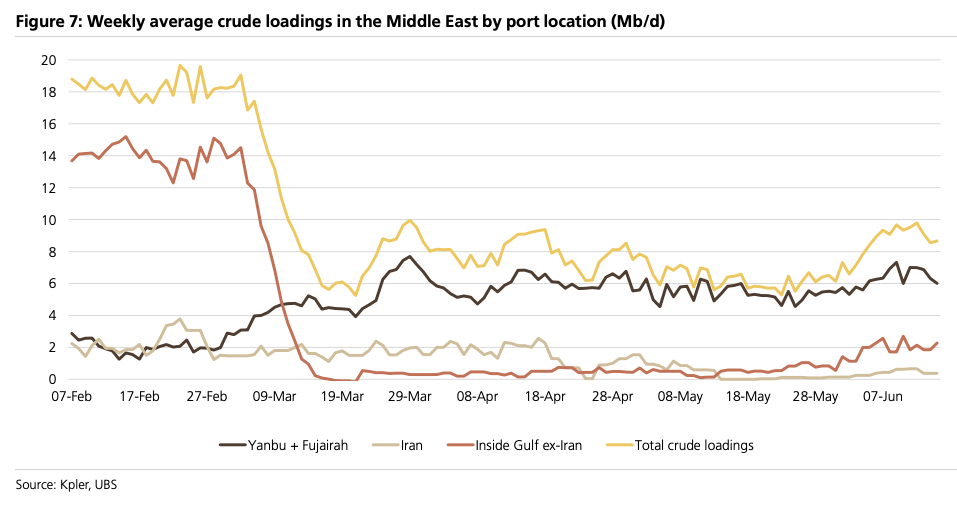

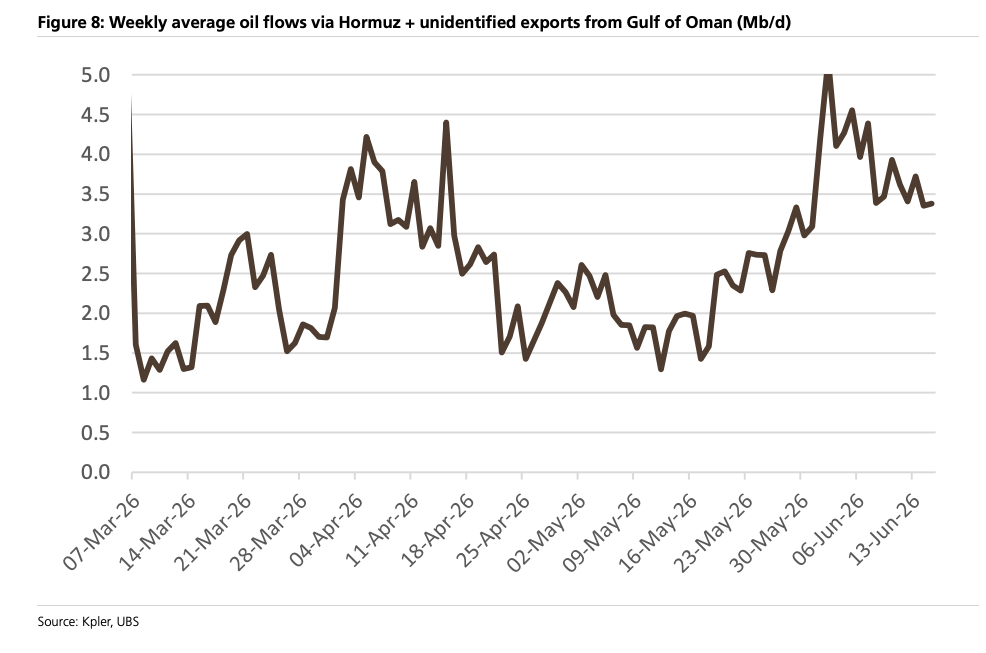

With global SPRs being aggressively tapped to offset lost Gulf energy production while the Strait of Hormuz remains shuttered, the clock is ticking closer and closer to midnight to fully reopen the waterway to restart the normalization process of tanker transits, which may take months.

The longer Hormuz stays closed, the faster emergency stockpiles are drained, raising the risk of an energy cliff, then a much worse energy shock. That urgency appears to be the real force behind the race to secure an interim agreement with Tehran.

Talk of Accelerated MoU Signing Timeline

Axios reports that US, Iranian, and mediator officials are discussing an accelerated timeline for signing the memorandum of understanding, moving it from Friday to as early as Wednesday, potentially via electronic signature.

More from Axios:

- The diplomatic source said the discussions around accelerating the timetable were intended to open the strait of Hormuz sooner than Friday, as both parties were in agreement on that issue.

- Another factor could be the political pressure on the White House to release the text of the MOU.

- The source familiar with the discussions claimed it was Iran that demanded the text not be published until the formal signing, and denied the White House was responding to political pressure.

Even if the electronic signing occurs early, Vice President J.D. Vance and Iranian Parliament Speaker Mohammad-Bagher Ghalibaf are still expected to meet on Friday in Switzerland to launch multi-month talks on Iran's nuclear program.

The takeaway here is that both sides appear aligned on quickly reopening the Hormuz chokepoint, as the world faces an energy cliff.

Watch Trump

President Trump is set to hold a very important press conference at the conclusion of the G7 summit in France.

Trump Tells Reporters At G7: We'll "Go Back To Dropping Bombs" if he Doesn't Like Final Deal

President Trump told reporters on the sidelines of the G7 summit in France that the pending U.S.-Iran memorandum of understanding is "not final" and warned that if he "doesn't like it ... we'll go back to shooting at them."

"If I don't like it [MoU], we'll go back to shooting at them, dropping bombs on their head," Trump said.

Trump repeated: "If they don't behave, we'll go right back to dropping bombs right smack in the middle of their head."

He added, "Because they misbehaved for 47 years. But nobody could've made this deal. The Obama-era JCPOA handed them $1.7 billion and gave them hundreds of millions of dollars in a Boeing 757. He tried to bribe his way out. I did not do that."

The proposed deal, expected to be signed on Friday in Geneva, would extend the U.S.-Iran ceasefire for 60 days and create a framework for negotiations over Iran's nuclear program.

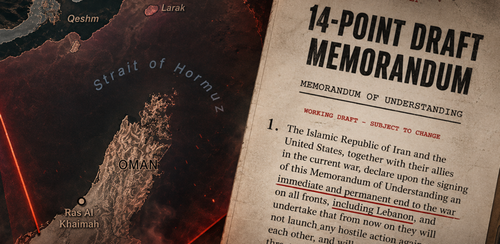

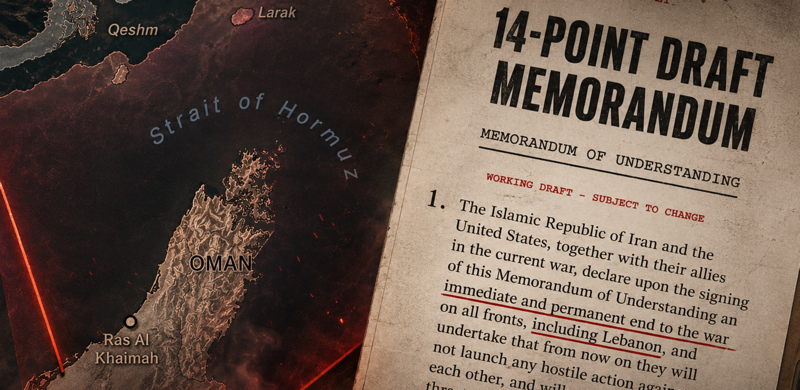

14-Point US-Iran Draft Deal Set For Friday Signing

With US and Iranian officials preparing to formally sign a memorandum of understanding in Switzerland on Friday, the conflict is entering the much-needed diplomatic phase to avert a potentially disastrous energy cliff. The MoU would open a 60-day negotiating window aimed at ending the war, restoring maritime traffic through the Strait of Hormuz, and hammering out the future of Iran's nuclear program.

Bloomberg published the text of the 14-point draft MoU, offering the clearest look yet at the proposed trade: de-escalation and sanctions relief for Iran, in exchange for a ceasefire across all fronts, commitments on shipping access, and a broader nuclear deal to be finalized by the end of summer.

But Iran's Tasnim news agency cited an unnamed official earlier today, saying some of the MoU published by Bloomberg is inaccurate. The report did not specify the discrepancies. Bloomberg noted that some of the wording could be different between the English and Persian versions.

Below is the text of the 14-point draft MoU:

1. The Islamic Republic of Iran and the United States, together with their allies in the current war, declare upon the signing of this Memorandum of Understanding an immediate and permanent end to the war on all fronts, including Lebanon, and undertake that from now on they will not launch any hostile action against each other, and will refrain from the threat or use of force against each other. The final agreement will confirm the provisions of this Article and the remaining Articles

2. The Islamic Republic of Iran and the United States undertake to respect each other's sovereignty and territorial integrity, and to refrain from interfering in each other's internal affairs

3. The Islamic Republic of Iran and the United States undertake to negotiate and reach a final agreement within a maximum period of 60 days, extendable by mutual consent

4. Immediately upon the signing of this Memorandum of Understanding, the United States Lift the naval blockade and prevent any interference or obstruction against the Islamic Republic of Iran, and restore traffic within a maximum of 30 days to its full capacity; the traffic of ships shall be proportional to the pre-war volume of traffic on the part of the Islamic Republic of Iran. The United States also undertakes to withdraw its forces from the surrounding areas within 30 days after the final agreement

5. Upon signing this Memorandum of Understanding, the Islamic Republic of Iran will immediately take steps to ensure that the movement of merchant ships from the Persian Gulf to the Sea of Oman and vice versa is resumed within 30 days to the pre-war volume, taking into account the need for the removal of technical obstacles and the neutralization of mines by Iran.

6. The United States undertakes, together with its regional partners, to create a comprehensive plan agreed upon by both parties for the rehabilitation and economic development of the Islamic Republic of Iran, While ensuring financing of at least $300 billion. The implementation mechanism of this plan, as part of the final agreement, will be formulated within 60 days.

7. The United States commits to ending, on a schedule to be agreed upon as part of the final agreement, all types of sanctions currently facing the Islamic Republic of Iran, including resolutions of the United Nations Security Council and the Board of Governors of the International Atomic Energy Agency (IAEA), and all unilateral U.S. sanctions, both primary and secondary.

8. The Islamic Republic of Iran reiterates that it will never produce nuclear weapons. The Islamic Republic of Iran and the United States have agreed that the fate of enriched material and the fate of all other mutually agreed nuclear-related issues, including Iran's nuclear needs, will be adequately addressed in a final agreement; the final agreement will confirm the provisions of this Article.

9. The Islamic Republic of Iran and the United States agree that, pending a final agreement, they will maintain the status quo: Iran will maintain the status quo on its nuclear program, and the United States will not impose new sanctions on Iran or strengthen its forces in the region.

10. The United States undertakes that immediately after the signing of this Memorandum of Understanding, and until the date of the lifting of sanctions, the United States Treasury Department will issue waivers for exports of Iranian crude oil, petrochemical products and their derivatives, and all related services, including banking, insurance, transportation, and the like.

11. The United States undertakes that, in light of the progress of negotiations towards a final agreement, frozen or restricted funds and assets of the Islamic Republic of Iran will be released and made fully available. These funds, whether held in the master account or transferred, will be used for any final beneficiary payment determined by the Central Bank of the Islamic Republic of Iran and will be fully available for use. The United States undertakes to issue all necessary permits and licenses on this basis.

12. The Islamic Republic of Iran and the United States agree that an implementation mechanism will be established to oversee the successful implementation of and future commitment to the Final Agreement.

13. Following the signing of this Memorandum of Understanding, and upon receipt of assurances regarding the commencement of implementation of Articles 4, 5, 10, and 11 of this Memorandum of Understanding, and the continued implementation of these steps, the Islamic Republic of Iran and the United States will enter into negotiations for a Final Agreement solely with respect to the remaining Articles.

14. The final agreement will be approved through a binding resolution of the UN Security Council

Based on the text above, the first take of the MoU appears to be front-loaded economic relief for Tehran in exchange for a ceasefire, a nuclear freeze, and commitments to negotiate hard topics, such as the nuclear program, at a later date.

Who Stands To Benefit:

Tehran benefits most directly because it gets economic oxygen, oil waivers, frozen funds, sanctions relief language, and reduced US military pressure in the region.

Hezbollah and Iran-aligned actors also benefit if "all fronts, including Lebanon" locks in a ceasefire that constrains Israeli operations.

And, of course, the global economy because global shippers benefit if Hormuz reopens and war risk premiums in crude oil collapse.

The Gulf states benefit if the conflict ends because energy exports through the Strait of Hormuz will resume. A report on Tuesday said that QatarEnergy was planning to ramp up LNG production in the coming months.

Where is Leverage Lost:

The US loses some coercive leverage once the Hormuz blockade ends, oil waivers are granted, and asset-release mechanisms begin.

Israel loses freedom of action if the agreement binds the Lebanon front and limits further strikes.

Sanctions and hawks lose leverage because the draft moves quickly toward broad sanctions dismantlement.

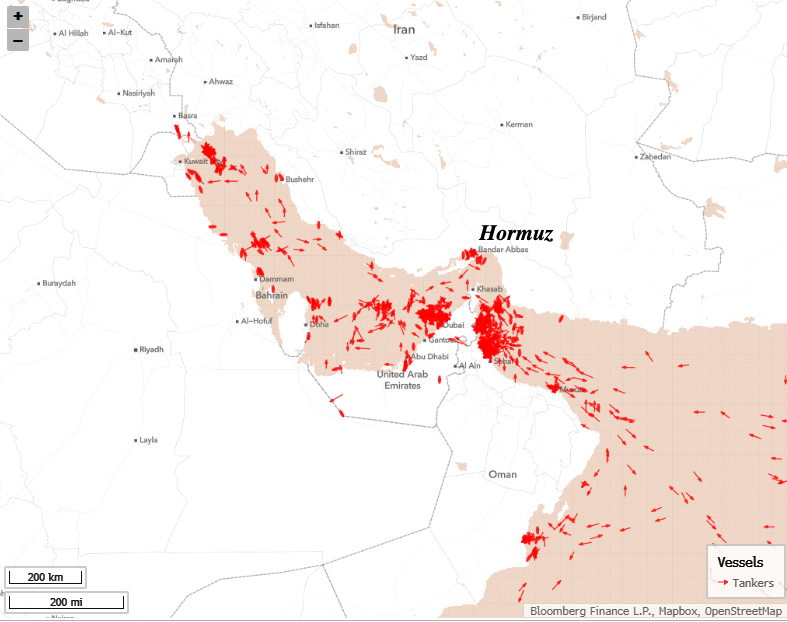

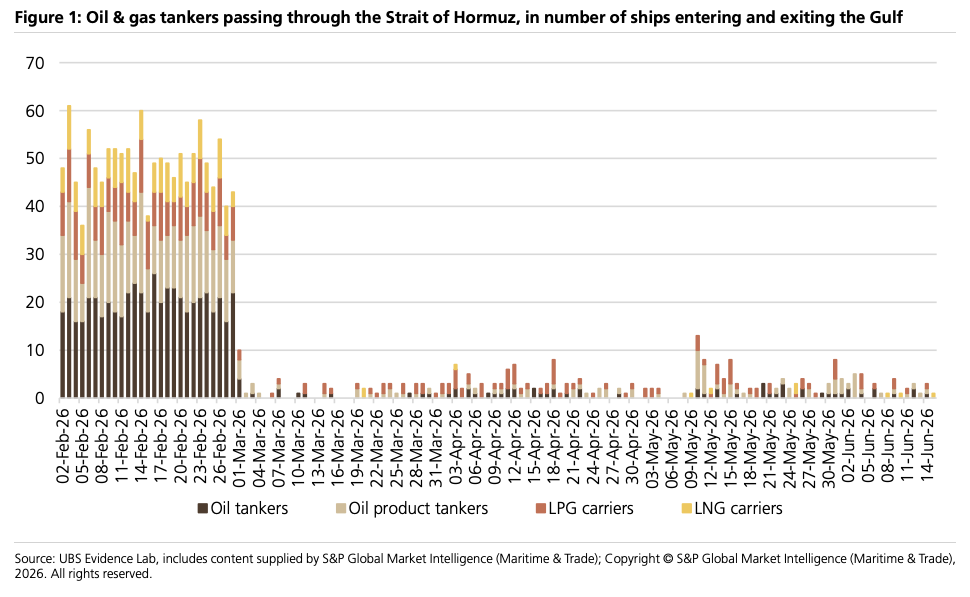

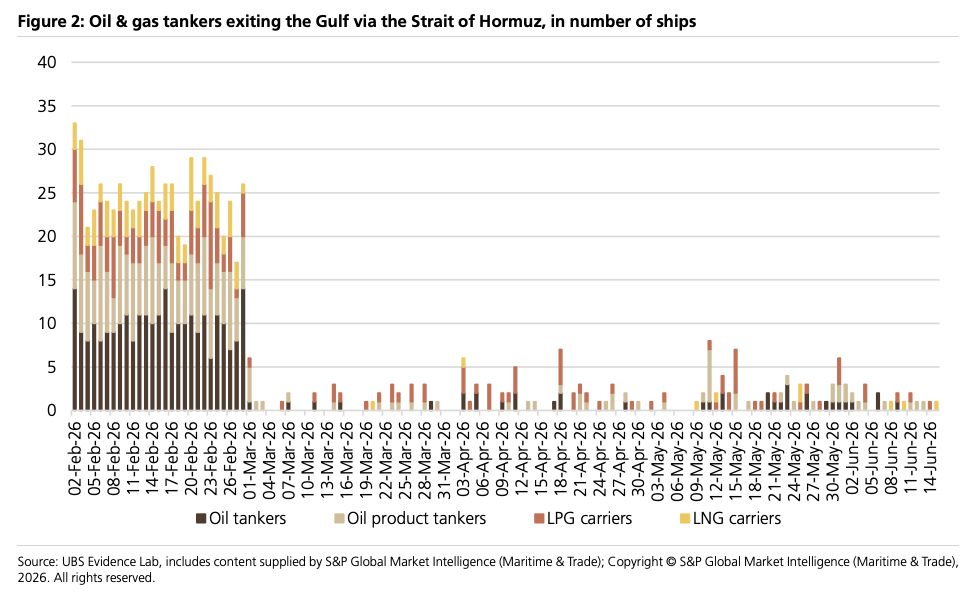

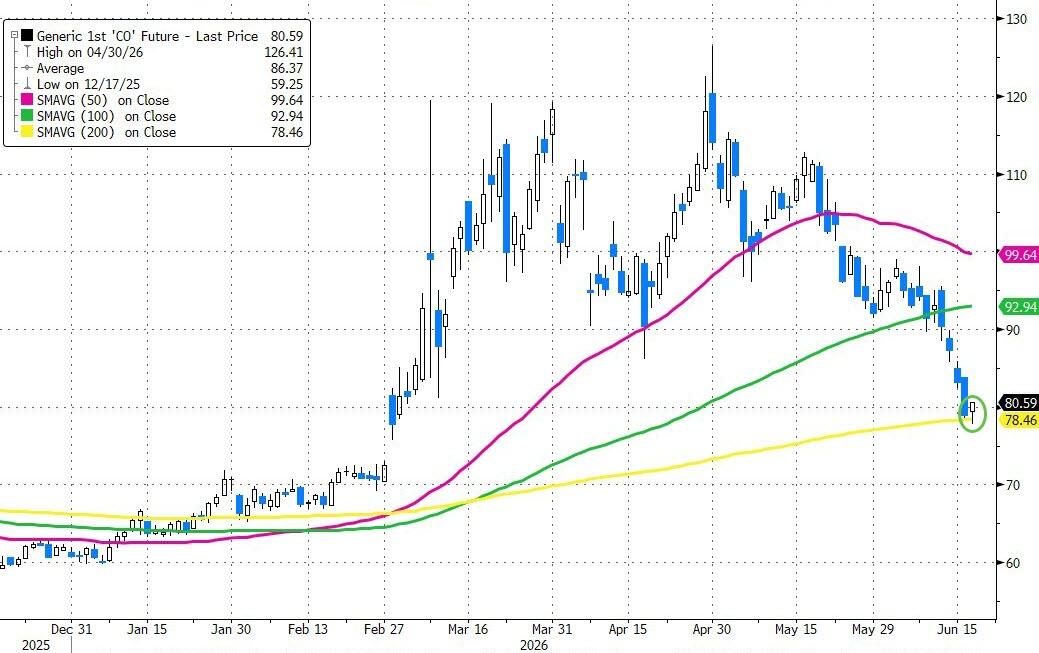

The urgency behind the MoU and locking in peace talks for 60 days, with a formal signing event at the Bürgenstock resort in Switzerland on Friday, stems mainly from the world being headed for an energy cliff, as SPRs globally were being drained to offset the loss of Gulf production with the Hormuz chokepoint shuttered. Brent crude futures edged down overnight, trading around $79 a barrel on Wednesday morning.

One of the biggest uncertainties remains the Strait of Hormuz. President Trump stated that the critical waterway will reopen permanently and be toll-free, but the MoU suggests the toll-free arrangement may only last through the 60-day negotiation period. Another major uncertainty is Tehran's compliance.

Most Important Overnight Headlines (courtesy of Bloomberg):

US-Iran Deal Framework

• The US and Iran plan to formally sign a memorandum of understanding on Friday, June 19, 2026 in Switzerland, paving the way for 60 days of talks aimed at ending the war and limiting Iran's nuclear program

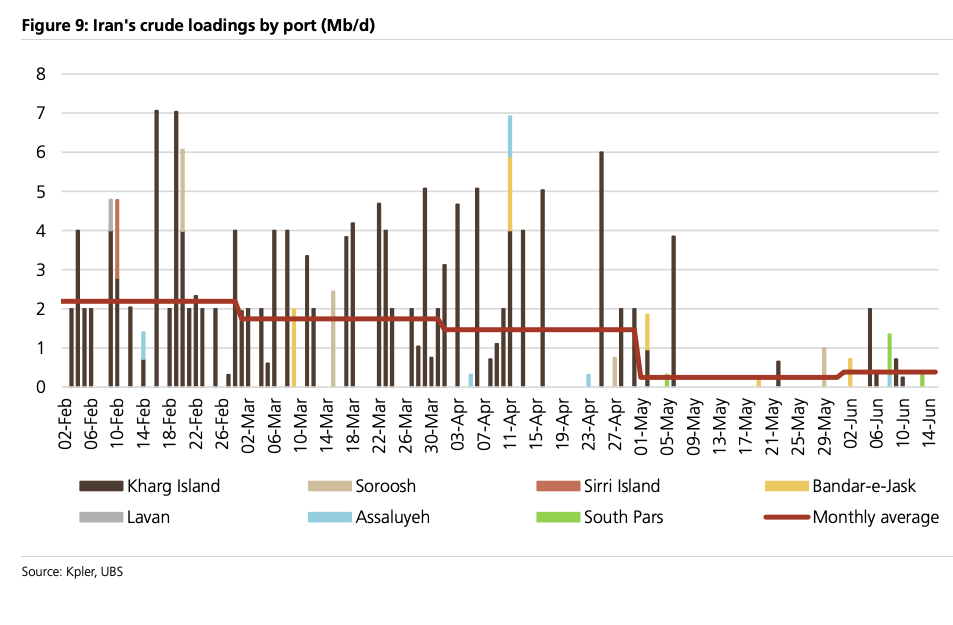

• Iran will immediately take steps to reopen the Strait of Hormuz once the tentative deal is signed and will be allowed to sell its oil without restrictions, according to leaked copies of an interim agreement

• Iran is set to receive broad financial incentives including the right to sell oil immediately, access to a $300 billion development fund, and eventual access to frozen assets

• The US would secure at least $300 billion to rebuild Iran after the war under the accord Web Content - US 6:43 AM

• The memorandum states only that Iran's stockpile of near-bomb-grade uranium be 'adequately addressed,' leaving unresolved the fate of enough material to fuel multiple weapons

International Reactions

• Senate Republicans are pressing the Trump administration for details on the deal and signaled Congress will ultimately vote on the final agreement

• European officials are wary of committing naval ships to clear Iranian mines from the Strait of Hormuz because of confusion about how the work would be done and Trump's strict end-of-week timeline

• China's Foreign Minister Wang Yi called for greater international support for the next phase of Iran-US peace talks on Tuesday, cautioning that the interim agreement marks only the beginning of a longer peace process

• European allies disagree with Trump's optimism that trade can resume by week's end and have practical questions about what was agreed before committing to de-mining missions

Shipping and Energy Markets

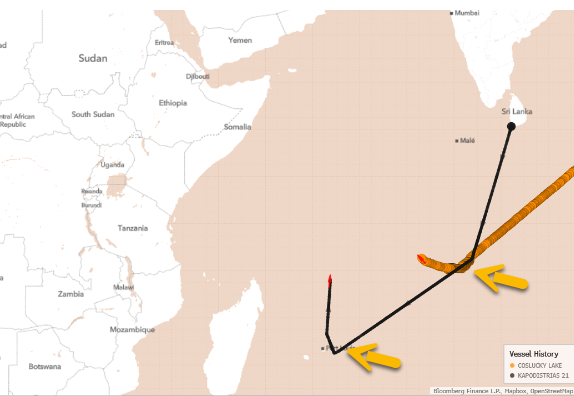

• A third fully-loaded crude tanker, the Suezmax Sonia I capable of hauling about 1 million barrels, left the Iranian port of Chabahar on Tuesday night and crossed the US blockade line heading toward Singapore

• Two oil tankers heading toward Africa U-turned in the Indian Ocean this week, switching destinations to the Middle East as shipowners race to re-position vessels ahead of the possible Strait of Hormuz reopening

• Qatar is beginning to bring some of its LNG tankers back to the Middle East, with at least four empty vessels recently heading toward the region after being idle or heading in a different direction

• Brent oil fell below $80 a barrel on Tuesday for the first time in more than three months as the US-Iran deal boosted expectations for a revival in supply

• The prediction market Kalshi assigns a 51% probability that Strait of Hormuz traffic will return to normal before August 1 and a 68% probability before September 1

Oil Market Impact

• The IEA said world oil consumption will slump by 1.1 million barrels a day this year, the biggest drop since the Covid pandemic in 2020, as higher fuel prices and disruptions curb buying

• The IEA previously expected a decline of about 420,000 barrels a day, making the revised forecast much deeper than anticipated

• A potential peace deal paves the way for a renewed supply glut in 2027, according to the IEA

Tyler Durden

Wed, 06/17/2026 - 18:15

The Small Business in Transportation Coalition said the U.S. Department of Transportation has failed to enforce federal law after finding states out of compliance. (Photo: Jim Alen/Freightwaves)

The Small Business in Transportation Coalition said the U.S. Department of Transportation has failed to enforce federal law after finding states out of compliance. (Photo: Jim Alen/Freightwaves)

An Iranian woman waves a national flag at Valiasr Square in Tehran. Photograph: Atta Kenare/AFP/Getty Images

An Iranian woman waves a national flag at Valiasr Square in Tehran. Photograph: Atta Kenare/AFP/Getty Images

Recent comments