The ForeclosureGate scandal poses a threat to Wall Street, the big banks, and the political establishment. If the public ever gets a complete picture of the personal, financial, and legal assault on citizens at their most vulnerable, the outrage will be endless. (Image)

Foreclosure practices lift the veil on a broader set of interlocking efforts to exploit those hardest hit by the endless economic hard times, citizens who become financially desperate due medical conditions. A 2007 study found that medical expenses or income losses related to medical crises among bankruptcy filers or family members triggered 62% of bankruptcies. There is no underground conspiracy. The facts are in plain sight.

ForeclosureGate represents the sum total illegal and unethical lending and collections activities during the real estate bubble. It continues today. Law professor and law school dean Christopher L. Peterson describes the contractual language for the sixty million contracts between borrowers and lenders as fictional since the boilerplate language names a universal surrogate as creditor (Mortgage Electronic Registration System), not the actual creditor. Other aspects of ForeclosureGate harmed homeowners but the contractual problems that the lenders created on their own pose the greatest threats.

When the Massachusetts Supreme Court upheld a lower court ruling that the actual creditor must be named in the mortgage agreement (a legal requirement that the banks forgot to meet in their contracts), there was consternation on Wall Street. What would happen if a class action lawsuit challenged these flawed mortgages? Isn't the Massachusetts decision the latest of many attacking the legal basis of the shoddy business practices and boilerplate industry contracts? What if homeowners started walking away from their underwater mortgages based on the legally flawed contracts? If there were a viable prospect of a class action suit against financial institutions threatening to invalidate these contracts, wouldn't that crash the stock values of the big banks and some Wall Street firms?

The big banks and their partners on Wall Street need a preemptive strike to derail the legal process that threatens their existence. They may get a temporary reprieve through pending consent decrees from the United States Department of Justice and consortia of state attorney's general. If that protection fails, big money will make every effort to buy a bill from Congress that absolves them retroactively, en masse. The consent decree might cost them a few billion dollars. That's much better than owing the trillions in lost home values due to their contrived real estate bubble and stock market crash.

As bad as this is, it gets worse.

Beyond ForeclosureGate

The surface scandal is about fraudulent business practices and a systematic assault on homeowners by lenders, servicers, and the legal system. A much broader picture must be viewed in order to understand the utter contempt that the ruling elite has toward citizens and the depraved tactics used to express that contempt, all to serve endless desire to accumulate more money and power.

The set up began when we heard about the ownership society in the 2004 presidential election. President Bush defined ownership as taking the government out of our lives so more people could own homes and control their destinies. The foundation was home ownership. As Bush said on the campaign trail, "We're creating a home -- an ownership society in this country, where more Americans than ever will be able to open up their door where they live and say, welcome to my house, welcome to my piece of property" October 2, 2004.

Then Federal Reserve Chairman Alan Greenspan was uncharacteristically coherent when he laid the foundation for the swindle earlier that year. Greenspan told the Credit Union National Association that the fixed rate mortgage was "an expensive way of financing a home." He was clear when he advised lenders that, "consumers might benefit if lenders provided greater mortgage product alternatives to the traditional fixed-rate mortgage." February 2, 2004. Home equity through exotic mortgage products fueled consumption and became the new "margin account."

The Chairman of the Federal Reserve and the president ratified the real estate bubble, already underway at the time, as political and financial doctrine. The advice was clear. Get an ARM, own your piece of the American Dream and spend that equity. Housing prices never go down, right?

Freddie Mac, Fannie Mae, Wall Street and the big banks provided the back room. Mortgage Backed Securities (MBS) derivatives were vastly expanded. This made it easy for more homebuyers to qualify for mortgages they might not otherwise get, credit standards dropped. Those with good credit saw an array of tantalizing zero interest loans and other mortgage products to maximize available cash and feed the stock market.

It was all good until it wasn't.

The real scandal is the unfathomable loss of wealth and opportunities by the vast majority of citizens and the vicious attack on the most vulnerable citizens as a part of that process. The attack continues and is worthy of review.

Foreclosure and Bankruptcy

Foreclosure is the down side of the ownership society. When you're sold a bill of goods, a property that you were told you were qualified to buy, and you lose it, you are evicted from ownership island.

Before Congress passed the 2005 bankruptcy reform act, homeowners could avert foreclosure in many states by filing for bankruptcy. Not just anyone could qualify. The process of qualifying was difficult and, oftentimes humiliating. But homes were saved and families were preserved with a chance to start over.

A myth emerged of the bankruptcy abuser, a high-class sort of welfare cheat. These reckless people worked the system to rack up large debts that were subsequently wiped clean through bankruptcy. The alleged abuse of the system became the excuse for a major overhaul of bankruptcy law. The legislation passed the Senate with 74 yes votes and soon became law.

The changes since the 2005 legislation provide substantial benefits to creditors. Morgan et al summarized the direct benefits to creditors in a forthcoming publication in the New York Fed's Economic Policy Review. Before bankruptcy reform, the filer of a bankruptcy claim used to determine Chapter 7 or 13 filing status. That makes a difference in the amount and type of debt relief. The legislation imposes means test that determines precisely which chapter (7 or 13) filers must use. Significantly, chapter 13 filers retain more debt from medical and other unsecured credit.

Legal costs ranged from $600 to $1500 before bankruptcy reform. Legal fees now range between $2800 and $3700. Previously, there was no requirement for credit counseling prior to filing.

Filers must now document approved credit counseling six months before filing or face dismissal of their case(Morgan et al.). This counseling requirement can lead to unwarranted dismissals or inordinate delays in filing at a time when filers need relief.

Under the old law, only bankruptcy trustees appointed by the federal court could file claims of abuse by the filer. Under the new legislation, anyone can file a claim of bankruptcy abuse, which can lead to a dismissal of the cause. This is a huge benefit to lenders who wanted to keep citizens from realizing debt relief.

The Real Benefit for Big Money - Delayed Bankruptcy Filings

The new law makes it harder to file a claim, doubles costs, and gives the creditors a say in claiming fraud on the part of those who file claims. Significant delays in filing for bankruptcy became the norm.

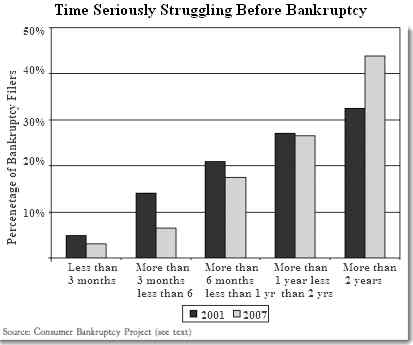

Time is money for loan servicers. A long delay before a bankruptcy filing, allows servicers the opportunity to add on special fees, many of which the borrower can't comprehend. One thorough study showed that many of these fees were questionable. The longer it takes, the greater the revenue opportunities. Delay benefits creditors since loan payments continue at their original level.

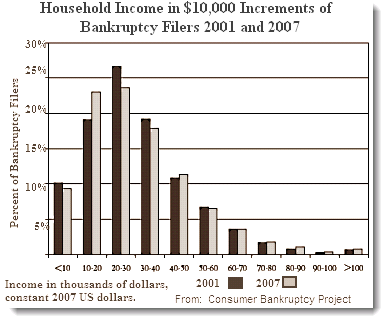

What happened to those big spending, reckless bankruptcy abusers that were the rationale for the 2005 reforms? The following graph from the Consumer Bankruptcy Project shows that there is virtually no difference between the incomes of filers before and after bankruptcy reform. The majority of filers made between ten and forty thousand dollars a year before reform. That has remained virtually unchanged. The big spending abusers were and remain a mythical construct; the centerpiece of a diversion strategy to keep attention away from this never-ending gift to creditors.

These newly empowered creditors were the same creditors who hired debt collectors to try and frighten people out of their filings. A major study found that 24% of filers reported that debt collectors told deliberate lies to avoid bankruptcy. They heard that filing for bankruptcy would lead to jail, job loss, or an IRS audit. Some were told that it was illegal to file for bankruptcy. Lawless, et al. Did the Bankruptcy Reform Fail? An Empirical Study, October 2008

The deck was stacked early against citizens and protection from creditors disappeared under the new law. The creditors, who so recklessly precipitated the economic collapse, came out on top. They were free to profit in any way they could from their new market,

What Causes Bankruptcy - Financial Shocks from Medical Expenses

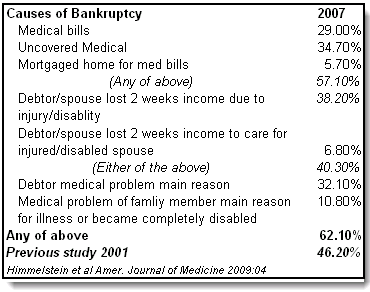

Prior to the new law, the major cause of bankruptcy stemmed from medical care expenses and the resulting disruptions to families. Rather than the mythical big spender contrived by Congress, for nearly half of filers, major medical expenses, family tragedies, were the tipping point to a loss of financial viability.

The Consumer Bankruptcy Project audited a representative sample of bankruptcy filers in 2001. The audit found that 46% cited a "major medical cause" for bankruptcy. This includes the direct cost of uncovered medical bills for major illness or injury, lost work due to the same, and the need to mortgage the family home to cover medical costs.

{kind=link}

Did Congress review this data? Were they intent on making it harder to file bankruptcy as a result of illness? When bankruptcy is delayed or simply not attainable, less money is available for needed medical care. Were the members supporting bankruptcy reform indifferent to the suffering compounded by their thoughtless legislation?

The situation is worse now. A comprehensive survey of those who filed bankruptcy in 2007 showed the increasing desperation of those faced with medical problems. When individuals or family members are in dire need of medical care, do they just sit home and suffer?

Nearly two thirds of bankruptcies result from medical care that people can't afford or losses in income from medically required leave. Where are the big spending cheats?

Nihilists at the Helm

The big banks, Wall Street, the politicians they own, and the Federal Reserve Board created the real estate bubble in bad faith.

They knew or should have known:

- that the real estate bubble was unsustainable;

- when the bubble deflated, many homeowners would hit a financial wall; and, that

- when homeowners hit the wall, to maintain viability for their families, they would need relief of some sort.

What did the nihilists of the financial elite and their hit men walking the halls of power do with all this knowledge? They went ahead with the real estate bubble, fostered it, deregulated meaningful controls on the financial industry, and crafted a new bankruptcy law to stick it to filers. They knew or should have know that data from 2001 showed a very high rate of filings due to the financial stress of medical care. Did they care? Do they care now? Has anything been done to correct this injustice?

Citizens suffer financial distress, often due to illness, at the behest of influential bankers and investors. At the same time, the Department of Justice crafts a settlement with lenders and their representatives to relieve them of the stern justice due for their specific crimes and the larger horrors they visit upon citizens.

We are most emphatically not a nation of laws. We are a nation where the law is used by a very few for their own purposes, without regard for the well being of the nation or its citizens. We are a lawless nation

END

This article may be reproduced entirely or in part with attribution of authorship and a link to this article.

In Economic Populist, also see:

ForeclosureGate Deal - The Mandatory Cover Up by Michael Collins

The Arc of Justice - The Ibanez Case Ruling by Numerian

An Update on the Foreclosure Mill by Robert Oak

Is Residential Real Estate a Ticking Time Bomb? By Robert Oak

Comments

very nice connection

I recall some mention of allowing bankruptcy judges to give a haircut on mortgages, of course that very good idea to keep people in their homes was squashed like the other bugs of the middle class.

Homeowners are the only ones getting a hair cut.

And it's a buzz cut against their will.

It all fits together for the Money Party - they run the swindles, buy the government, fix the cases, and come out ahead of the game. The idea that the administration would float a $20 billion settlement offer is offensive to everyone. How about the $6 trillion loss in wealth by the people. It was a deliberate scheme to squeeze everybody. Then they turn around and drain every last ounce from people who have medical emergencies but lack sufficient health insurance. I'm sure the geniuses who brought on the ruin think they're superior for surviving. If they worked for any thing resembling a normal organization, they'd all be fired for cause. Instead, they continue to prosper. They are a toxic asset.

Michael Collins

My advice to the seriously struggling

Don't seriously struggle. Let the banks have the under-water house and go rent. Go to cash only transactions, cut up your credit cards. Tell the bill collecors to go screw themselves. Get rid of your land line and get a cell phone. Keep your personal assets in judgement-proof accounts, like IRAs if you have them. The only way you will get change in this country is to stop cooperating with the crooks. Look at the French -- they do general strikes. We can learn from them. FICO is a bankster scam. Chapter 13 is a scam foisted on the American people.

Yes, I pay my bills because I can afford it, but my heart goes out to the seriously screwed. I understand their angry. I also recall a quote from President Richard Nixon -- "Don't get mad, get even."

Now I wouldn't say that the

Now I wouldn't say that the Bankruptcy Abuser was a myth. But familarity with bankrupty laws and figuring out who is able and willing to pay you back is SUPPOSED to be the core competency of those making loans. But by subsittuting regulatory capture for good business sense, the debt pushers pushed "bankrupty reform" as a way of being bailed out of their own bad business decisions. Changing the bankruptcy laws making it harder to escape from EXISTING debt was a HUGE gift to the credit card companies. There will will ALWAYS be people standing in line, waiting for a chance to borrow their way to the poor house. One of the reasons for bankruptcy law is to discourage others from making those loans to them.

The statistics in Warren's

The statistics in Warren's paper do not hold up.

http://www.theatlantic.com/business/archive/2009/06/elizabeth-warren-and...

http://www.theatlantic.com/business/archive/2009/06/why-warrens-new-bank...

The numbers are fine

It's actually Himmelstein, et al. who should be tagged with any problems with the analysis, which I don't think are significant. Warren is a second author, although it's easy to tag criticisms by using her well known name. The study on 2001 data and 2007 were done through survey research techniques described in detail in the article. In the two "acting out" reviews by McCardle, there was no real attack on this so the numbers stand. The methodology didn't yield what McCardle expected from her "Googling" but that's not a reason to doubt the numbers and, as I pointed out, the methodology wasn't challenged. The final critique by McCardle was to disparage those who file. This reveals McCardle's character and discretion sufficiently to cause me to dismiss her. Critiques of any major study are vital, even when peer reviewed as the studies cited were:

McCardle says the popularity of this study is extensive and, from that, she concludes that the authors manipulated the numbers to achieve that end. That's post hoc ergo propter hoc (at its worst)and it's also defamatory. If there was data manipulation in these articles (as opposed to errors of some sort) then the authors would be accountable to the university and the journal would have to retract. McCarcle combines a logical fallacy that most high school debaters would notice with a casual defamation as part of her critique.

I'll stick with Himmelstein et al. and say there should be more studies of these issues. If the numbers are inflated 10%, due to sampling error (which I doubt), they are still significant and show that the system ultimately ends up exploiting those with little chance to defend themselves and who are in the midst of a crisis.

Michael Collins

HISTORY

Just remember that a prime mover of the 2005 legislation was none other than our dear presidents assistant, Joe Biden.

The Senator from MBNA

Thanks for pointing that out. I should have elaborated a bit after the 74 vote Senate majority was referenced. The Senate shamed itself that day. Clinton vetoed this. It was just too much.

It would be worth doing a correlation with bankruptcies prior to the vote in the states where two Senators voted for the bill. They don't care. They don't have to.

Michael Collins

Enough with the theoretical...

I have personally been coming land records and posting the results on the internet. How would you feel if 50%-70% of the land records have fraud on the face of the document. We have felonies in the public record and we can't prosecute? you don't even need discovery. It's public record with names attached! This isn't hard.

It's so obvious it is in your face.

How does this look , compare signatures.

These documents where supposed to clear title. Now they are clouded.

https://docs.google.com/document/pub?id=1OdFaLKtGzg8bYxD3DBXcSGo0rM_CTtk...

or this the Corporate Vp and the Notary have the same signature.... I've witnessed myself do things but not in the public record...

2 people one signature...

https://docs.google.com/document/pub?id=19wXsY3B5a17Y81xiznCysbqQ48zlpwb...

Then there are notaries that don't exist....

https://docs.google.com/document/d/1C5s7jr0rjPHl4undKkbxVyr0EZ2i0yyL98_r...

this goes on and on in every county....

This can't be ignored.

The three faces of "Linda" - I agree totally

I was less theoretical here

ForeclosureGate Deal - The Mandatory Cover Up by Michael Collins

But your point is huge. How can lawlessness be tolerated? What is the meaning of fundamental requirements for contracts and contract law if there are no sanctions for those who break the law?

There are two standards - those for the "elect" and those for the rest of us. I have huge objections to any consent decree that lets these people off the hook. One has to wonder why there are not local prosecutions, just one would do it.

Thanks

Michael Collins

thx for the reply, I didn't

thx for the reply, I didn't mean the article is theoretical. I mean the entire foreclosuregate episode is often couched in theoretical terms. They banks and their cronies have been floating the idea that only true debtors are being hurt theoretically by "procedural errors", while innocent mortgagors are unscathed. Realistically ,the entire land record system might need to be purged of bad paper.

But you were right

It is a bit more on the theory side.

I got an email from a colleague of mine, an activist attorney who excellent on just the subject you raised. He talked about remedies in the system that require action by officials. I expect that he will be writing an article for EP soon and outline actions that can flow from what you have observed. Probably out Tuesday or Wednesday next week. I'd characterize it but it's better to get the whole thing explained by someone with considerable expertise.

Thanks for sharing that raw data. When you can just eyeball the record and see it's flawed, it's time to educate the rulers, get them to earn their money.

Michael Collins

reply to indio007

I'd like to discuss further with you. Please contact me re public land record off line at mcfid1 at gmail.com, thank you.

cm

So glad I found this....

Great article. I think some people got tired of me talking/blogging about ForeclosureGate, robosigners and MERS. Or they don't understand what I am talking about. Or maybe they just want to stick their heads in the sand and believe whatever their political party tells them.

Bookmarking this site!

I'm glad you did too!

ForeclosureGate is a prism through which we can view the general decline of any semblance of legal and equitable behavior by the ruling class. Everything must be in service of their goals. When they get caught, the same philosophy applies. They just make a law or cut a deal and it's "Get out of jail free!"

There should be more press on this. The CBS 60 Minutes story was excellent but notable in it's unique perspective. Keep talking and sharing. The internet provides a way to get the word out that can't be stopped, although they will continue to try.

When the law is just for the majority and a tiny minority claims and receives exemptions again and again, the law is seen as their province. That can't last long before we are underwater in the worst way.

Thanks for your comments.

Michael Collins

If you what started the

If you what started the residential real estate problem , check out

Public Law 106–122

106th Congress

An Act

To amend the Federal Reserve Act to broaden the range of discount window loans

which may be used as collateral for Federal reserve notes.

Be it enacted by the Senate and House of Representatives of

the United States of America in Congress assembled, That the

third sentence of the second undesignated paragraph of section

16 of the Federal Reserve Act (12 U.S.C. 412) is amended by

striking ‘‘acceptances acquired under the provisions of section 13

of this Act’’ and inserting ‘‘acceptances acquired under section 10A,

10B, 13, or 13A of this Act’’.

Approved December 6, 1999.

Go check out what 10 B is in the Federal Reserve Act. The FED can use residential mortgages as collateral for NEW Federal Reerve Note Issues. Meaning .. How did you house become the collateral for the dollar in your pocket?

Origins of US monetary system

I'm not sure that my house becoming collateral for the dollar in my pocket is necessarily an evil or mistaken idea.

Isn't that how money got started in the colonies way back in the 1700s?

The problem isn't the idea of monetarism. The devil is in the Fed details, no?

I can't get a loan to refinance my house, but the bank can?

If the bailouts had just been larger

Then the banks could have done it. We're last in line.

The banks were happy to proactively do refis in the DC suburbs, you'll be interested to know. They picked out homes that met two criteria: a) the home had equity and b) the home had a MERS contract. This happened before Albanez came down and while ForeclosureGate was getting heavy press. The deals were very good. A clean swap with a 1/4 point off interest, no fees at all. They were thinking about the future in one of the only stable real estate markets. Enough foreclosures while the market was still good and they'd make some decent money on the deal. Very strange but who can figure these guys out.

Michael Collins

Thank you

I had noted the relatively stable economic condition of D.C. throughout all this 'recession', but I never knew about the ugly details regarding the mortgage aspect and bailouts. So, yes, I am interested - and I thank you.

As you aptly express it, the rule today is that

"We're last in line" -- we, the working people of America.

public land records

please contact me re public land record off line at mcfid1 at gmail.com, thank you.

Additional Perspective

READ Treasure Islands by Nicholas Shaxon: Tax Havens and the Men Who Stole the World. The pieces fit in nicely with this whole story.

I knew a very rich man (almost a billionaire) who loaned money on houses - not seconds, only first mortgages. He taught me how he did it. He told his prospective borrower that he "collected houses". His rates were kneecap rates for people in trouble. His favorite phrase: I believe in the golden rule. Those that own the gold makes the rules. Needless to say, I learned quite a bit by watching. He almost always ended up with the house.

David Cay Johnston

The classic in analysis of Congress and the federal income tax law:

"Perfectly Legal: The Covert Campaign to Rig Our Tax System to Benefit the Super Rich -- And Cheat Everybody Else" by David Cay Johnston, published (2003) by Penguin.

Michigan Court Rules Against MERS

http://www.wxyz.com/dpp/news/region/detroit/michigan-court-of-appeals-ru...

THANKS!!!

From your link:

The lawyers are also saying that under this ruling, MERS has no standing at all in Michigan, and that any foreclosures that were carried out by MERS or in the processes of being carried out by MERS are null and void.

Michael Collins