The Canadian Press

reports CPP Investments earned 7.8% for fiscal 2026, net assets total $793.3 billion:

The Canada Pension Plan Investment Board has reported a return of 7.8 per cent for its 2026 fiscal year.

The

results helped increase its net assets to $793.3 billion at March 31,

up from $714.4 billion at the end of its 2025 fiscal year.

It

says the increase for the year included $56.9 billion in net income and

$22.0 billion in net transfers from the Canada Pension Plan.CPP

Investments chief executive John Graham says the results reflected the

strength of its diversified portfolio and the reach of its global

investment platform.

The returns were helped

by its holdings in public equities, while its real assets, particularly

energy and infrastructure assets, also contributed to the gains.

The

results for the year by CPP Investments fell short of its benchmark

portfolio which returned 13.2 per cent for the same period, as it was

boosted by relatively heavier exposure to the large technology companies

that outpaced the broader market for the year.

Layan Odeh of Bloomberg also reports that stocks, data centers drive the Canada Pension Fund to 7.8% return:

Canada Pension Plan Investment Board notched a 7.8% return in its most

recent fiscal year, as gains on stocks and data center investments

helped offset the impact of a softening US dollar and a weak year in

private equity.

The

returns, which pushed net assets to C$793.3 billion ($576.2 billion),

came in a period “marked by geopolitical uncertainty, market volatility

and currency movements,” Chief Executive Officer John Graham said in a

statement.

Public equities gained 17.5% and were a key driver of results,

particularly in the US, led by information technology and communication

services. But private equity rose just 2.9%, partly because of the poor

performance of some holdings in the software business, which investors

see as vulnerable to AI-related disruption.

Real assets delivered a 12.2% return, boosted by data center investments

and industrial real estate in the Asia-Pacific region, the fund said.

CPPIB’s

results were hurt by the decline of the greenback against the Canadian

dollar and by losses on government bonds, as expectations for central

bank rate cuts shifted. The weakening of the US dollar contributed to a

foreign currency loss of C$12.4 billion.

During

the fiscal year ended March 31, Canada’s largest pension plan shifted

some real estate, infrastructure and energy investments that were

previously reported as equities to the real assets group, “to better

reflect the underlying characteristics of these assets,” according to

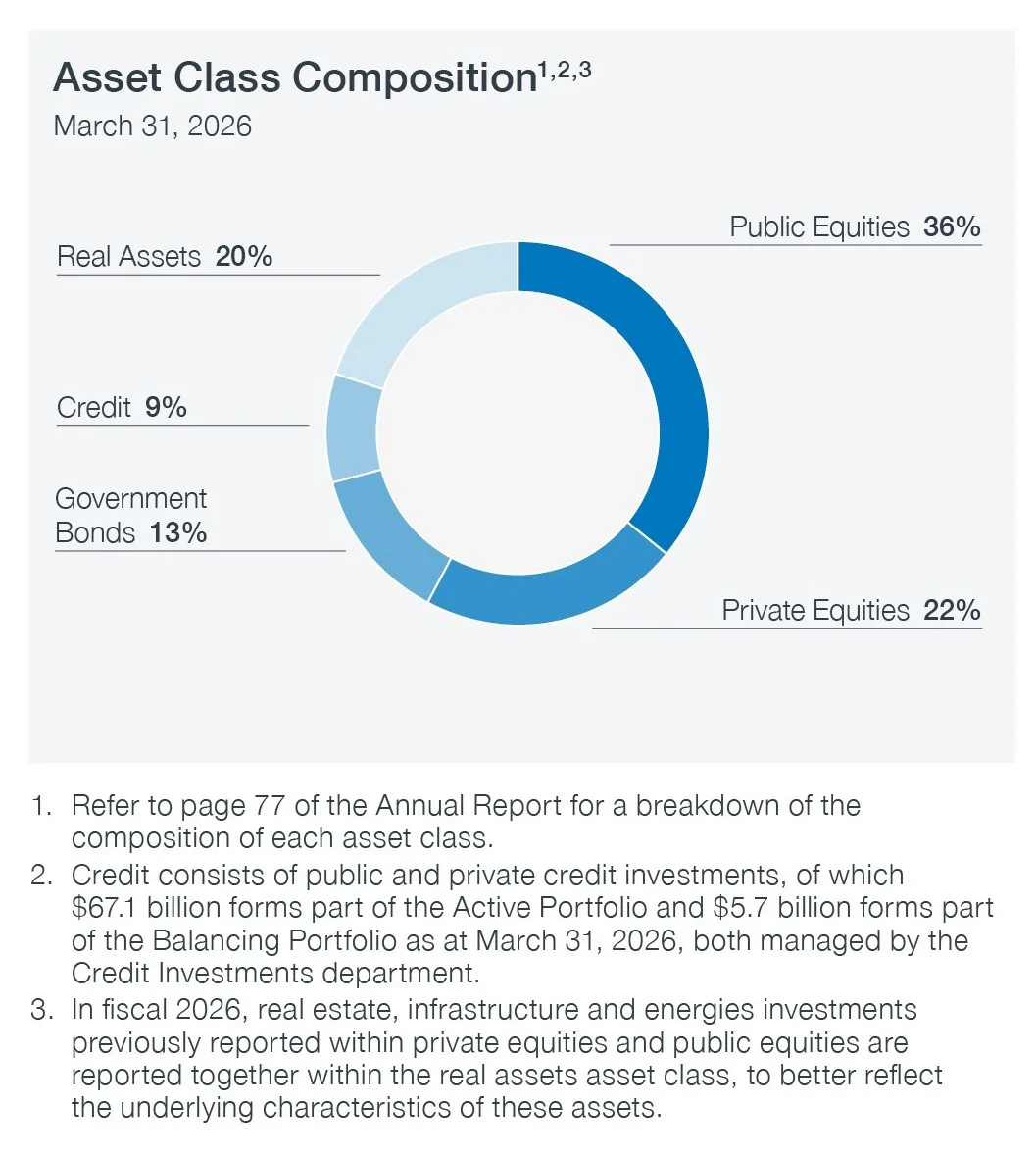

the annual report. Private equity now makes up 22% of the total fund,

down from 25% a year earlier.

The

pension plan made billions in new data center-related investments or

commitments, including a C$225 million loan for a hyperscale expansion

of a data center in Cambridge, Ontario.

CPPIB

also committed $1.5 billion to an account managed by Blackstone Inc.

that invests globally across diversified credit, including fund

commitments, spanning private corporate credit, asset-based and real

estate credit, structured products and liquid credit.

Layan Odeh also reports that CPP investments' boss warns about AI-fueled valuations as stocks keep rising:

Canada Pension Plan Investment Board’s

top executive said the firm is getting increasingly uncomfortable with

rich valuations in a stock market that’s dominated by technology and

artificial intelligence companies.

“We have a market that is rewarding concentration. We have a market that is being driven by a handful of companies,” said John Graham, chief executive officer of the C$793 billion ($576 billion) fund.

The six largest technology companies in the S&P 500 now represent more than a third of that benchmark, led by Nvidia Corp.,

which is worth $5.3 trillion. They’ve been on a tear lately, helping

lift the US stock gauge 14% since the end of March — and it has nearly

doubled since the beginning of 2023.

The

sustained rally has left far fewer opportunities, Graham said in an

interview after the pension fund revealed its results for the fiscal

year that ended in March. “I wouldn’t say we’re a deep-value investor,

but we certainly have a value bias,” he said. “We certainly like to

invest in cash flows, and we struggle with some of the valuations in the

market today.”

Canada’s

largest pension manager posted a 7.8% return in the 2025-26 fiscal

year, driven by double-digit gains in public equities. Like some other

members of the so-called Maple Eight group of Canadian pension funds,

CPPIB’s stock portfolio is outpacing private equity returns by a wide

margin.

But

parts of CPPIB’s equities team had a difficult year. The fund’s active

equities strategies incurred a C$3.5 billion net loss, bringing the

five-year loss to C$6 billion. Regulatory changes in China weighed on

the overall performance over the five-year period, prompting the fund to

to reduce its exposure in that country.

The firm’s active equities team, which invests in public and soon-to-be-public companies, shrank to 120 employees from 139 people two years ago.

“We

think it’s an important part of the broader portfolio to have a

fundamental equities capability,” Graham said. “The big question is, how

big do you think it should be?”

The

rise of passive investing has reshaped markets in recent years, with

investors directing more capital toward lower-cost strategies.

Some Canadian pension funds are now revisiting how much stock-picking they do. British Columbia Investment Management Corp.

is closing two active equities strategies that oversee about C$4.3

billion, saying they’re no longer useful in a shrinking global pool of

publicly listed firms. Last year, Ontario Teachers’ Pension Plan said it was altering its approach by prioritizing passive investing over stock picking.

Canada’s

largest pension plan shifted some real estate, infrastructure and

energy investments that were previously reported as equities to the real

assets group, “to better reflect the underlying characteristics of

these assets,” according to the annual report. Private equity makes up

22% of the total fund, down from 25% a year earlier.

CPPIB

will continue to emphasize diversification across hedge funds, private

equity, infrastructure, stocks, credit and real estate, Graham said. The

credit team was “quite opportunistic” during the year, he said, helping

credit investments gain 3.8%. The fund’s overall returns were hurt by

the weakening of the US dollar, which represented the majority of its

currency exposure, according to the annual report.

On

investing in Canada, Graham said CPPIB has staffed each investment

department for a while with teams dedicated to the domestic market, to

“have Canada as part of their remit and their mandate,” the CEO said.

CPPIB also disclosed that Graham was paid C$7 million in the fiscal year, up from C$6.4 million a year earlier.

Earlier today, CPP Investments announced net assets total $793.3 billion at 2026 fiscal year end:

Highlights:

- Net income of $56.9 billion

- Net annual return of 7.8% in fiscal 2026

- 10-year annualized net return of 8.8%

TORONTO, ON (May 21, 2026): Canada Pension Plan Investment Board (CPP Investments)

ended its fiscal year on March 31, 2026, with net assets of $793.3

billion, compared to $714.4 billion at the end of fiscal 2025. The $78.9

billion increase in net assets consisted of $56.9 billion in net income

and $22.0 billion in net transfers from the Canada Pension Plan (CPP).

The Fund, composed of the base CPP and additional CPP accounts1,

generated a 10-year annualized net return of 8.8%. For the fiscal year,

the Fund’s net return was 7.8%. As the CPP is designed to serve

multiple generations of beneficiaries, evaluating the performance of CPP

Investments over extended periods is more suitable than in single

years.

“Fiscal 2026 was a strong year for CPP Investments. In a period

marked by geopolitical uncertainty, market volatility and currency

movements, we delivered a 7.8% net return and the Fund grew to more than

$790 billion,” said John Graham, President & CEO. “These results

reflect the strength of our diversified portfolio and the reach of our

global investment platform. By staying disciplined and investing for the

long term, we continued to build value for generations of CPP

contributors and beneficiaries.”

A diverse range of asset classes contributed to the strength of the

fiscal year’s performance at CPP Investments. Public equities were a key

driver of results, particularly in the U.S., led by information

technology and communication services in the first half of the year.

Real assets, particularly energy and infrastructure assets, also

contributed meaningfully, alongside steady gains in credit. These gains

were partially offset by foreign exchange movements, driven by the

depreciation of the U.S. dollar against major currencies including the

Canadian dollar, and by losses in government bonds as market

expectations for major central bank interest policies shifted. Conflict

in the Middle East at the end of the fiscal year contributed to a broad

selloff in global equity markets, against a backdrop of ongoing

geopolitical uncertainty and global inflation.

On a 2025 calendar-year basis, the Fund delivered a 7.7% net return,

primarily driven by public equities, with gains across all asset

classes.

“What matters most for a pension fund serving generations of

Canadians is long-term performance, and over the past decade our

investment programs have contributed positively to the Fund’s returns,”

said Graham. “Through disciplined decision-making and global

diversification, we have earned $549 billion in cumulative net income

since we started investing more than 25 years ago, helping us protect

and grow the Fund while building resilience through changing market

conditions.”

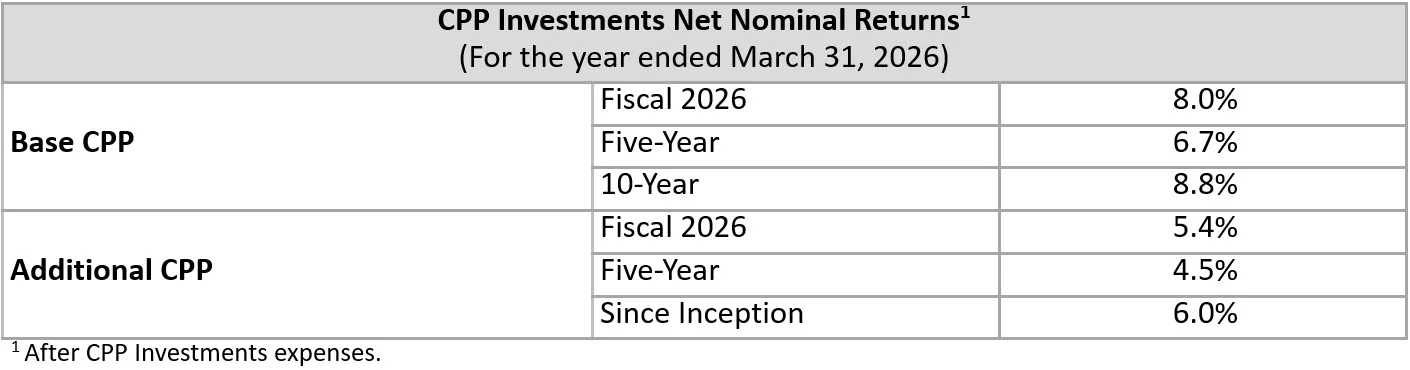

Performance of the Base and Additional CPP Accounts

The base CPP account ended the fiscal year on March 31, 2026, with

net assets of $712.9 billion, compared to $655.8 billion at the end of

fiscal 2025. The $57.1 billion increase in net assets consisted of $53.2

billion in net income and $3.9 billion in net transfers from the base

CPP. The base CPP account’s net return for the fiscal year was 8.0% and

the 10-year annualized net return was 8.8%.

The additional CPP account ended the fiscal year on March 31, 2026,

with net assets of $80.4 billion, compared to $58.6 billion at the end

of fiscal 2025. The $21.8 billion increase in net assets consisted of

$3.7 billion in net income and $18.1 billion in net transfers from the

additional CPP. The additional CPP account’s net return for the fiscal

year was 5.4% and the annualized net return since inception was 6.0%.

The additional CPP was designed with a different legislative funding

profile and contribution rate compared to the base CPP. Given the

differences in its design, the additional CPP has had a different market

risk target and investment profile since its inception in 2019. As a

result of these differences, we expect the performance of the additional

CPP to generally differ from that of the base CPP.

Furthermore, due to the differences in its net contribution profile,

the additional CPP account’s assets are also expected to grow at a much

faster rate than those in the base CPP account.

Long-Term Financial Sustainability

Every three years, the Office of the Chief Actuary of Canada (OCA),

an independent federal body that provides checks and balances on the

future costs of the CPP, evaluates the financial sustainability of the

CPP over a long period. In the most recent triennial review published in

December 2025, the Chief Actuary reaffirmed that, as at December 31,

2024, both the base and additional CPP continue to be sustainable over

the long term at the legislated contribution rates.

The Chief Actuary’s projections are based on the assumption that,

over the 75-year projection period following December 31, 2024, the base

CPP account will earn an average annual rate of return of 4.05% above

the rate of Canadian consumer price inflation. The corresponding

assumption is that the additional CPP account will earn an average

annual real rate of return2 of 3.53%.

CPP Investments continues to build a portfolio designed to achieve a

maximum rate of return without undue risk of loss, while considering the

factors that may affect the funding of the CPP and its ability to meet

its financial obligations on any given day. The CPP is designed to serve

contributors and beneficiaries today and across future generations.

Accordingly, long-term results are a more appropriate measure of CPP

Investments’ performance and impact on plan sustainability.

“Canadians can continue to rely on the CPP as a strong foundation for

their retirement income,” said Graham. “The Chief Actuary’s latest

report shows our approach is on track, with investment income coming in

approximately $80 billion higher than expected over the three-year

period since December 31, 2021. This performance has strengthened the

CPP’s funding outlook and helped create the conditions for governments

to agree to a reduction in the contribution rate, while maintaining

benefit levels and supporting a strong, sustainable plan for current

contributors and future retirees alike. As a pension fund investor whose

role is to prudently grow the Fund so Canadians can rely on the CPP for

generations, it is especially meaningful that we have been able to

contribute to this outcome.”

The OCA report provides forward-looking return assumptions and

projected financial states for the base and additional CPP. The table

below presents CPP Investments’ historical net real returns, which

reflect realized performance over past periods.

Relative Performance

CPP Investments was created to invest and help grow the Fund, with

the legislative mandate to maximize returns without undue risk of loss.

The organization’s overall investment strategy is therefore focused on

delivering a level of absolute performance that will help ensure the CPP

meets all current and future obligations to contributors and

beneficiaries.

CPP Investments also tracks investment performance relative to

benchmarks to report on the value active management adds after all costs

over different time horizons. It does so against the benchmark

portfolios, which provide target allocations for our active and

balancing investment strategies. We construct the benchmark portfolios

by aggregating the sector- and geography-relevant public market index

benchmarks to assess relative performance of each individual investment

strategy. CPP Investments’ performance relative to the benchmark

portfolios is measured in percentage terms.

On a relative basis, the Fund’s 10-year return outperformed the

aggregated benchmark portfolios, generating 0.7% per annum of value

added, net of costs. The benchmark portfolios’ fiscal 2026 return of

13.2% exceeded the Fund’s net return of 7.8% by 5.4%.

Significant concentration in public equities, with relatively heavier

exposure to large-cap technology and communication services companies

largely tied to artificial intelligence, were the principal drivers of

benchmark portfolio performance in fiscal 2026. These companies

delivered outsized returns compared to the wider universe of investable

assets. By design, however, the Fund’s more diversified asset mix across

public and private markets, sectors and geographies that helps reduce

the impact of sharp equity market declines, limited participation in

strong equity market rallies, such as those reflected in the benchmark

portfolios’ public market indexes this past fiscal year. CPP

Investments’ diversified portfolio is intentionally constructed to be

less concentrated than public market indexes, with the purpose of

enhancing the Fund’s resilience as it continues to grow over time.

For information on which of our decisions we believe are adding the

most value, please refer to page 42 of the CPP Investments Fiscal 2026

Annual Report.

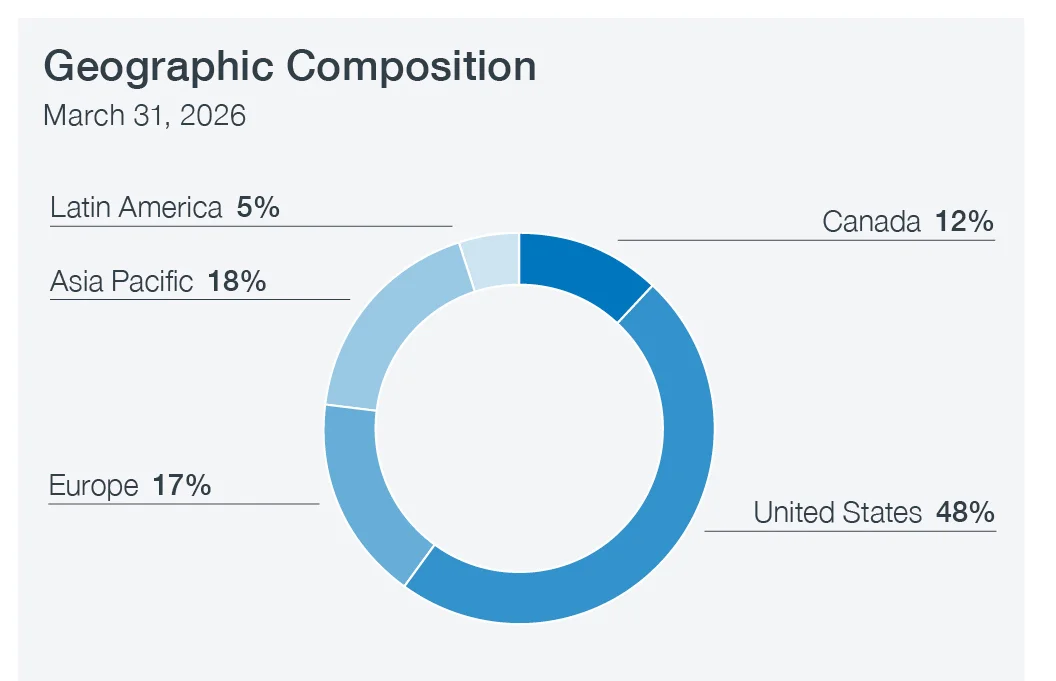

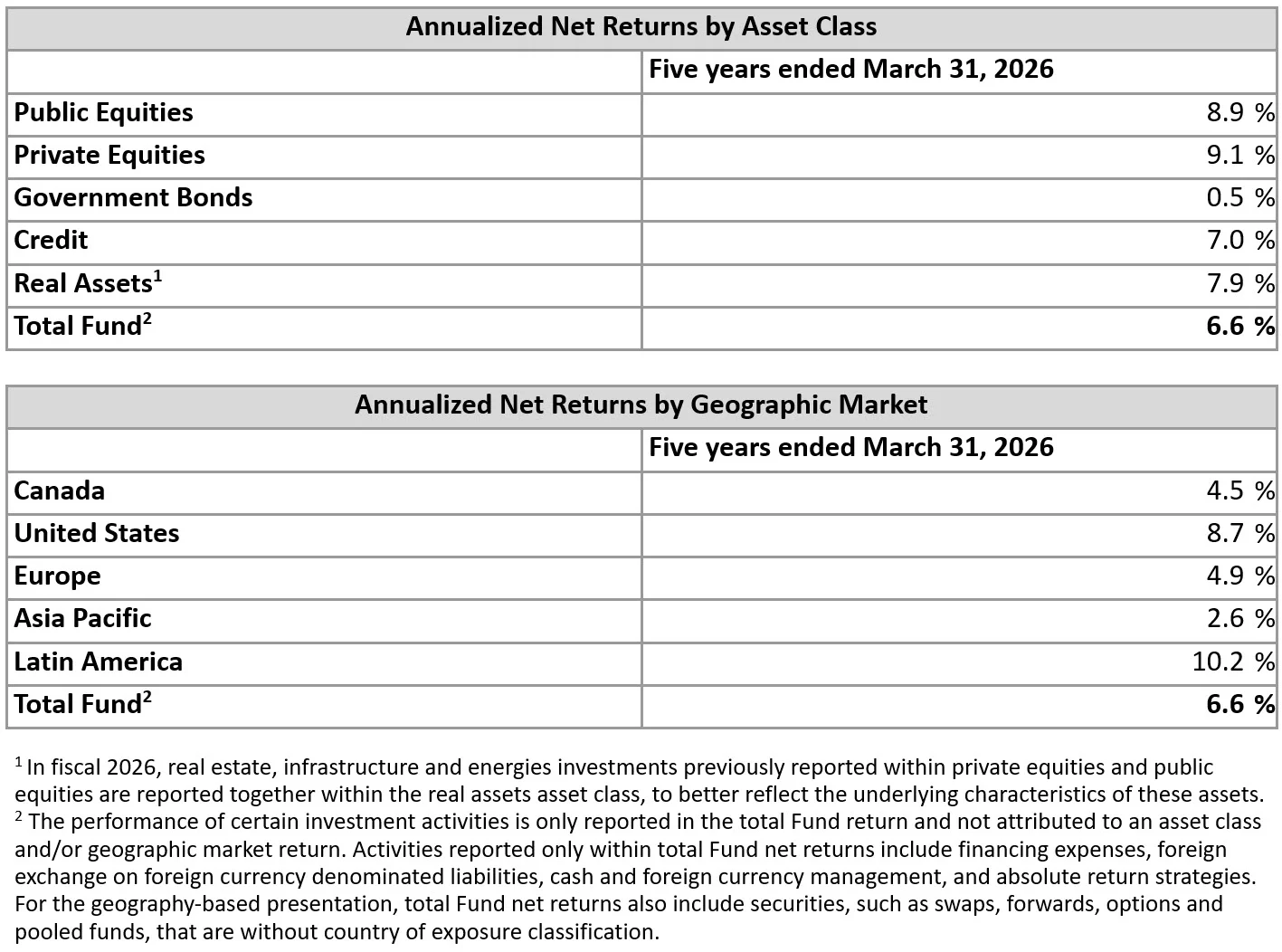

Asset Class and Geography Composition

CPP Investments’ portfolio, inclusive of both the base CPP and

additional CPP investment portfolios, is diversified across asset

classes and geographic markets.

Performance by Asset Class and Geographic Markets

Five-year Fund returns by asset class and geographic markets are

reported in the tables below. A more detailed breakdown of performance

by investment department is included on page 53 of the Fiscal 2026

Annual Report.

Managing CPP Investments Costs

Discipline in cost management is a main tenet of how we operate an

internationally competitive enterprise that exists to create enduring

value for multiple generations of CPP contributors and beneficiaries.

To generate $56.9 billion of net income, CPP Investments directly and

indirectly incurred $1,757 million of operating expenses, $1,976

million in investment management fees and $2,758 million in performance

fees paid to external managers, as well as $753 million of

transaction-related costs.

Operating expenses were broadly flat in fiscal 2026, increasing by $1

million due to inflationary increases in personnel costs offset by

lower general and administrative expenses. The net result is an

operating expense ratio of 23.1 basis points (bps), below both last

year’s 26.1 bps and our five-year average of 26.5 bps. We have also

improved our operational efficiency, measured by net investments managed

per employee, from $269 million in fiscal 2022 to $364 million in

fiscal 2026, reflecting a 8% growth rate per year.

Management fees incurred increased by $216 million, driven by growth

in externally managed assets. Performance fees increased by $535 million

reflecting the positive performance delivered by our external managers.

Transaction-related costs, which increased by $23 million, vary from

year to year according to the activity level, size and complexity of our

investing activities. In fiscal 2026, we announced more than 50

transactions of $250 million or more, including approximately 20

transactions valued at more than $1 billion. Other categories affecting

our total cost profile include taxes and expenses associated with

various forms of leverage.

Refer to page 29 of the Fiscal 2026 Annual Report for more

information on how we manage our costs and to page 50 for a complete

overview of CPP Investments combined expenses, including year-over-year

comparisons.

Operational Highlights for the Year

Corporate developments

- Once again ranked one of the world’s top-performing public pension

funds by Global SWF when measuring annualized returns between fiscal

years 2016 and 2025 (Global SWF Data Platform, May 2026).

- The Federal government announced, with the support of provincial and

territorial governments, a proposed reduction in base CPP contribution

rates (from 9.9% to 9.5%). This follows the most recent actuarial review

released in December 2025, which confirmed the CPP remains financially

sustainable and in a stronger financial position than in the previous

assessment, supported in part by the growth of the CPP Fund and

investment income over time. This underscores the long-term strength of

the CPP and its ability to meet its obligations to current and future

generations.

- Entered into a Memorandum of Understanding under the

Canadian-Australian Pension Funds Investment Initiative (CAP Invest

Initiative), which defines a voluntary commitment among leading pension

investors to facilitate dialogue on investment environments and policy

barriers to generate solutions that unlock greater opportunities for

value creation.

- Ranked first among Canadian pension funds and second among 75

pension funds across 15 countries in the 2025 Global Pension

Transparency Benchmark developed by Top1000funds.com and CEM

Benchmarking, its fifth and final edition. The Global Pension

Transparency Benchmark focuses on the transparency and quality of public

disclosures relating to the completeness, clarity, information value

and comparability of disclosures.

Board appointments

- Welcomed the following appointments to our Board of Directors:

- Gillian Denham, effective September 25, 2025. Ms. Denham has

extensive experience on public company boards and is the former Head of

the Retail Bank at CIBC.

- Stephanie Coyles, effective October 10, 2025. Ms. Coyles is an

experienced director and is the former Chief Strategic Officer at

LoyaltyOne, Inc.

- Elio Luongo, effective April 29, 2026. Mr. Luongo has more than

three decades of experience in financial services and advisory and

served as Chief Executive Officer and Senior Partner of KPMG in Canada.

- Barry Perry and Sylvia Chrominska were reappointed as Directors of

the Board for three-year terms, effective September 25, 2025, and

December 3, 2025, respectively.

Leadership announcements

- David Colla was appointed Senior Managing Director & Global Head

of Credit Investments, effective April 1, 2026, and joined the senior

management team. Mr. Colla joined CPP Investments in 2010 and most

recently led the Capital Solutions group. He succeeds Andrew Edgell who

will continue with the organization as a Senior Advisor.

Public accountability

- Hosted our first two in-person public meetings for 2026 in Calgary

and Edmonton, Alberta, providing an accessible forum to ask questions of

our senior leaders. Additional meetings, including a national virtual

meeting, will be held in the fall of 2026 to reflect our continued

accountability to the CPP’s more than 22 million CPP contributors and

beneficiaries.

Transaction Highlights for the Year

Active Equities

- Invested C$73 million for a 0.8% stake in Definity Financial Corp, a

property and casualty insurance services provider in Canada.

- Invested C$411 million for a 0.6% stake in Medline Inc., a

medical-surgical products and supply chain solutions provider in the

U.S.

- Invested C$322 million for a 0.1% stake in Hitachi, Ltd., which

provides digital systems and services, green energy and mobility, and

connective industry solutions in Japan and internationally.

- Invested C$320 million for a 1.5% stake in Informa PLC, an

international events, digital services and academic research group based

in the U.K.

- Invested an additional C$1.1 billion in Ares Management, a global

alternative investment manager operating in the credit, private equity

and real estate markets, resulting in a total ownership stake of 2.0%.

- Invested an additional C$594 million in DSV A/S, a Danish transport

and logistics company offering global transport services by road, air,

sea and train, resulting in a total ownership stake of 1.9%.

Capital Markets & Factor Investing

- Completed 34 co-investments alongside external fund managers through

fiscal 2026, committing approximately C$3,640 million to macro-themed

strategies in addition to equity trades in a variety of sectors,

including communication services, consumer discretionary, and

financials.

Credit Investments

- Committed US$250 million to Lumina Strategic Solutions Fund III and

US$200 million to a discretionary Separately Managed Account. Lumina

invests at scale in the Latin American special situations market.

- Committed US$1.5 billion to a separately managed account managed by

Blackstone, which is designed to invest globally across diversified

credit investments, including fund commitments, spanning private

corporate credit, asset-based and real estate credit, structured

products and liquid credit.

- Invested US$200 million in a preferred equity facility to support

ProAmpac’s acquisition of TC Transcontinental Packaging. Headquartered

in the U.S., ProAmpac is a leading global provider of flexible packaging

serving a diverse range of end markets.

- Participated in a US$500 million senior term loan supporting Sixth

Street’s acquisition of Global Lending Services, an auto financing

solutions provider in the U.S.

- Invested US$75 million in the first loss tranche of a significant risk transfer issued by a scaled non-bank lender in the U.S.

- Invested US$200 million into a first lien term loan for Global

Cellulose Fibers, a leading global producer of bleached softwood fluff

pulp, based in the U.S.

- Committed US$205 million as part of a term loan credit facility to

Emergent Cold Latin America, the largest cold storage operator in Latin

America, operating 112 facilities across 11 countries.

- Invested £190 million in the primary commercial mortgage-backed

securities debt issuance of Caister Finance, secured by a portfolio of

U.K. holiday parks owned by Haven.

- Invested US$100 million into the preferred equity issuance of CI

Financial, a global wealth management and asset management advisory firm

headquartered in Canada.

- Invested C$225 million in a loan to construct a hyperscale expansion

to a data centre in Cambridge, Ontario, Canada, funding 50% of the

total construction cost, alongside Deutsche Bank.

- Invested A$300 million (C$264 million) in an Australian commercial

real estate debt strategy managed by Nuveen, a global investment

manager. The strategy will focus on institutional senior and junior

loans secured by prime real estate across major cities in Australia.

- Invested US$300 million in the partial royalty monetization of

Leqvio, a cardiovascular drug for the treatment of hyperlipidemia.

Private Equity

- Invested US$50 million in 9fin, alongside Highland Europe.

Headquartered in the U.K., 9fin is an AI-enabled credit intelligence and

workflow platform serving global debt capital markets.

- Committed JPY 11.75 billion (approximately C$100 million) to Bain

Capital Japan Middle Market Fund II, which will target mid-sized

companies in diversified sectors across Japan.

- Committed US$63 million to Dragoneer Select Opportunities Fund,

which will focus on growth-oriented companies in the technology sector

globally.

- Committed a combined US$145 million to Sands Capital’s Global

Innovations Fund III, which invests in category-defining technology

companies with an emphasis on long-term secular themes.

- Invested US$175 million in Aadhar Housing Finance, the largest

affordable housing finance company in India, alongside Blackstone Asia.

- Invested US$27 million in Federal Bank, a private bank in India, alongside Blackstone Asia.

- Committed US$300 million to Francisco Partners VIII, which will focus on technology investments in North America and Europe.

- Committed US$50 million to NinjaOne through a single-asset

continuation vehicle with Summit Partners. Based in the U.S., NinjaOne

is a leading provider of cloud-based software solutions to outsourced IT

managed service providers.

- Committed US$200 million to Thrive Capital X across its Early,

Growth and Opportunity funds and invested US$18 million in OpenAI

alongside Thrive Capital. Thrive Capital is a New York-based,

multi-stage venture capital firm.

- Committed US$135 million to Consumer Cellular through a single-asset

continuation vehicle with GTCR. Consumer Cellular is a U.S.-based cell

phone provider that focuses on the 55+ demographic.

- Committed US$155 million across a16z’s Late-Stage Venture Fund V, AI

Applications Fund X and AI Infrastructure Fund X. Based in the U.S.,

a16z is a multi-stage venture capital and growth firm that invests in

disruptive companies and technologies.

- Committed US$100 million to Accel Leaders 5, which will invest in

later-stage rounds of technology companies across the U.S., Europe and

India.

- Invested US$100 million in Advent LAPEF VIII, a private equity fund

that will pursue control-oriented buyouts and select minority positions

across business and financial services, healthcare, industrials,

consumer and technology sectors in Latin America, with a primary focus

on Brazil and Mexico.

- Committed US$400 million to Bain Capital Asia Fund VI, which will

focus on control buyout investments across Japan, India, China,

Australia and Korea.

- Committed to invest an additional C$750 million through our

established Canadian mid-market private equity program managed by

Northleaf Capital Partners, supporting the growth and scaling of

domestic private companies.

- Invested approximately US$600 million for a co-control interest in

Boats Group, a global provider of online marketplaces for boats and

yachts, alongside General Atlantic and existing investor Permira.

- Invested approximately C$60 million in Wealthsimple through a

primary and secondary offering at a post-money valuation of C$10

billion. Wealthsimple is one of Canada’s fastest growing money

management platforms.

- Acquired a US$135 million limited partner interest in TA Associates

Fund XII via a secondary transaction. TA Associates is a global growth

private equity firm investing in technology, health care, financial

services, consumer and business services.

- Invested approximately C$1 billion in OneDigital, a U.S.-based

insurance brokerage, financial services and workforce consulting firm.

We invested together with funds managed by Stone Point Capital for a

majority position in the company. The transaction will support the

company’s continued growth through a combination of organic expansion

and strategic acquisitions.

- Committed US$100 million to Glenwood Korea Private Equity Fund III,

managed by Glenwood Private Equity, which will target mid-market control

carve-out opportunities in South Korea.

- Invested approximately €275 million in IFS, acquiring shares from

EQT alongside other investors. Headquartered in Sweden, IFS is a leading

global provider of cloud enterprise software and industrial AI

applications.

- Committed A$150 million (C$135 million) to Pacific Equity Partners

PE Fund VII, which focuses on upper mid-market buyout opportunities in

Australia and New Zealand.

- Sold our remaining approximate 36% stake in Informatica, an

AI-powered enterprise cloud data management company, as part of

Salesforce’s acquisition, generating net proceeds of US$2.7 billion. Our

original investment was made in 2015.

Real Assets

- Committed US$400 million to Greystar Global Strategic Partners II

(GGSP II) managed by Greystar, a global leader in property management,

investment management, and development. GGSP II will provide equity to

Greystar’s global investment offerings across a diversified portfolio of

living sector real estate strategies.

- Committed approximately US$175 million to a real estate portfolio of senior living communities across the U.S.

- Agreed to invest approximately US$1.6 billion for a 60% controlling

interest in atNorth, a leading Nordic high-density colocation and

built-to-suit data centre provider, in partnership with Equinix who will

own an approximate 40% stake.

- Agreed to acquire a 50% ownership interest in Inkia Energy, a

private power generation company in Peru, at a total enterprise value of

US$3.4 billion, alongside I Squared Capital.

- Committed to initially invest up to JPY 25.4 billion (C$222 million)

to a Japan hospitality strategy managed by Singapore-based real estate

investment manager SC Capital Partners Group.

- Formed a joint venture with Dream Industrial REIT and Dream Asset

Management Corporation to acquire last-mile industrial properties in

major markets across Canada. We have allocated C$1.0 billion of equity

capital (90%) to the joint venture. The partners have agreed to acquire a

portfolio of 12 Canadian industrial assets totaling 3.6 million square

feet across Ontario, Quebec and Alberta, for a purchase price of C$805

million.

- Committed a combined US$310 million to U.S.-based Vantage Data

Centers (Vantage), which provides data centre campuses to cloud

providers and enterprises, as well as an additional US$200 million

commitment across Vantage and Yondr, a global developer, owner and

operator of hyperscale data centres.

- Invested US$1.0 billion for a strategic minority position in

AlphaGen, one of the largest independent power portfolios in the U.S.,

alongside ArcLight Capital Partners.

- Entered into a definitive agreement to acquire an approximate 13%

indirect equity interest in Sempra Infrastructure Partners, a leading

North American energy infrastructure company, for approximately US$3.0

billion, alongside affiliates of KKR.

- Invested €234 million to support Nido Living, a European student

housing operator, in its acquisition of Livensa Living, a student

housing platform operating across Iberia. The acquisition positions the

enlarged Nido group as one of the leading student housing operators in

Europe, with approximately 13,000 beds. We acquired Nido Living in 2024.

- Committed JPY 192.5 billion (C$1.8 billion) in Japan DC Partners I

LP, a data centre development partnership managed by Ares Management

following its acquisition of GCP. The partnership will support the

development of three large-scale campuses in Greater Tokyo to meet

growing demand for scalable computing and AI solutions.

- Completed the sale of our 49.87% stake in Transportadora de Gas del

Peru S.A., which operates Peru’s main natural gas and natural gas

liquids pipelines under a long-term concession, to EIG. Net proceeds

from the sale were approximately US$820 million. Our original investment

was made in 2013.

- Entered into a definitive agreement to sell our 49% stake in Island

Star Mall Developers Private Limited, a real estate investment program

in India, to joint venture partner The Phoenix Mills Limited and

affiliates. Net proceeds will be approximately INR 54.5 billion (C$871

million) before closing adjustments. The joint venture was established

in 2017.

- Sold our 50% interest in a portfolio of seven high-quality office

properties in Western Canada to Oxford Properties for C$730 million. Our

original investments were made in 2005 and 2016.

Transaction Highlights Following the Year-End

- Committed US$104 million indirectly in the acquisition of Zentiva, a

leading European generics and over-the-counter pharmaceuticals company,

alongside GTCR.

- Invested US$100 million for a minority stake in Sealed Air, a

U.S.-based leading global provider of food and protective packaging

solutions, alongside CD&R.

- Invested US$100 million in Accuity Healthcare, a leading provider of

pre-bill, revenue integrity services to hospital and healthcare systems

in the U.S., through a single-asset continuation vehicle managed by

Frazier Healthcare Partners.

- Invested US$150 million in the preferred equity of Cerity Partners, a national registered investment advisor in the U.S.

- Committed US$1 billion in financing to Blackstone Private Credit

Fund, which is a U.S.-based investment fund focused on providing senior

secured loans to large, performing companies.

- Entered into a two-year forward-flow commitment with Global Lending

Services, a U.S. auto financing solutions provider, to acquire up to

US$1 billion of auto loans.

- Committed US$50 million to Accel Core, which will invest in Accel’s

core technology sectors, expected to include artificial intelligence,

security, developer tools, fintech, defense and software. Accel is a

leading global venture capital firm.

- Sold Greenway Plaza, a mixed-use office property in Texas. No net

proceeds were generated from the asset sale. Our original investment was

made in 2017.

- Sold a diversified portfolio of 33 limited partnership fund

interests in North American and European buyout funds to Blackstone

Strategic Partners and Ardian, for net proceeds of approximately C$4.0

billion. The portfolio of interests represents various investments made

in funds over the course of approximately 20 years.

To read our fiscal 2026 annual report, please click here.

About CPP Investments

Canada Pension Plan Investment Board (CPP Investments™) is a

professional investment management organization that manages the Canada

Pension Plan Fund in the best interests of the more than 22 million

contributors and beneficiaries. In order to build diversified portfolios

of assets, we make investments around the world in public equities,

private equities, real estate, infrastructure and fixed income.

Headquartered in Toronto, with offices in Hong Kong, London, Mumbai, New

York City, São Paulo and Sydney, CPP Investments is governed and

managed independently of the Canada Pension Plan and at arm’s length

from governments. At March 31, 2026, the Fund totalled $793.3 billion.

For more information, please visit www.cppinvestments.com or follow us on LinkedIn, Instagram or on X @CPPInvestments.

You can download and read CPP Investments' FY2026 Annual Report here.

I had a chance to speak with CPP Investments' CEO John Graham earlier today, but before I get to this discussion, some of my observations and take the time to read the president's message below:

In a year of volatility and disruption, the CPP Fund (the Fund)

did exactly what it was designed to do: remain resilient, grow steadily

and help protect the retirement security of millions of Canadians.

The Canada Pension Plan (CPP) is one of Canada’s most important

public programs and a cornerstone of retirement income for Canadians.

Millions rely on it in retirement to provide a dependable monthly

benefit that lasts for life and adjusts with inflation.

CPP Investments plays a distinct role in that system: we invest

the Fund to help ensure the CPP is there for generations of Canadians.

To keep the Plan financially sustainable, we must invest prudently

through whatever the world throws our way.

The CPP remains strong and financially sustainable for generations

I’m pleased to report that the CPP Fund delivered strong performance

in fiscal 2026 and the long-term financial sustainability of the Fund is

secure.

In its latest report released in December 2025, the Office of the

Chief Actuary of Canada reconfirmed that the CPP is financially

sustainable for at least the next 75 years. The report also found that

the funding outlook of the CPP – its expected ability to pay benefits

over the long term – has strengthened since the previous assessment.

Investment income also exceeded projections; between 2022 and 2024, it

was about $80 billion higher than anticipated in the prior report. That

independent, forward-looking assessment of the CPP’s ability to meet its

obligations through changing demographics and economic conditions

speaks to the Plan’s underlying health.

In fact, it is in part because of this underlying health that the

federal government, with the support of provincial governments,

announced in April 2026 a reduction in the contribution rate of the base

CPP from 9.9% to 9.5%. This reduction will be implemented while

maintaining benefit levels, supporting a strong, sustainable plan for

current contributors and future retirees alike. As a pension fund

investor whose role is to prudently grow the Fund so Canadians can rely

on the CPP for generations, it is especially meaningful that we have

been able to contribute to this outcome.

Strong long-term returns

The world is adjusting to a more fragmented global order, where trade

and investment rules can shift quickly and uncertainty remains

elevated. Market gains have been, at times, concentrated in a handful of

large U.S. technology stocks, conflicts in Europe and the Middle East

disrupted energy markets and renewed inflation concerns and shifting

trade rules added to volatility. At the same time, artificial

intelligence continued to move at pace from experimentation to

production, reshaping capital spending and market leadership. These

forces will influence investment opportunities and risks for years to

come.

In fiscal 2026, the Fund delivered a net return of 7.8%, earned $56.9

billion in net income and ended the year at $793.3 billion, up $78.9

billion from last year. Public equities were a key driver of results,

particularly in information technology in the first half of the year.

Infrastructure, energy assets, and credit also contributed meaningfully.

These gains were partly offset by foreign exchange losses as the

Canadian dollar strengthened against the U.S. dollar, and by losses in

government bonds, as central banks moved more cautiously on interest

rate cuts.

For a pension fund designed to support generations of Canadians, long-term results matter most.

Over the past decade, the Fund delivered an annualized net return of

8.8%. Over that period, all our investment departments contributed

positively to returns across very different market environments. This

includes areas such as private equity, which is facing a more

challenging period today, but has been a strong driver of absolute

performance for the Fund over the longer term.

Over time, cumulative investment income has become a significant part

of the Fund. At $549 billion, about 70% of the Fund today is a direct

result of investment activity. That is compounding at work: patient

capital invested across global opportunities with discipline around

risk, liquidity and cost.

To understand performance, we look at it through more than one lens.

The actuarial report provides an independent view of long-term financial

sustainability. Absolute returns grow the Fund and help pay pensions.

We also compare long-term results with global peers; Global SWF again

ranked the CPP as the second best-performing pension fund globally on a

10-year basis. And we use sector and geography relevant benchmarks to

assess relative investment performance. Together, these perspectives

give a fuller picture of how the Fund is supporting the CPP for

generations of Canadians.

Performance versus benchmarks

For the past three years, the benchmarks used to measure relative

performance have advanced faster and higher than our more diversified

portfolio built for long-term financial sustainability.

A component of the gap reflects a period in which large-cap, U.S.

equities outperformed smaller companies and other geographies by a wide

margin, while a relatively small number of technology and AI-related

heavyweights drove a disproportionate share of benchmark returns. In

addition, some parts of the Fund’s private-market portfolio – including

private equity and real estate – faced cyclical headwinds, which weighed

on more recent relative performance.

We did not design the Fund to mirror increasingly concentrated

markets. Rather, we build resilience into the portfolio even as it is

also designed to produce healthy returns over the long haul. Our

investment portfolio is diversified by region, sector, and asset type,

and actively managed to adjust to changing conditions. When market gains

are largely driven by a single sector, our approach can lag for a

period, but it is designed to reduce downside risk and keep the Fund

resilient through many market cycles. That matters for a pension fund

because the CPP must support contributors and beneficiaries through both

strong markets and downturns.

Over 10 years, value added versus the benchmarks remains positive at 0.7%.

We remain focused on improving both the absolute and relative returns

of the portfolio. Over the past year we reviewed the forces driving

performance, challenged our assumptions and tested alternatives –

including higher equity concentration, less diversification and

different geographic mixes – to see whether they could improve outcomes

without taking undue long-term risk. Some alternatives would likely have

improved short-term results, but to the detriment of long-term

risk-adjusted performance.

We have also taken a number of actions in response to recent

performance, including sharpening how we assess and manage AI-related

exposures, refining how we characterize private equity exposures and

reviewing geography and sector positioning. All to help improve

investment performance while maintaining the diversification and

resilience required for a long-term pension fund. We believe that these

new market conditions have revealed new opportunities to apply our

enduring advantages: the ability to invest at scale, to partner with the

best investors and operators, and to allocate capital flexibly across

asset classes and geographies.

We remained disciplined on risk and liquidity. We have maintained an

elevated level of liquidity in recent years, and that has served the

Fund well during periods of market volatility.

Although markets have recently rewarded concentration, our conviction

in diversification remains unchanged. We see diversification as both

essential and an act of humility: no investor can reliably predict which

narrow slice of the market will lead in any given cycle. While

benchmarks matter because they hold us accountable and push us to keep

improving, our goal is to build a portfolio that delivers the highest

long-term absolute returns, with resilience, across changing market

conditions.

Our investing activity, in Canada and beyond

Canadians rightly ask how the Fund invests at home. We apply the same

return-and-risk discipline in Canada as we do globally, and we invest

when opportunities meet our requirements.

At fiscal year end, we had $119.2 billion invested in Canada – an

all-time high in dollar terms. We are encouraged by the attractive

investment opportunities we are seeing in our home market.

This year we made a number of significant investments in Canada: we

expanded our Canadian mid-market private equity program with Northleaf

Capital Partners through an additional $750 million commitment; formed a

joint venture with Dream Industrial REIT and Dream Asset Management to

acquire last-mile industrial properties in major Canadian markets,

allocating $1.0 billion; and invested $60 million to Wealthsimple, one

of Canada’s fastest-growing money management platforms.

These investments reflect the same approach we use globally: backing

strong businesses and assets, partnering with experienced operators and

managers, and investing where we believe we can earn attractive returns

without taking undue risk.

Around the world, our teams also continued to make investments that

we believe will strengthen the Fund over the long term. This year, those

included investments in atNorth, a leading Nordic built-to-suit data

centre provider; Inkia Energy, a power generation company in Peru; and

Hitachi,a Japanese technology conglomerate.

How we run CPP Investments: cost discipline, efficiency and governance

Managing a pension fund at this scale requires strong governance,

clear accountability and careful risk management. CPP Investments

operates with an independent, arm’s-length governance model. We manage

market, credit, liquidity and operational and technology-enabled risks,

including those arising from AI adoption, through robust frameworks and

oversight built for a long-horizon investor.

We continued to focus on operating discipline. We now manage

approximately $220 billion more in net assets with fewer employees than

at the end of fiscal 2023, while investing in technology, data, and ways

of working that allow the organization to scale efficiently.

Cost discipline matters because every dollar spent is a dollar not

invested on behalf of CPP contributors and beneficiaries. As the Fund

has grown, we have built a scalable model focused on doing more with the

same base rather than simply growing our cost footprint. That

discipline supports net performance.

Positioning the Fund for a changing world

The investment environment is changing in ways that matter for

long-term returns. Conflicts, fragmentation, shifting trade and capital

flows, the build-out of AI infrastructure, digital sovereignty and the

whole-economy energy transition are reshaping investment conditions. We

respond by building a portfolio that can perform across many scenarios

and by investing where long-term fundamentals remain durable.

Conflicts, fragmentation and supply chains

Tariffs, trade disputes and geopolitical tension shape costs, supply

chains and investment conditions across many sectors. Conflicts in

Europe and the Middle East have also affected energy markets, shipping

routes and inflation expectations. These pressures can create market

dislocations and widen differences across countries and sectors. We

invest through that reality by diversifying by country, sector and

currency, and our global platform and long-standing relationships help

us evaluate opportunities with local insight and partner with operators

who understand their markets.

AI, infrastructure and digital sovereignty: investing behind the backbone

Data growth is increasing demand for data centres and the power and

grid capacity behind them. Governments and companies are also paying

more attention to digital sovereignty – the ability to store, process

and move data within trusted systems and jurisdictions. We are

increasing our focus on the infrastructure that supports the digital

economy, including power generation and storage, transmission and grid

upgrades, data hubs and related infrastructure, where long-term

contracts and strong counterparties can provide stable returns.

Climate: protecting value through a whole-economy transition

Climate change affects risk and opportunity across the portfolio

through physical impacts, regulation, technology shifts and changes in

energy systems. Progress is not linear. We embed climate considerations

into investment decisions across the Fund as we invest for a

whole-economy transition. That means we stay invested across sectors and

work with companies to reduce risk and protect value over decades

rather than relying on blanket divestment.

Within each of these themes, the thread is the same: long-term

investing requires patience, diversification and prudent risk

management. It also requires learning and adapting as conditions change,

without letting the latest narrative become the strategy.

Looking ahead

The CPP remains financially sustainable for generations, and the Fund

continues to grow through disciplined long-term investing. In a world

that will keep testing investors, CPP Investments will stay focused on

what matters for a pension plan: resilience, sound risk management and

strong long-term returns.

None of this happens without the dedication of our people. I want to

thank all my colleagues across CPP Investments, including our Senior

Management Team (SMT), for their hard work this year in pursuing our

mandate with focus and care.

This year, we welcomed David Colla to the SMT, succeeding Andrew

Edgell as Global Head of Credit Investments, following Andrew’s decision

to become a Senior Advisor with CPP Investments. I want to thank Andrew

for his leadership and contribution.

Uncertainty will persist. But the CPP was designed for exactly this

kind of environment: to provide a dependable benefit, paid for life and

indexed to inflation, through many market cycles. Contributors and

beneficiaries can continue to rely on the CPP as a stable foundation of

retirement income, and CPP Investments will keep investing the Fund with

discipline so that foundation remains strong.

Now, before I get to my discussion with John Graham, I think it's critically important to go over some items in the Fiscal 2026 Financial Results Overview, which is available to download here.

I will not go over all the slides in this presentation, so take the time to read it here.

One of the most important slides is this one on funding:

The base CPP funding ratio improved (and the bulk of the assets remain there), allowing for a proposed cut in the contribution rate from 9.9% to 9.5%. This was attained because of stronger-than-expected investment income.

Next, performance relative to benchmark over a 1, 5, and 10-year period:

As you will see below, I got into this quite a bit with John Graham because critics will be focusing on 1-year underperformance of the Fund (-5.4%) relative to benchmark and we discussed this at length.

Importantly, when you look at pension fund returns, you have to look at long-term returns to evaluate its performance and on this basis the Fund is still doing well.

The key culprits for the underperformance are well-known, concentration risk in US equity indexes remains very elevated, and that impacted relative performance, especially in private equity:

Despite the relative underperformance over the last 1 and 3 years, the Fund is not chasing returns and remains highly diversified to maintain its resilience over the long run:

And they are very careful about how they manage exposures:

This is critically important to remember because critics will focus on short-term performance and ignore the inherent risks of investing in passive equity indexes when concentration risk is high.

Again, I went over this with John, but I want to make it clear in my post that CPP will not/ cannot beat its benchmark every single fiscal year, especially when concentration risk is high and stocks are ripping higher. This is by design; the focus is on maintaining a globally diversified portfolio to maintain resilience over the long run.

The Fund also needs to manage its liquidity properly to make sure it can access funds when market dislocations occur and take advantage of them.

I am giving you important context to keep in mind before you read my discussion with John Graham below.

A few minor points of criticism that I shared with John and Frank Switzer during our discussion:

- CPP Investments needs to have a table next year where it discloses its 1, 5 and 10 year returns by asset class relative to the benchmarks as well as total Fund level. This has to be in the press release and if possible, also do one by calendar year (I know, I'm asking for a lot).

- Next, CPP Investments invests in top hedge funds all over the world and also invests in emerging hedge fund managers. We need more transparency on the performance of this external manager portfolio (performance, etc.)

Alright, long preamble but there is a lot to cover before I get to my conversation with John.

Discussion With CPP Investments CEO Going Over Fiscal 2026 Results

Earlier today, CEO John Graham called me to go over fiscal year results.

I want to begin by thanking him and Frank Switzer for setting up the call and sending me material early this morning.

John began by giving me an overview of total portfolio results:

The 10-year return of 8.8% which continues to be very strong, and I'd say comps well to global institutional investors. One-year return at 7.8%. Put that into context, we started the year this time last year we spoke, we were probably right into the kind of volatility of Liberation Day. We ended the year with the invasion of Iran, which obviously put the markets down for the last few weeks of the fiscal year, and through that, we had a market that rewarded concentration.

We had a market that rewarded concentration, and I think continues to reward concentration, and continues to have valuations that in certain parts of the market, to be blunt about it, that we struggle with.

So, we sit here today, and we sat there through the year. We have a pretty profound belief in diversification, even though diversification isn't paying off right now. And at a time when the range of potential outcomes is as big as it is today, we actually think it's time to lean into diversification and not lean out of it.

I would say the results were from having a well-diversified portfolio across asset classes and geographies, and in some ways, trying to be less concentrated in the broader markets.

I completely agree with him and noted in his message that he mentioned they looked at alternatives

for taking more concentration risk in their public equity exposure: "Some alternatives would likely have

improved short-term results, but to the detriment of long-term

risk-adjusted performance."

I asked him to explain:

That's a

little bit of what I was referring to. We spent a lot of time looking at some of the themes that were driving the market, and let's say the AI theme, and while we do have exposure to it, I think it's fair to say we're probably underweight compared to the broader markets. So, thinking about are there ways we would actually put in kind of a more concentrated exposure in, and if we did, how much would we want at the end of the day, you know, again we do have some exposure, but we're probably not at market weights.

At the end of the day, we have a view that if we take a step back and say who we are and what we're actually solving for, and that's to contribute to the financial security and retirement of 22 million Canadians. There are times when you have to let the market run away from you. There are times when, if you look at the dispersion of outcomes, you know our mandate is to maximize return with that undue risk of loss, and you have to pay attention to that second point of the undue risk of loss.

Now, we're not immune to a big market sell-off in any way, so I wouldn't want to give you that impression. But there are times when you think you know valuations are astronomical and you've got to make a decision that, as I wouldn't say we're a deep value investor, but we certainly believe in cash flows, and certainly believe in the long run you need to see cash flows that we'd rather be more diversified than concentrated.

That makes perfect sense to me. In fact, I told John this is how I read it. On a funding level, CPP is in great shape. The latest report from the Chief Actuary of Canada confirms this.

But I told him, over the short-term, CPP Investments and other Canadian pension funds have been criticized for not keeping up with their benchmarks, and we know that there are benchmark issues, especially in this type of market where the share of the semiconductor sector reached a high of maybe 18 or 19% of the S&P and MSCI ACWI recently.

I also noted hedge funds are driving these hot money flows, so he's right, chasing these stocks to keep up with the benchmark without consideration of risk is just plain stupid and dangerous.

So, I asked him point blank: "I think what you're telling me is you don't want to chase performance here, right?"

He replied:

Yes, that's right. So the way we think about performance is that we're close to CAD $800 billion AUM now, and you have to think about what that actually means from how you think about various alternatives. But there is a desire in this industry to reduce performance to a single number, and it's a little bit more complicated than that.

What I do is look at absolute returns, because you need to grow the fund. Relative performance is an important accountability framework, and it also provides a lot of insight into how your various programs are performing, but you can never lose sight of the purpose of the organization, and what the organization was actually created to do, and we're trying to jointly solve those three things, but it doesn't mean we put equal weight on each one at all time.

And you mentioned the funding ratio. The funding ratio is at 40%. It's what allowed the feds and the provinces to cut the contribution rate by 40 basis points, which is real money back into the pockets of Canadians, which is ultimately why we're here.

So we jointly solve for absolute, relative and kind of the sustainability of the plan, but they aren't equally weighted. And in times like this,

I'll say it to you, if

somebody really outperformed their benchmark over the past year, I think you'd have to look hard at how they did it and what risk they took to do it.

Again, I completely agree. I told him I have very close friends of mine who keep throwing in my face that the Norwegian sovereign wealth fund has outperformed all of the Canadian pension funds in recent years as the AI theme took off, at a fraction of the cost of Canada's Maple 8.

I told my friends that I know, I covered their 2025 results here, Norway's GPFG gained 15.1% in calendar year 2025, far outpacing all of Canada's pension funds but even that mighty fund, which has huge tech exposure and a different objective function, underperformed its benchmark last year.

All this to say, whenever I look at the performance of any fund, I look at the asset mix and the embedded risks in the portfolio, and try to understand it at that level.

I also stated the importance of looking at long-term performance for the Fund as a whole and by asset class where John remarked:

One of the things we did in this annual report is we put in 10-year returns, so maybe you planted the seed last year, but one thing in this annual report you will see is 10-year returns. I agree it's one thing that we've been trying to get more and more long-term, because that's what matters.

If it didn't come out clearly in the report, I can take that away, but you will see when you get into the report that we did actually add commentary on 10-year returns, and I think that's a great segue to private equity (PE). Look, diversification means that some things are firing and some things aren't. If everything is firing, you're probably not diversified.

The PE portfolio has been a long-term kind of contributor to performance. You get 10-year returns probably close to 12% for PE, but the short-term returns are challenged. And they're challenged in that you had a period of low distributions in the PE industry, and then the software challenges that in an asset class that had kind of gone overweight software.

PE, the way I think about it, is you have a, you have the stock in the flow, right? You have the portfolio that's in the ground, and then you have the new opportunities, and the stock has to be worked through. And broadly, in the industry, there are some challenges with the stock, but the flow is pretty interesting, and you've got to make sure you're not cutting off the flow because of decisions that you made five years ago around valuation.

What our PE team is doing -- and I'd be happy to have you spend time with Caitlin at some point -- they're actively managing the stock. You would have seen the press release about a $5 billion disposition to Blackstone and Ardian.

This is all about managing the stock, and I've been pushing on the whole organization, even real assets, real estate, for the past five years, and it's probably my credit background. You've got to actively manage these portfolios, you got to embrace a relative value perspective. When the investment thesis is played out, even if it's a good asset, sell it and find a better place to put the money. So one thing is, over the past year, there was a lot of turnover in the portfolio, which is going to serve as well going forward, but it's, it's a lot of work.

So, PE is definitely working through the working through the stock right now. I don't know, anything else I want to talk about PE. I can move on to the other asset classes.

Indeed,CPP Investments has the biggest private equity portfolio in the world. It is selling C$4 billion in fund stakes to Blackstone and Ardian on the secondary market, creating liquidity in that portfolio to invest in better opportunities going forward. Y

Yes, they're taking a little bit of a haircut as they sell at a small discount but it doesn't matter over the longer term, as they are investing the money where they see better opportunities.

I told John the thing with PE that scares me is whether there a profound structural change going on. Higher rates for longer, margin compression, much lower distributions, intense competition for assets throughout the industry, continuation funds to extend and pretend instead of taking a loss on an asset. It all makes me wonder whether the good old glory years are over for a very long time.

John replied:

Yes, it's a good question. I think you got to go back to first principles with PE, and ask why do you invest in PE? Do you believe it actually can add value? I think our kind of fundamental assumption is the governance model of PE allows the investor to get kind of right up close to the management team, and then drive some value creation through the organization.

Undoubtedly, the industry benefited from multiple expansion and kind of cheap leverage for a long time, and going forward, those are not two sources of return that you should really be baking into any projections. And it's going to come down to who really has the ability to drive value through the through the organization, and if there is multiple accretion, is because the fundamental quality of the business.

I think the asset class will come out in better shape from these challenges as they usually do, but there's going to have to be a bit of a shakeout. I think one of the questions that people have to ask themselves with private assets, like I think the institutional investor base also has to ask themselves, that when you have technology evolving at a quicker pace than your old period, what do you have to pay? Get paid for liquidity. What do you get paid to hold an asset for six to eight years with no liquidity on it? And I think we could have a debate as to whether or not liquidity has been properly priced in the market over the past few years or I should say, illiquidity.

Another excellent point. I asked him whether they are happy here with 22% exposure to private equity or whether they are looking to lower it going forward.

He replied:

One of the reasons PE got to that size is because it had good returns for a long time. From an allocation perspective, it's probably pretty close. It is higher than what we would have liked, because you don't want to do anything unnatural with these illiquid assets. At 22%, it's probably at the high end, but we would never do anything unnatural to bring it down.

I told him the reason why I ask him about PE exposure is that I see more opportunities in infrastructure right now, and from what I'm reading in their annual report, and in his message, particular data centers, energy, and so in the real asset classes.

John responded:

I think our appetite for PE and broader infrastructure are pretty similar, as long as we're getting paid for it in the real asset space. Energy is probably the one area that we've been pretty keen on for a while, and as you know, we have continued to invest across the entire energy spectrum.

Our oil and gas portfolio did great over the past year, our LNG portfolio did great, our renewables portfolio did great. Energy is something that the world needs more of. The world needs more electrons, and so we're keen on growing that portfolio, and we're seeing lots of opportunities there, but I still like PE, and I still think on the flow side, there continues to be good opportunities.

We have to take the long-term perspective here, looking at this market. I may have shared this with you before, it's been my experience in investing that this time is different, is over 10, and you have to continue to maintain that long-term perspective.

I asked if that is the same for real estate as well and he replied:

Look, we took some hits on real estate, and our real estate portfolio dealt a positive gain this year, but again, some of the data centers actually sit in our real estate portfolio and logistics has been good. We've got through the office and the retail pain. Our real estate portfolio, as you know, is smaller than some of the others, kind of six 7% and they're still active, looking for opportunities.

There's a new global head of real estate there, Sophie van Oosterom, and she seems to be doing a great job thus far but that portfolio is still in transition and fundamentals there are improving.

The other portfolio I asked John about was absolute returns, their massive external hedge fund portfolio made up of top global hedge funds and emerging managers. Heather Tobin, Senior Managing Director & Global

Head of Capital Markets and Factor Investing, oversees that portfolio, and I wondered why they don't share a lot more public information on it.

John replied:

I think we do disclose every manager on our website now, so I think every manager is disclosed on the website (some are listed here). I don't have a great answer for you. I'd have to look exactly what we put, because it's part of our CMF department, so we have a small systematic strategies group, but the CMF department that you see there, is almost entirely our external portfolio management team, which is the external hedge funds, and they had a great year.

They've had a great few years. I think it's also fair to say that the hedge fund industry had its best year ever in the past year.

[...] You should talk with Heather and Caitlin. I mean, PE and CMF, or the hedge funds. If we've had this conversation five years ago, everybody would have been gung-ho on PE and negative on hedge funds.

I will cover hedge funds tomorrow when I go over my quarterly activity but fair to say most of them jumped on the semiconductor trade in early April and are still riding it.

I circled back to benchmarks and said benchmarks matter a lot, especially for compensation. I said comp was based on five-year returns (maybe four-year), so you can underperform your benchmark in any given year but if you underperform over a 5-year period, compensation will be impacted.

And this AI investment cycle/ bubble can last for another three years, nobody really knows so I asked how they will handle this.

John responded:

So, as I look at this year, we've underperformed the benchmark three years running, and you know, and I think we got a good understanding why, and I think we have the conviction to maintain our current approach.

But as you know, markets can stay in their current state for a very, very long time, and if the markets continue to be concentrated like this, there's a good chance we'll underperform again if you get another 20% run by driven by a handful of companies. Institutional investors are not meant to keep up that way. It's a fact. I think that your math is correct, but you know that that's part of the part of how the industry works, right?

I said that's the only fear I have with this concentration risk. It can last, "markets can stay irrational longer than you could stay solvent", is an old famous expression, and these markets can stay irrational, especially in investment-led AI fuel bubbles.

That's one thing I realize, and we talk a lot about this throughout the industry, but you have to also remain disciplined. That's part of your focus. You can't just chase returns. It's going back to our initial conversation. You're going to get criticized by the Andrew Coynes of this world, but at the same time, you have to be very risk-conscious, a responsible fiduciary.

I told him you have a responsibility to be highly diversified.

John replied:

You mentioned something earlier, which I think is important to circle back to, when you brought up Norges. They run a very public strategy, so they're going to have a more kind of up and down portfolio by definition, but one of the things that gets forgotten in this, and you highlighted it, is pension plans have liabilities, and pension plans are created because of that liability, not because of the asset side.

You manage the assets to meet the liabilities, where sovereign wealth funds don't have liabilities, and that gets forgotten sometimes when people talk and mingle a sovereign wealth fund in a pension plan. To your point about comparing strategies, and even within the Maple 8, you have very different approaches to investing, because we have different liabilities and we have different kind of cash flow profiles. As we mature as an organization, now we're 27-28 years old, you see it, our approach is evolving based on what our liability stream looks.

I noted that additional CPP is much more diversified and much more risk-focused, because the liabilities are going to be changing, the profiles are going to be changing, and that additional CPP reminds me more, of what other Maple 8 pension funds are doing. I said base CPP is much more equity focused, private and public.

He replied:

That's because base CPP is a partially funded plan, and so as base CPP becomes more funded, when we started out as about 15% funded, and now it's 40% funded. As it becomes more funded, one would expect that it will kind of converge to look like other plans.

The additional CPP, for reasons of generational fairness, was set up as a fully funded plan with a really tight collar around it, so there's no real incentive to get it into a very overfunded status. That's why it has a very different risk profile, because it's 103% funded.

I interjected, saying "so you don't want to get to 125% funded" and he added:

It

actually can't, the way they set it up, it can't, because, but they didn't want that. They really wanted it to have a tight collar around it, and so to say to us, like, just keep this around 100 don't try to get it to 120 you're not being incentivized to do that.

I switched the conversation to discuss Canada, stating I know everybody's patriotic this year but I personally don't care if investments in Canada are increased unless it's in the right area (like infrastructure).

I understand it makes a lot of people happy. What I care about is the CPP Fund is taking the appropriate risks globally, and focuses on global investments, and I want it to do well over the long run.

I asked John where they are in their discussions in terms of infrastructure opportunities opening up, and what he can share with my readers on this front.

He replied:

Sure. I think you got to remember that Canada is still our second biggest investment destination after the US. We have on a growth basis C$120 billion invested domestically. It's a big portfolio. I would share that our pipeline in Canada is probably the deepest it's been in my memory.

We'll see what comes to fruition, and we'll see what really kind of plays out. Some of that is due to the ambition from the provinces and the federal government to actually do big things, and when you want to do big things, it attracts big money.

So, whereas we're seeing opportunities in de novo development, recycling of assets that we haven't seen before, but I would say it's very formative at this time, and I think you know various governments across the country need to figure out what they're solving for. Are they solving for privatization, are they solving for recycling capital, are they solving for improvement in operations, are they solving for someone taking over a capex program?

Some of these details have to be worked out, and that'll be, but I think we're hopeful, Leo, that we're going to see some good opportunities. My view on it, for what it's worth, I'm a big believer that you need to have competitive capital, and if there are opportunities in Canada or any country in the world, you should have global and domestic capital looking at those opportunities, and competition is what drives better outcomes.