The most creative sector of the business community has a dagger at its heart in the form of the relentless, unyielding, and over burdening cost of health insurance. The self-employed and very small businesses have seen their insurance premiums climb 20% to 75% since 2009. To purchase an adequate family plan, a self-employed person will pays an amount 50% to 70% of the nation's median personal income, $32,000 a year, for family health plan. This includes premiums, deductibles, and out of pocket expenses. That is twice the cost for relatively generous plans at medium to large size companies. Very small businesses, two to twenty employees, pay about the same (Image: Paul Henman)

Wasn't health reform supposed to take care of just this sort of inequity? Didn't the title of the bill say it all? The Patient Protection and Affordable Health Care Act There is no protection for the self-employed when they have these stark choices facing them due to unaffordable insurance rates. They can give up working for themselves; buy adequate insurance and take a huge hit to income; buy a substandard plan and hope that whatever comes up is covered; or, abandon insurance at real risk to their health and, in some cases, their lives.

What would the country be like if here were no self-employed individuals, no very small businesses?

Apple started out as two entrepreneurs in a garage. Microsoft began as a small tech company in Albuquerque, New Mexico. There is an impressive list of high revenue, high performing companies that traveled the route of self-employment and very small businesses.

The nation cannot afford to lose the extraordinary resources offered by the self-employed and very small business sector. It cannot afford the loss of small businesses that provide services like your favorite diner; solo and small group health practitioners; repair people; computer consultants; yard services; etc. The list goes on.

Business creativity and personalized services are on the chopping block, all because the self-employed can't afford their health insurance anymore than they can afford to risk their lives without adequate insurance.

This did not happen by accident. Before it ever arrived at the president's desk for signature, the health reform act contained a fatal poison pill.

State Insurance Commissioners in Charge

The very same people who failed miserably to protect the self-employed and small businesses in the past are now in charge of protecting them in the future. They were written into the health reform legislation early on. They have powers to determine the share of insurance premiums spent on your medical care and much more.

We were told that the president's healthcare reform legislation was special; that it would force insurance companies to spend the following shares of insurance premiums on actual medical expenses: 80% for single plans (individual and family) and 85% of premiums for small businesses. This was implemented for 2010.

Medium to large sized companies self-fund their health benefits. They pay the costs and have insurance companies manage the plans. These firms already spend 85% or more of their health benefits on medical care.

The self-employed and very small businesses are different. They cannot self fund their healthcare. They must buy directly from health insurance companies.

That is where the state insurance commissioners come in. Their group is called the National Association of Insurance Commissioners (NAIC). This association wrote the federal regulations that define what is and what is not considered medical care. Their definitions influenced insurance premiums. By doing that, they determine how quickly companies have to meet the 80-20 or 85-15 ratios referred to as medical loss ratios (MLR). Prior to this national standard, MLRs required by state regulations were any where from 55% to 70% for medical care.

NAIC was named to write more than just MLR regulations for the act (see Appendix). The regulations are implemented by the federal Department of Health and Human Services. NAIC defines allowable delays to putting the ratios in place. It defines "market destabilization" and "credibility" factors that allow an adjustment of MLRs in favor of insurance companies. The state insurance commissioners association has the broadest of powers to determine the quality, quantity, and cost of medical care.

Hijacking Health Reform Legislation

NAIC is a $75 million dollar organization. A third of its income comes from health insurance companies who pay fees to access data that NAIS collects. The association gains income from the very organizations they are tasked to regulate in the states. These are also the same insurance companies who are highly dependant on the health reform MLR and other regulations NAIS is writing for the new health care act.

There is a clear appearance of undue influence on NAIC by the insurance companies that help fund the organization. In 1998, Ralph Nader wrote an open letter demanding independent funding for the group to reduce this influence. To make his point, Nader described a NAIC research finding on minority discrimination that upset the health insurance companies. The companies simply withheld payment for data fees, the core income for NAIC, until NAIC "backed off" of its position. The letter exposed an ongoing problem but failed to generate any change.

The organization lacks independence from the insurance industry. Skepticism about the organizations effectiveness is well justified.

NAIC is governed by twelve elected and thirty-eight appointed state health commissioners. Those running for election need campaign funds. Insurance companies are major contributors. Those appointed gain the office from governors. For the appointed, the contributions are just one-step away from the commissioners.

Elected and appointed commissioners have hefty political baggage. These are not the type of objective analysts and thinkers you want writing critical regulations that will affect your health.

These are just some of the reasons to expect little or no change in rates for those who purchase their insurance directly, primarily the self employed and small business owners. Were there any reason to expect change, the change should have arrived by now.

On October 21, 2010, we saw the future. NAIC announced that it had completed its model regulations on medical loss ratios. On the very same day, Kathleen Sebelius, Secretary of Health and Human Services (HHS), announced that:

"We will work quickly to promulgate this regulation, using the NAIC recommendations as a basis, because we believe these new policies will help ensure not only cost savings but higher quality care for consumers. We look forward to working closely with NAIC throughout the process." Kathleen Sebelius, Secretary HHS, October 21, 2010

Sebelius must be a very fast reader. I hope that she will read about the total failure of her favorite regulatory authors to gain any "cost savings' while they regulated insurance rates in their states for the self employed and small business. Then she might realize that "care for consumers" is not possible without affordable health care.

Don't hold your breath.

END

This article may be reproduced entirely or in part with attribution of authorship and a link to this article.

Appendix

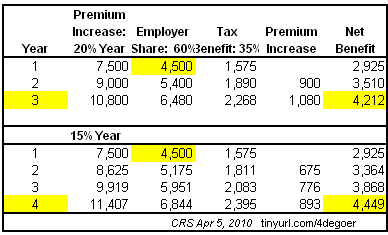

I. Tax breaks to very small business

The tax provisions of the health care act were supposed to help very small businesses afford insurance for their employees. It appears that the tax breaks will lose their utility about the time that they expire. While they offer initial savings, premium increases wipe out the benefits of the tax cut in year three using the 20% per year increase and year four using the 15% premium increase.

From: Summary of Small Business Health Insurance Tax Credit Under PPACA (P.L. 111-148) Congressional Research Service, April 5, 2010

II. The Influence of National Association of Insurance Commissioners (NAIC)

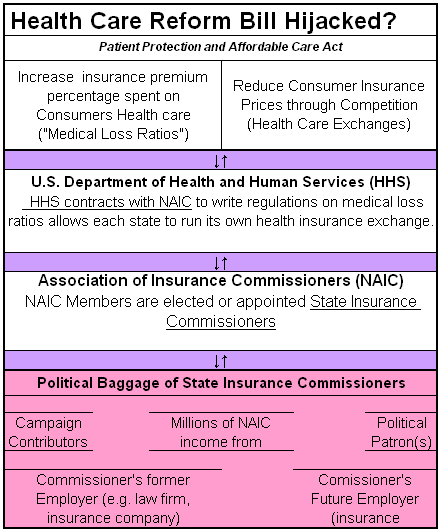

A) Political conflict of influence flow chart

This chart provides a graphic representation of the various potential conflicts of interest that raise serious questions about providing an association of elected officials and political appointees with vast regulatory power. After all, this is about our ability to stay well and deal with life threatening and other medical emergencies. Also see:

B) NAIC in the health care act:

The Patient Protection and Affordable Health Care Act

NAIC is mentioned through out the Patient Protection and Affordable Health Care Act. The association has vast powers which HHS is more than willing to give up. It is noteworthy that there are no formal ties mentioned between

NAIC will help insurance companies in ", in compiling and providing to enrollees a summary of benefits and coverage explanation that accurately describes the benefits and coverage under the applicable plan or coverage" (p. 192, pdf).

NAIC will determine the amounts for "reinsurance payments" for polls of high risk individuals without insurance based on its data (p. 209, pdf).

NAIC will also help with standards for Medicare supplemental insurance (p. 460-61, pdf), fraud and abuse reporting (p. 780, pdf), and help with standards for Medigap programs (p. 460-61, pdf).

NAIC has a special benefit. They have the privilege of total privacy, unlike the rest of us.

The transparency promised has not been delivered.

SEC. 6607. PERMITTING EVIDENTIARY PRIVILEGE AND CONFIDENTIAL

COMMUNICATIONS.

Section 504 of the Employee Retirement Income Security Act of 1974 (29 U.S.C. 1134) is amended by adding at the end the following:

(d) The Secretary may promulgate a regulation that provides an evidentiary privilege for, and provides for the confidentiality of communications between or among, any of the following entities or their agents, consultants, or employees:

(1) A State insurance department.

(2) A State attorney general.

(3) The National Association of Insurance Commissioners.

(4) The Department of Labor.

(5) The Department of the Treasury.

(6) The Department of Justice.

(7) The Department of Health and Human Services.

(8) Any other Federal or State authority that the Secretary determines is appropriate for the purposes of enforcing the provisions of this title.

(e) The privilege established under subsection (d) shall apply to communications related to any investigation, audit, examination, or inquiry conducted or coordinated by any of the agencies. A communication that is privileged under subsection (d) shall not waive any privilege otherwise available to the communicating agency or to an who provided the information that is communicated..

C) Medical Loss Ratio language

(1) REQUIREMENT TO PROVIDE VALUE FOR PREMIUM PAYMENTS.

A health insurance issuer offering group or individual health insurance coverage shall, with respect to each plan year, provide an annual rebate to each enrollee under such coverage, on a pro rata basis, in an amount that is equal to the amount by which premium revenue expended by the issuer on activities described in subsection (a)(3) exceeds --

(A) with respect to a health insurance issuer offering coverage in the group market, 20 percent, or such lower percentage as a State may by regulation determine; or

(B) with respect to a health insurance issuer offering coverage in the individual market, 25 percent, or such lower percentage as a State may by regulation determine, except that such percentage shall be adjusted to the extent the Secretary determines that the application of such percentage with a State may destabilize the existing individual market in such State. (p. 886, pdf)

(2) CONSIDERATION IN SETTING PERCENTAGES.—In determining the percentages under paragraph (1), a State shall seek to ensure adequate participation by health insurance issuers, competition in the health insurance market in the State, and value for consumers so that premiums are used for clinical services and quality improvements.

(3) TERMINATION.—The provisions of this subsection shall have no force or effect after December 31, 2013.

Also see:

NAIC Model Regulations October 27, 2010

REGULATION FOR UNIFORM DEFINITIONS AND STANDARDIZED METHODOLOGIES FOR CALCULATION OF THE MEDICAL LOSS RATIO FOR PLAN YEARS 2011, 2012 AND 2013 PER SECTION 2718 (b) OF THE PUBLIC HEALTH SERVICE ACT

Federal Register December 1, 2010: Part III Department of Health and Human Services 45 CFR Part 158

Health Insurance Issuers Implementing Medical Loss Ratio (MLR) Requirements Under the Patient Protection and Affordable Care Act; Interim Final Rule

Comments

Less For More

I believe that most citizens see health care reform ( Obamacare ) as being less benefits and coverage, and more cost. The main villains in the medical professions remain doctors, hospitals, and clinics. In addition to the "hands-on-care" provided by medical personnel, pharmaceuticals are basically legalized thieves. Proper health care is a necessity, and therefore a perfect scenario for fraud, corruption, and price gouging. While some are quick to blame insurance companies for the high cost of health care, they fail to realize and understand that hospitals do not ask insurance companies if they can charge $5.00 for an aspirin, or if they can charge $900.00 a day for a tiny filthy hospital room.

The health care industry, like many others, are very influential on the floors of Congress. It is doubtful that the medical professionals will fall into poverty, or be forced into bankruptcy by any legislation that might get through Congress. Remember we have a Lobbyists' controlled U.S. Congress. Votes on the floors of congress are bought and paid for by the corporate elite, the wealthy, the influential, and the powerful.

Health care cost, energy cost, and wars, will eventually bankrupt John Q. Public. Affordable health care will not happen in the foreseeable future, and maybe not in my life-time. The economic deck is always stacked against John Q. Public.

Because you can do wrong, and get away with it, doesn't make it right

Higher good

You have this nailed down: "Health care cost, energy cost, and wars, will eventually bankrupt John Q. Public." We are well on our way. There are rational solutions to each of these problems but rationality depends on good will. Our leaders would rather pose and profit than study, plan and implement. The good news is that this is a problem of the very few who control finances. Once the public has the will to do something about that, we're going to do things people never thought would get done.

Michael Collins

nice call out

They assuredly are screwing the individual or self-employed policy holders. What was the latest CA increase, 69% over a year in premiums?

They are forcing people who could be starting businesses, generating jobs, working independently to get some crap job and stay there just over health insurance.

It's starting to look increasingly insane to tie people's health and insurance to employers.

Thank you Robert

Wasn't that a great picture of Allen and Gates. Just a couple of exceptionally bright people who took the big risk. As you pointed out to me originally, when a decent health insurance plan comes close to the individual media income, we're in serious trouble.

Michael Collins

MEDIAN income (and Sen. Monynihan)

Maybe there's a pun intended around 'media income', I'm not sure, but I think it's a typo. I think Michael Collins intended:

"when a decent health insurance plan comes close to the individual MEDIAN income"

But I don't mean to nitpick. Just was referred to this article from a link in a recent comment, I think at the Bankruptcy Hell article.

About median INDIVIDUAL income, I would note that the WAGES (including self-employment) part of that is subject to the Medicare tax - regardless of whether the worker who reports the wages (and pays the tax) has any publicly funded (or otherwise) medical insurance, or not. Any real medical insurance reform that fails to adequately address this glaring inequity is no real reform at all.

To my memory, the only well-known member of Congress to address this inequitable taxation policy was the late great Senator Daniel Patrick Moynihan, who was replaced by Hillary Clinton. Did Hillary campaign for president on this issue? Not to my recollection.

While there are certainly

While there are certainly some doctors who seek to game the system for their own financial advantage, I disagree completely that this is the norm.

Several key bits of evidence:

1) There are 2 health insurance company employees for every doctor in America. These employees collectively provide zero health care - they are a bureaucracy which drives up costs. It isn't that these should all be removed, it is that there are clearly far too many.

2) Doctor's pay. Sure, they may make $500,000 a year for key specialties, $150,000 a year for others on average.

But even the former figure only encompasses $250/hour.

Consider the hourly cost of the surgeon in an open heart surgery: 10 hours? 5 hours? this $25000 or $12500 is an insignificant cost compared to the operation itself.

In reality any hospitalization or visit to the OR has a doctor's fee component which is insignificant. The rest? The hospital's bureaucracy and other overhead costs.

It isn't that socialized medicine will fix everything; the Canadian model is equally flawed for a non-oil exporting nation.

It is that there is no alternative: the government could very easily offer a 'safety net' for all individuals as it already has a gigantic health care cost administration sector (Medicare) and a huge health care delivery sector (VA hospitals).

Furthermore while a government employee might not work that hard, might not be that motivated, etc etc - at the same time they could give a crap about squeezing profits via denying health care.

I find a bit of BS in the figures

I enjoy reading things that present objective subjects to debate but when I read such things that are easy to prove as propaganda.....well it makes me want to become an anarchist. Fight the machine which propaganda like this.

"a self-employed person will pays an amount 50% to 70% of the nation's median personal income, $32,000 a year, for family health plan. This includes premiums, deductibles, and out of pocket expenses. "

Only? Bet most people would jump at one quarter of that "only" hourly pay.

"2) Doctor's pay. Sure, they may make $500,000 a year for key specialties, $150,000 a year for others on average.

But even the former figure only encompasses $250/hour. "

What??? You again find $2,000 an hour to be insignificant.

"Consider the hourly cost of the surgeon in an open heart surgery: 10 hours? 5 hours? this $25000 or $12500 is an insignificant cost compared to the operation itself.

In reality any hospitalization or visit to the OR has a doctor's fee component which is insignificant. The rest? The hospital's bureaucracy and other overhead costs."

You seem to think that the very well paid, highly paid individuals in the system are insignificant? My friend the PA makes $125,000 a year and complained about the receptionist's pay of $21,000 a year. I know a guy working the ER shift that makes $225,000 a year (before benefits).

Recently the newspaper wrote an article. The heating bill for one of our small hospitals (non profit) is $35,000 a month during the winter, $100,000 for the year. That is not small change. Takes quite a few insurance premiums to pay for the heating bill on just one hospital

This business of medical care is expensive stuff and I get tired of people that don't look at things in a rational manner.

I just went to a quote site and did a quote for my family -

PPO Plan 7 - Optional RX and Maternity Available

Plan Type Deductible Coinsurance Office Visit

$2,500 20% $20

Monthly premium $639.00

$32,000 a year, for family health plan......pure propaganda!

Do the math

According to the Kaiser Foundation's 2010 report, the average cost of health insurance is $13770.00 per year. That's for a medium to large company that uses it's own funds to pay medical costs. The health insurers are just administrators, although the checks come from them. Those are not health care costs, they're insurance costs. You add on another $2,300 to the $13,700 for out of pocket expenses: co payments, procedures not covered, etc. Then there's the deductible, an expense threshold that has to be reached before the plan kicks in. That ranges from $500 per person on up. For a family of three that's $1,500.00. The grand total for the efficiencies of a direct payment by employer plan is$17,500.

The self employed get no such deal, as is the fact and as I explained clearly. Remember, we're not talking about premiums. Those can be very cheap. But healthcare isn't. Take this Utah plan from an article I wrote in 2009, Screwing the Self-Employed Out of Health Insurance.

Utah 2 person plan (five other states presented as well with original insurance company quote)

Annual Premium: 1682.15 ($140.18 a month)

Deductible: $15,000 (2 person family-$7,500 each)

Prescription Drug deductible: $2,000 (2 person fam ily $1,000 each)

Those procedures, medicines, etc. not covered are in addition and do not satisfy the deductible.

That's how you look at this.

When you compare low deductible plans with high deductible plans, they come out about the same for total health care costs (not ust premiums).

The self-employed tend to be older - 38% are 40 to 60. That drives rates up. In addition, the insurance companies take 30 to 45% right off the top (compared to 5% for Medicare and 15% at most for employer self funded plan administration).

Here's what it looks like when you add premiums, deductibles, and adjust for cost of living for six sates in 2009. Rates and costs have gone up considerably since then.

(NCPA refers to a think tank analysis in blue that was premiums only. That's propaganda!)

If you take Massachusetts at $17,000 a year, increase it by 20% to bring you to 2011 rates, it comes to $24,480. That is 75% or more of the individual median income in the USA.

Michael Collins

Insurance employees versus doctors

Doctors perform a service, even mediocre doctors can save your life, deliver a baby, etc. Health insurance companies add no value to the health equation. They subtract. Eliminating the insurance carriers would save 25% immediately. That would allow for the reasonable compensation of those who keep us healthy. There are many doctors making $500,000 but many more who are around $300,000. When you consider that medical school is between $200,000 and $500,000, it is clear that those investments need to be recovered.

But practitioner rates are under control in terms of increases. Specialists who are not covered raise rates all the time but they don't effect insurance or health care costs for the rest of us.

The Swiss model may have been an alternative to state run care. It's private insurance but highly regulated. Here we turn the entire process of defining how healthcare reform works over to failed regulators. Something has to give. The self-employed and very small businesses are the canaries in the cave of the medical system. These problems will get worse for everyone soon if reality is not brought to bear.

Michael Collins

There are many ways ...

... to successfully organize medical care in a modern nation-state, but they mostly seem to require a functioning democracy.

Meanwhile:

"There are many ways to drown, only the most obvious wave their arms as they're going under." — Nick Flynn (Another Bullshit Night in Suck City)

Looks Like I'm Out of Luck

I've been asking for months now how the new and improved health care system will work for me: single, female, small business owner, no children, never been sick (knock on wood) so no preexisting conditions, but sure as hell can't afford the cost of health insurance. The last time I worked for a company, and on a 'cafeteria benefits plan', I dropped my health insurance after 4 years with the company, as the rates increased 25% each year. I instead put that money into my IRA. So for the next 4 years, instead of buying health insurance with my cafeteria plan, I placed it into the IRA. And we see how that has worked out. The only solace I have is that instead of paying that money to the insurance industry, AND NOT GETTING SICK DURING THAT TIME, I was actually able to keep that money...at least until the time that I may get sick.

I own my home and I'm seriously considering selling my property with lifetime rights. That way if I do get sick, they can't take what I've worked for all of these years, and I'll go to the emergency room. Either that or I will throw a brick through a post office window and let them put me in jail where I will receive health care.

Lastly, I'm reminded each time I pay my 15.3% social security self employed tax, that someone out there is getting health care, but it sure ain't me.

Sorry to tell you about this

Don't forget - your self-employment tax includes the "medicare tax" which is paid by working people to fund medical care mostly for people who are not working. It would have been easy, considering the Medicare tax that has been levied for some time now, to expand the Medicare system rather than enact the so-called Affordable Health Insurance Act to make it illegal for self-employed people NOT to pay private insurance companies.

But that's not the worst of it:

A few years back, less than 10 years ago, Oregon reneged on promises made to a quadriplegic who had been assured that he could receive state aid for home care if he would give the state title to his home (while he retained lifetime rights). The man had signed over this home on the conditions, but Oregon reneged (without returning title to his home).

The policy whereby this happened followed an election in which the public rejected an income tax increase on high income brackets.

The policy was insane since it drove the man into a facility which cost more than the home care. BUT the facility care was picked up by federal funds, whereas the home care was all or mostly on the State of Oregon.

I personally know home care nurses (working part-time in various private residences) who, after that policy was implemented, were left with the choice of abandoning bed-ridden patients or continuing to drive to their homes and provide care WITHOUT PAY. Many home care nurses did provide care for some time WITHOUT PAY. And many of those home care nurses are self-employed, working for service organizations or companies on 1099s.

I am not sure, because the law is so complex and disputed as to constitutionality, etc., but it may be that the recent legislation did something to improve the kind of situations here described. I don't know, but I do know that the cases I am describing were about severely physically disabled people, with intact mental functioning. (Not addressing issues about brain-dead.)

Insurance

I think what scares people the most is that they call it "Health Care Reform" when it is actually "Health Insurance Reform." Our care doesn't need reformed but the insurance and the cost of that care does. It is terrible how the self-employed pay so much more for insurance.

Insurance vs. care

Thank you for noting that. In my comment, above, I referred to the 2010 legislation as 'Affordable Health Insurance Act" but it is actually titled "Affordable Health Care Act".

Didn't George Orwell call it "NewSpeak"?

Care Reform

Richard,

FYI :

Every year in the US there are:

12,000 deaths from unnecessary surgeries;

7,000 deaths from medication errors in hospitals;

20,000 deaths from other errors in hospitals;

80,000 deaths from infections acquired in hospitals;

106,000 deaths from FDA-approved correctly prescribed medicines.

The total of medically-caused deaths in the US every year is 225,000.

This makes the medical system the third leading cause of death in the US, behind heart disease and cancer.

( http://www.dailypaul.com/node/153886 )

Because you can do wrong, and get away with it, doesn't make it right

Thanks to Sonny Clark

Great catch. Thanks.