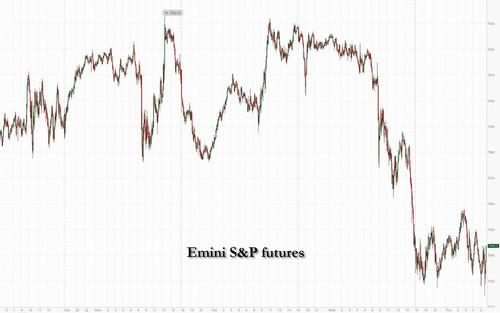

Futures Slide After Broadcom Forecast Miss Chills Tech Euphoria

US equity futures are weaker, dragged lower by Tech after a disappointing outlook from Broadcom triggered doubts that the blistering rally in technology shares had gone too far, a move exacerbated by euphoric positioning. As of 8:00am ET, S&P futures dropped 0.4%, while Nasdaq futures slumped 1.2%. Broadcom, which added around $150 billion in market value just this week, slumped 13% in US premarket trading after its forecast for artificial-intelligence semiconductor revenue in the current quarter fell short of expectations. CrowdStrike shares also drop 10% after their revenue projection failed to impress investors. Semis are under pressure following AVGO’s earnings, while Mag7 are bid led by AAPL (+1%). Parts of Cyclicals and Defensives are bid as portions of the AI Theme are weaker pointing to a potential de-risking or the very early stages a rotation. Given the sell off in APAC and EU bid, it appears to be the former rather than the latter. Bond yields are lower as the curve bull steepens, and USD weakens. Commodities are lower as Energy sells-off on news that Israel / Lebanon will resume their conditional ceasefire within 24 hours (although Hezbollah was notably not mentioned); but, precious metals are a notable outperformer. Today’s macro data focus is on Challenge Job Cuts, Initial Claims, and Continuing Claims, with NFP coming tomorrow.

In premarket trading, Mag 7 stocks are mixed (Microsoft +0.8%, Amazon +1.1%, Apple +1%, Alphabet +0.4%, Nvidia -1%, Meta Platforms -0.7%, Tesla -0.8%.

- Broadcom (AVGO) is down 14% after the chipmaker gave an outlook that was seen as underwhelming, given the industry’s AI-related demand. Analysts note that AI sales and margins for the current quarter are weaker than expected. AI-linked companies fall after Broadcom’s outlook for AI chip revenue failed to impress investors. Decliners include Intel (INTC), which is down about 4%, and Lumentum (LITE), which is falling 3%.

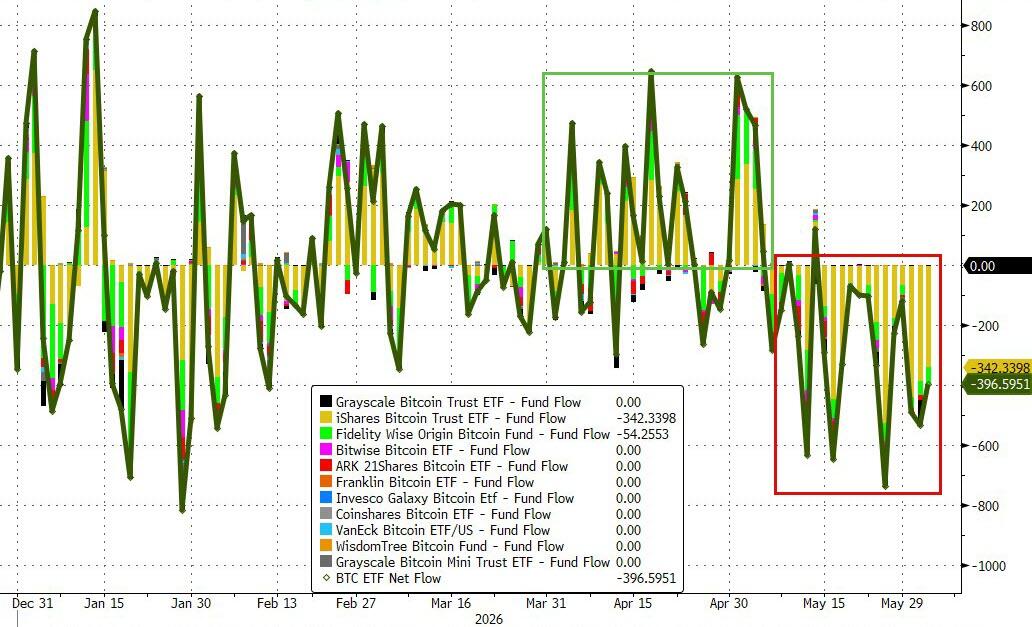

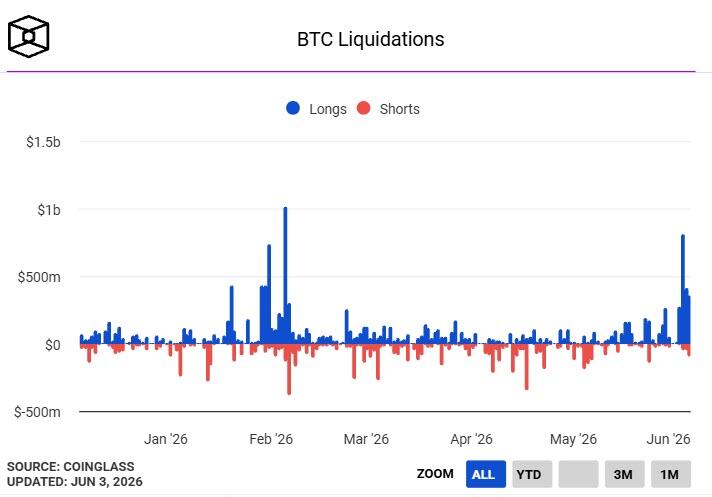

- Cryptocurrency-linked stocks fall as Bitcoin extended losses for a fifth consecutive session after renewed clashes in the Middle East weighed on market sentiment.

- Ciena (CIEN) falls 5% after the maker of equipment used by telecom companies posted quarterly results.

- CrowdStrike (CRWD) falls 10% as the security software company’s first-quarter beat wasn’t strong enough to lift the stock that has more than doubled from a March low.

- Five Below (FIVE) falls 10% after the retailer reported results, and while the quarter was a “standout,” the growth rate might be peaking, according to Jefferies.

- Netskope (NTSK) tumbles 19% after the cloud security firm reported an adjusted loss of 6 cents per share in the first quarter.

- Petco (WOOF) falls 12% after the pet health and wellness company’s adjusted Ebitda forecast for the second quarter came in below the average analyst estimate.

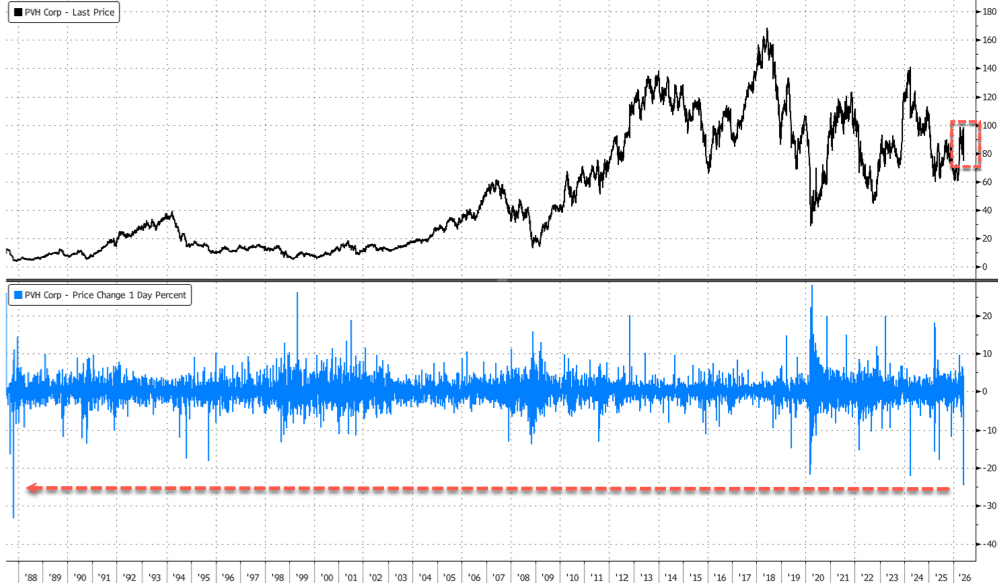

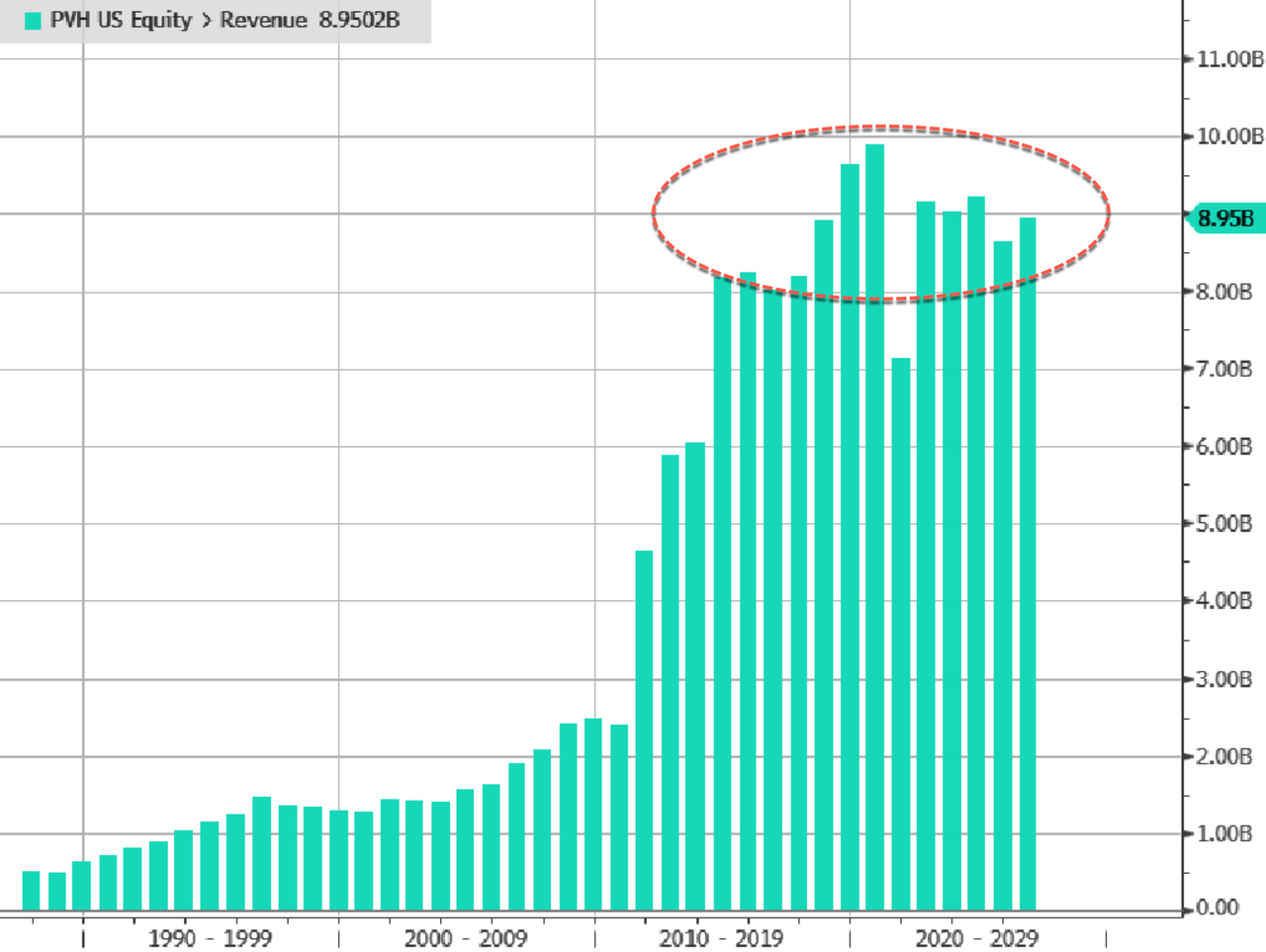

- PVH (PVH) slides 22% after reaffirmed adjusted earnings-per-share guidance from the owner of the Calvin Klein and Tommy Hilfiger brands missed consensus estimates. Analysts note sustained pressures from the Middle East conflict.

- UnitedHealth (UNH) rises 2% after BofA Global Research upgraded the health insurer to buy, citing improving medical cost trends.

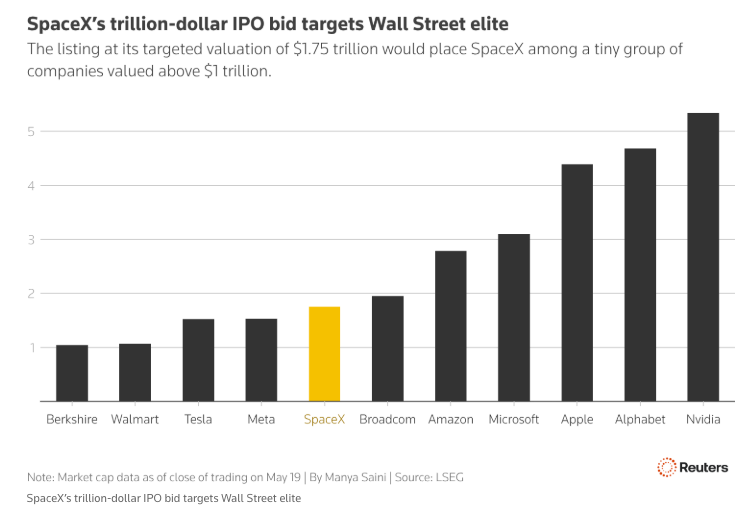

In other corporate news, Eli Lilly and BioNTech joined a growing chorus of drugmakers warning that proposed healthcare reforms in Germany risk undermining investment in Europe’s biggest economy. Some members of the billionaire Glazer family have been debating whether to sell their stake in Manchester United FC, after more than 20 years of ownership. Netflix is using AI to help customers cut through the noise of content overload. In other news, Alphabet upsized its equity raise to $84.75 billion from the $80 billion it announced just two days earlier. Mike O’Rourke at Jonestrading said a recent Alphabet investor presentation “sounds like bragging about plans to spend beyond free cash flow generation.” He questioned what he called “a bold spending stance at such an early juncture” in the competitive industry. Elsewhere, SpaceX is seeking to raise $75 billion in a record IPO to fund expansion of its AI, rocket launch and satellite infrastructure. Based on the SEC filing, it would have a market value of almost $1.77 trillion.

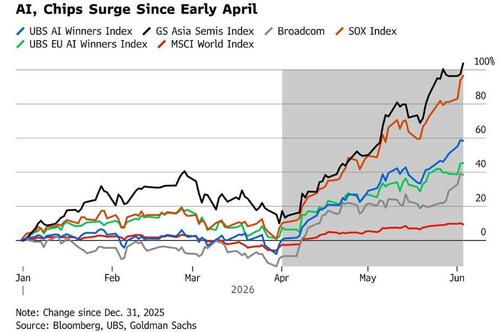

Broadcom reminded upside-chasing investors that risk still exists in markets, with its shares tanking 12% in premarket trading after it issued a disappointing forecast for full-year sales of its AI chips. Still, if the stock opens at similar levels in the cash market, it’ll only be back to where it was trading last Thursday. Those earnings followed weeks of “great-to-amazing results from its competitors and partners, which meant the bar was extremely high (some would say impossibly high),” notes Vital Knowledge founder Adam Crisafulli. The stock had soared 65% from its 2026 trough on March 30, making it the third-biggest point contributor to the S&P 500’s 20% surge.

The downturn extended to other corners of the tech trade, with cybersecurity firm Crowdstrike Holdings Inc. dropping 10% even after raising its revenue forecast. The sector also fueled losses in Asia, where South Korea’s Kospi index fell 1.8% while the Korean Won tumbled to the lowest since 2009. Europe’s benchmark was down 0.2%.

Tech and AI will remain in focus for traders: earnings are due from Ciena premarket and AI pioneers are due to speak at Bloomberg Tech — while TSMC reminds us that chip supply won’t meet AI-fueled demand for years. Chipmaker Cerebras Systems said it plans to cooperate with a wide variety of suppliers of AI data center components, except Nvidia.

Concern over the AI trade threatens to dent a record-breaking rally that has seen global gauges shake off worries about the biggest disruption to oil markets in history. The risk-off tone comes even as Brent heads for its first daily retreat of the week, trading 1.4% lower at about $96.40 a barrel.

“Valuations are looking slightly frothy in pockets of the market which have seen the strongest gains over recent weeks,” said Wolf von Rotberg, equity strategist at Bank J Safra Sarasin. “A leadership change in equities is not unlikely at this point, with less powerful drivers than tech taking over.”

In hedge fund news, D.E. Shaw is extending the time it will take investors to fully exit two of its biggest hedge funds, as it joins peers such as Millennium and Citadel in seeking to keep client cash for longer.

In politics, the Republican-led House voted to halt the US war with Iran, breaking with President Donald Trump on an unpopular conflict. Trump announced that he planned to soon make Todd Blanche “permanent attorney general” months after he assumed that post in an acting capacity.

European stocks have fared better as oil prices retreat, with the Stoxx 600 little changed. The Stoxx 600 was up 0.2%, led by consumer stocks which were boosted by positive earnings from Remy Cointreau. The artificial intelligence trade took a breather following a disappointing outlook from Broadcom. Here are the biggest movers Thursday:

- Remy Cointreau shares rose as much as 15%, the most since January 2024, after the French alcoholic drink maker reported earnings that slightly beat consensus profit expectations

- CMC Markets shares rose as much as 18% to highest since August 2021, after the online trading platform guided to stronger-than-expected FY27 revenue and highlighted accelerating growth across its partnerships and institutional businesses

- Abivax shares climbed as much as 14% in Paris, extending a rally after the stock plunged due to cancer cases in a crucial clinical trial

- Puuilo shares rose as much as 6.3%, the most since March, after DNB Carnegie predicted that upcoming first-quarter earnings would show the Finnish retail group started the year on a “solid footing,” helped by improving consumption

- Partners Group shares rose as much as 1.8%, attempting to recover from the previous day’s record 16% drop that was triggered by the Swiss investment firm’s decision to cap withdrawals from one of its private equity funds

- Universal Music shares fell as much as 7.6% on Thursday morning to €17.74 after Bill Ackman sold his €1.42 billion ($1.65 billion) stake in the record label just days after the Amsterdam-listed company rejected a takeover bid by the hedge fund billionaire

- Tech hardware stocks in Europe fall on Thursday and pare their year-to-date gains after US-listed Broadcom gave an outlook for artificial intelligence revenue that missed more bullish expectations

- Pirelli shares declined as much as 13% as Grizzly Research said it’s short the Italian tire maker, citing concerns regarding the company’s exposure to Russia

- Burckhardt Compression shares fell as much as 13%, the largest daily drop in over six years, after the Swiss industrial manufacturer’s full-year results showed a significant drop in order intake

- Intrum fell as much as 19%, the most in a month, after the Swedish credit management firm announced the terms of its SEK7.5 billion capital raise

Asian stocks are poised to snap a four-day winning streak as the artificial intelligence rally that drove a regional benchmark to record highs lost steam, following Broadcom’s underwhelming forecast. The MSCI Asia Pacific Index fell as much as 1.8%, on pace for its worst day since May 15. Chip-related companies including Samsung, SK Hynix and TSMC were among the biggest drags. Most markets in the region slipped, led by South Korea, Indonesia and Taiwan. The blistering rally in Asian chip stocks has left them exposed to any doubts about the durability of the AI boom. Broadcom’s weaker-than-expected guidance rattled investor confidence, sparking declines in shares that had benefited from high expectations for sustained tech hardware spending.

In FX, the Swedish krona is the best performing G-10 currency, rising 0.6% against the greenback after CPI surprised to the upside. The South Korean won fell to the lowest since 2009 even as the government pledged to curb excessive volatility.

In rates, treasuries trade near session highs in early US session, with modest gains led by front-end tenors amid oil price declines. Yields in 2-year sector yields are nearly 4bp lower on the day. Treasuries outperform bunds and gilts, with Bank of England Governor slated to speak at 11:40am New York time.US yields are 1bp to 3bp richer across a steeper curve, leaving 5s30s spread 2bp wider on the day near session highs; 10-year near 4.47% is 2bp lower, outperforming bunds and gilts in the sector by more than 1bp

In commodities, WTI crude oil futures are down more than 2% following three straight increases; Washington and Tehran have a framework to extend a truce agreement by two months, reopening the Strait of Hormuz, but an agreement hasn’t been reached and sporadic attacks have resumed.Oil prices and yields extended declines in early US trading after US President Donald Trump said negotiations to end the war in Iran were in final stages, repeating a comment he’s made at least twice since mid-May. Precious metals advance while Bitcoin falls to the lowest since before the Iran war began.

US economic data calendar includes 1Q final productivity and unit labor costs and weekly jobless claims (8:30am). Fed speaker slate includes Barkin (8:30am), Bowman (10am), Daly (11:40am, 1:10pm) and Schmid (1pm)

Market Snapshot

Top Overnight News

- An informed source to Al Arabiya said the agreement on the release of frozen Iranian funds in its final stages, but the search continues for a mechanism on frozen funds. However, US President Trump informed the mediators of his refusal to release funds to Iran before signing the agreement.

- Israel and Lebanon agreed to a ceasefire in US-brokered talks, with the ceasefire contingent on Hezbollah's evacuation from the Litani. Despite this, there have been reports of continuing attacks in Southern Lebanon.

- House backed a resolution curbing Trump's Iran war powers with the House voting 215 to 208 to pass the War Powers resolution.

- Nasdaq Futures Tumble as Broadcom Tests AI Trade: BBG

- SpaceX Seeks $75 Billion in Record IPO to Fund AI, Launch: BBG

- Challenger Job Cuts (May) 97.006K (Prev. 83.387K); May Job Cuts Rise 16% from April, the highest May total since 2020.

- Trump is to announce nearly USD 700mln in coal support and to use the Defence Production Act for the coal sector: Axios.

- Trump Says He Plans to Make Blanche ‘Permanent Attorney General’: WSJ

- Agricultural Secretary Rollins announced additional USDA personnel deployment to South Texas, and urged livestock producers to remain vigilant, while she stated that potential New World screwworm detection is being fully contained and is not a harm to US food supply or safety.

Iran War News

- US President Trump said they have been hitting Iran pretty hard and Iran negotiations are going well, while he suggested a deal could happen over the weekend and said anything can happen when you are dealing with Iran, but also stated it could go another two or three weeks. Trump also stated he would rather not use the military in Iran, and would rather not wipe Iran out, as well as noted that they are close to signing papers in theory. Furthermore, Trump said they are trying to separate Iran and Lebanon issues, while he responded that in that part of the world, a ceasefire is when you're shooting in a more moderate manner, when questioned about the ceasefire.

- US President Trump told aides privately that he would consider ending the ceasefire with Iran if US troops are killed, according to WSJ.

- An informed source to Al Arabiya said the agreement on the release of frozen Iranian funds in its final stages but the search continues for a mechanism on frozen funds. US President Trump informed the mediators of his refusal to release funds to Iran before signing the agreement. The source notes that the main obstacle relates to the mechanism for disposing of part of the frozen Iranian funds and there is a proposal to create a special fund for depositing frozen Iranian funds that is under discussion.

- Sources noted that the first phase of the interim agreement between the US and Iran involves cessation of direct military operations, phase 2 is a full reopening of maritime traffic, phase 3 includes limited easing of some sanctions and phase 4 includes major issues such as the Iranian nuclear program, according to Al Hadath.

- Pakistani Foreign Minister, on reports of halted US-Iran talks, said "Our dialogue process continues”, Pakistani journalist Mallick posted.

- Israel and Lebanon agreed to a ceasefire in US-brokered talks, with the ceasefire contingent on Hezbollah's evacuation from the Litani, while Lebanese armed forces will take control of pilot zones, and Israel and Lebanon agreed to reconvene negotiations in the week of 22nd June.

- US State Department confirmed Israel and Lebanon agreed to the implementation of a ceasefire and that the sides agreed with guidance of the US to swiftly advance creation of pilot zones in which Lebanese armed forces will take exclusive control of the territory. Israel and Lebanon also reaffirmed they have no hostile intent towards one another and are committed to continuing negotiations.

- Lebanese President said the implementation of the ceasefire could begin within 24 hours of final approval, Arab News reported.

- The Israeli army has begun withdrawing its forces from Dibbin in southern Lebanon, Al Hadath reported.

- Israeli Defence Minister said the IDF will continue its operations on the ground in Lebanon at this stage, Al Hadath reported. "The Lebanese will not return to the south and we will continue to destroy infrastructure."

- Israeli military said fighting in Southern Lebanon continues.

- Israeli airstrikes were reported in several areas in southern Lebanon, according to SNN.

- Hezbollah attacked Israeli positions in southern Lebanon.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were lower following the negative handover from the US, where risk sentiment was weighed on by the recent retaliatory attacks between the US and Iran, as well as weakness in tech stocks. ASX 200 was pressured by underperformance in the mining and materials industries, while most sectors were subdued aside from the resilience in defensives. Nikkei 225 retreated from record levels and briefly tested the 67,000 level to the downside amid intervention risks following FX comments from Japanese PM Takaichi, while comments from BoJ Governor Ueda signalled the central bank could resume rate normalisation this month. On that front, hawkish BoJ sources noted the central bank is to mull a hike this month, with another possible in 2026. Hang Seng and Shanghai Comp conformed to the downbeat mood amid tech-related headwinds and with the PBoC refraining from open market operations for a second consecutive day.

Top Asian News

- Australian Balance of Trade (Apr) 1.791B vs. Exp. -1.61B (Prev. -1.841B).

- Australian Imports MoM (Apr) M/M 0.8% (Prev. 14.1%).

- Australian Exports MoM (Apr) M/M 7.2% (Prev. -2.7%).

European bourses (STOXX 600 +0.1%) started the European morning on a positive footing, as markets digested positive geopolitical updates from President Trump and a Lebanon-Israel ceasefire. However, markets have since soured amidst reports that Israel were conducting operations in Lebanon, and following the negative action seen across the pond. European sectors are mixed. Retail (+1.7%) continues to gain following the earnings by Inditex on Wednesday. Consumer Products & Services (+1.7%) and Travel & Leisure (+1.2%) round out the top 3. The laggards include Telecoms (-1.6%), Media (-1.6%) and Basic Resources (-1.1%).

Top European News

- UK PM Starmer is considering watering down plans to boost defence spending by GBP 18bln over concerns that they are unaffordable, according to The Times.

FX

- The Buck is lower this morning vs initially starting the European morning flat. Not really any geopolitical market-moving headlines overnight; however, the Buck was pushed lower after hawkish BoJ sources (see below). In terms of Fed speak since the close, Williams said he sees no obvious direction for rates and no reason to change them. Logan said higher rates could be needed later this year. Ahead, Daly, Bowman & Barkin are slated to speak.

- JPY is slightly firmer and trading in line with most G10s. Sources told Bloomberg and Reuters that the BoJ would raise rates at the June meeting, with the Bloomberg piece suggesting more tightening was possible in 2026. Markets assign 20bps of tightening in June (80% probability), with an additional 20bps implied by year-end. The BBG report saw a 35-pip move lower in USD/JPY over ten minutes, which ultimately proved fleeting, with Yen fundamentals remaining bearish and two hikes close to being fully priced this year. A strategist at SMBC Nikko Securities said: “Even if the BoJ raises rates in June, any rebound in the yen will be limited”. USD/JPY trades higher by 0.1%, a touch below the 160.00 mark.

- CHF is performing well against the Euro and Buck after CPI metrics from Switzerland. Although a cooler-than-expected report is unlikely to shift the dial for policymakers at the SNB. This is because the headline remains towards the lower half of the 0-2% target band, and the SNB continues to make clear that inflation meets its medium-term stability objective. As such, policy is expected to remain at the ZLB for the foreseeable future. EUR/CHF -0.1% at 0.9181, USDCHF -0.3% at 0.7896.

Central Banks

- Fed's Logan (2026 voter) said she is increasingly concerned higher interest rates could be necessary later this year and monetary policy is not restraining the economy, while she added that inflation is taking too long to return to 2%, economic activity remains strong and corporate earnings are 'going gangbusters'. Logan said financial conditions are accommodative, and the labour market is stable, but separately noted that the higher price of gas is feeding through to prices of other goods and services. Furthermore, she stated that mildly restrictive policy is needed and that the current monetary policy looks neutral or loose.

- RBA Governor Bullock said the RBA expects inflation to increase further in the near term and notes flow of data and development since May has not been materially different to our expectations. She notes that inflation is too high, and the board will do what it considers necessary to achieve its mandate of delivering price stability and full employment. Some signs of tightening impact already seen, but full effects to take 1 to 2 years.

- BoJ is said to mull a June rate hike with another possible in 2026 and sees less need to cut bond buys at the same pace in FY27, according to Bloomberg source reported. Reuters then corroborated this report.

Fixed Income

- Global fixed benchmarks are mixed as energy prices cool a touch after President Trump said Iran negotiations are going well, while he suggested a deal could happen over the weekend. Though noted that it could go another two or three weeks. Separately, reports suggest that Israel and Lebanon agreed to a ceasefire, though recent reports have suggested that the Israeli army is continuing its operations in the region. This uncertainty has led to the tentative action across fixed paper this morning.

- USTs (+4 ticks) are slightly firmer and trade within a narrow 109-12+ to 109-19+ range. Really not much driving the action this morning aside from geopolitics, but domestic data will likely garner some attention later. To recap, ISM Manufacturing & Services indicate a solid activity picture, with labour market reports (ADP/JOLTS) also pushing back on near-term rate cut expectations. Ahead, focus will be on: Jobless Claims (May/30), Revelio PLS (May), and Chicago Fed Labor Market Indicators Final (May).

- JGBs (-20 ticks) are on the back foot this morning for two key reasons: a) hawkish BoJ reports, b) an enhanced-liquidity auction. Delving into the report, Bloomberg first reported that the BoJ is mulling a hike in June, and potentially one more this year. Moreover, a source said that the Bank sees less need to pare back its bond purchasing plans. This was later corroborated by a Reuters piece, where a source said, “Unless there's a severe escalation in the conflict, the BOJ will probably hike rates in June”. Before the sources piece, markets already expected the Bank to hike in June; therefore, the pressure in JGBs this morning stems from comments related to the plans later in the year.

- Bunds and Gilts follow the tentative action seen in USTs, but are lower by a handful of ticks. Domestic updates for EZ have been lacking this morning, but traders will eye Retail Sales. Irrespective of the report, the ECB is set to hike at the June meeting – money markets assign a 96% chance of such a decision; another hike is then priced in for October.

- France sells EUR 13.998bln vs exp. EUR 12-14bln 3.70% 2036, 4.00% 2038, 3.60% 2042, 4.40% 2057 OAT.

- Spain sells EUR 4.973bln vs exp. EUR 4.5-5.5bln 2.35% 2029, 3.10% 2031 and 3.50% 2041 Bono and EUR 0.593bln vs exp. EUR 0.25-0.75bln 2.05% 2039 I/L Bono.

Commodities

- Crude markets are on a softer footing amid ongoing mediation efforts to broker some sort of US-Iran deal following two flare-ups earlier this week. In terms of the major updates, US President Trump said negotiations with Iran were progressing and suggested a deal could come within days, although talks could also continue for several more weeks. Meanwhile, US Secretary of State Rubio said the US is awaiting Iran’s final sign-off on negotiations surrounding Tehran’s nuclear programme. On the other side, Iranian officials outlined a four-stage framework for a potential agreement with the US. The four-stage proposal for a deal with the US includes: 1) Ending the war, 2) tangible measures re. the Strait, 3) sanctions and nuclear issues, 4) the establishment of a supervisory committee. More recently, Al Arabiya reported that the agreement on the release of frozen Iranian funds is in its final stages, albeit the search continues for a mechanism for frozen funds. The sources added that Trump informed the mediators of his refusal to release funds to Iran before signing the agreement. Elsewhere, Israel and Lebanon agreed to implement a US-brokered ceasefire framework and continue negotiations, although since the ceasefire, Hezbollah and IDF continued to exchange fire in the south of Lebanon.

- WTI Jul and Brent Aug futures are subdued in USD 94.06-95.91/bbl and USD 95.61-97.44/bbl ranges, respectively, at the time of writing, with fleeting downside seen on the aforementioned Al Arabiya sources. Dutch TTF ekes mild gains (+0.2%) but trades choppy on either side of EUR 49/MWh. “Positioning data for TTF continues to show that investment funds have been somewhat unfazed by ongoing LNG supply disruptions in the Middle East amid optimism over a resumption of LNG flows through the Strait of Hormuz”, analysts at ING write.

- Spot gold and silver are firmer after yesterday's losses, with the yellow metal finding support this morning at its 200 DMA (USD 4,423/oz) before rebounding to trade in a current USD 4,423-4,484/oz range. Spot silver trades in a USD 72.45-73.91/oz range, still some way off yesterday’s peak at USD 75.33/oz.

- Base metals are mostly lower amid the broader cautious risk tone. 3M LME copper ekes mild gains but remains under USD 14,000/t in a USD 13,701.13- 13,849.00/t at the time of writing.

- Russian Deputy PM Novak said Russia expects to reach its OPEC+ oil production quota this year. The oil market has not yet fully seen the consequences of the Middle East conflict, and stockpiles are being used. There has been no oil production lower than the start of the year due to “unscheduled maintenance” at refineries.

- Russian Deputy PM Novak said OPEC+ countries do not plan to share the UAE's oil output quota.

- Russia's Investment Fund Head Dmitriev said the EU is already going to make a number of concessions to Russia on energy as they need this for survival, TASS reported.

- China to lower retail gasoline prices by CNY 525 per metric ton from June 5th.

US Event Calendar

- 8:30 am: May 30 Initial Jobless Claims, est. 215k, prior 215k

8:30 am: May 23 Continuing Claims, est. 1780k, prior 1786k

- 8:30 am: Fed’s Barkin in Fireside Chat

- 10:00 am: Fed’s Bowman Testifies Before House Financial Services Committ

- 11:40 am: Fed’s Daly Appears on Bloomberg TV

- 1:00 pm: Fed’s Schmid Speaks in Fireside Chat

- 1:10 pm: Fed’s Daly at Bloomberg Technology Summit

DB's Jim Reid concludes the overnight wrap

The geopolitical headlines have become slightly more positive this morning, with oil prices falling back after the US said that Israel and Lebanon agreed to a ceasefire. That ceasefire is conditional on Hezbollah also stopping fighting, but in theory, the news helps to take out a key sticking point in the US-Iran talks that was holding up a deal. So that’s seen oil prices reverse a run of three consecutive gains, with Brent crude down -0.96% to $96.87/bbl. And given the news, the 10yr Treasury yield (-1.4bps) has also fallen back to 4.48%.

Nevertheless, even as the geopolitical news looks more positive, equities have taken a hit this morning after Broadcom’s forecast for AI chip revenue was beneath estimates, which pushed their share price down over -13% in overnight trading. Those concerns around AI have extended more broadly too, with S&P 500 futures down -0.37% this morning. And in Asia overnight, all the major indices have lost ground, including the Nikkei (-1.73%), the KOSPI (-1.17%), the Hang Seng (-1.39%), the CSI 300 (-0.58%) and the Shanghai Comp (-0.43%). Moreover, there’s been a broader slide in risk assets, with Bitcoin at a 3-month low this morning of $64,593.

Before that, markets had already struggled yesterday, as growing doubt about a US-Iran peace deal pushed Brent crude (+1.89%) up for a third consecutive session, closing at $97.81/bbl. And with the Strait of Hormuz still blocked and no clear sign of a resolution, there were even mounting expectations about a potential Fed rate hike this year, with market pricing for that up to 81% by the close. So that pushed bond yields higher, with a fresh dose of momentum from another round of strong US data, which added to the rate hike speculation. So it was a tough day all round, with the S&P 500 (-0.74%) finally ending a run of 9 consecutive gains, whilst the 10yr Treasury yield (+5.1bps) was back up to 4.49%.

In terms of the Middle East, events there were still dominating the market agenda, with few obvious signs that a peace deal was imminent. For instance, as we went to press yesterday, Bahrain said they’d intercepted three missiles and several drones, whilst Kuwait had to suspend air traffic briefly after an Iranian attack. Meanwhile, Iran’s foreign minister Abbas Araghchi posted that “Any hostile act will be met with an immediate, decisive response” and also said that “no tangible progress” had been made in talks with the US.

There was little clarity from Trump himself, who said the negotiations could complete over the weekend but could go on another two, three weeks. So tensions seemed to be ratcheting up again, and hopes for a durable peace deal continued to decline. Meanwhile, CNN reported yesterday that one of the key sticking points was monetary compensation for Iran. Otherwise, the US House of Representatives did vote against the Iran war in a 215-208 vote yesterday, after four Republicans joined with the Democrats. But in practice that won’t end the military conflict, as the Senate would also need to pass it, and Trump could issue a veto as well.

That backdrop meant that oil prices posted a fresh increase yesterday, with Brent crude up +1.89% to $97.81/bbl. Indeed, we can see from the Polymarket odds that there’s growing scepticism about a return to normality in the Strait of Hormuz. For instance, the probability of a return to normal traffic by the end of July was down to 34% yesterday, having been 39% the previous day. And it was clear investors were pricing the longer conflict scenarios as well, with the 6-month Brent crude future (+1.07%) up to $86.91/bbl.

With oil prices rising again, that led to a renewed bout of concerns around inflation on both sides of the Atlantic. For instance, the US 1yr inflation swap (+6.8bps) was back up to 3.18%, whilst the Euro 1yr inflation swap (+6.5bps) was up to 3.05%. So that led to a fresh round of pressure on sovereign bonds, with the 10yr Treasury yield (+5.2bps) up to 4.50%, whilst yields on 10yr bunds (+6.0bps), OATs (+7.7ps) and BTPs (+8.5bps) saw even bigger increases.

The rise in bond yields got even more momentum from another strong batch of US data, which added to expectations of a Fed rate hike this year. For example, the ISM services index rose by more than expected in May, up to 54.5 (vs. 53.8 expected). Moreover, we also had the ADP’s report of private payrolls, before the US jobs report tomorrow. That ADP release pointed to a robust labour market in May, with private payrolls up by a 16-month high of +122k (vs. +120k expected).

With that data in hand, the probability of a Fed rate hike by December was up to 81% at the close, up from 71% the previous day. And similarly in Europe, the number of ECB hikes priced by December was up to 68bps, up from 65bps the previous day. Meanwhile in Japan, markets have also priced in a growing chance of a rate hike, as BoJ Governor Ueda signalled in a speech yesterday that it may need to be considered. For instance, he said that if “upside risks to prices outweigh downside risks to economic activity, it will be necessary to thoroughly discuss the pros and cons of raising the policy interest rate”.

That combination of negative geopolitical headlines and more hawkish rates pricing meant US equities finally stumbled after a long run of gains. So the S&P 500 (-0.74%) and the NASDAQ (-0.89%) both fell back after 9 consecutive moves higher. The declines were fairly broad, with the equal-weighted S&P 500 (-0.42%) also seeing a decent pull back. But it was the Magnificent 7 (-1.25%) that saw a particular underperformance, dragging US equities more broadly, even as the Philly Semiconductor index (+1.39%) reached another record high.

Over in Europe, there were more broad-based equity declines, with the STOXX 600 (-0.66%) falling back, alongside losses for the DAX (-1.31%), the CAC 40 (-0.71%) and the FTSE MIB (-1.07%). But as in the US, the latest data also pointed in a slightly better direction than expected. So the final composite PMI for the Euro Area was revised up a point from the flash reading to 48.5. Admittedly, that was still beneath the 50-mark separating expansion from contraction, but it suggested the economy wasn’t deteriorating as rapidly as previously thought given the energy shock. Peter Sidorov published his latest global PMI monitor yesterday, where the data shows the global economy adapting to the energy shock, albeit with some signs of rising employment risks.

Looking at the day ahead now, data releases include the May construction PMIs for Germany and the UK, along with Euro Area retail sales for April, and the US weekly initial jobless claims. Otherwise, central bank speakers include ECB President Lagarde, BoE Governor Bailey, and the Fed’s Barkin, Bowman and Daly.

Tyler Durden

Thu, 06/04/2026 - 08:23

via Politico

via Politico

Source: The White House

Source: The White House

Constellation Energy’s Three Mile Island nuclear power plant near Middletown, Pa. The company’s plans to restart the plant’s Unit 1 were boosted when the Federal Energy Regulatory Commission approved a waiver for the company from PJM Interconnection rules on June 1, 2026.

Constellation Energy’s Three Mile Island nuclear power plant near Middletown, Pa. The company’s plans to restart the plant’s Unit 1 were boosted when the Federal Energy Regulatory Commission approved a waiver for the company from PJM Interconnection rules on June 1, 2026.

Recent comments