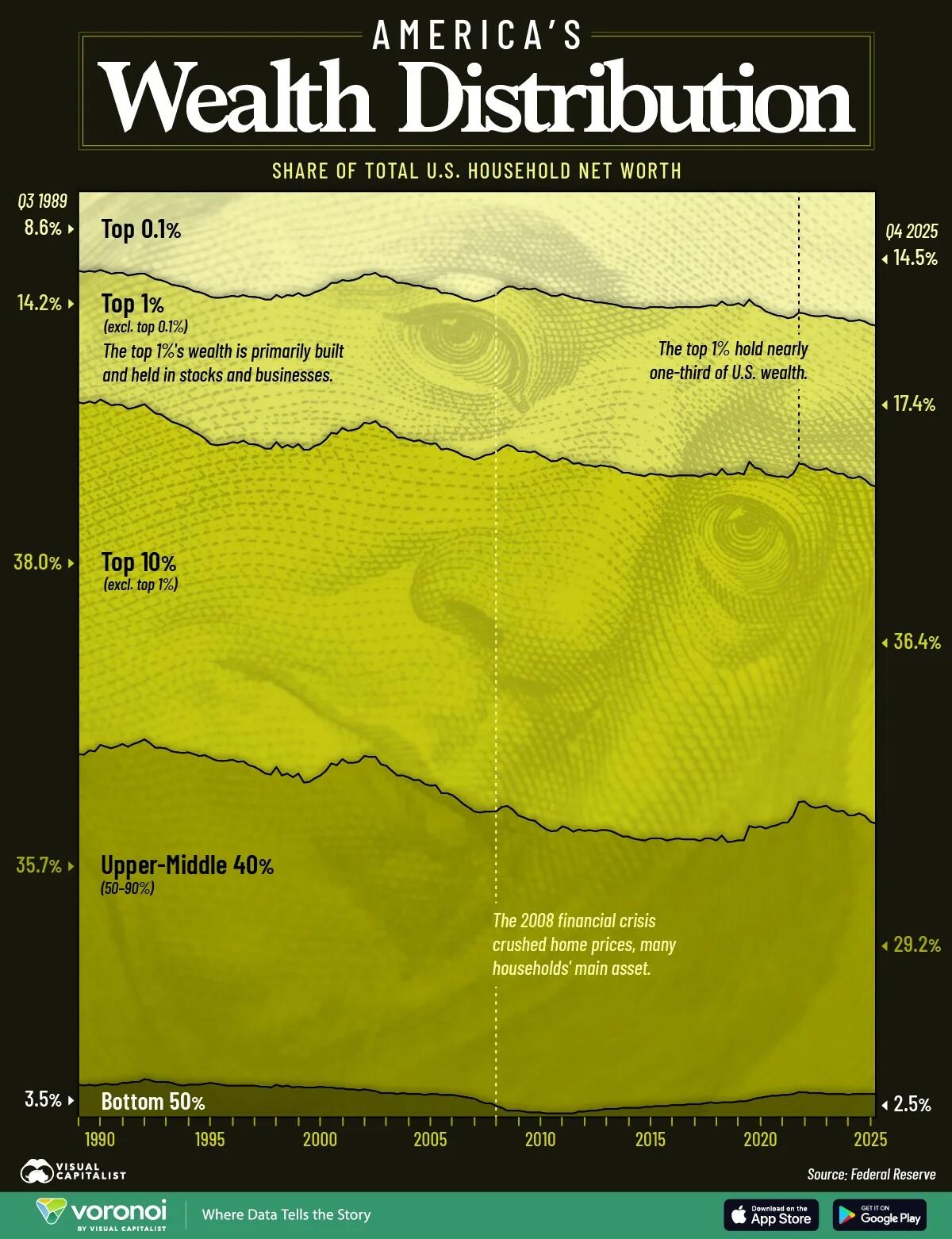

How America's Wealth Distribution Has Changed Over The Last 40 Years

Wealth reflects the value of everything households own, including homes, stocks, businesses, and savings, minus what they owe.

Because different wealth groups own very different mixes of assets, long-term market trends can reshape how the nation’s wealth is divided.

This graphic, via Visual Capitalist's Boyan Girginov, tracks how U.S. household wealth has shifted across wealth groups from Q3 1989 to Q4 2025 using data from the Federal Reserve’s Distributional Financial Accounts.

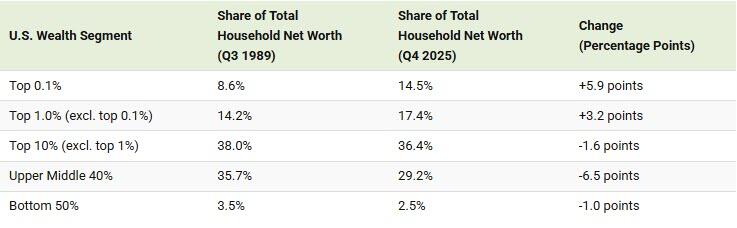

The table below shows how the wealth distribution has changed over the last 35 years:

The top 1% built its wealth primarily through stocks and businesses, assets that have soared in value for decades. In fact, every group below the top 1% has lost share since 1989: even the next 9% of households, from the 90th to 99th percentiles, slipped from 38.0% to 36.4%.

Wealth further down the ladder is tied mostly to the family home, which appreciates far more slowly than the stock market. Much of the bottom 50%’s net worth is home equity, and many households in that group have little or no net worth at all. That’s why the gap between the top and the bottom has widened over the last 36 years.

How Markets Move Each Group’s ShareMarket swings move each group’s share differently, depending on the assets its households own.

Every boom rewards whoever holds financial assets, and those gains compound: between 1989 and 2025, the top 0.1% increased its share of household wealth from 8.6% to 14.5%, while the top 1% as a whole climbed from 22.8% to 31.9%.

Busts fall hardest on those with the least cushion. The 2008 housing crash crushed the value of ordinary households’ main asset, and the bottom 50%’s share eventually fell to a record low of 0.4% before recovering to 2.5% today.

Over the full period, no group lost more ground than the upper-middle 40%, households between the 50th and 90th percentiles, whose share slid from 35.7% to 29.2% as home values trailed the stock market.

Wealth Distribution by Income Segment (1989-2025)See all the data for the last 36 years below:

Time Period Top 0.1% Top 1%(excl. top 0.1%) Top 10%

(excl. top 1%) Upper-Middle 40%

(excl. top 10%) Bottom 50% Q3 1989 8.6% 14.2% 38.0% 35.7% 3.5% Q4 1989 8.7% 14.2% 37.9% 35.7% 3.4% Q1 1990 8.6% 14.1% 37.7% 36.1% 3.5% Q2 1990 8.7% 14.2% 37.6% 36.1% 3.4% Q3 1990 8.5% 14.0% 37.3% 36.7% 3.5% Q4 1990 8.7% 14.1% 37.2% 36.4% 3.6% Q1 1991 8.9% 14.2% 37.0% 36.3% 3.5% Q2 1991 8.8% 14.2% 36.9% 36.5% 3.5% Q3 1991 8.8% 14.3% 36.6% 36.6% 3.7% Q4 1991 9.1% 14.4% 36.5% 36.3% 3.7% Q1 1992 9.0% 14.4% 36.3% 36.5% 3.8% Q2 1992 8.9% 14.3% 36.3% 36.7% 3.8% Q3 1992 8.9% 14.1% 36.2% 36.7% 4.1% Q4 1992 9.2% 14.3% 36.1% 36.4% 4.0% Q1 1993 9.5% 14.5% 36.1% 36.1% 3.8% Q2 1993 9.6% 14.5% 36.0% 36.1% 3.8% Q3 1993 9.8% 14.7% 35.7% 36.0% 3.8% Q4 1993 10.1% 14.8% 35.6% 35.8% 3.7% Q1 1994 10.2% 14.9% 35.5% 35.9% 3.5% Q2 1994 10.3% 15.0% 35.3% 35.9% 3.4% Q3 1994 10.5% 15.1% 35.0% 35.9% 3.5% Q4 1994 10.8% 15.2% 34.8% 35.7% 3.5% Q1 1995 10.9% 15.4% 34.7% 35.5% 3.5% Q2 1995 11.1% 15.6% 34.2% 35.5% 3.6% Q3 1995 11.4% 15.9% 33.9% 35.1% 3.7% Q4 1995 11.5% 15.9% 34.0% 34.9% 3.6% Q1 1996 11.5% 15.9% 34.2% 35.0% 3.5% Q2 1996 11.4% 15.9% 34.2% 35.1% 3.4% Q3 1996 11.3% 15.8% 34.3% 35.2% 3.4% Q4 1996 11.4% 15.8% 34.5% 35.0% 3.4% Q1 1997 11.2% 15.7% 34.6% 35.0% 3.4% Q2 1997 11.4% 15.9% 34.7% 34.6% 3.4% Q3 1997 11.4% 15.9% 34.8% 34.4% 3.4% Q4 1997 11.5% 16.0% 35.0% 34.2% 3.3% Q1 1998 11.7% 16.1% 35.1% 33.8% 3.3% Q2 1998 11.7% 16.1% 35.2% 33.8% 3.2% Q3 1998 11.2% 15.9% 35.1% 34.3% 3.5% Q4 1998 11.5% 16.2% 35.4% 33.6% 3.3% Q1 1999 11.2% 16.2% 35.5% 33.7% 3.4% Q2 1999 11.3% 16.4% 35.6% 33.5% 3.2% Q3 1999 11.0% 16.3% 35.6% 33.8% 3.3% Q4 1999 11.3% 16.6% 35.9% 32.9% 3.2% Q1 2000 11.2% 16.7% 35.9% 33.0% 3.2% Q2 2000 10.9% 16.6% 35.9% 33.4% 3.2% Q3 2000 10.7% 16.6% 35.8% 33.6% 3.3% Q4 2000 10.4% 16.4% 35.8% 34.2% 3.2% Q1 2001 9.9% 16.2% 35.7% 35.0% 3.2% Q2 2001 9.9% 16.3% 35.8% 34.9% 3.1% Q3 2001 9.6% 16.0% 35.8% 35.6% 3.1% Q4 2001 9.7% 16.2% 35.9% 35.3% 3.0% Q1 2002 9.6% 16.2% 36.0% 35.3% 3.0% Q2 2002 9.4% 16.2% 36.0% 35.5% 2.9% Q3 2002 9.0% 16.0% 36.0% 36.0% 3.0% Q4 2002 9.0% 16.1% 36.0% 36.0% 2.9% Q1 2003 8.8% 16.0% 36.2% 36.1% 2.8% Q2 2003 9.2% 16.2% 36.5% 35.5% 2.6% Q3 2003 9.2% 16.3% 36.5% 35.3% 2.6% Q4 2003 9.5% 16.5% 36.6% 34.8% 2.6% Q1 2004 9.9% 16.7% 36.5% 34.4% 2.5% Q2 2004 9.9% 16.7% 36.5% 34.3% 2.6% Q3 2004 10.0% 16.8% 36.5% 34.2% 2.5% Q4 2004 10.2% 16.8% 36.6% 33.9% 2.5% Q1 2005 10.2% 16.7% 36.7% 33.9% 2.5% Q2 2005 10.4% 16.8% 36.9% 33.6% 2.4% Q3 2005 10.5% 16.8% 36.9% 33.3% 2.5% Q4 2005 10.5% 16.7% 36.9% 33.3% 2.5% Q1 2006 11.0% 16.9% 37.1% 32.6% 2.4% Q2 2006 11.0% 16.8% 37.2% 32.6% 2.4% Q3 2006 11.1% 16.9% 37.3% 32.4% 2.4% Q4 2006 11.3% 16.9% 37.4% 32.0% 2.3% Q1 2007 11.6% 17.0% 37.6% 31.6% 2.2% Q2 2007 11.7% 17.0% 37.8% 31.3% 2.1% Q3 2007 11.9% 17.1% 38.0% 31.0% 2.0% Q4 2007 11.8% 17.0% 38.3% 31.2% 1.7% Q1 2008 11.6% 16.9% 38.5% 31.5% 1.5% Q2 2008 11.4% 17.0% 38.6% 31.5% 1.5% Q3 2008 11.2% 17.0% 38.9% 31.9% 1.2% Q4 2008 10.6% 17.1% 38.8% 32.5% 1.0% Q1 2009 10.3% 17.1% 39.0% 32.9% 0.7% Q2 2009 10.3% 17.3% 39.2% 32.5% 0.7% Q3 2009 10.6% 17.5% 39.4% 31.9% 0.7% Q4 2009 10.5% 17.6% 39.6% 31.8% 0.6% Q1 2010 10.6% 17.6% 39.7% 31.6% 0.5% Q2 2010 10.5% 17.6% 39.9% 31.5% 0.5% Q3 2010 10.8% 17.7% 40.0% 31.0% 0.5% Q4 2010 11.0% 17.8% 40.1% 30.7% 0.4% Q1 2011 11.3% 17.9% 40.0% 30.5% 0.4% Q2 2011 11.3% 17.8% 39.9% 30.5% 0.4% Q3 2011 11.1% 17.7% 39.8% 31.0% 0.4% Q4 2011 11.3% 17.7% 39.8% 30.8% 0.4% Q1 2012 11.5% 17.9% 39.7% 30.4% 0.4% Q2 2012 11.6% 17.8% 39.6% 30.5% 0.6% Q3 2012 11.8% 17.8% 39.5% 30.3% 0.6% Q4 2012 11.8% 17.8% 39.4% 30.3% 0.7% Q1 2013 12.0% 17.8% 39.4% 30.2% 0.7% Q2 2013 12.0% 17.6% 39.4% 30.2% 0.8% Q3 2013 12.1% 17.6% 39.3% 30.1% 0.9% Q4 2013 12.2% 17.6% 39.4% 30.0% 0.9% Q1 2014 12.3% 17.7% 39.4% 29.7% 0.9% Q2 2014 12.5% 17.9% 39.3% 29.3% 1.0% Q3 2014 12.5% 17.9% 39.3% 29.3% 1.0% Q4 2014 12.6% 18.0% 39.4% 29.1% 1.0% Q1 2015 12.6% 18.0% 39.3% 28.9% 1.0% Q2 2015 12.7% 18.1% 39.4% 28.8% 1.1% Q3 2015 12.5% 18.0% 39.4% 29.0% 1.1% Q4 2015 12.5% 18.1% 39.3% 28.9% 1.2% Q1 2016 12.5% 18.1% 39.3% 28.9% 1.2% Q2 2016 12.6% 18.2% 39.4% 28.7% 1.2% Q3 2016 12.6% 18.2% 39.2% 28.7% 1.3% Q4 2016 12.5% 18.2% 39.2% 28.8% 1.3% Q1 2017 12.5% 18.2% 39.3% 28.7% 1.3% Q2 2017 12.5% 18.2% 39.3% 28.6% 1.4% Q3 2017 12.5% 18.2% 39.3% 28.6% 1.4% Q4 2017 12.5% 18.3% 39.3% 28.4% 1.4% Q1 2018 12.4% 18.2% 39.3% 28.6% 1.5% Q2 2018 12.3% 18.2% 39.4% 28.5% 1.6% Q3 2018 12.4% 18.3% 39.5% 28.4% 1.5% Q4 2018 11.9% 18.1% 39.6% 28.8% 1.6% Q1 2019 12.3% 18.3% 39.7% 28.1% 1.6% Q2 2019 12.3% 18.3% 39.7% 28.2% 1.6% Q3 2019 12.1% 18.3% 39.7% 28.2% 1.7% Q4 2019 12.4% 18.2% 39.5% 28.2% 1.7% Q1 2020 11.7% 17.5% 39.3% 29.6% 1.8% Q2 2020 12.3% 17.6% 38.9% 29.3% 2.0% Q3 2020 12.5% 17.5% 38.6% 29.3% 2.1% Q4 2020 13.0% 17.6% 38.3% 29.0% 2.2% Q1 2021 13.2% 17.5% 37.9% 29.1% 2.3% Q2 2021 13.4% 17.4% 37.6% 29.2% 2.3% Q3 2021 13.5% 17.3% 37.4% 29.4% 2.4% Q4 2021 13.7% 17.2% 37.2% 29.4% 2.4% Q1 2022 13.6% 16.9% 36.9% 30.1% 2.5% Q2 2022 13.1% 16.3% 36.5% 31.3% 2.7% Q3 2022 13.2% 16.3% 36.4% 31.4% 2.7% Q4 2022 13.4% 16.5% 36.5% 31.0% 2.6% Q1 2023 13.5% 16.6% 36.5% 30.8% 2.6% Q2 2023 13.5% 16.6% 36.4% 30.9% 2.6% Q3 2023 13.4% 16.5% 36.4% 31.1% 2.5% Q4 2023 13.6% 16.7% 36.5% 30.7% 2.5% Q1 2024 13.7% 16.8% 36.5% 30.5% 2.5% Q2 2024 13.7% 16.8% 36.4% 30.6% 2.5% Q3 2024 14.0% 16.9% 36.5% 30.2% 2.4% Q4 2024 14.0% 17.0% 36.4% 30.1% 2.5% Q1 2025 13.9% 16.9% 36.4% 30.3% 2.5% Q2 2025 14.1% 17.1% 36.4% 30.1% 2.5% Q3 2025 14.4% 17.3% 36.4% 29.4% 2.5% Q4 2025 14.5% 17.4% 36.4% 29.2% 2.5%

If you enjoyed today’s post, check out The Global Wealth Pyramid in 2025 on Voronoi.

Tyler Durden Wed, 07/08/2026 - 05:45

via Associated Press

via Associated Press

Anadolu Agency

Anadolu Agency

Here's how modern interceptor missiles protect against aircraft, cruise missiles, and ballistic threats.

Here's how modern interceptor missiles protect against aircraft, cruise missiles, and ballistic threats.

via Reuters

via Reuters

Recent comments