"Approaching Unheard Of Inventory Levels": Exxon, Chevron Issue Apocalyptic Warning About What Happens Next To Oil

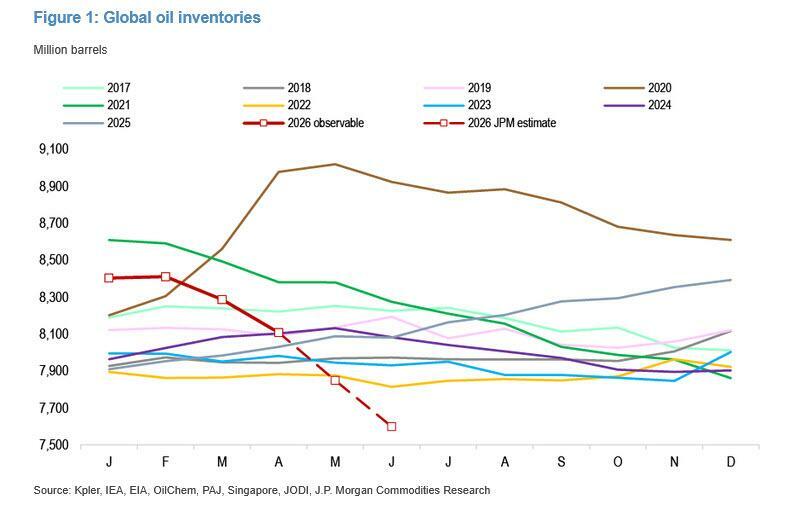

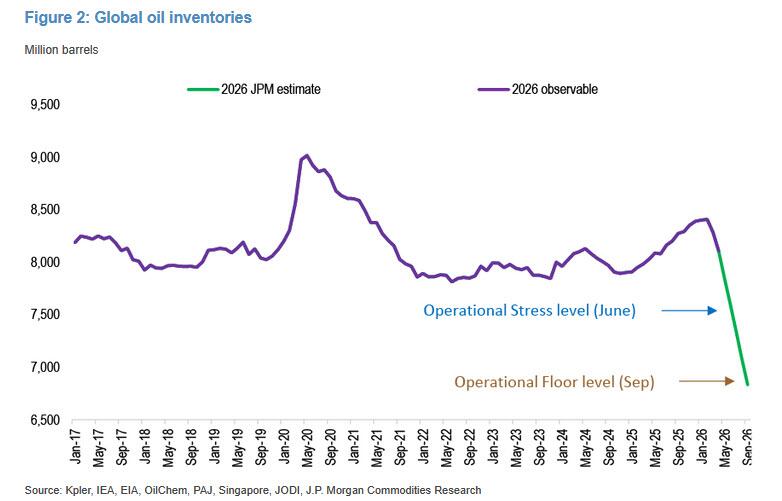

Just about two months ago, JPMorgan did the math on "How Long Before The World Hits Crude Oil Operational Minimum." The punchline was that while the market can hold hundreds of millions of barrels, it would still become fragile once working stocks fell too low. Like blood pressure in the human body, the issue is circulation.

Then, approximately 4 weeks later, the bank followed up this analysis with some more math, explaining "Why Hormuz Will Reopen By September... One Way Or Another." The bank calculated that of the 8.4 billion barrels in global oil inventories at the start of 2026, only 0.8 billion barrels were realistically available without pushing the system into operational stress. Long story short (and the long story can be found here), OECD commercial stocks could fall to operational stress levels by June, and then hit the global operational floor by September if the Strait of Hormuz remains closed, assuming demand destruction stabilized at 5.5 mbd (with oil prices paradoxically dropping since the last JPM article, demand destruction has actually slowed).

Meanwhile, the biggest paradox during this period when the blocked Hormuz Strait meant that roughly 10 million barrels of oil wasn't reaching its intended destination each day, was that instead of prices going sharply higher to destroy demand, oil prices were actually dropping after peaking in late March and then again a month later, in effect incentivizing more demand. This prompted JPMorgan to published that "Something Is Off" With The Global Oil Math...

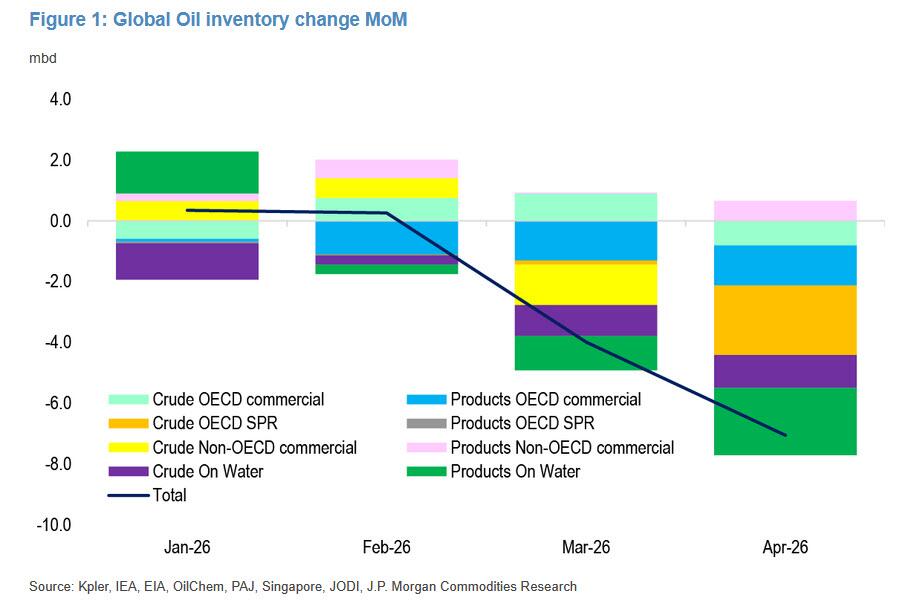

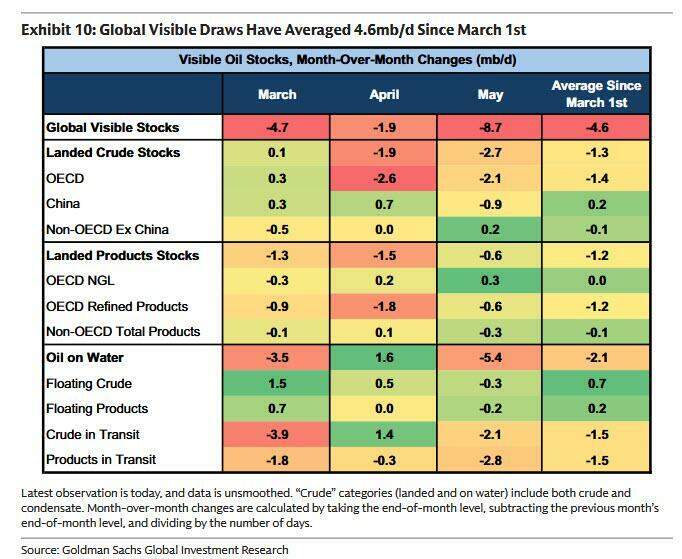

... and Goldman to follow up a few weeks later by observing that in May, global oil inventories plunged by a record 8.7 million barrels per day, with Hormuz still largely blocked.

And yet, oil prices are sharply lower in May, in no small part due to the daily market jawboning manipulation by various official and unofficial sources, who signal that an Iran deal is imminent... any minute now.

Only it isn't, and while the market may prefer to shove its head in the sand, the biggest names in the room are no longer keeping quiet.

Today, Chevron CEO Mike Wirth warned oil prices are likely to rise over the next two months as already near record low crude inventories continue to decline due to the Iran war.

“The buffers and the shock absorbers are being steadily drawn down, and the ability for the market to absorb this imbalance is drastically diminished today versus where we started,” he said at a Bernstein conference on Thursday.

“Over the next few weeks, we’re likely to see those pressures flow through more directly to physical prices and there’s more upwards pressure that I would expect as we get into June and certainly into July.”

Wirth’s comments follow a 10% fall in oil prices over the past week amid optimism that the US and Iran can agree a deal to end the three-month-long conflict that has closed the Strait of Hormuz, a narrow waterway through which a fifth of crude flows. They highlight growing concern among economists that the war’s impact on energy prices will continue to be felt for many months after any deal is agreed to end it... not that that moment is even remotely close. The conflict has removed 12mn-13mn barrels of oil a day from global markets.

The comments by Wirth echo a growing chorus of warnings from other oil executives, including the head of the United Arab Emirates state oil group Adnoc, who cautioned last week that full oil flows through the Strait of Hormuz were unlikely to return before next year even if the conflict is resolved.

“It will take at least four months to get back to 80% of pre-conflict flows, and full flows will not return before the first or even second quarter of 2027,” Adnoc chief executive Sultan al-Jaber said during an Atlantic Council event on May 21.

Echoing JPMorgan's observations, Wirth said oil prices had not risen as much as people had expected due to higher-than-normal stocks of crude prior to the outbreak of the war, releases from the US Strategic Petroleum Reserve and flows of sanctioned oil from Iran, Russia and Venezuela. But he said these stocks were now running low. One wildcard is the rapid, yet very stealthy, drain of Chinese stocks, both commercial and strategic. With 1.4 billion in China's SPR, the moment of reckoning could be delayed yet again if Beijing decides to open the floodgates.

Wirth also said the energy crisis would force governments to focus more on “an insurance policy” by building up oil reserves to insulate them from shocks such as the pandemic and wars in Iran and between Russia and Ukraine. “The likelihood that another shock is around the corner is something policymakers are going to have to bear in mind . . . how long they want to roll the dice before they refill inventories is a question that I think we’re going to see policymakers have to grapple with.”

“That’s going to put more demand into the market, which is going to put a bit of additional tension on the price,” he said.

The Chevron boss concluded by warning that damage to oil and gas infrastructure in the Middle East would cost tens of billions of dollars to repair, putting additional upwards pressure on prices. “If this goes on for long, it tips us into an economic slowdown or a recession, you might have an offset on the demand side, which you can’t rule out.”

But if Chevron was pessimistic, the company's biggest domestic competitor, Exxon, was downright apocalyptic. Speaking at the same Bernstein conference, Exxon SVP Neil Chapman had some truly horrifying remarks, certainly not something that Donald Trump would like to hear. We present them below.

Commercial inventories of crude oil, of liquids, think petroleum, gasoline, diesel, jet fuel, they've all run down. And running down those inventories has mitigated or offset, supplemented by the release of strategic petroleum reserves, which most of the Western countries have done. All of that has mitigated the impact. You can model this. We've modeled it. I think a lot of people in the industry have modeled it.

Nothing new here: we've discussed all this in the previous three months. But it is what he said next that was a moment of shocking insight into just how bad things are about to get:

We're approaching unheard of inventory levels. I mean, really, really low levels. You can debate whether that's going to hit those really low levels in two weeks or three weeks. Once you get to that point, then you'll see price shoot up. A model would say dated Brent will shoot up. Once you get to that really low inventory level, up to $150, $160.

The models would tell you that. And then what happens is when the price gets to a certain level, demand destruction brings it back into balance. Prices go so high, it becomes unaffordable. And that's what happens. And so we're at that level right now.

Next, Chapman connected all the abovementioned dots: "I think crude being in this sort of $90 to $110 for the last whatever it is, six weeks, has really been mitigated by running down inventories. It can't last forever. So we'll see what happens.... predicting this and the exact timing, it's always a challenge. But that's the way we see the picture."

Putting all of the above in simple terms: by playing a jawboning game of cat and mouse with oil markets, the Trump administration is only draining stocks, both commercial and strategic, faster as consumers can afford to buy more, and they do. However, the supply sid of the pipeline remains blocked.

And until the war in Iran truly ends, and the Strait returns to normal transit, global inventories will continue to drain by about 10-14 million per day. Which is why when the operational floor is reached in less than three months, the resulting parabolic move in oil will be just as memorable as when it plunged deep into negative territory in April 2020 when traders were paying others any amount asked, to take physical oil off their hands. It will be just like that... only in reverse.

Tyler Durden Fri, 05/29/2026 - 08:00

The concept of floating nuclear power plants is not new. (Representational image)

The concept of floating nuclear power plants is not new. (Representational image) South African President Cyril Ramaphosa speaks to lawmakers in parliament, in Cape Town, South Africa, May 14, 2026

South African President Cyril Ramaphosa speaks to lawmakers in parliament, in Cape Town, South Africa, May 14, 2026 Wegovy at a pharmacy in London on March 8, 2024. Hollie Adams/Reuters

Wegovy at a pharmacy in London on March 8, 2024. Hollie Adams/Reuters Overweight people walk through the city center in Glasgow, Scotland, on Oct. 10, 2006. Jeff J. Mitchell/Getty Images

Overweight people walk through the city center in Glasgow, Scotland, on Oct. 10, 2006. Jeff J. Mitchell/Getty Images

via Associated Press

via Associated Press

US President Donald Trump walks towards the Rose Garden for a "Rose Garden Club" dinner in honor of Police Week at the White House in Washington, DC, on May 11, 2026. Photo by Kent NISHIMURA / AFP via Getty Images

US President Donald Trump walks towards the Rose Garden for a "Rose Garden Club" dinner in honor of Police Week at the White House in Washington, DC, on May 11, 2026. Photo by Kent NISHIMURA / AFP via Getty Images A woman casts her mail-in vote at an official ballot drop box in Washington on Nov. 5, 2024. Madalina Vasiliu/The Epoch Times

A woman casts her mail-in vote at an official ballot drop box in Washington on Nov. 5, 2024. Madalina Vasiliu/The Epoch Times

U.S. Trade Representative Jamieson Greer speaks during a tour of the Atomic Industries manufacturing facility in Warren, Mich., on April 9, 2026. AP Photo/Julia Demaree Nikhinson

U.S. Trade Representative Jamieson Greer speaks during a tour of the Atomic Industries manufacturing facility in Warren, Mich., on April 9, 2026. AP Photo/Julia Demaree Nikhinson

Recent comments