Trump: Iran Deal Should Be Done 'Pretty Quickly' But 'Subject To Settling' Over Next Few Days

Summary

- Trump Talks Endgame In Iran: Says 'we'll have a signing very soon.'

- TACO SEASONING: Trump tells NY Post that Iran deal "pretty much all wrapped up," but FARS news agency says no deal has been approved.

- TACO: Trump Cancels Strikes After All Day Bluster About 'Bigger' Strikes on Iran Tonight (shocking TACO!)

- Iran Parliament Speaker Ghalibaf says "Wrong strategies and impulsive decisions will reset the entire board for the worse, explode energy infrastructure and markets & create an endless quagmire that you will be stuck in for years."

- Trump follows with mention of "bigger, more powerful" bombing of Iran tonight. He pledged "they're finished".

- Trump announces intent to hit the Iranians "VERY HARD TONIGHT" (surely there will be no TACO?)

//-->

//-->

//-->

Trump Says Deal Imminent

President Donald Trump announced Thursday evening that he had cancelled scheduled U.S. strikes and bombings against Iran, citing rapid progress on a U.S.-Iran memorandum of understanding (MOU) aimed at extending a fragile ceasefire and launching formal negotiations on Tehran’s nuclear program. In a Truth Social post and a phone interview with the New York Post, Trump said the agreement was “pretty much all wrapped up,” with documents at a “fairly final stage.” He added that he had spoken with Israeli Prime Minister Benjamin Netanyahu and claimed the deal had received approval at the highest levels in Iran and from multiple regional players, including Saudi Arabia, the UAE, and others. The U.S. naval blockade of Iranian ports will remain in place until the deal is signed, with time and location of the signing to be announced shortly.

US x Iran permanent peace deal by June 30, 2026?

Yes 17% · No 84%

View full market & trade on Polymarket

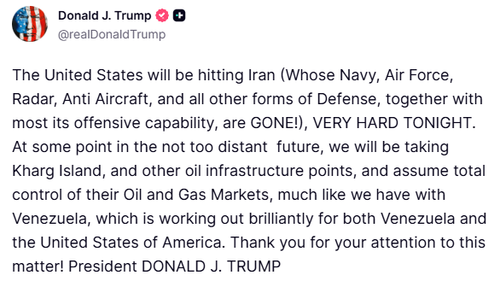

The Israeli Prime Minister’s Office later confirmed that Trump spoke with Netanyahu this evening specifically about the emerging MOU. According to the readout, Netanyahu expressed appreciation for Trump’s commitment that any final agreement would require the removal of enriched nuclear material, dismantling of enrichment infrastructure, limits on missile production, and an end to Iran’s support for terrorist proxies - even though Israel is not a direct party to the MOU. Earlier in the day, Trump had sharply escalated rhetoric by threatening to seize Iran’s key oil-export hub at Kharg Island and hit Iran “very hard,” a move widely seen as leverage that may have accelerated the diplomatic opening.

"President Trump spoke this evening with Prime Minister Netanyahu regarding the emerging memorandum of understanding (MOU) with Iran to enter into negotiations," the PM's office wrote on X. "Even though Israel is not a party to the memorandum of understanding, the Prime Minister expressed his appreciation for President Trump's commitment that the final agreement at the conclusion of negotiations will include the removal of enriched material, the dismantling of enrichment infrastructure, limits on missile production, and the cessation of Iran's support for its terrorist proxies in the region."

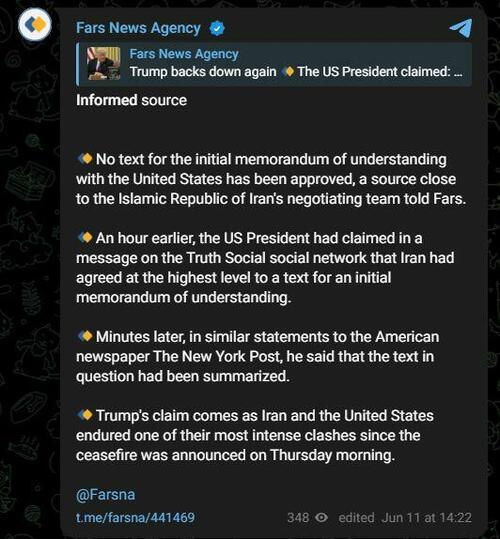

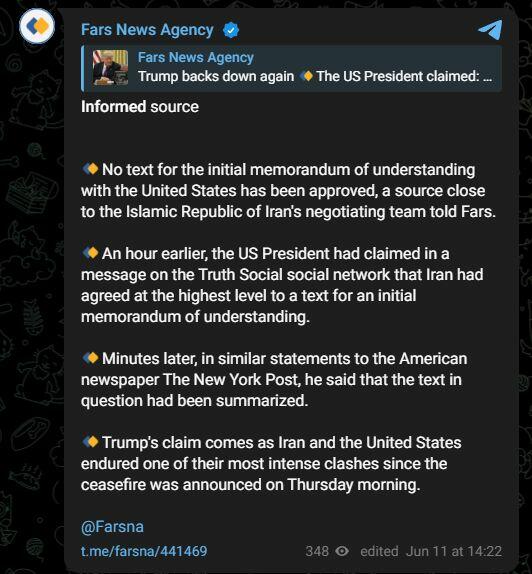

Iranian state media, including Fars News Agency, quickly pushed back, stating that no final MOU text had been approved. Some Israeli officials also indicated they had not been briefed on a finalized deal. Markets reacted positively in the short term, with U.S. stocks rising and oil prices falling on hopes of de-escalation. The developments remain fluid, with both sides continuing to trade public signals amid ongoing regional tensions.

Via Telegram

Via Telegram

And of course, oil:

Trump Claims Iran Deal 'Pretty Much All Wrapped Up' - FARS Says No Text Approved

President Trump told the New York Post in a phone interview that the US-Iran agreement is "pretty much all wrapped up," claiming high-level approval and announcing he has called off further strikes on Iran.

Iranian state media immediately pushed back. Fars News Agency, citing a source close to Iran’s negotiating team, stated that no text for the initial memorandum of understanding with the United States has been approved.

The dueling statements reflect the familiar pattern in these negotiations: the US side projecting near-completion while Iranian officials emphasize that no final text has received leadership approval. This comes amid ongoing indirect mediation efforts, including Qatari involvement.

* * *

Trump Cancels Strikes After All Day Bluster About 'Bigger' Strikes on Iran Tonight

TACO Thursday... Trump again backs off prior repeat vows. He's been threatening since last night that he'll "bomb the shit" out of Iran, and followed by specifically saying this morning that 'bigger airstrikes' would come tonight. It's after 9pm in Iran and there's been nothing yet.

And now the president is saying he's canceled the planned strikes altogether. He's saying this is due to "discussions" at the highest level with Iranian leadership. But Tehran has rejected that it's engaged with talks. One side or the other is lying. Might the following from CNN have some direct bearing on this sudden reversal in intentions?

Energy executives have warned the White House that key oil reserves being used to limit the Iran war’s impact on prices are running dangerously low, via CNN citing sources.

Stocks surging, oil dumping...

Oil plunges after the bombshell Truth Social reversal and sudden de-escalation in US military posture from the Commander-in-Chief:

US Still Holding Israel Back

This is another latest sign Washington is still looking for an off-ramp through negotiations. Trump is hoping to push Iran back into talks through bombing, which thus far hasn't worked (since even the opening days of Epic Fury). According to the latest reporting out of Israel's public broadcaster Kan News:

Ghalibaf to US: "Endless quagmire that you will be stuck in for years."

Iran Parliament Speaker Ghalibaf says "Wrong strategies and impulsive decisions will reset the entire board for the worse, explode energy infrastructure and markets and create an endless quagmire that you will be stuck in for years."

He's seizing on the lessons of Bush's Afghan and Iraq wars, which the media and history books have long looked critically on as 'forever wars'. There's also the general war-weariness among the American public, also as the Russia-Ukraine war is in its fifth year. This is Tehran again counter-signaling that there is no imminent deal or even so much as forward-moving negotiations to speak of.

Meanwhile, the Pentagon is pushing back against Iran's assertion that it has again locked down international shipping transit in the Strait of Hormuz:

And more from Trump on from bad to worse escalatory 'options':

Trump on Fox News: "My preference has always been to take Kharg Island. I don't know that America has the stomach for it, to be honest."

Trump: 'Bigger, More Powerful' Bombing Tonight

President Trump follows on the heels of vowing to hit Iran "very hard tonight" with some further words revealing his thinking in a morning Fox News interview. Trump has promised a "bigger, more powerful" bombing of Iran. "They have no defense," he said, and pledged "they're finished". But be again lambasted the media for not saying that they are actually "finished".

He explained that if needed, US troops can be used to "take over the whole place" - but still expressed he doesn't desire to put US American forces on the ground.

Separately, CNN has cited US admin officials who suggest that a move to capture Kharg Island is an "endgame" strategy option. So this suggests its low on the White House agenda, after Trump earlier hinted that this could be done.

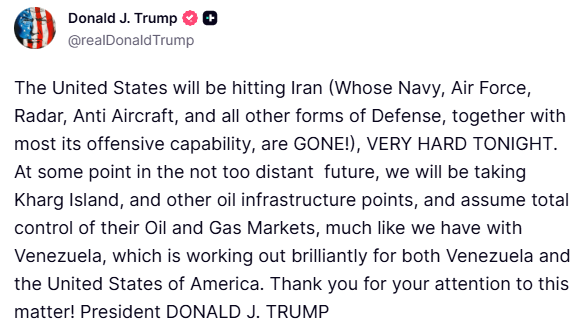

Trump: Will Be Hitting Iran Very Hard Tonight

After already issuing an ultimatum the evening prior, President Trump has just announced his intent to launch a second consecutive night of direct missile attacks on Iran. He's vowing to hit the Iranians "VERY HARD TONIGHT".

He also just renewed prior threats to 'take' Kharg Island and 'other oil infrastructure points' in the not too distant future.

The Thursday morning Truth Social post previewing the next escalation in this war resulted in a spike in oil prices:

US Attack Renders Ceasefire 'Meaningless'

Overnight, there did not appear to be any new major exchanges of fire after Iran launched retaliatory strikes on US bases in Kuwait, Bahrain and Jordan - following the US bombing of some dozens of targets in Iran earlier, in the wake of the downing of a US Apache attack helicopter in the Hormuz area earlier this week.

But since then, Iran has announced it is closing the Strait of Hormuz - or rather seeking to tighten its grip with the likelihood of more aggressive attacks on international and 'unauthorized' tankers to come. Iran had also struck US bases in Kuwait, Bahrain, and Jordan - according to its statements as well as emerging open source material.

The most important new statement to come out of Tehran is the Iranian Foreign Ministry's charge that the US attacks "rendered the ceasefire dated April 8, 2026 effectively meaningless" and that the US will be held responsible for the "consequences". The formal statement also urged regional Arab stated to not allow American forces to use their territories.

Day 104: Return to Regional Airspace Closures

It is day 104 of the enduring conflict, with active war having newly erupted again, and so we are seeing airspace closures over the region once again, with Kuwait confirming flight diversions amid a temporary airspace closure.

Aerial alerts have also been issued for Jordan.

A slew of new videos have emerged showing missile intercepts, with US Patriot batteries active, over areas from Kuwait to Bahrain to Jordan - however, the United Arab Emirates (UAE) interestingly continues to be sparred from Iran's wrath and retaliation.

Scope of US Attack & Iran's Military Response

As for the latest of what's confirmed in the wake of the prior day's major US attacks on Iran, which involved over 40 Tomahawk missiles fired, Al Jazeera has the following summary and review of the situation:

- US strikes on Iran: US Defense Secretary Pete Hegseth confirmed that Washington was launching strikes on “key facilities” in Iran, saying the attacks were part of attempts to secure a permanent ceasefire. Speaking outside CENTCOM headquarters in Tampa, Florida, Hegseth said President Donald Trump had ordered Iran to be hit “hard” and warned the strikes could continue for a second consecutive night if necessary.

- Strait of Hormuz closed: In response to the latest attacks, Iran’s top military command announced the complete closure of the Strait of Hormuz, one of the world’s most critical oil transit routes. Officials warned all vessels to stay away from the strategic waterway, saying any ships attempting to pass through could come under attack.

- Water services restored: Authorities in Iran’s Hormozgan province said water supplies had been restored to affected communities in Sirik county less than 12 hours after US strikes damaged infrastructure. Iranian media reported that two concrete water storage reservoirs were hit in the attacks. A New York Times analysis suggested the tanks may have been struck with precision-guided munitions, raising concerns as international humanitarian law considers civilian water infrastructure a protected site.

- Tehran reacts to renewed fighting: Reporting from Tehran, Al Jazeera’s Mohamed Vall said many Iranians had been expecting another US attack despite renewed talk of negotiations. “They have been waiting and expecting a surprise American attack,” Vall said, adding that Tehran retaliated by striking US bases in Kuwait and Bahrain, according to military commanders. The latest exchanges mark another night of direct confrontation after both sides had suggested the previous round of attacks had come to an end.

Below: Iran releases video showing this its latest missile launches targeting US bases in the Middle East:

'Tomorrow Night' Warning

President Trump is again trying his hand at forcing Iran to negotiate and capitulate through bombing, most recently warning in a statement to Fox News that if Iran does not accept a US deal, it would come under American fire power once again "tomorrow night" -- so the clock is ticking Thursday, apparently.

While Trump claimed the Iranians had contacted Washington, urging a halt to the attacks, Tehran leadership has rejected that this actually happened. The whole situation is somewhat of a return to the same stalemated reality of the opening days and weeks of Operation Epic Fury.

Third Tanker this Week Disabled by US Forces

In the Gulf of Oman, US forces have reportedly disabled another oil tanker charged with 'violating the blockade' put into place by the US Navy. This marks the third commercial vessel disabled by American forces this week. According to a fresh CENTCOM description of the action:

U.S. forces disabled an oil tanker in the Gulf of Oman at 11:20 p.m. ET on June 10 after the vessel violated the blockade against Iran by attempting to transport Iranian oil, marking the third commercial ship disabled by American forces this week.

U.S. Central Command (CENTCOM) acted against Guinea-Bissau flagged M/T Jalveer as it attempted to transport oil from Iran through the Gulf of Oman. A U.S. aircraft fired two Hellfire missiles into the ship’s engine room after the crew repeatedly failed to comply with directions from U.S. forces.

Earlier this week, U.S. aircraft disabled Palau-flagged vessels M/T Marivex and M/T Settebello on Monday and Tuesday, respectively. Marivex violated the blockade by attempting to sail to an Iranian port and Settebello attempted to transport Iranian oil.

In total: U.S. forces have disabled 9 non-compliant vessels since initiating the blockade of Iran's ports on April 13.

Claims of Ongoing Indirect Talks

Bloomberg reports early Thursday:

Qatar negotiators depart Tehran after talks on US, Iran: diplomat to AFP

Some regional media, such as Al Arabiya, are reporting that negotiations between Tehran and Washington are ongoing (likely only indirectly, if at all) - though there hasn't been official confirmation of this from the Islamic Republic side at all. Instead, they are calling even the extended ceasefire itself 'meaningless'.

According to the latest communication, Iran's Defense Ministry says the country will not back down in the face of threats or pressure, with the national armed forces remaining on high alert, ready to inflict retaliation and punishment.

Tyler Durden

Thu, 06/11/2026 - 15:44

Via

Via

Destruction caused by the Palisades Fire near Los Angeles on Jan. 9, 2025. John Fredricks/The Epoch Times

Destruction caused by the Palisades Fire near Los Angeles on Jan. 9, 2025. John Fredricks/The Epoch Times A firefighter battles the Palisades Fire as it burns homes on the Pacific Coast Highway during a powerful windstorm in Los Angeles on Jan. 8, 2025. The wildfire lasted for 24 days, resulting in the deaths of 12 residents, forcing thousands to evacuate their homes, and rendering entire neighborhoods uninhabitable. Apu Gomes/Getty Images

A firefighter battles the Palisades Fire as it burns homes on the Pacific Coast Highway during a powerful windstorm in Los Angeles on Jan. 8, 2025. The wildfire lasted for 24 days, resulting in the deaths of 12 residents, forcing thousands to evacuate their homes, and rendering entire neighborhoods uninhabitable. Apu Gomes/Getty Images

Undated handout file photo issued by the US Department of Justice (left-right) of the former Duke of York, Virginia Giuffre, and Ghislaine Maxwell.

Undated handout file photo issued by the US Department of Justice (left-right) of the former Duke of York, Virginia Giuffre, and Ghislaine Maxwell.

via Reuters

via Reuters

Recent comments