A Lot More Than Just Rates Moving Markets

By Peter Tchir of Academy Securities

The plan this weekend was to write about the AI Revolution. It would have dovetailed well with recent pieces Buggy Whips and Horses and Being Forced to Understand UBI. We discussed this, Iran, and much more on Bloomberg TV (1:43:30 mark), where I did bring out the red rocket ship tie, in honor of the SpaceX IPO.

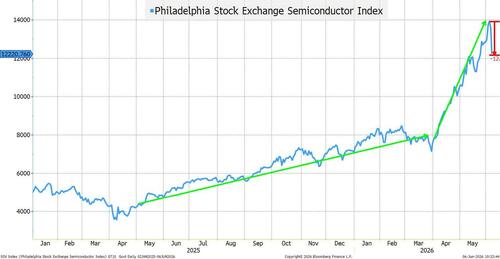

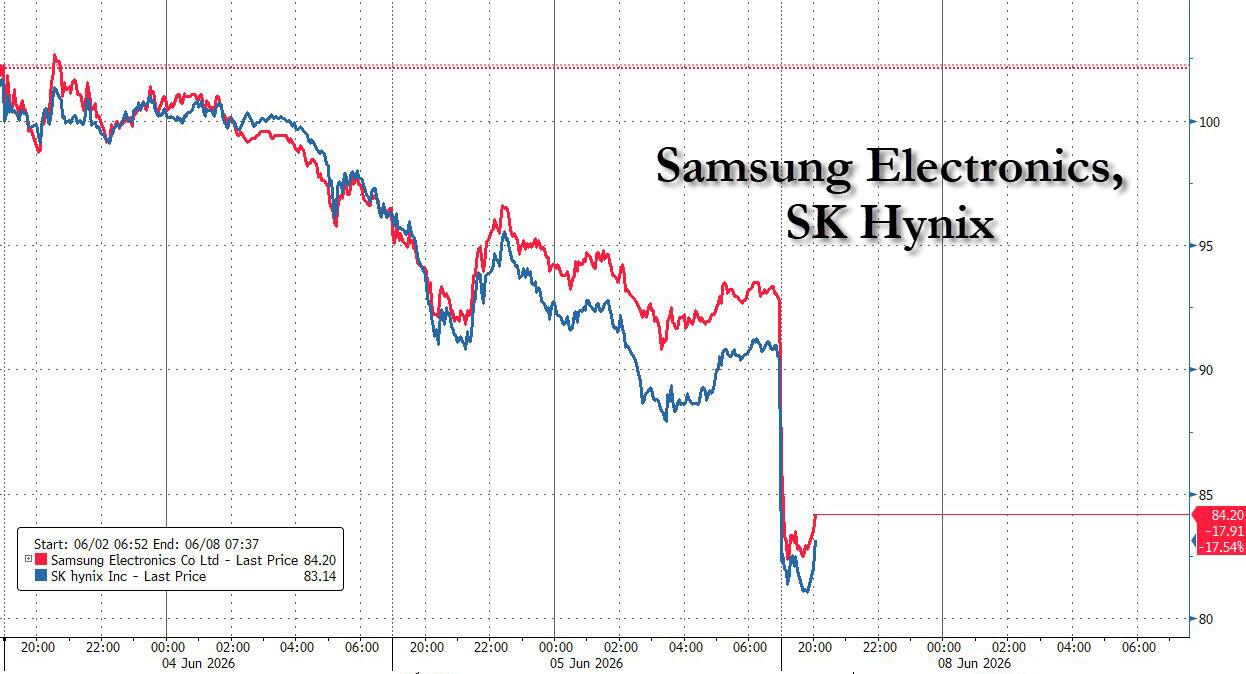

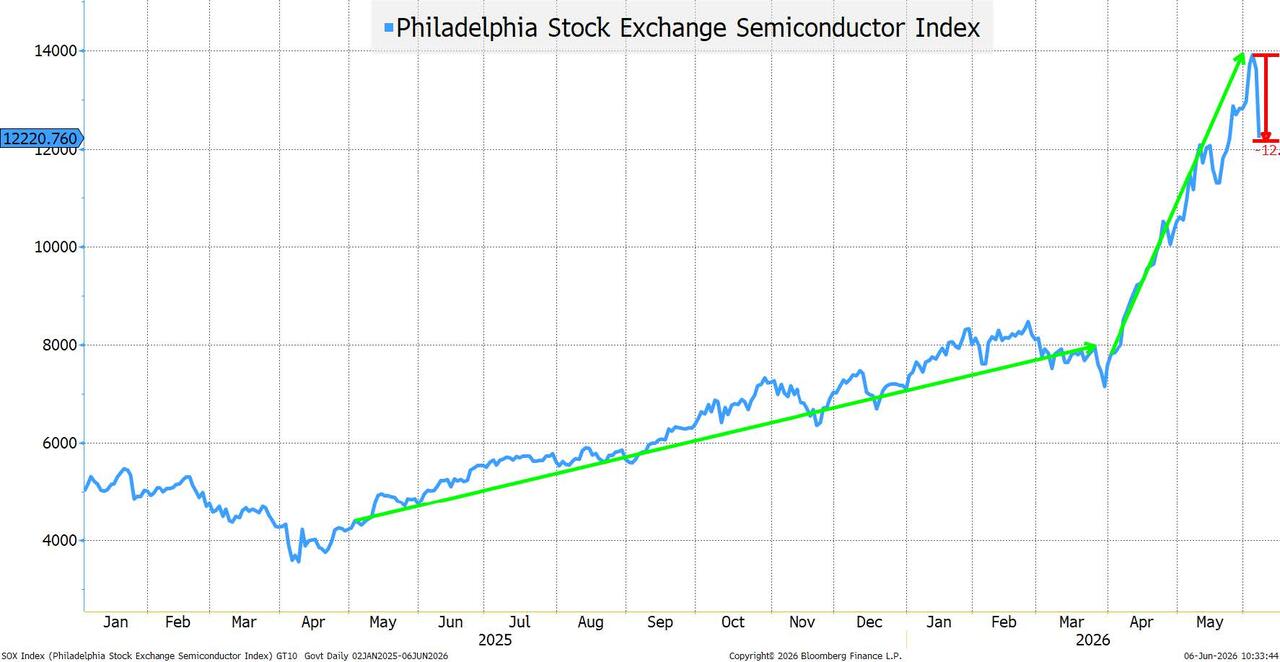

But it is difficult to stick to the plan when the Nasdaq 100 drops almost 5% in a day and the Philly Semiconductor Index (a driving force of the big rally since the initial Iran attack sell-off) dropped over 10%! 10% in a single day for the most important subsector (of late) is a big deal!

As Mike Tyson famously said, “we all have a plan until we get punched in the face” and I’m not sure which would have been worse, a punch in the face from Tyson or 5% down on the Nasdaq 100? At least we can recover from market movements, not sure I could recover from a Tyson punch.

Rates – A Part of the Story

The jobs data came in hot. I would say, yet again, but as we published in our NFP Instant Reaction, there were fewer inconsistencies in this report. It doesn’t quite settle the Jobs – Data vs Vibes question, but it was a step in that direction.

The market is now pricing in one hike in 2026, as opposed to a 69% chance at the start of the week (though that should not have derailed stocks the way they were derailed).

10-year Treasury yields rose to 4.53% from 4.43% at the end of last week. Hardly warranting such a large sell-off in equities. The 10-year only moved 3 bps higher from Wednesday’s close to Friday’s close – kind of noise in the grand scheme of things. It was 4.66% on May 19th but the Nasdaq 100 was a touch lower than today.

I continue to think we see a steady grind higher in yields:

- Price increases are being passed on to the consumer, and in the vast majority of industries, the consumer seems willing to pay those prices.

- I continue to focus on the longer-dated oil futures contracts. My “go-to” choice has been the January 2027 WTI contract – it finished the week marginally higher ($78.22 vs $77.14) on increased concerns about the lack of a deal with Iran. My pain point is that higher for longer is baked into oil prices, but not necessarily bond prices. This will feed into diesel costs, amongst other things, that will feed into more potential price pressures in the economy. As we discussed briefly, as of May 29th (last reporting date) the U.S. Strategic Petroleum Reserve was almost back to the 2023 lows. How much more can be released? Yes, the world is figuring out ways to counter the supply shock, but the tool of releasing reserves may be nearing an end.

- Spending on military is increasing globally. There are also spending pressures on many countries to offset the affordability issue, which is global in nature.

- Iran isn’t the only country in the Middle East selling less oil. While Iran bears the brunt of the pain, the entire region is selling less. For countries where much of the population lives on government handouts from their petroleum profits, that creates the need to borrow. So, some traditionally large buyers of U.S. Treasuries may be busy dealing with their own funding needs.

- Stablecoins to the Rescue? One interesting element to the admin’s strategy was to use stablecoins in particular as a backdoor way for foreigners to buy T-bills. With the Clarity Act struggling to get turned into law, and Bitcoin back to its lows of the year (more on that later), that doesn’t seem like it will help much in the near-term.

I don’t like the backdrop for bond yields here. It is a global issue, but the transition from Treasuries being the “gold standard” to a “generic sovereign bond” to many purchasers impacts Treasuries a little more.

Fighting Parabolic Moves is Crazy! (until it isn’t)

You can fight parabolic moves all you want, but normally you go broke by the third or fourth time you call the market crazy. Once a parabolic move cracks there may be opportunities.

Gold in the past year is a pretty good example. The steady churn higher. One decent pullback, that quickly turned back into a grind higher, followed by a “final” parabolic move higher. It never reclaimed that level and has been grinding lower.

Everyone seems to be asking, is this the fake pullback, like we saw with gold in 2025, or the end of the parabolic run? SOXX, an ETF tracking this index, had a small outflow on Friday, in terms of share count, but is close to its share count high. SOXL, a 3x ETF, had inflows, but from a relatively low base. I have found the flows of these two “sibling” funds to be curious over the past few weeks, and that latest flow data doesn’t help. Maybe the best explanation is some retail holders were getting nervous and selling the 3x leveraged ETF to buy unleveraged versions and shifted some money back on the big drop?

Not sure if this parabolic move is over, but it is interesting to think about.

3.5 Stories FAR MORE IMPORTANT than Rates

I think there were 4 stories that hit the tape later in the week that bear the most responsibility for the move. Let’s start with what I think was the most important headline.

- SpaceX, Other Mega IPOs Denied Fast Index Entry by S&P. The eligibility rules for inclusion in S&P Dow Jones Indices would not shorten the 12-month seasoning period, and there would be no waivers on profitability regardless of size/market cap. I don’t think it is possible to overestimate the importance of index inclusion. China working hard to get their stocks (and to a lesser extent, their bonds) into indices is probably enough evidence to stop right there, but I won’t. There was some small 100-year issuance done in Europe a few years ago, that immediately skyrocketed in price, primarily because index demand was insatiable (eligible bonds typically go in at the end of the month). Again, according to Grok, at the end of 2024 there was $20 TRILLION linked to the S&P 500. MU is the 10th largest holding in SPY with a market cap of just under $1 trillion. It is 1.5% of the index. So presumably a company with a market cap of $1 trillion (which is around where some are being talked about) would mean $300 billion of “instant” demand if included in the indices? That seems so wrong, but the math seems to work, so I’ll run with it.

- That ruling changes the potential “forced” demand. If it goes into the index, it gets bought. And no one is going to underweight these mega IPOs given their potential for outsized gains (index people are primarily afraid of not tracking in general). According to Grok, at the end of 2025, “only” $1.5 trillion tracked the Nasdaq 100. Impressive by any standard, but not the holy grail for these new IPOs.

- The profitability test is also a concern. The goal of many of these IPOs remains growth, as it probably should be given the market environment, but that means they are not focused on profitability. From what I understand, the offering documents are not talking about near-term profitability. That potentially pushes the inclusion further down the road.

- The ½ important story, is that the offering documents let investors see the numbers, and by the sounds of it, some of the numbers relative to valuations are raising an eyebrow. I don’t think that is super important, or should be a surprise, but I heard it mentioned enough this week, to put it down as ½ a headline that is important.

- This is largely a zero-sum game, because stocks would have been sold to make room for the IPOs, but from a headline perspective that is one or two steps removed, and forces participants to come up with money for the new issues using different mechanisms. Maybe that is a “weak” answer, but I don’t think it impacts markets as zero-sum at the moment – treat this lack of inclusion as a headwind.

- It will be curious to live in a world where some of the biggest companies, by market cap, don’t move the S&P 500, but it seems that this is the path we are heading down.

- Stories hit the tape that Meta was potentially considering raising “tens of billions” in a stock offering after Google’s record $85 billion share deal. We have lived in a world where knowing “blackout” periods was important because companies tended to buy back less stock during those periods (not sure if that was ever true, but it is a perception that was out there). Is the market going to have to digest a lot more equity issuance than previously thought? Is the share buyback era shifting? Share buybacks have been a tailwind for markets, and a reversal of that could weigh on markets. The issuance seems to make a lot of sense (tapping as many pools of capital as possible to work on the AI and Data Center buildout), but it should weigh on markets as it is yet more dollars to absorb.

- Broadcom missed AI Expectations. Not sure how true that headline is, but it gathered momentum after their earnings. I suspect it was as much about the market waiting for an excuse to sell, than it was anything really inherent to their business. If it was just their business, the damage wouldn’t have been so widespread. Regardless of the accuracy of the headlines, we had the media, for the first time in ages, being able to question the ongoing AI spend. That is important, especially for anyone who was looking for a “catalyst” to end the parabolic run.

I think these 3.5 stories played a much bigger role in the weakness than either Iran or rates did.

That is somewhat concerning from a risk perspective, because all 3.5 stories have “legs” to them and if this is a real challenge to the parabolic move, we have plenty of downside left for stocks.

More AI Anecdotes

Last week I mentioned that at conferences, attendees no longer want to “hear” about AI. They want concrete examples of implementations. What worked? What didn’t?

Conversations I’ve had this past week all point to similar questions about “is AI currently a good value proposition.” If I wasn’t hearing that so much, I wouldn’t have planned on writing about the AI Revolution. A lot of questions rising to the surface about whether the cost of tokens is delivering what was expected in terms of efficiencies or business opportunities/development. It is far from being one-sided, but the move for many from “relatively inexpensive monthly subscriptions” to a token-based model is letting people do more thorough analysis.

Yes, AI is only going to get better, but are we paying too much for what it delivers today? Probably not, but the parabolic run in stocks linked to the sector leaves them susceptible to any level of doubt.

Gambling versus Investing

Sometimes I refer to the “gambling” crowd as the “degens.” The ones who love 0DTE (Zero Day to Expiration Options), “meme” stocks, Leveraged ETFs (especially single stock leveraged ETFs), and even alt coins. Anything to turn 1 into 100.

I believe they helped drive gold higher at the margin. Without a doubt they focus on crypto periodically, but as bitcoin volatility has declined, it has attracted less of this money.

Have they played a role in the big move in semis? Not if SOXL or TQQQ (3x leveraged ETFs) are a sign, as they’ve been experiencing outflows, but I cannot help but think they have helped the parabolic move (it is, almost definitionally, the type of thing they do).

Which brings me to one other security I’m watching closely. The MSTR Multi-Coupon Cumulative Perpetual Preferred often referred to by MSTR and social media as STRC. The current coupon is set to 11.5%. My “basic” understanding is that this instrument is designed to set its coupon to pull the instrument towards par. Whenever it trades much above 100, the strategy is to use the premium to add bitcoin.

It was trading around 99 until early this week when MSTR sold some bitcoin, apparently to fund the dividend.It was 32 bitcoin – a tiny fraction of the almost 850,000 bitcoin MSTR holds! It seems like a trivial amount (and in fact is a trivial amount). But there was a sentiment that MSTR would never sell bitcoin to pay the dividend (saw a lot of quotes about being told to sell a kidney to buy more Bitcoin).

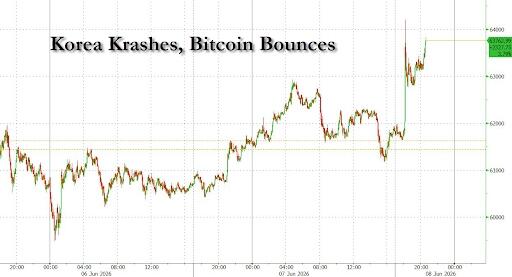

This closed Friday at 93.4 (with bitcoin at $61.5k). Bitcoin is trading lower than that now. While this particular security should not be directly linked to the price of bitcoin (based on capital structure, etc.), it seems to be a driving factor.

Is the “gambling” crowd still heavily invested in crypto? Did they chase the recent upside, only to end up down 25% in less than a month?

Disruptive tech (I often use ARKK as a proxy) got hit hard this week and while off its lows is down on the year.

I fear that the crowd that gambles in some or all of these spaces is under pressure across the board, which may lead to selling pressure. As a whole, this isn’t a big group, but at the margin, when they are chasing the same trade, they have an outsized impact.

Bottom Line

Look for yields to trend higher. That isn’t a major problem for equities, but it isn’t helping.

Credit will have to leak wider, even with higher yields, if equities continue to drop. There is just too much money in various cap structure trades for that not to occur, but credit will outperform. In fact, the equity issuance by some companies, rather than issuing even more debt, is good for credit at the expense of the equity price. Not quite the Debt Diet, but plays out similarly (5-year ORCL CDS for example is well off its highs in March).

I think the 3.5 stories, along with Iran, and higher yields, can add to pressure on stocks.

Having said that, this admin has come up with some stick saves for stocks before and they have all weekend to come up with another one! It is so painfully scary to be bearish equities, and that is probably the right trade, but that doesn’t make it any less scary.

Sell in May and Go Away seemed stupid, until this first week of June.

I continue to see this as an economy with two distinct components:

- An economy facing “affordability” issues, dealing with a low hire, low fire job market (though that might be understating the health of the job market, but I haven’t fully gotten on board with that). That part of the economy is struggling and consumers seem to be sticking to experiential spending versus goods spending, but how long can that last? The stocks affected reflect this.

- The AI and data center buildout economy. Booming! Yet, after any parabolic move, was Wall Street so stupid a couple of months ago that this area was so undervalued that a parabolic move makes sense? Or was the move so great that any questions could cause a significant pullback (who’d have thought we’d be wondering if a one-day 10% move is “significant”). The answer is probably somewhere in between.

Without some new headline out of DC (or a change of tune from the S&P) look for choppiness and more weakness in stocks.

I think the “rotation” theme is limited as this move is about questioning the AI/Data Center valuations and nothing has been done to fix the affordability issues.

Tyler Durden

Sun, 06/07/2026 - 17:30

U.S. Secretary of Defense Pete Hegseth (C) speaks with U.S. WWII and D-Day Landing veterans at a memorial ceremony held as part of the 82nd anniversary of the World War II D-Day Allied landings in Normandy, north-western France, on June 6, 2026. Screenshot via The Epoch Times/X/Department of War

U.S. Secretary of Defense Pete Hegseth (C) speaks with U.S. WWII and D-Day Landing veterans at a memorial ceremony held as part of the 82nd anniversary of the World War II D-Day Allied landings in Normandy, north-western France, on June 6, 2026. Screenshot via The Epoch Times/X/Department of War

The Pentagon in Arlington, Va., on May 25, 2026. Madalina Kilroy/The Epoch Times

The Pentagon in Arlington, Va., on May 25, 2026. Madalina Kilroy/The Epoch Times

Sam Altman exiting Bernie Sanders' office.

Sam Altman exiting Bernie Sanders' office.

Apache Generating Station near Cochise, Arizona;

Apache Generating Station near Cochise, Arizona;

Pentagon file image

Pentagon file image U.S. President Donald Trump hands a pen to Senior White House Policy Advisor on Artificial Intelligence Sriram Krishnan after signing an executive order while U.S. Sen. Ted Cruz (R-Texas) (2nd L) and Commerce Secretary Howard Lutnick look on in the Oval Office of the White House in Washington, DC, on Dec. 11, 2025. Alex Wong/Getty Images

U.S. President Donald Trump hands a pen to Senior White House Policy Advisor on Artificial Intelligence Sriram Krishnan after signing an executive order while U.S. Sen. Ted Cruz (R-Texas) (2nd L) and Commerce Secretary Howard Lutnick look on in the Oval Office of the White House in Washington, DC, on Dec. 11, 2025. Alex Wong/Getty Images A data center in Tennessee. Courtesy of CleanSpark

A data center in Tennessee. Courtesy of CleanSpark Image source: White House

Image source: White House

Recent comments