Apple Negotiating To Buy Blacklisted Chinese Chips To Ease AI-Driven Shortage

After raising prices on their entire product line last week as much as 50% thanks to "unsustainable" input costs from the memory cartel (SK Hynix, Samsung, Micron and Sandisk), Apple is in active negotiations to buy memory chips from two Chinese semiconductor manufacturers on the Pentagon's blacklist, aiming to diversify supply and mitigate the impact of sharply rising component costs triggered by surging AI demand.

Adding to Friday reporting from the Financial Times, Bloomberg now reports that the iPhone maker is seeking chips from ChangXin Memory Technologies (CXMT), a major DRAM producer, and Yangtze Memory Technologies Co. (YMTC), a fast-growing NAND flash maker. The components would be used exclusively in devices sold in China, where Apple already offers market-specific models. The talks are ongoing and not yet finalized, according to people familiar with the matter.

This was the logical next step...

*APPLE SHARES CLOSE DOWN 6.1% IN BIGGEST DROP SINCE APRIL 2025

— zerohedge (@zerohedge) June 25, 2026

China's memory makers are waiting by the phone

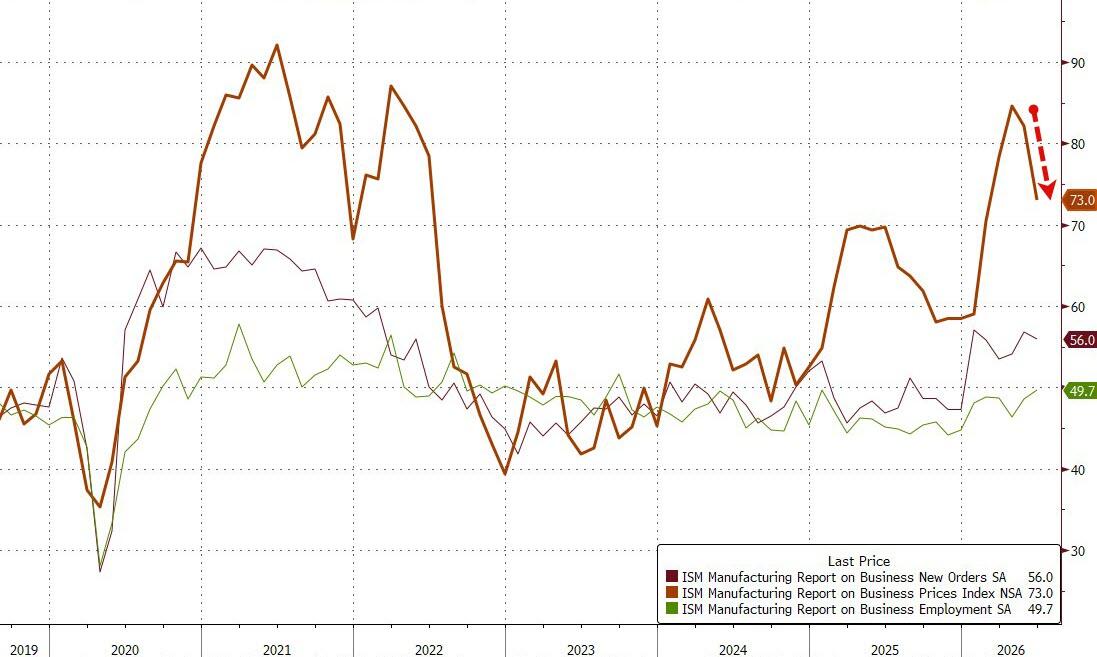

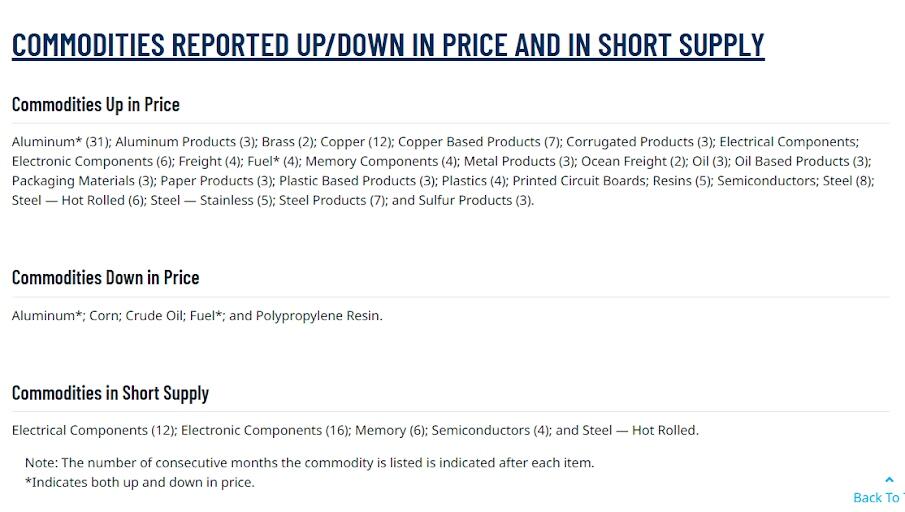

This move would expand Apple's memory supplier base from its current three - Samsung Electronics, SK Hynix, and Micron Technology - to five. It comes after Apple raised prices across its Mac, iPad, and other product lines last week to offset what it described as an unprecedented surge in memory and storage costs. A company spokesperson attributed the increases to the "rapid expansion of AI," noting the firm had "never seen a component price increase this much, this quickly."

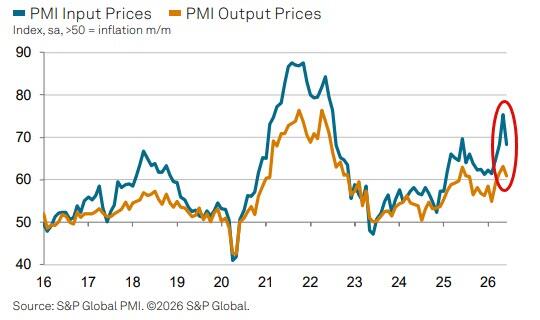

The global memory shortage stems from hyperscale data-center operators prioritizing high-end memory for AI training and inference workloads. This has pulled production capacity toward premium segments, driving up prices for the DRAM and NAND used in consumer electronics. Microsoft took similar action last week, raising Xbox console prices for the third time in 13 months, largely due to the same memory squeeze.

The Apple news was the straw that broke the memory's back: chip stocks had already gotten whacked on Wednesday amid a momentum-meltdown sparked by news that Meta would pivot to a cloud business to sell excess compute from its overpriced collection of data centers, effectively become a neocloud, while capitulating on hopes to build a leading frontier model.

Aaaand Micron is now below its 20-day moving average for the first time since April...

It's not clear what happens next. Both CXMT and YMTC appear on the Defense Department's 1260H list of Chinese companies believed to have ties to the People's Liberation Army. YMTC has carried an additional Commerce Department Entity List designation since 2022, which generally bars it from receiving U.S. technology without special licenses.

That said, Apple does not require formal U.S. government approval to proceed with purchases - though adding the two firms to its supply chain carries significant political risk amid ongoing U.S.-China tensions over advanced technology. Apple CEO Tim Cook has appealed directly to Trump administration officials, including Treasury Secretary Scott Bessent, to help manage potential backlash from national security hawks in Washington. Some officials within the administration have expressed objections to giving Apple leeway on the matter.

To limit exposure, Apple is structuring any deal around devices sold only in China rather than global models. The company previously explored sourcing memory from YMTC in 2022 for China-market iPhones, but that effort was abandoned after strong opposition from U.S. lawmakers and officials concerned about supply-chain security.

In short - the memory market has been reshaped by AI infrastructure spending. Major producers have shifted output toward high-margin products demanded by data centers, leaving tighter supply and higher prices for mobile and computing applications. Samsung and SK Hynix have outlined massive capacity expansions, while Micron is investing heavily in U.S. production - but meaningful relief for consumer electronics remains months away.

For Apple, securing additional sources could help stabilize costs on China sales and reduce reliance on the dominant trio of suppliers. For policymakers, the episode highlights a recurring tension: balancing efforts to secure critical technology supply chains against the immediate economic pressure of higher consumer prices driven by concentrated global demand.

Any agreement would likely draw scrutiny from Congress and administration hardliners who view partnerships with firms on the 1260H list as contrary to U.S. efforts to reduce dependence on Chinese technology. At the same time, the memory-driven component inflation has become visible enough that some officials may see limited, geographically restricted sourcing as a pragmatic pressure valve.

Tyler Durden Wed, 07/01/2026 - 16:40

Democratic socialist Melat Kiros (L) ousted 15-term Rep. Diana DeGette in Tuesday's Democratic primary

Democratic socialist Melat Kiros (L) ousted 15-term Rep. Diana DeGette in Tuesday's Democratic primary

via Atlantic Council

via Atlantic Council

Vadym Iermolaiev, via X

Vadym Iermolaiev, via X

Recent comments