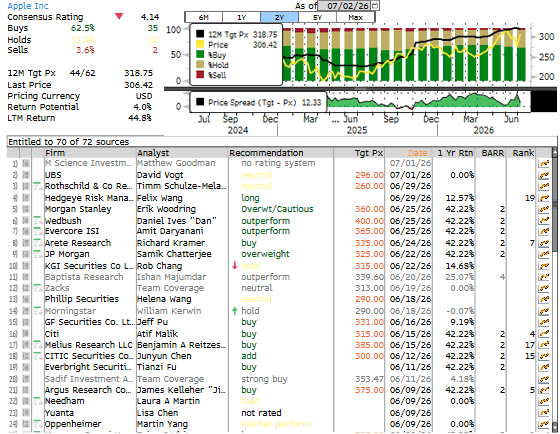

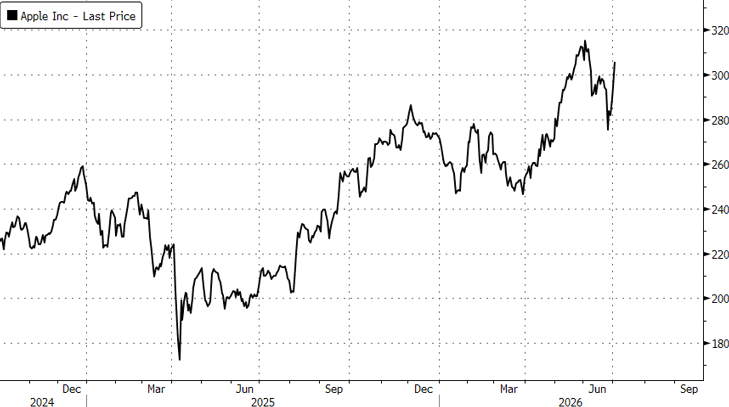

Watch: Shocking Footage Of Britain's Two-Tier Policing

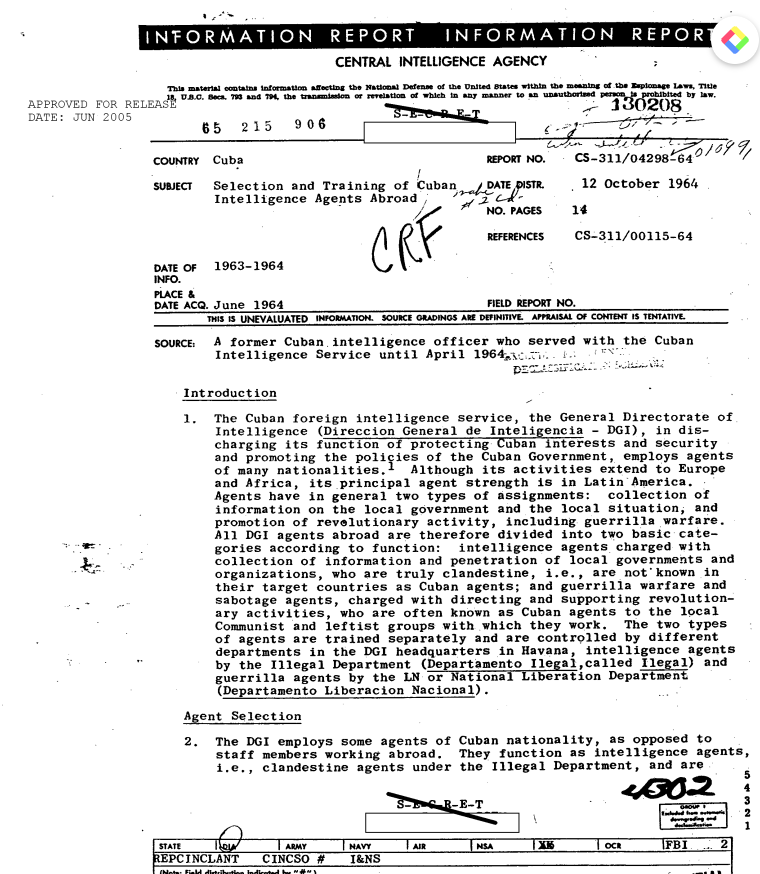

Authored by Steve Watson via Modernity News,

In the latest sickening example of two-tier policing under Keir Starmer's government, a female officer in Birmingham charged straight into a street attack, shielded the three black aggressors, and then turned her aggression on their white British victim - an inebriated teenager who had just been randomly assaulted.

While the attackers dispersed without consequence, multiple officers swarmed the white lad, barked obscenities at him, shoved him into a police car the wrong way round, and then dragged him back out again.

A bystander who tried to explain that the white kid was the victim was completely ignored.

3 blacks attack a drunk white kid in Birmingham, the female police officer comes in to protect the violent blacks and arrest the white kid

— ??????????????? (@Re_mi_gra_tion) July 1, 2026

Absolutely disgusting the way white people are treated in England (@KnockoutAudit) pic.twitter.com/Nct3OcqxaQ

This is not policing. This is ideological enforcement, where native Britons are treated as the problem and mass migration's imported violence gets a free pass.

The main footage of the attack and the officer's intervention spread rapidly on X.

Further clips reveal the tone of the encounter. One officer is heard snarling at the restrained teen: "You're going to walk to the car you fucking dick." The contrast with how such language would be deployed against anyone else is glaring.

"You're going to walk to the car you fucking dick"

— ??????????????? (@Re_mi_gra_tion) July 1, 2026

They would never speak to a darkie like this pic.twitter.com/irPoNe9Yhg

Another angle captures officers trying to force the handcuffed lad into the back seat the wrong way round while yelling "Get in the fucking car."

"Get in the fucking car"

— ??????????????? (@Re_mi_gra_tion) July 1, 2026

Whilst they try to shove him into the back seat the wrong way pic.twitter.com/MpWJuZKhpo

When that fails, reinforcements arrive - another eight officers in total - and they drag him out again because of the botched seating.

Another 8 police officers turn up

— ??????????????? (@Re_mi_gra_tion) July 1, 2026

They drag him out of the car because he's not in the seat properly because they forced him the wrong way pic.twitter.com/zR3QJ2y3ON

A witness wearing glasses can be seen on camera telling officers that the white lad had just been randomly attacked by the group. The officers brush past the information and continue processing the victim as the aggressor.

Public reaction has been swift and unforgiving. One observer captured the robotic programmed nature of the response:

?? British police in 2026 are genuinely like circuit-programmed androids

— welshman (@welshmaan) July 1, 2026

When they identify a scuffle, their sights lock on to the nearest white human regardless of the circumstances

Shameless cyborgs pic.twitter.com/uxlryjILci

The handling shows a blatant failure of duty, with the arresting officer targeting the white male despite clear evidence he was not the agressor. It is impossible the officer did not see the two black males actively attacking him.

We must demand the immediate release of the bodycam footage from the recent unlawful arrest in Birmingham.

— Anth?? (@AnthNFS) July 2, 2026

The handling of this incident is a blatant failure of duty, as the arresting officer targeted the white male as the aggressor despite the clear reality of the situation.... pic.twitter.com/sDmwwZJoKf

West Midlands Police have reportedly asked people to stop sharing the footage. Of course they have.

This is not an isolated lapse. It fits a documented pattern of selective enforcement and excessive force against native Britons while authorities tiptoe around minority perpetrators.

Earlier this month, outrage erupted over South Yorkshire Police officers filmed shoving, baton-wielding and Tasering teenage girls during a dispersal in Rotherham.

The footage showed male officers brutally shoving small teenage girls flying onto the concrete like ragdolls. These are young girls, not hardened criminals. One wrong landing and they could have smashed their heads open.

South Yorkshire Police later acknowledged: "The short clip on social media of the police response to an incident in Rotherham over the weekend appears nothing short of shocking." The force's Professional Standards Department said it was reviewing all available footage, including body-worn video, and that officers are expected to act in a "lawful, proportionate, and fair" manner.

The Rotherham location itself sharpened the hypocrisy. It remains the epicentre of the grooming gangs scandal in which authorities failed for years to protect an estimated 1,400 young victims from predominantly Pakistani Muslim gangs. Political correctness and fears of racism accusations paralyzed police and social services. Now the same forces apply heavy-handed tactics to young British girls celebrating a school leavers' event.

Similar incidents piled up around the same period. Footage emerged of officers manhandling a five-year-old boy - nearly yanking his arms from their sockets while forcing him into a police car - while pepper-spraying his father and confronting his mother who was holding a baby.

South Yorkshire police shove a five year old kid into a car while almost pulling his arms out of their sockets, pepper spraying the father and getting in the mother's face as she holds a baby in her arms. What on earth did they do? pic.twitter.com/BV40eH9sD1

— m o d e r n i t y (@ModernityNews) June 14, 2026

Another clip showed officers smashing a man's head into a metal bollard, then handcuffing and dragging him while threatening the person filming.

This case is actually way worse than the initial footage revealed. This longer video shows that after smashing the guy head first into a metal bollard the police handcuff him and drag him around. They then threaten and shove around the person filming it. https://t.co/3rF0kufikg

— m o d e r n i t y (@ModernityNews) June 14, 2026

A further video captured police slamming Siobhan Whyte to the ground during a protest linked to the Henry Nowak case. Her daughter had been murdered by an illegal migrant, stabbed 23 times in the head with a screwdriver.

???BREAKING: British Police Slam Elderly Woman to the Ground in Broad Daylight!

— Mario ZNA (@MarioBojic) June 15, 2026

Her daughter was stabbed 23 times in the head with a screwdriver – but Starmer's police don't care.

While arresting 5-year-olds, UK cops now beat Britons of any age. pic.twitter.com/SXag5tNjhe

A 50-year-old military veteran and father of three with 13 pins in his right ankle was struck with riot shields and kicked in the head four times while sitting on a wall filming and stating he was doing nothing wrong.

These episodes form part of a growing catalogue of police interactions with native British citizens that many describe as disproportionately aggressive. The common thread is eroding public trust.

If you keep assaulting and arresting innocent members of the public, especially when they're being victimised, then the people are going to start turning on you.

— Cthulhu Loves You (@CthulhulLovesU) July 2, 2026

Best stop it.

When consent is revoked, and it will be at this rate, you're nothing more than civilian thugs....

The Henry Nowak case stands as the starkest recent precedent. On 3 December 2025, 18-year-old Henry was fatally stabbed five times in Southampton. His attacker, Vickrum Digwa, convinced arriving officers he was the victim and claimed racial abuse.

Police arrested and handcuffed the dying Henry instead of providing immediate aid. It took eight minutes for officers to discover the stab wound even though Henry repeatedly told them he had been stabbed and could not breathe.

Digwa was never handcuffed during his time in custody before being charged.

The Independent Office for Police Conduct confirmed it is investigating two Hampshire officers for potential gross misconduct. The evidence indicates both officers may have breached standards of duties and responsibilities, use of force, and discreditable conduct.

These relate to potential failures to recognise that Henry needed urgent medical attention, to immediately act after he said he had been stabbed and could not breathe, and the decision to arrest and handcuff Henry rather than provide immediate first aid.

There is also an indication one officer may have breached the standard relating to authority, respect and courtesy for appearing to dismiss Henry saying he had been stabbed.

'I don't just want these officers under investigation, I want them arrested!'

— GB News (@GBNEWS) July 1, 2026

Adam Brooks (@EssexPR) discusses the police's failings following the murder of 18-year-old Henry Nowak, who was handcuffed in his final minutes. pic.twitter.com/mVxtd9Xx68

The officers face investigation but have not been suspended. Adam Brooks stated on GB News: "I don't just want these officers under investigation, I want them arrested!"

The Birmingham incident follows the same script. The white victim is processed aggressively while the actual attackers are permitted to leave. West Midlands Police have reportedly moved to limit circulation of the footage rather than address the conduct on camera.

This suggests the same institutional reluctance to confront anti-white bias that has already been admitted in training contexts around the Nowak case.

Britons pay for policing through their taxes. They have every right to demand officers who de-escalate rather than escalate against teenagers, who protect the vulnerable instead of dismissing them, and who operate without the stain of two-tier standards.

When footage repeatedly shows the opposite - and when legacy media largely ignores it until social media forces the issue - the contract between police and the public frays further.

Accountability mechanisms exist. Body-worn video exists. The public expects both to deliver transparency and consequences where warranted. Without that, resentment will only deepen.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden Fri, 07/03/2026 - 08:10

Experts say the best retirement withdrawal strategy adjusts to changing conditions. oneinchpunch/shutterstock

Experts say the best retirement withdrawal strategy adjusts to changing conditions. oneinchpunch/shutterstock Gov. Gavin Newsom, Alexis Podesta

Gov. Gavin Newsom, Alexis Podesta

Acting U.S. Attorney Bill Essayli speaks as Los Angeles Police Department Chief Jim McDonnell (R) and Special Agent in Charge Kenny Cooper of the Bureau of Alcohol, Tobacco, Firearms, and Explosives, Los Angeles Field Division, look on at a press conference announcing an arrest in the Palisades Fire investigation in Los Angeles on Oct. 8, 2025. Mario Tama/Getty Images

Acting U.S. Attorney Bill Essayli speaks as Los Angeles Police Department Chief Jim McDonnell (R) and Special Agent in Charge Kenny Cooper of the Bureau of Alcohol, Tobacco, Firearms, and Explosives, Los Angeles Field Division, look on at a press conference announcing an arrest in the Palisades Fire investigation in Los Angeles on Oct. 8, 2025. Mario Tama/Getty Images Former First Lady Dr. Jill Biden speaks with journalist Paola Ramos (L) at the Sixth and I temple and venue on June 3, 2026 in the Chinatown neighborhood of Washington, DC. while promoting her new book, "View from the East Wing: A Memoir”.Tom Brenner—Getty Images

Former First Lady Dr. Jill Biden speaks with journalist Paola Ramos (L) at the Sixth and I temple and venue on June 3, 2026 in the Chinatown neighborhood of Washington, DC. while promoting her new book, "View from the East Wing: A Memoir”.Tom Brenner—Getty Images

Recent comments