Gigantic US Error Or All Part Of A Plan?

Via Rabobank,

Anybody thinking US payrolls, even at -92K, matters much in the current environment is probably at the head of the queue to be replaced by an AI soon. That data series is always volatile and 2.5m undocumented workers are estimated to have left the US since Trump was re-elected: 394K foreign-born workers lost their jobs in the reported month while the native-born series rose 877K, albeit after a shocking 2.5m drop of its own the month before. How can anyone take these numbers seriously even if the underlying signal is deadly serious?

This is eclipsed by Brent oil this morning trading over $110 with WTI at $107: both look to be going exponential, perhaps even opening up the $150 scenario the GCC warn of. Worse, that doesn’t account for more dramatic moves in diesel, jet fuel, fertilizer, key chemicals like sulphur, and gases like helium, without which not a lot moves in the industrial economy, grows in the agricultural economy, or is produced in terms of metals like copper and tech goods like chips.

In short, this is now starting to look like a potential combination of the 1973 post-Yom Kippur War oil shock, the 2022 Russia-Ukraine War commodity shock, and the 2020-21 Covid supply chain shock.

The longer this goes on, the more exponential the damage becomes in a domino effect, which is exactly what oil is now showing to a market that saw some takes last week that ‘things could be a lot worse.’ Well, now they are: and if we are still in the same position this time next week, things could be quite terrifying.

Yet while credible estimates today are that if all fighting were to suddenly cease, it would take two weeks to start to right the ship and a further two months to get back to normal, what we should call Gulf War 3 is showing many signs of widening its geography and escalating within it.

On geography: even if Trump is reportedly now against using the Kurds as a military wedge against Tehran (perhaps due to Turkish opposition), Azerbaijan, which was recently struck by Iran, is another matter. So is Pakistan, which has underlined its mutual defence pact with the Saudis. EU member Cyprus has reported that the drone which struck it was fired by Hezbollah in Lebanon, and was a Russian Shaheed model, not an Iranian one. Russia has also openly said that it isn’t neutral in this conflict, and favours Iran, alongside reports that it’s providing Tehran with data to help it strike its opponents. In Lebanon, Israeli actions are intensifying.

On escalation: after an apology to its neighbours from Iran’s president was rebuffed by the IRGC, the weekend saw strikes on energy facilities against both sides, where Iran came off worse. Moreover, we saw several reports of attacks on desalination plants: if those critical facilities were to go in the region, much of its population would have to as well. Trump is reportedly weighing the introduction of special forces ground troops into Iran, while a third carrier strike group is now on the way. Moreover, Tehran has appointed Mojtaba Khamenei, the son of the former Supreme Leader, to replace him. He is clearly unacceptable to both the US and Israel and reflects the hardest of lines from the regime rather than any possible compromise, Venezuela style.

It’s also time to take a deep breath and note energy expert Anas Alhajji is asking if this is a gigantic US error or part of a plan.

I’d flagged 2026, besides telling 2025 to “hold my beer”, was logically going to see the US use its military to disrupt upstream supply chains heading to China to counterbalance the downstream and rare-earths midstream (i.e., processing) dominance Beijing can coerce it with. The goal was cheap commodities for them and pricey ones for others.

Alhajji takes this further to note that the US is *relatively* less impacted by the tidal wave of economic and market chaos heading our way:

-

the US (with the Americas) is relatively energy self-sufficient: what if the US were to stop exporting oil, its historic policy norm, to bring WTI down sharply, for example? Could we, as others float, see $200 oil globally and $50 oil State-side?

-

Likewise, US LNG is now the lowest risk global choice: who will trust the Gulf as a secure provider again unless the entire region is brought under a true Pax Americana?

-

The US, with the Americas, is also self-sufficient in many commodities being choked off directly or indirectly via Hormuz. That includes fertilizer, which means US and LatAm food supplies could remain secure when others’ aren’t. It also includes helium, which allows for the manufacture of semiconductors, when others may be about to fall short.

By contrast, Europe is again in a bad position in this looming crisis, as are energy- and commodity-reliant Asian exporters already struggling with US tariffs.

China will have to rely on its stockpiles for a while, then Russia, which greatly strengthens Moscow’s hand in that relationship.

Perhaps this is paranoia or looking for a strategy in a geopolitical miscalculation; or it could have been a plan B if Iran didn’t ‘do a Venezuela’; or it might just be a happy coincidence the US can now take advantage of if it wishes.

Yet the Donroe Doctrine ‘Shield of the Americas’ project launched at the same time as Gulf War 3, the increased likelihood Cuba flips to the US camp, following the pressure on Greenland, and the evident lead set by US economic (and military) statecraft is quite the coincidence if this is all just random.

Indeed, it’s incredibly important to grasp that this *might* be the Great Game being played, because if it is, assuming “because markets” will bail us out (“Iran/Trump can’t let this happen”) could be false hope.

Oil vey, indeed.

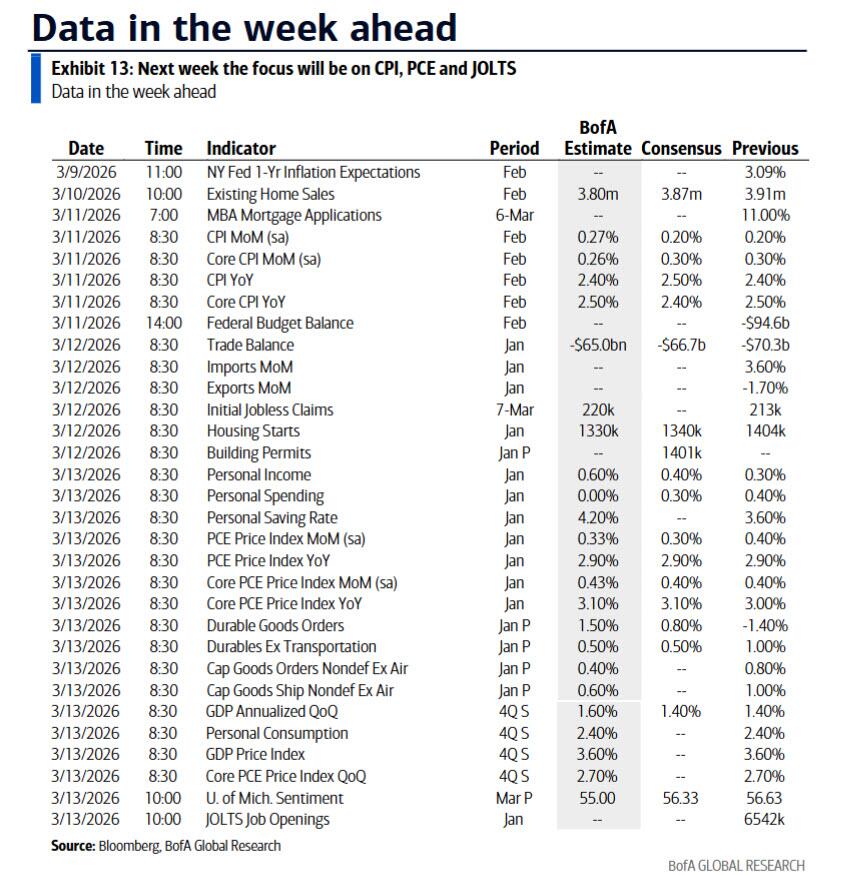

Week ahead

Tuesday: sees more of Japan Q4 GDP, Aussie NAB business confidence, German trade data, Chinese trade data, and the US NFIB small business survey and existing home sales.

Wednesday: has US CPI. Again, irrelevant right now.

Thursday: it’s US trade data and initial claims, housing starts and building permits.

Friday: sees UK industrial production and trade data, Canadian employment, US personal income and spending and the PCE deflator, durable goods, initial claims, JOLTS data, and Michigan inflation expectations.

Tyler Durden

Mon, 03/09/2026 - 12:05

via Duvar English

via Duvar English

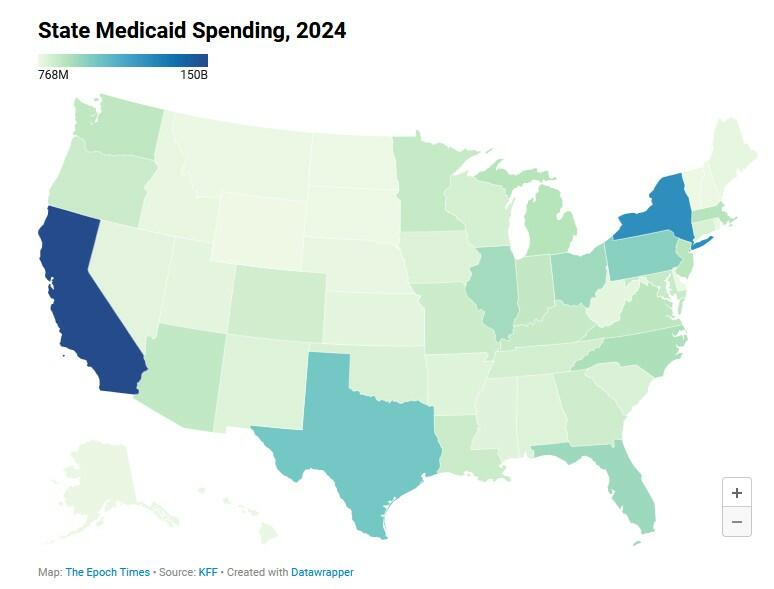

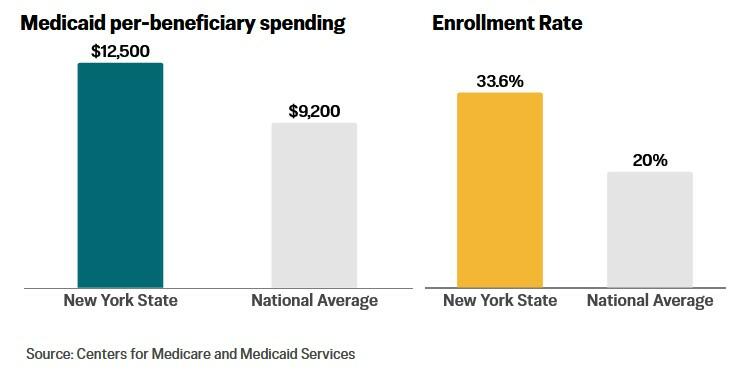

Dr. Mehmet Oz, administrator for the Center for Medicare and Medicaid Services, speaks at a press conference in the Library of the Eisenhower Executive Office Building in Washington on Feb. 25, 2026. Travis Gillmore/The Epoch Times

Dr. Mehmet Oz, administrator for the Center for Medicare and Medicaid Services, speaks at a press conference in the Library of the Eisenhower Executive Office Building in Washington on Feb. 25, 2026. Travis Gillmore/The Epoch Times

Recent comments