H.R. 5497, Apostle Islands National Park and Preserve Act

As ordered reported by the House Committee on Natural Resources on February 11, 2026

Speak Your Mind 2 Cents at a Time

Authored by Stephen Soukup via American Greatness,

Over the past week or so, many on the political Right have understandably enjoyed a laugh or two at the expense of Congresswoman Alexandria Ocasio-Cortez (D, N.Y.). AOC went to the Munich Security Conference to provide “balance” to the Trump administration’s presence and to burnish her own credentials on the global stage. Instead, she mostly just made a fool of herself. Not only did she stutter, stammer, and offer a Kamala Harris-esque non-answer when asked about American interests in and obligations to Taiwan, but she also demonstrated a comically poor grasp of geography and a righteously ignorant understanding of history. In an effort to rebut and embarrass U.S. Secretary of State Marco Rubio, AOC embarrassed only herself, showing that historical facts mean far less to her than identity-inspired fiction.

But while it’s inarguably fun to chuckle at and mock the ignorance of the smug congresswoman and presumed presidential aspirant, it is also important to acknowledge that her historical and political illiteracy extends beyond the superficial and touches on matters of real and critical importance. Notably, this purported champion of the working class does not know the history of working-class politics, does not understand the reasons for the collapse of the working-class-centered ideology, and, as a result, has never contemplated the dangers inherent in attempting to resuscitate that failed doctrine.

Congresswoman Ocasio-Cortez has long emphasized her biography and working-class roots to enhance her political status—and justifiably so. Her childhood may not have been quite the struggle she pretends it was, but she nevertheless endured economic hardships—especially after her father’s death—and was unable to find employment commensurate with her education. She was, famously, a bartender and a cocktail waitress before her election to Congress and, as a result, has long fashioned herself a champion of the working class and its purported priorities.

Indeed, on her trip to Munich, AOC emphasized her affinity with the working class and admonished democratic nations to erect a bulwark against totalitarianism by focusing on workers, workers’ rights, and worker-centered politics. “It is of utmost urgent priority that we get our economic houses in order and deliver material gains for the working class,” the congresswoman said, “or else we will fall to a more isolated world governed by authoritarians that also do not deliver to working people.” She railed against large corporations and especially billionaires, insisting that they had to be stopped from “throwing their weight around” in domestic and international politics. In short, the good congresswoman used her trip to Munich to urge the workers of the world to unite, because, as she sees it, they have nothing to lose but their chains.

There’s only one little problem with AOC’s exhortation: it’s ridiculous. Indeed, it’s been tried . . . and tried . . . and tried. It doesn’t work. And when I say that, I don’t mean that socialism doesn’t work or that communism has been tried countless times before and failed every time. That much is obvious by now. Rather, what I mean is that the workers of the world don’t care about the rest of the workers of the world. They don’t like the idea of being divided into classes, and they don’t have any particular affection for their fellow laborers. They don’t dislike other workers necessarily, but they don’t see themselves as a monolithic federation sharing the same interests, needs, or political predilections. Truth be told—and this is the key to understanding the silliness of the whole “global proletariat” nonsense—even the Marxists long ago gave up on uniting the workers of the world. In fact, in the United States, the most prominent Marxist theorists actually gave up on workers altogether as allies in the fight against capitalism.

One of the most pervasive bits of common knowledge about World War I is the idea that the ruling classes of Europe did not expect it to last very long or to be particularly destructive. Kaiser Wilhelm infamously predicted that Germany’s troops would be home “before the leaves fall.” What is less well known is that this “short-war illusion” was shared and embraced even more unequivocally by the era’s Marxist agitators. They believed, as Engels in particular predicted, in the inevitability of a “new man,” who would evolve from the working classes and would never harm his fellow new men. Just two years before Archduke Franz Ferdinand was assassinated, the Manifesto of the Second International Socialist Congress in Basel in 1912 declared that war between working men was a virtual impossibility:

It would be insanity for the governments not to realize that the very idea of the monstrosity of a world war would inevitably call forth the indignation and the revolt of the working class. The proletarians consider it a crime to fire at each other for the profits of the capitalists, the ambitions of dynasties, or the greater glory of secret diplomatic treaties.

Of course, things didn’t exactly go as planned—either for the ruling classes or the Marxists. World War I did many things to Europe, most of them awful and ugly and demoralizing. It did many of the same things to Marxism. Although the war did incite revolution in Russia, that was far less than the Marxists had hoped for. Russia’s revolution was led by the educated classes and animated by peasants. Proletarian “workers” were largely non-existent. In the industrialized parts of Europe, workers flat out rejected appeals to class unity, choosing instead to fight for God and country. German workers saw themselves not as workers but as Germans. French workers saw themselves not as workers but as Frenchmen. And so it went.

In the aftermath of the war, Marxists were forced to confront two massive and related problems: the workers’ refusal to unite and the rise of profound and entrenched nihilism. In order to save their ideology, these Marxists had to revise it and explain its failures. As any schoolboy knows, they did so by concluding that the workers of the world did not understand their own interests or even their own natures. Workers were dissociated from their interests by the institutions of society, especially the institutions of cultural transmission: the Church, the schools, the media, art, entertainment, and so on. Therefore, to enable workers to see their real interests, those institutions had to be taken over, destroyed, and rebuilt along ideological lines. And thus began the Gramsci, Lukács, and Frankfurt School-led “long march through the institutions,” which largely killed economic Marxist theory, creating what we know today as “cultural Marxism.”

In 1964, Herbert Marcuse—a latecomer to the Frankfurt School who became America’s most prominent Marxist theorist—essentially gave up on the workers as the stimulators of revolution. As I have noted before in these pages, “Marcuse conceded that the capitalist system was simply too good at providing goods and services that made the masses comfortable and happy. It therefore deprived them of ever knowing or caring about their true oppressed consciousness. Workers had become one-dimensional consumers, distracted from their fate by their egos and the creature comforts of capitalism.” In turn, Marcuse laid the foundations for “identity politics,” which would, he believed, enable the rise of a new revolutionary class, motivated by new perceptions of oppression.

Long story short (if that’s possible any longer), over the course of the last century, Marxists gave up on workers and even on economics, deciding instead to focus on culture and identity-based grievances.

Congresswoman Ocasio-Cortez doesn’t appear to know any of this, of course, which means that she also doesn’t know that appeals to working-class unity have tended to end in tragedy, followed by massive, civilization-destroying revisionism. Most notably, because she doesn’t know that revisionism was necessary in Marxism, she also doesn’t know that the other stream of post-World-War-I Marxist revisionism ran through Rome and Berlin and resulted in authoritarianism on a scale previously unimagined.

AOC’s ignorance isn’t just about cowboys, in other words. It’s also about the greatest and most profound tragedies in world history. Her ignorance is dangerous.

Tyler Durden Mon, 02/23/2026 - 14:45After disrupting countless Software/SaaS/finance/real estate/broker sectors, Anthropic's Claude is now going after targeted companies.

A little before 2pm ET, Bloomberg sent out a headline that Anthropic's Claude has found yet another skillset:

A herd of panicked IBM longs flooded to the Claude blog to read more on what is happening. Here's what it found (excerpted):

COBOL is everywhere. It handles an estimated 95% of ATM transactions in the US. Hundreds of billions of lines of COBOL run in production every day, powering critical systems in finance, airlines, and government.

Despite that, the number of people who understand it shrinks every year.

The developers who built these systems retired years ago, and the institutional knowledge they carried left with them. Production code has been modified repeatedly over decades, but the documentation hasn't kept up. Meanwhile, we aren't exactly minting replacements—COBOL is taught at only a handful of universities, and finding engineers who can read it gets harder every quarter.

Given these roadblocks, how can organizations modernize their systems without losing the reliability, availability, and data they’ve accumulated over decades? And without breaking anything?

* * *

How AI changes COBOL modernization

AI excels at streamlining the tasks that once made COBOL modernization cost-prohibitive. With it, your team can focus on strategy, risk assessment, and business logic while AI automates the code analysis and implementation.

* * *

Start your COBOL modernization

The approach outlined above works for COBOL systems of any size. Tools like Claude Code can automate much of the exploration and analysis work described, giving your team the comprehensive understanding they need to plan and execute migrations confidently.

Start with a single component or workflow that has clear boundaries and moderate complexity. Use AI to analyze and document it thoroughly, plan the modernization with your engineers, implement incrementally with testing at each step, and validate carefully. This will build organizational confidence and surface adjustments needed for your systems.

In kneejerk reaction, IBM stock, already down sharply on the day, and tumbling 20% from its all time highs just earlier this month, plunged $15 to the lowest level since Liberation Day, briefly dipping below $230...

... as the market realized that it is the latest target of the Claude disruption train. You see, Common Business-Oriented Language (COBOL) is a high-level, English-like compiled programming language developed specifically for business data processing, via IBM. As such, anything that disrupts this lucrative ecosystem created by IBM (code COBOL, then sell consultancy contracts to adjust the code which virtually nobody knows how to use), would immediately smash IBM stock... and that's precisely what happened.

Which begs the question: after various Claude updates caused hundreds of billions in market cap damage in the past 3 weeks, is the company's strategy to keep rolling incremental disruption updates becoming Antrhopic's self-funding strategy. After all, if Dario Amodei had bought puts on IBM, and the dozens of companies that have plunge dmore than double digits in recent weeks, he would have made billions, certainly enough to fund his company for months if not years.

And if not Anthropic, when will OpenAI - which needs capital much more badly than its enterprise-focused peer - do the same?

Tyler Durden Mon, 02/23/2026 - 14:25Authored by Zachary Stieber via The Epoch Times,

A federal judge on Feb. 23 said that the final report on President Donald Trump compiled by a former special counsel shall not be released.

U.S. District Judge Aileen Cannon, who is based in Florida (and was appointed by President Trump), said in a 15-page decision that she was granting requests from Trump and his co-defendants to keep part two of the report from former special counsel Jack Smith shielded from the public.

Cannon said that Smith wrongly forged ahead with investigating Trump and others for allegedly violating federal law by gathering and retaining sensitive documents even after she ruled his appointment was unconstitutional and threw out the case.

“Rather than seek a stay of the Order, or clarification, Special Counsel Smith and his team chose to circumvent it, for months, by taking the discovery generated in this case and compiling it in a final report for transmission to then-Attorney General Garland, to Congress, and then beyond,” Cannon said.

“The Court need not countenance this brazen stratagem or effectively perpetuate the Special Counsel’s breach of this Court’s own order.”

She added later:

“While it is true that former special counsels have released final reports at the conclusion of their work, it appears they have done so either after electing not to bring charges at all or after adjudications of guilt by plea or trial. The Court strains to find a situation in which a former special counsel has released a report after initiating criminal charges that did not result in a finding of guilt.”

The Department of Justice (DOJ) had appealed Cannon’s ruling, but dropped the appeal after Trump won a second term in office.

The department also released part of Smith’s report just before Trump began his second term.

The other part, which has not been made public, was not to be released, according to a January 2025 order from Cannon.

Cannon announced in December 2025 that her injunction was set to expire in February this year.

Trump and co-defendants said in filings on Jan. 20 that Cannon should permanently block the release of the other part of Smith’s report. Lawyers for Trump said Smith was illegally appointed, and all acts he undertook were thus void, so the release “would constitute an irreversible violation of this Court’s constitutional rulings in the underlying criminal action and of bedrock principles of the separation of powers.”

DOJ officials backed that position.

“Put simply, Smith’s tenure was marked by illegality and impropriety, and under no circumstance should his work product be given the full weight and authority of this Department,” they said in a brief, adding later that making the second part of the report public would “lead to the public dissemination of sensitive grand jury materials, attorney-client privileged information, and other information derived from protected discovery materials, raising significant statutory, due process, and privacy concerns for President Trump and his former co-defendants.”

The DOJ and Trump did not immediately respond to requests for comment on Cannon’s ruling. Smith’s law firm did not return an inquiry by publication time.

Two outside groups, American Oversight and Knight First Amendment Institute, recently requested to intervene in the case because they wanted the second part of Smith’s report disclosed.

Cannon declined to allow the requested intervention.

In an appeal, the groups said that because the government had aligned with the defendants in the case, unless they were allowed to intervene, the hidden portion of Smith’s report would be buried or destroyed.

“There is no good reason for withholding this report from the public,” Scott Wilkens, senior counsel at the Knight First Amendment Institute, said in a Feb. 9 statement. “The public has a right to the report under the First Amendment and common law, and the Freedom of Information Act requires its release as well.”

Tyler Durden Mon, 02/23/2026 - 12:45

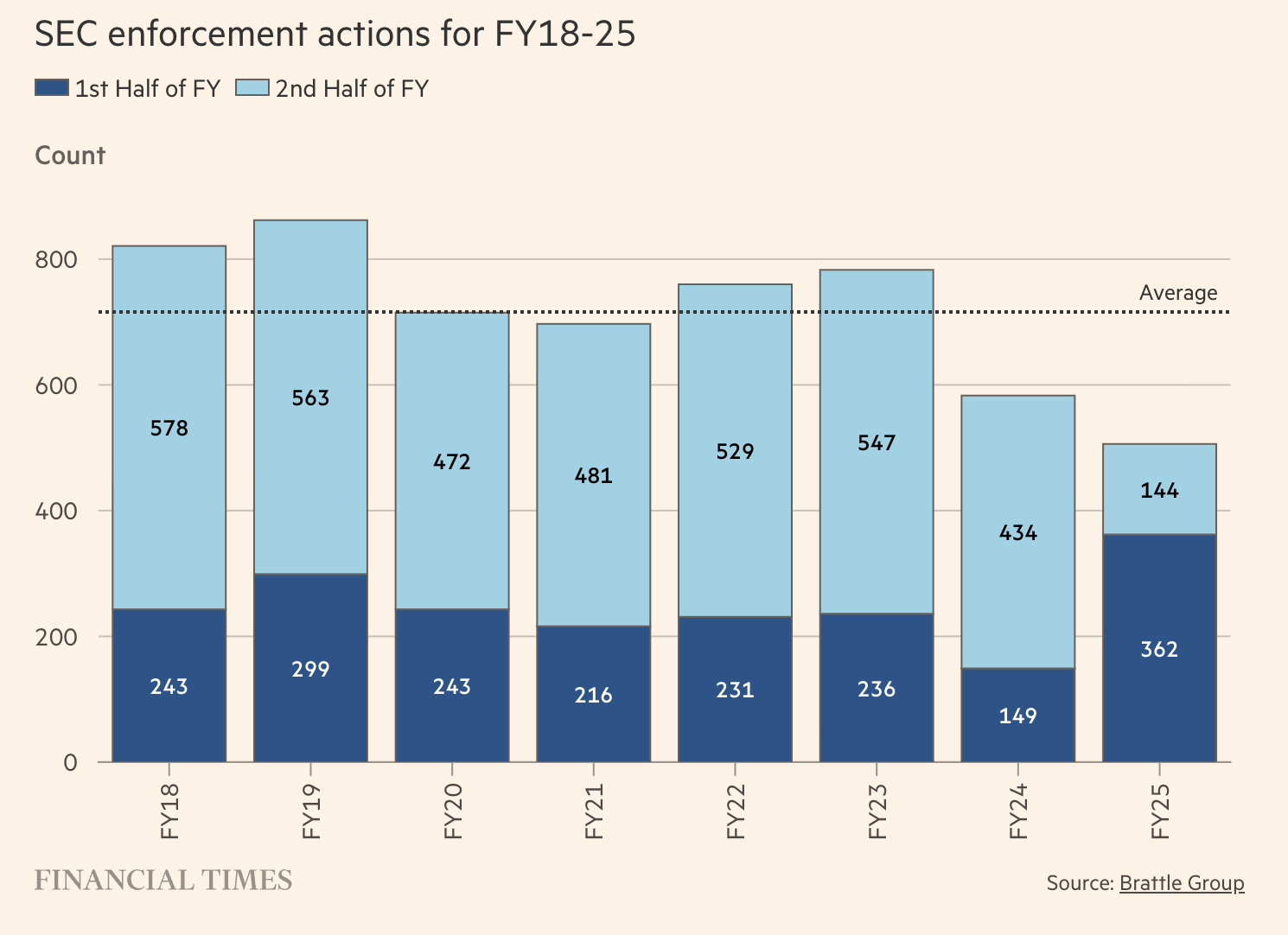

Soon after the Supreme Court dropped its IEEPA decision Friday morning, I wrote up a post on who the IEEPA decison Winners were. Today, as promised, we review the losers. Spoiler alert: there are a lot of them.

In broad strokes, the winners were the large companies that filed for refunds or sued the US, the dollar, consumers, the separation of powers, the US Constitution, and the Supreme Court. The losers are a bit more nuanced: some are obvious, many are not.

My analysis of who won and who lost is based on both the immediate reaction to the tariffs being found unlawful, and the longer-term results of this case. As always, the world is complex and not black-and-white, with much nuance to be found.

Let’s jump right in:

LOSERS

• Consumers: On Friday, my immediate reaction was that US consumers would have a lower tariff burden. But the President added a 10% (150-day) global tariff, and then raised it over the weekend to 15%.

15%. This regressive Trump Tax will be borne by every consumer on a wide range of imported foodstuffs, manufactured parts, and finished goods. It is much less of a victory than I originally believed due to the latest tariffs POTUS imposed.

• U.S. Equities: What should have been a clear victory for US equities has turned into a muddled mess. (See chart at top). Blocking the president’s power to arbitrarily tariff any country any amount is a significant win; it was offset by the President’s immediate use of Section 232 to impose 10% 15% tariffs for 150 days. While Markets rallied right after the decision, they reacted negatively to the president’s actions over the weekend.

¶ Commodities (especially Gold & Silver): If the dollar was the big winner Friday, then anything priced in dollars is the loser. As noted, 2025 – just like 2017 before it – was a bad year for the dollar What’s been driving the dollar lower has been frustration from our trading partners, the repatriation trade, and a spreading concern that the United States is no longer the reliable ally it once was.

• Domestic automakers: Ford and GM have seen their stocks rise over the past year, but they have been underperforming the industrials and the broader market lately. Aluminum & Steel tariffs have made their cars more costly; other non-IEEPA tariffs1 affecting automobiles were not before the Court.

• Bonds & Deficits: If you believe that the bond market does not like unfunded spending, then it’s hard to see how bonds are not at least modest losers post SCOTUS decision. Tariffs are taxes that raised nearly $200 billion. While nobody here wanted a VAT tax, it did affect government revenues.

On a related note, in the first year of his second term, President Trump added $2.25 trillion to the national debt. His claim was that tariffs would help balance the budget, notwithstanding the Constitution – and that claim is no more.

….I am a Tariff Man. When people or countries come in to raid the great wealth of our Nation, I want them to pay for the privilege of doing so. It will always be the best way to max out our economic power. We are right now taking in $billions in Tariffs. MAKE AMERICA RICH AGAIN

— Donald J. Trump (@realDonaldTrump) December 4, 2018

Tariff Man: Trump has largely defined his presidency by promoting the benefits of tariffs. Alongside tax cuts and deportations, it is this administration’s signature policy. It’s not surprising that the Supreme Court’s rejection has sparked a wide range of reactions. At one end, Hakeem Jeffries called the tariff ruling a “crushing defeat for the wannabe King”; at the other, U.S. Trade Representative Jamieson Greer described tariff policy as “unchanged.”

The truth lay somewhere in between.

It was a frustrating defeat for POTUS, one that led him to lash out at Justices, Democrats, trading partners, and others. (Tomorrow night’s State of the Union address could become unhinged). Regardless, it was a significant loss with consequences that have yet to be fully determined.

• Tariff benefits:

The other thing we learned was that none of the promised benefits of tariffs have materialized:

“It’s the most beautiful word in the dictionary, and it’s my favorite word. It will make our country rich. Tariffs cost Americans nothing, it’s not going to raise our inflation. If I’m going to be president of this country, I’m going to put a 100%, 200%, 2,000% tariff. We’re going to generate hundreds of billions in tariffs; we’ll become so wealthy we won’t know how to spend that money.” 2

Every economist not named “Navarro” had previously forecast this…

• Foreign Policy: The single biggest hammer the president had has been taken away: His ability to single out specific countries and then impose unlimited tariffs (100%) is no longer.

The NYTimes blew this one: “They Did Deals With Trump to Get Lower Tariffs. Now They Are Stuck.”

A naïve headline that is laughably wrong. Nobody who was strong-armed into a deal based on unlawful tariffs is going to honor those deals. (Good luck enforcing them in the court of international trade).

These deals will be slow-walked, empty-gestured, let-me-get-back-to-you, and ultimately ignored.

• Congress: While the Constitution, the Supreme Court, and the separation of powers were victors on Friday, the subtle loser in our system was Congress. They had the ability – indeed the obligation – to push back on the executive branch’s power grab. The failure to stand up to the President’s overreach was a self-own. Their timidity allowed the bully to take what was rightfully theirs: the power to tax.

• Sycophants: There are numerous people who have thoroughly embarrassed themselves throughout the tariff regime3 but one stands out above them all: Brett Kavanaugh.

I could criticize Gorsuch’s concurring opinion as an unneeded performative treatise running 46 pages, only to ultimately agree with Chief Justice Roberts.4

But really, it is Kavanaugh whose dissent will be remembered. It fell somewhere in between embarrassing and sycophantic, fluffy and nonsensical.5 He spends 61 pages telling President Trump he won: “Although I firmly disagree with the Court’s holding today, the decision might not substantially constrain a President’s ability to order tariffs going forward, because numerous other federal statutes authorize the President to impose tariffs and might justify most (if not all) of the tariffs at issue in this case.”

Then Kavanaugh – and let me remind you, this is a sitting Supreme Court Justice, and not a junior lawyer in State or DOJ – helpfully lists the alternative statutes (Section 232, 122, 201, and 301 of the Trade Act) as a roadmap for the administration to use to reinstate tariffs in other ways. (Which they did)

The supposed intellectual heir to Scalia brand of conservatism was revealed as neither. Legally incoherent, intellectually indefensible, and blatantly partisan, Kavanaugh did not write a dissent, but rather, a very long op-ed, or if you want to be less charitable, a loyalty oath dressed up in judicial robes. It will likely haunt the rest of his judicial career.

Previously:

Winners & Losers of SCOTUS Decision Striking Down Tariffs (February 20, 2026)

__________

1. Passenger vehicles, Light trucks, Medium‑ and heavy‑duty vehicles, and buses are all covered by a separate Section 232 tariffs, as are auto parts, including engines, transmissions, key electrical components, etc.

2. A few assorted dates of quotes:

The word tariff is the most beautiful word in the dictionary” -2018

“[They]will make our country rich” -2019

“Tariffs cost Americans nothing.” -2019

“The word ‘tariff’ to some people, and not very smart people, but to those people tariff is a dirty word. To me it is not a dirty word, it’s the most beautiful word there is.” Sept 15, 2024 (KNTV‑13, Las Vegas interview):

“It’s not going to raise our inflation.” -2024

“To me the most beautiful word in the dictionary is tariff. And it’s my favorite word.”-2024

“If I’m going to be president of this country, I’m going to put a 100%, 200%, 2,000% tariff. They’re not going to sell one car in the United States.” -2024

“The higher the tariff, the more you’re going to put on the value of that piece, those goods, the higher people are going to pay in shops.” -2024

“Tariffs are going to make us rich as hell, it’s going to bring our country’s businesses back that left us.” -2025

“We’re going to generate hundreds of billions in tariffs; we’ll become so wealthy we won’t know how to spend that money.” -2025

3. Lots of sycophants deserve at least a footnote:

Robert Lighthizer: U.S. Trade Representativewho was the key architect and executor of Trump’s tariff strategy

Peter Navarro: The one economist in the country who thought this wasa good idea.

Kevin Hasset: The uniquely unqualified adviser, who, despite multiple sources that correctly identified consumers as shouldering the burden for the Trump Tax, threatened NY Fed researchers for using data toshow the same. Thus, the author who wrote Dow 36,000, the most embarrassing financial book ever written, has another bit of ignominy to add to his resume.

4. Gorsuch: “Whatever else might be said about Congress’s work in IEEPA, it did not clearly surrender to the President the sweeping tariff power he seeks to wield.” WTH dude, 46 pages for THAT?

5. I don’t want to spend too much time on the structural issues with Kavanaugh’s dissent, but here are 3 problems.

1) He simultaneously argues the president has this power under IEEPA, but that the major questions doctrine shouldn’t apply in foreign affairs, and even if the court disagrees, the president has alternative authorities that make the decision moot. That’s not a coherent jurisprudential position — it’s kind words to an upset client.

Second, 61-pages?

Third, and most damning is that Kavanaugh, who supposedly is committed to judicial restraint and textualism, advocates in his dissent for (a) maximally expands executive power against the clear weight of the statutory text, (b) gave explicit political cover to route around the ruling,

The post Part II: IEEPA Tariff Ruling’s Losers appeared first on The Big Picture.

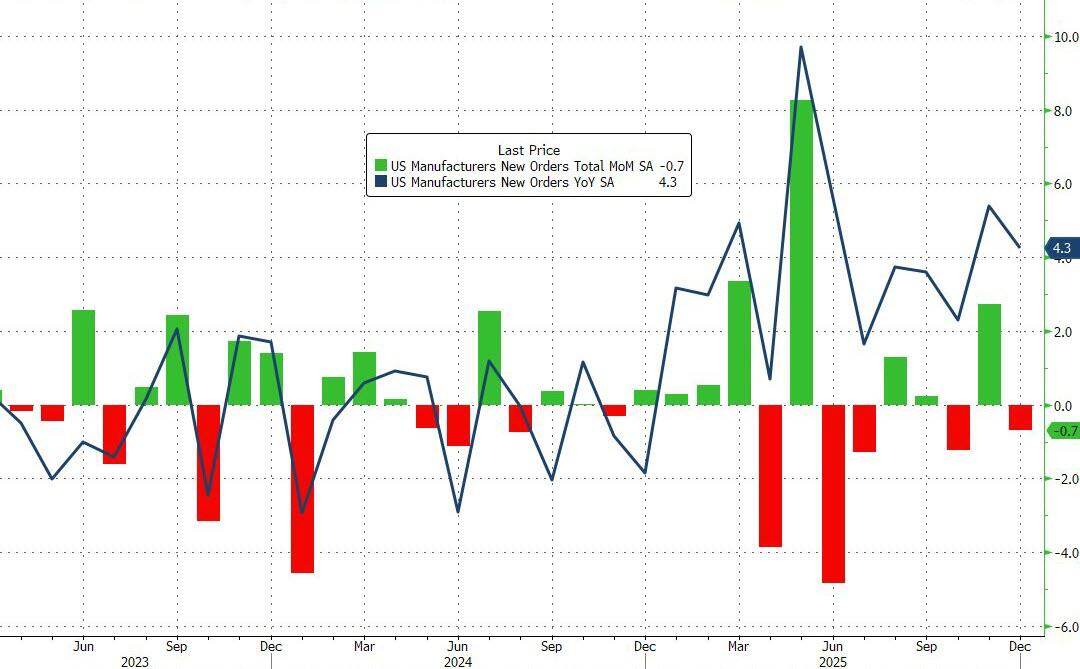

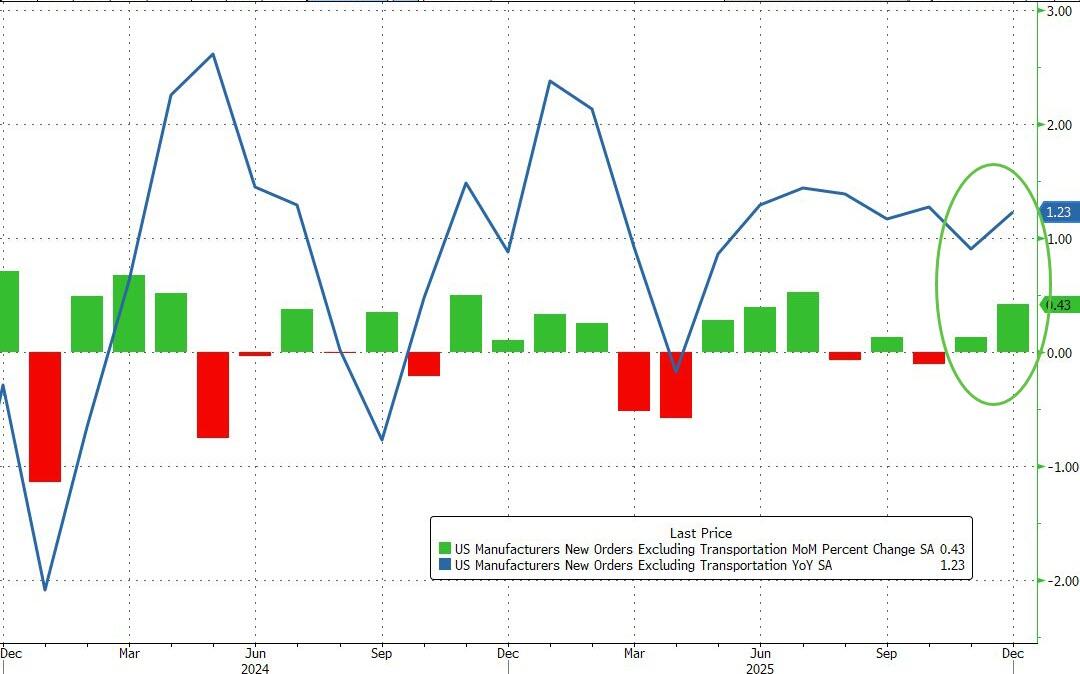

While sentiment is sagging to multi-year lows, 'hard' data is helping support growth forecasts (GDPNOW) and holding stocks at record highs.

This morning we get a fresh glimpse at America's manufacturing segment - hard data - with Orders data (which is expected to drop MoM in December).

After surging higher in November (+2.7% MoM), analysts expected US Factory Orders to drop 0.6% MoM in December but the actual print disappointed, dropping 0.7% MoM

Source: Bloomberg

Interestingly, Core Factory Orders rose 0.4% MoM - better than expected

Source: Bloomberg

The final December prints for Durable Goods Orders fell 1.4% as expected (and in line with the preliminary data).\

New orders non-defense, ex-air - a proxy for spending - rose 0.8% MoM (better than expected).

The bottom line is this data is overall supportive for GDP guesstimates (and earnings).

Tyler Durden Mon, 02/23/2026 - 10:06Update (9:40am ET): In response to the EU's decision to freeze ratification of Trump's landmark deal, the US president has come out swinging and on Truth Social threatened any countries that "play games" with the supreme court decision that they "will be met with a much higher tariff." It just isn't clear what the procedure for these much higher tariffs - aside from Section 122 which is limited to 150 days - will be now that IEEPA has been ruled unconstitutional.

Earlier:

In the aftermath of Friday's SCOTUS decision to reverse Trump's tariff policy, one lingering question is what happens to the bilateral trade deals Trump struck with various countries (and which supposedly would lead to hundreds of billions of fresh investment into the US). Well, in the case of the EU we no longer have to wonder:

The morning, the European Union said it would freeze the ratification process of its trade deal with the US and was seeking more details from the Trump administration on its new tariff program. Zeljana Zovko, the lead trade negotiator in the European People’s Party group on the US deal, said in an interview with Bloomberg that “we have no other option” but to delay the approval process to seek clarity on the situation.

The main political groups in the European Parliament say they’ll suspend legislative work on approving the trade deal on Monday, days after the US Supreme Court struck down Trump’s use of an emergency-powers law to impose his so-called reciprocal tariffs around the world.

The center-right EPP, which is the largest political bloc in parliament, will be joined by parties including the Socialists & Democrats and the liberal Renew group to back freezing the process.

According to Bloomberg, Bernd Lange - chairman of the parliament’s trade committee - called an emergency meeting later Monday to reassess the EU-US trade accord. He said over the weekend that parliament should delay work on the trade accord until the EU receives more clarity on the new tariffs. EU ambassadors will also meet Monday afternoon to discuss the US trade relationship.

Trump’s announcement following the court decision to impose a 10% global tariff, which he then increased to 15%, left many questions unanswered for American trading partners, stirring up more economic turbulence and uncertainty about the US policy.

As a reminder, the deal struck last summer between Trump and European Commission President Ursula von der Leyen would impose a 15% tariff rate on most EU exports to the US while removing tariffs on American industrial goods heading into the bloc. The US would also continue to impose a 50% tariff on European steel and aluminum imports. The bloc agreed to the lopsided deal in the hopes of avoiding a full-blown trade war with Washington and retaining US security backing, particularly with regards to Ukraine. Parliament had been aiming to ratify the agreement in March.

The trade deal had already faced a rocky path to ratification. After the initial agreement, the US expanded its 50% metals tariff to hundreds of additional products, angering EU lawmakers and European officials. Trump’s Greenland threats amplified that frustration, leading some to call for the deal to be canceled.

EU lawmakers froze the approval process once before, after Trump threatened to annex Greenland. After Trump backed down from his push to annex Greenland, a Danish territory, EU lawmakers briefly restarted the trade deal ratification process. But they also introduced changes such as a sunset clause, meaning that even if parliament ultimately approves the agreement, it will have to go back to other EU institutions for further negotiations.

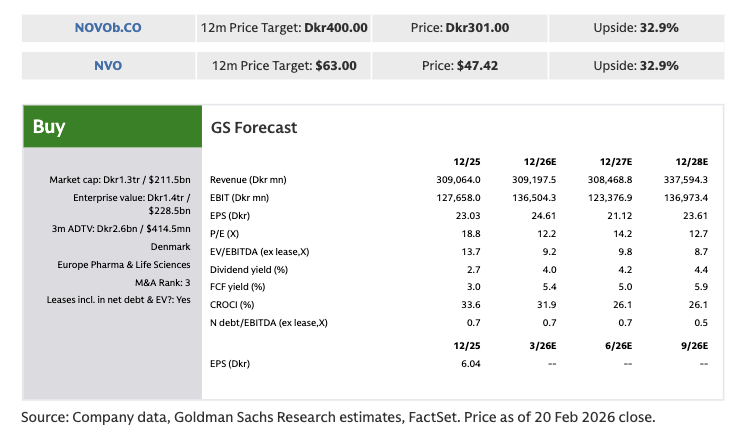

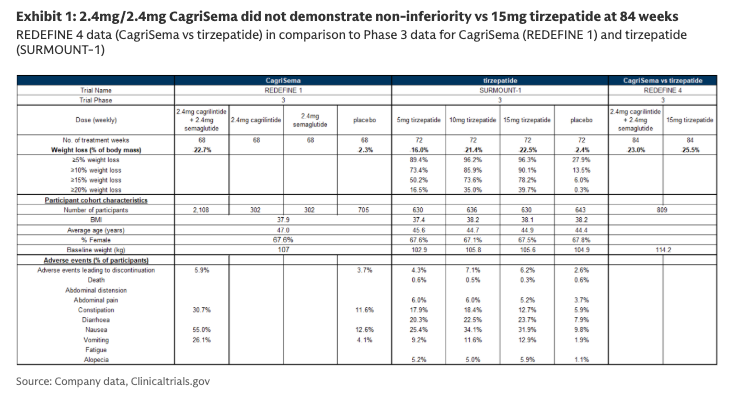

Tyler Durden Mon, 02/23/2026 - 09:36Shares of Novo Nordisk A/S plummeted again on Monday after the company reported trial results showing its next-generation obesity shot, CagriSema, delivered 20.2% weight loss at 84 weeks, compared to 23.6% for Eli Lilly & Co.’s tirzepatide (Zepbound).

Bloomberg Intelligence analyst Michael Shah explained, "This outcome is the worst-case scenario for Novo and heightens the need for M&A with Novo’s other GLP-1/Amylin drug."

Shares of Novo in Copenhagen plunged as much as 16.5%, breaking below a support level that had held since August 2025. The stock is now down about 75% from its 2024 peak and is near its 2021 low.

The result is yet more trouble for Novo’s new leadership, led by Mike Doustdar, following Lars Fruergaard Jørgensen's recent exit, along with board turnover linked to disagreements over a turnaround plan to regain GLP-1 market share. There’s also the copycat GLP-1 compounding issue involving the telehealth firm Hims & Hers.

Novo’s strategy revolves around CagriSema as Wegovy and Ozempic face longer-term patent pressure; it combines semaglutide and another gut hormone called amylin. Early studies have shown mixed results, and at least one large trial failed to meet Novo’s targeted weight loss.

Another CagriSema trial, due later this year, could yield better results because it aims to move patients to the highest dose.

“Clearly this weakens Novo Nordisk’s competitive stance in the obesity market - especially if the obesity market develops into a ‘winner takes it all’ market,” Danske Bank Credit Research analyst Brian Borsting wrote in a note. “That said, we continue to believe that Novo Nordisk’s product portfolio in the obesity market is diversified and solid although we see today’s news as credit negative.”

Meanwhile, Goldman analyst and Novo super bull James Quigley provided clients with an update on the CagriSema trial:

This morning (23rd February), Novo announced that CagriSema did not achieve the primary endpoint of non-inferiority in REDEFINE-4, with weight loss of 23% for the CagriSema arm vs. 25.5% for the tirzepatide 15mg arm, after 84 weeks of treatment. Previously, we had said that in a non-inferiority scenario, taking the PoS of CagriSema down to 0% in obesity, leaving $5bn in sales only for cagrilintide monotherapy, would lead to a -12% impact to our DCF, all else equal, but noted that investor expectations were likely lower for CagriSema. These data points could further reduce market expectations for CagriSema, even ahead of the REDEFINE 11 trial (1H'27), and while we continue to expect approval for CagriSema and likely some use by physicians as part of a portfolio approach in obesity, investors are not likely to give credit here until the sales start to come though post approval. Novo is looking to explore higher doses of CagriSema with a Phase 3 trial planned for 2H26 - although we believe investors are unlikely to give any credit until the sales trajectory is seen. Therefore, given our expectations noted above, the share price reaction at the time of writing of c.-12% appears in line, as any residual potential for CagriSema moves out of the expectations built in for the stock. Continued momentum for the launch of the Wegovy pill is even more important, we believe, as shifting volumes to the oral market could be advantageous, given Novo has a more competitive profile on weight loss.

CagriSema failed to meet the primary endpoint of demonstrating non-inferiority vs tirzepatide on weight loss at 84 weeks. On an efficacy-estimand basis, 2.4mg/2.4mg CagriSema showed -23.0% weight loss at 84 weeks, vs 25.5% weight loss with 15mg tirzepatide over the same time period. On a treatment-regimen estimand basis, CagriSema showed -20.2% weight loss at 84 weeks vs -23.6% with 15mg tirzepatide. As a result, REDEFINE-4's primary endpoint of CagriSema demonstrating non-inferiority on weight loss vs tirzepatide was not reached.

CagriSema showed a well-tolerated safety profile, per Novo. While no tolerability data was given, in the release Novo said that overall CagriSema appeared to show a well-tolerated and safe profile, with the most common AEs being GI AEs. Of these, the vast majority were mild to moderate and improved over time, which was consistent with other drugs in the GLP1 agonist class.

In terms of next steps, Novo anticipates a decision from the FDA on CagriSema by y/e 2026. This is following the company's submission to the FDA in December 2025 based on data from REDEFINE 1 and 2. Novo also expects to initiate an additional Phase 3 trial of higher dose CagriSema in 2H26, and expects the readout from REDEFINE 11 of 2.4mg/2.4mg CagriSema in 1H27 (longer term trial looking at the full weight loss potential of CagriSema in obesity).

Not surprisingly, Quigley's continued "Buy" rating on the stock even as it has collapsed 75% from the peak and nears 2021 lows. "We are Buy rated on Novo Nordisk," he said.

Related:

"Big Miss": Wall Street Disappointed After Dismal Novo Nordisk GLP-1 Sales Outlook, Shares Plunge

GLP-1 Feud: HIMS Fires Back At Novo Nordisk, Slams Lawsuit As "Blatant Attack" By Big Pharma

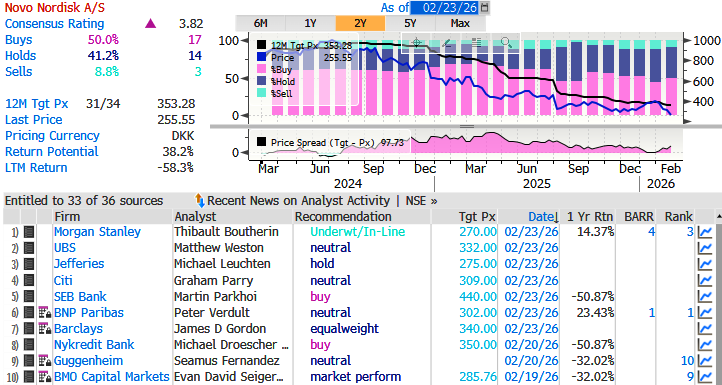

Bloomberg data shows 17 "Buy" ratings, 14 "Hold" ratings, and 3 "Sell" ratings on Novo. The average 12-month price target among Wall Street analysts is 353 kroner.

How many Goldman clients are furious with Quigley's Novo coverage?

Tyler Durden Mon, 02/23/2026 - 09:25The post The Grand Illusion: The US – Europe Growth Gap appeared first on CEPR.

When former President Barack Obama announced plans for his presidential center on Chicago’s South Side, he described it as a privately funded investment in the city that would give back to the community that shaped his political career.

Former President Barack Obama is pictured next to construction of the Obama Presidential Center in Chicago, a project facing delays, soaring costs and mounting scrutiny over its finances. (Scott Olson/Getty Images; Reuters/Vincent Alban) via Fox News

Former President Barack Obama is pictured next to construction of the Obama Presidential Center in Chicago, a project facing delays, soaring costs and mounting scrutiny over its finances. (Scott Olson/Getty Images; Reuters/Vincent Alban) via Fox News

And while construction of the brutalist eyesore itself remains privately financed through the Obama Foundation, taxpayers are footing the bill for massive infrastructure costs.

A review by Fox News found that state and city agencies have not produced a unified accounting of total public expenditures tied to the project’s surrounding infrastructure. While individual agencies have disclosed partial figures, no single office has reconciled those totals or clarified how they overlap.

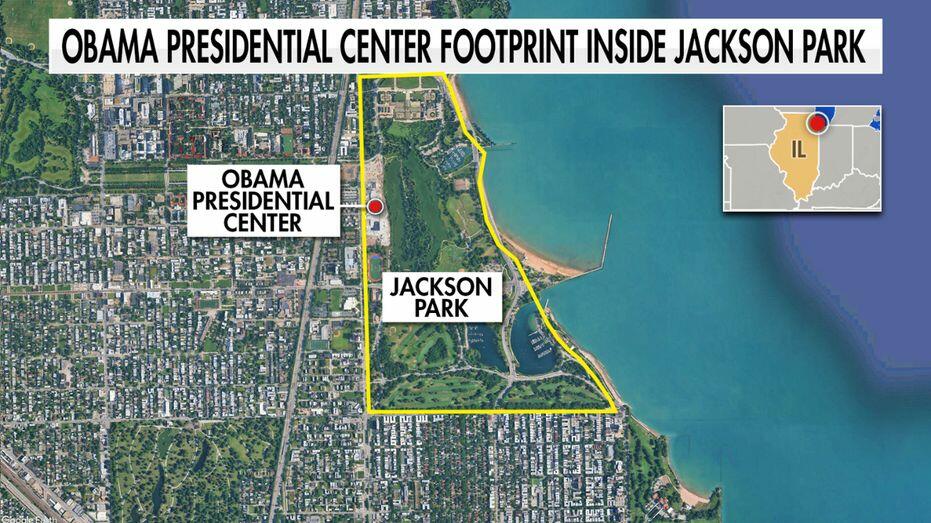

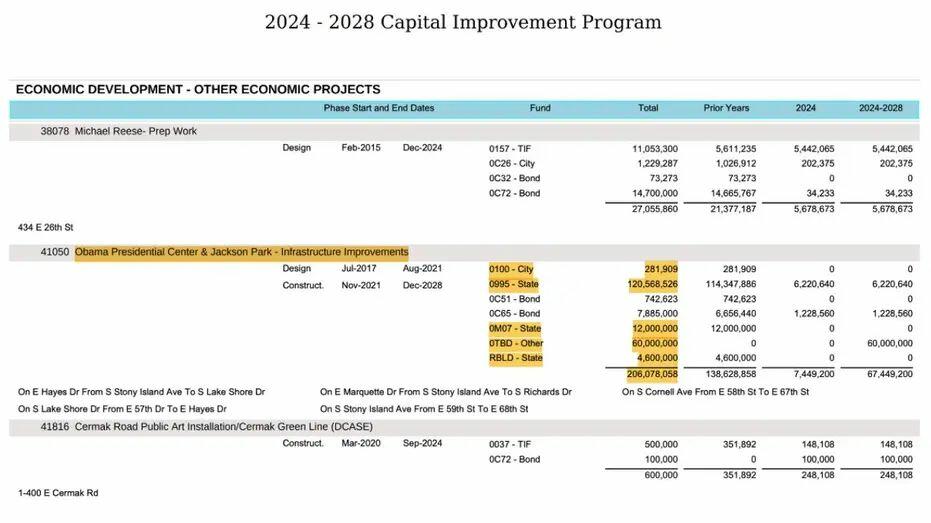

At the time the project was approved in 2018, public infrastructure costs were projected at roughly $350 million, to be split between the State of Illinois and the City of Chicago. Those estimates covered roadway modifications, utility relocations and related improvements necessary to accommodate the 19.3-acre campus in Jackson Park that nobody asked for.

In July, the Illinois Department of Transportation said that approximately $229 million in state-managed infrastructure spending had been committed to the project. That total includes about $19 million for preliminary engineering, $24 million for construction engineering and $186 million for construction activities. A department spokesperson described the earlier $174 million figure as a preliminary 2017 estimate.

Now, Chicago’s most recent 2024–2028 Capital Improvement Plan lists more than $206 million allocated to roadway and utility work associated with the project. However, much of that funding is labeled as “state,” and neither state nor city officials have clarified how the figures relate to one another or whether they represent overlapping commitments.

A map graphic shows the footprint of the Obama Presidential Center inside Jackson Park on Chicago’s South Side along Lake Michigan. (Fox News)

A map graphic shows the footprint of the Obama Presidential Center inside Jackson Park on Chicago’s South Side along Lake Michigan. (Fox News)

Fox submitted records requests to several agencies, including the Illinois Department of Transportation, Chicago’s Department of Transportation, the city’s Office of Budget and Management, the mayor’s office and Gov. J.B. Pritzker’s administration - yet, not one provided a consolidated, up-to-date accounting of total public infrastructure spending. The Illinois Attorney General’s Public Access Counselor is reviewing whether agencies complied with state transparency laws in responding to the requests.

The Obama Foundation defended the project, reiterating that the center’s construction - whose cost has grown from early projections of roughly $330 million to at least $850 million, according to its 2024 tax filings - is being financed by private donations. In a statement to Fox, foundation spox Emily Bittner said the organization is “investing $850 million in private funding to build the Obama Presidential Center and give back to the community that made the Obamas’ story possible,” adding that the project is intended to catalyze economic opportunity on the South Side. Bittner, of course, didn't address the infrastructure costs - which have been extensive.

Chicago’s 2024–2028 Capital Improvement Program lists $206,078,058 for "Obama Presidential Center & Jackson Park – Infrastructure Improvements," with most funding labeled as state sources. (City of Chicago Capital Improvement Program)

Chicago’s 2024–2028 Capital Improvement Program lists $206,078,058 for "Obama Presidential Center & Jackson Park – Infrastructure Improvements," with most funding labeled as state sources. (City of Chicago Capital Improvement Program)

Cornell Drive, a four-lane roadway along the eastern edge of Jackson Park, was removed and traffic rerouted farther west. Utilities, including water mains and sewer lines, were relocated, and new drainage systems were installed. City and state officials have said the changes were necessary to manage anticipated traffic and visitor demand.

The center occupies 19 acres of public parkland transferred under a 99-year agreement for $10, a decision that prompted legal challenges arguing that the arrangement was not in the public interest. Courts ultimately dismissed those lawsuits.

Though often described as a presidential library, the Chicago complex will not function as a traditional library operated by the National Archives and Records Administration. Former President Obama’s official records will be maintained by the federal government at a facility in Maryland, while the Chicago site will be operated privately by the Obama Foundation.

The foundation also pledged to establish a $470 million endowment intended to protect taxpayers in the event the project encounters financial difficulty. According to previous reporting by Fox News, that fund has received $1 million in deposits.

Who didn't see this coming?

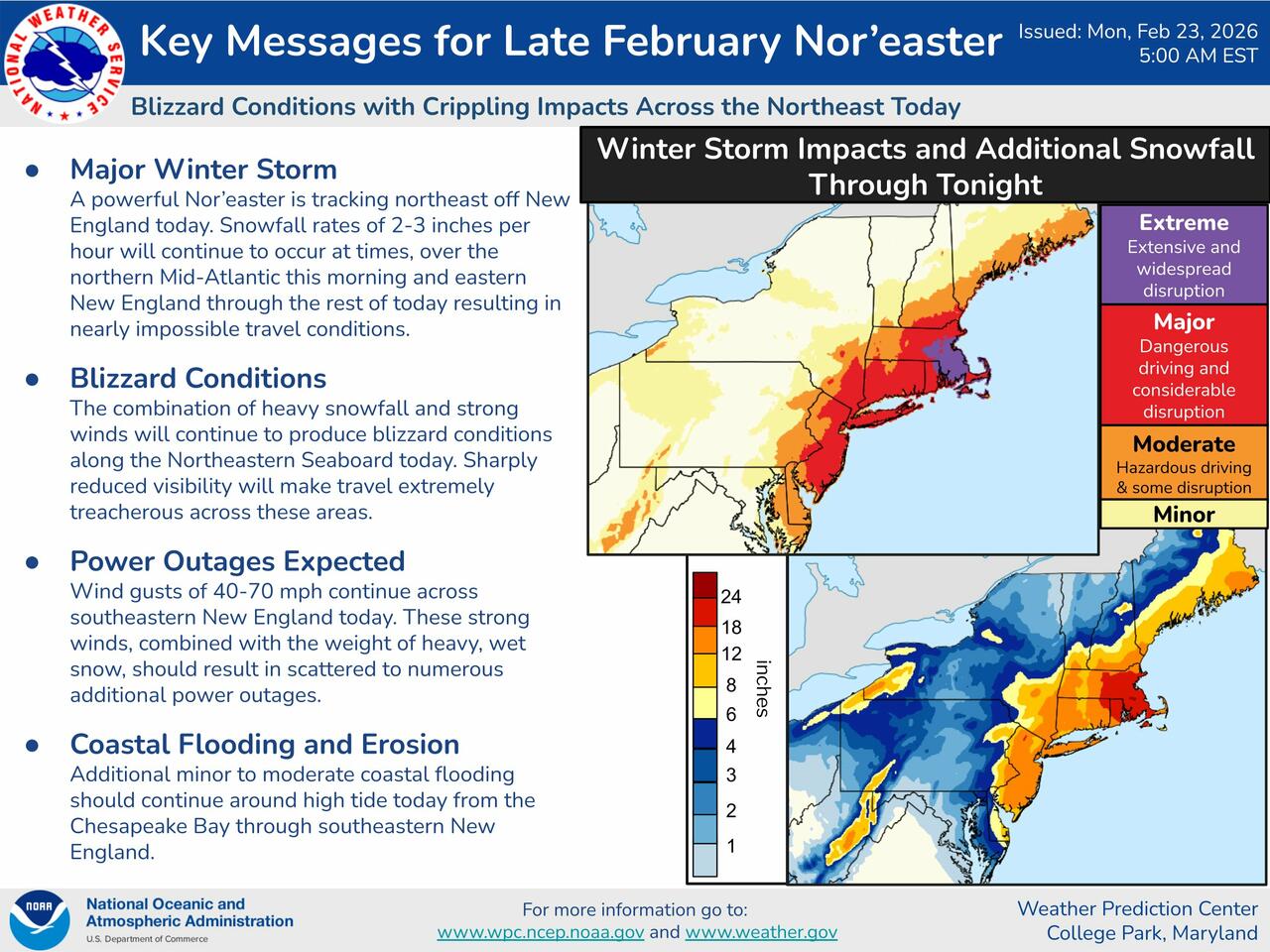

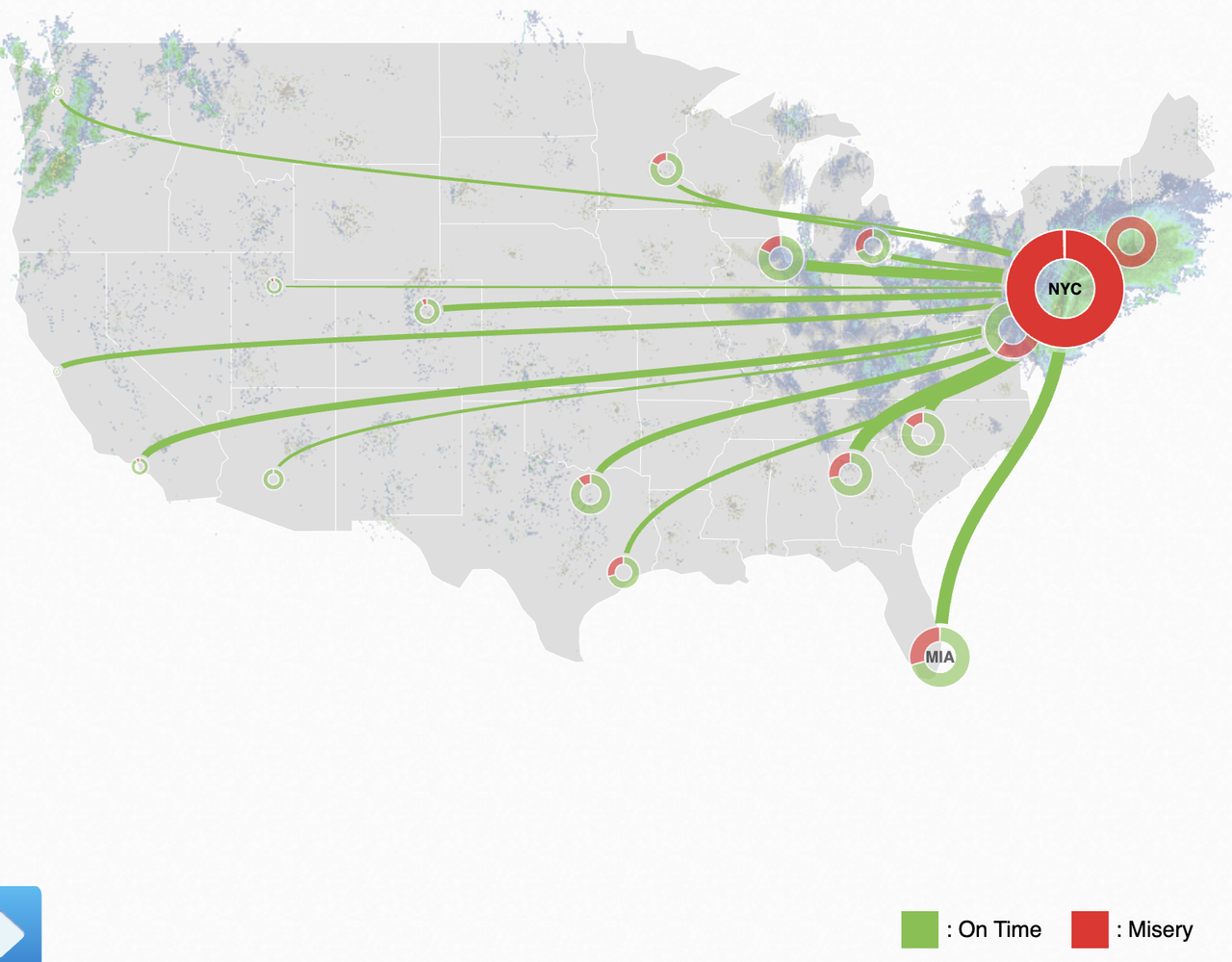

Tyler Durden Mon, 02/23/2026 - 07:45Blizzard conditions are expected from Delaware into southern New England, and travel will be "extremely treacherous" to "nearly impossible" today, according to the National Weather Service Weather Prediction Center.

Expect travel delays along the I-95 corridor, as well as flight cancellations at airports from the Mid-Atlantic to the Northeast.

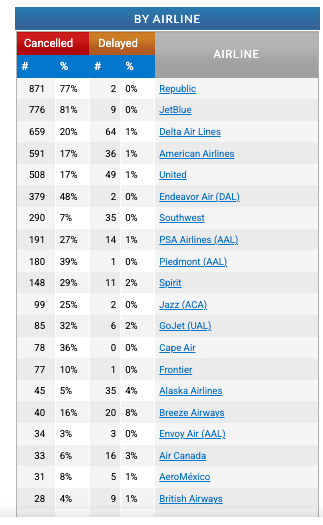

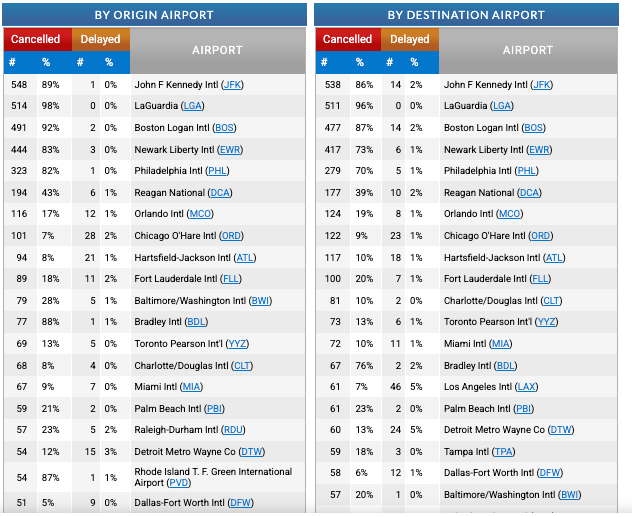

Nearly 5,600 flights in, out, or within the US were cancelled at the start of the week, according to flight-tracking website FlightAware.

Travel nightmare for Republic Airways, JetBlue, Delta Air Lines, American Airlines, and United early Monday morning, with the bulk of the cancellations affecting these airlines.

Airports in the Mid-Atlantic and Northeast, such as John F. Kennedy International Airport, LaGuardia, Boston, Newark, and Philadelphia, experienced the highest number of cancellations and delays.

Here's a map of the flight misery as of 0630 ET.

The heaviest snowfall, as much as two feet in some locations across the Mid-Atlantic and Northeast areas, fell in the overnight hours and will continue into the morning, NWS warned in the most recent update.

Besides the unfolding travel chaos, nearly a quarter million customers are without power this morning because of the blizzard conditions, with a large percentage of the outages concentrated from Delaware to New Jersey.

Over a quarter million people are waking up this morning without power in the Northeast due to blizzard conditions.

— BAM Weather (@bam_weather) February 23, 2026

Over 15" of snow has fallen in some locations and 50-60+ MPH gusts have been recorded along the coast.

Snow and strong winds continue today. pic.twitter.com/RKS693uskf

Anyone planning to travel into NYC or out of it, well, forget about it, because Mayor Zohran Mamdani declared a state of emergency and closed streets, highways, and bridges to most traffic from late Sunday through Monday afternoon. His collective army of snow shovelers will save the day.

"These are blizzard conditions. New York City has not faced a storm of this scale in the last decade," Mamdani said. "We have activated additional high-water rescue teams should flooding grow dire."

How do the blizzard and winter blast compute in the minds of Mamdani's followers after years of being brainwashed about the global warming crisis?

Meteorologist Ryan Maue looks ahead:

That monstrous Greenland "polar vortex" cold pool is the "Final Boss" ... goes toward Alaska in a week.

— Ryan Maue (@RyanMaue) February 23, 2026

Then it heads Southeast into the Lower 48 to crash into the Great Lakes and Northeast by Day 12 (March 6th) ... from ECMWF HRES 00z

Coldest of winter in March! pic.twitter.com/xJ9vFXrX1i

Winter isn't over.

Tyler Durden Mon, 02/23/2026 - 07:20As the world watches unchecked immigration fundamentally transform the West, a growing backlash has gained a foothold - and it's made it to the ballot box.

In Alberta, Canada, Premier Danielle Smith announced a referendum this fall to decide whether the province should limit the number of new international, temporary foreign workers and asylum seekers - as Alberta seeks to take charge of the issue amid a surge of proud Canadians who do not embrace change.

As Reuters notes;

The move, announced by Premier Danielle Smith in a televised address on Thursday evening, represents an attempt by Alberta to wrest control of a key issue from the federal government. Immigration policy in Canada is primarily the responsibility of Ottawa, not the provinces.

It is also an attempt by Smith to ward off a simmering Alberta separatism movement, which has threatened Canadian unity as Prime Minister Mark Carney makes efforts to improve relations with western, resource-rich provinces in the face of economic challenges posed by U.S. President Donald Trump's trade policy.

Giving citizens a say on immigration policy is the government's way of giving Albertans hope that the Canadian federation can work, Smith told reporters on Friday.

Smith has also blamed Alberta's financial woes on immigrants - noting that a surge of over 600,000 migrants over the past five years, putting Alberta's population over 5 million in 2025 - has put a strain on provincial resources.

"Throwing the doors wide open to anyone and everyone across the globe has flooded our classrooms, emergency rooms and social support systems with far too many people, far too quickly," she said.

Pissed Swiss Want Population CapMeanwhile in Switzerland, a landmark vote is set for June 14 that would cap the nation's population at 10 million from its current 9.1 million.

The proposal has been put forth by the country's largest political coalition, the Swiss People's Party (SVP), and would require the government to refuse entry to all migrants - including those 'asylum' seekers who go home to party when the weather is nice.

Hitting 10 million residents would also force Switzerland to end its free-movement agreement with the EU. Of note, the EU and Switzerland are integrated through more than 120 bilateral agreements, which grants it access to the EU single market and the free movement of people and trade in goods, CNN reports.

SVP argues that Switzerland is undergoing a 'population explosion,' that is straining resources and infrastructure, and inflating rents.

According to a 2025 poll by Swiss-based polling firm Leewas, the proposal has wide support.

Tyler Durden Mon, 02/23/2026 - 06:55My snowed-in-Nor’easter-Blizzard WFM morning reads:

• Amazon takes the No. 1 spot on the Fortune 500, ending Walmart’s 13-year run. Amazon finally overtook Walmart atop the Fortune 500, a coronation for the company that essentially invented e-commerce and now dominates 40% of U.S. digital retail. It figured out how to develop a practical, easy way to shop online and take it mainstream. The Seattle company now dominates the U.S. market — 180 million Americans have a Prime account. But Amazon didn’t overtake a rival with a 32-year head start by remaining wedded to one line of business or following one approach to running it. (Fortune)

• Hedge fund Saba offers to buy stakes in Blue Owl funds at steep discount: Boaz Weinstein’s Saba Capital is making an aggressive play for Blue Owl fund stakes, offering to buy them at a significant markdown, as private credit group is seeking to shore up investor confidence (Financial Times) see also Boaz Weinstein Is Hunting Blue Owl’s Funds: The hedge-fund manager is adding private credit to his crusade against funds sold to individual investors. (I am always interested when the manager who discovered the London Whale and beat Blackrock’s proxy spots a problem elsewhere). The activist hedge fund manager is circling Blue Owl’s closed-end funds, looking for discounts and willing to fight for them. (Wall Street Journal)

• The Reign of the Dollar Is Coming to an End. What Investors Can Do About It. The dollar’s dominance as the world’s reserve currency is eroding — slowly, then perhaps all at once. How to position portfolios for the shift?Consider investment in foreign stocks and debt juiced by a falling dollar. (Barron’s)

• How Zoning Won: In 1926, the Supreme Court’s Euclid decision enshrined zoning in US cities. At 100 years old, Euclidean zoning — the system that separates homes from businesses from industry — the landmark ruling’s mixed legacy has become America’s most durable and least questioned land-use policy. It may finally be overdue for reform. (Bloomberg)

• Stock Slide and Slow Sales: What’s Happening in China’s E.V. Market? The Chinese EV juggernaut is showing cracks — slowing domestic sales, falling share prices, and a price war that’s squeezing margins across the board. Investors are selling shares of Chinese E.V. companies, concerned that intensifying competition and shorter production cycles mean the years of easy growth are over. The global implications for legacy automakers and battery supply chains are significant. (New York Times)

• How Hamilton Lane extracted more money from its ‘NAV squeezing’ The FT digs into how one of private equity’s biggest players is gaming NAV lending to juice returns. If you don’t understand the plumbing, you’re the one getting squeezed. It’s a good example of what can happen when private capital firms seek to tap less sophisticated retail investors to replace retrenching institutional investors — something that even some industry insiders warn will end in tears — in an era where many financial watchdogs are being neutered. (We read proxy statement so you don’t have to). (Financial Times)

• The Media Can’t Stop Propping Up Elon Musk’s Phony Supergenius Engineer Mythology: “CEO said a thing!” journalism is now utterly pervasive, and includes parroting billionaire and CEO claims with a total disregard for whether or not anything being said is actually true. The press keeps treating Musk as a hands-on engineering visionary. The evidence overwhelmingly suggests otherwise. (Karl Bode)

• ‘Is university still worth it?’ is the wrong question: UK graduates are struggling — but the real issue isn’t whether degrees have value. It’s that the economy has fundamentally changed around them. The graduate earnings premium isn’t really measuring what most people think. (Financial Times)

• Look how much Canadians hate the United States now: It’s not just about the trade war. Nearly half of America’s neighbors to the north now think the U.S. is a bigger threat to world peace than Russia. Five charts showing the dramatic collapse in how Canadians view their southern neighbor. The damage to the relationship may be lasting. (Politico)

• The Multibillion-Dollar Foundation That Controls the Humanities: The Andrew W. Mellon Foundation’s $540 million in annual grants wields near-monopolistic power over humanities scholarship. Is it the last best hope for American arts and letters—or is it killing them? (The Atlantic)

Be sure to check out our Masters in Business interview this weekend with Hilary Allen, Professor of Law at the American University Washington College of Law. She specializes in financial regulation, banking law, securities regulation, and technology law, with a particular focus on how new financial technologies like fintech, crypto, and AI intersect with financial stability and public policy.

The giant void of nothingness where US financial regulation used to sit

Source: Financial Times

Sign up for our reads-only mailing list here.

The post 10 Monday AM Reads appeared first on The Big Picture.

For years, anyone who questioned whether Washington’s intelligence machinery tilted left was told they were peddling conspiracies. That narrative fell apart on Friday, when CIA Director John Ratcliffe ordered the official retraction or major revision of nineteen intelligence products produced during the Obama years, citing political bias and substandard analytic tradecraft. It’s the first official acknowledgment that America’s most powerful spy agency let politics color its assessments.

"The intelligence products we released to the American people today — produced before my tenure as DCIA — fall short of the high standards of impartiality that CIA must uphold and do not reflect the expertise for which our analysts are renowned," Director Ratcliffe said in a statement. "There is absolutely no room for bias in our work and when we identify instances where analytic rigor has been compromised, we have a responsibility to correct the record. These actions underscore our commitment to transparency, accountability, and objective intelligence analysis. Our recent successes in Operation ABSOLUTE RESOLVE and Operation MIDNIGHT HAMMER exemplify our dedication to analytic excellence.”

The bombshell came after the President’s Intelligence Advisory Board (PIAB) completed an independent review of hundreds of finished CIA reports spanning the past decade. This period includes Barack Obama’s second term and the Russian collusion hoax.

The PIAB identified nineteen intelligence products that “failed to be independent of political consideration.” Deputy Director Michael Ellis led an internal review that confirmed the findings. Ratcliffe’s response was swift and blunt. “The intelligence products we released to the American people today — produced before my tenure as DCIA — fall short of the high standards of impartiality that CIA must uphold and do not reflect the expertise for which our analysts are renowned,” he said. “There is absolutely no room for bias in our work… These actions underscore our commitment to transparency, accountability, and objective intelligence analysis.”

That’s a rather diplomatic way of saying that Barack Obama’s CIA got caught red-handed playing politics. The agency admitted that at least some of its Obama-era intelligence relied on questionable sourcing, including political activist groups. One report even drew on material from Planned Parenthood, something one official described as “clearly not an appropriate use of CIA resources.” For an organization that prides itself on independence and tradecraft, that revelation is a true humiliation.

CANCELLED: 19 @CIA intelligence products officially retracted over “inappropriate insertion of DEI issues" and failure to meet "objectivity" standards, per senior CIA official.@CIADirector Ratcliffe ordered the removal of 17 intelligence products from CIA databases + 2 reports… pic.twitter.com/UdaHp6S8Gh

— Catherine Herridge (@C__Herridge) February 20, 2026

The implications stretch far beyond nineteen flawed reports. The time frame under review encompasses the same period that produced the now infamous 2017 Intelligence Community Assessment (ICA) — the document commissioned in the last days of the Obama administration and released just before Donald Trump’s inauguration, alleging Russian interference in the 2016 election.

That assessment relied heavily on the debunked Steele Dossier and cast a dark cloud over President Trump’s first term, giving Democrats cover to claim Trump was an illegitimate president.

If nearly twenty reports from that same era failed to meet analytic standards due to political bias, the question is no longer whether the intelligence community was politicized; it’s how deep the rot went.

However, Democrats clearly aren’t convinced.

Sen. Mark R. Warner (D-Va.), the top Democrat on the Senate Select Committee on Intelligence, dismissed the retractions, insisting that “the strength of the Intelligence Community has always depended on its ability to deliver objective, apolitical analysis, grounded in rigorous tradecraft and insulated from political pressure.” He emphasized that such judgments “must be made by intelligence professionals and not subject to politics.”

Warner warned that when politically appointed bodies “appear to be dictating what analysis is acceptable, it risks eroding confidence in the objectivity of our intelligence.” He described the CIA’s action as part of a “broader and deeply troubling pattern in this administration: sidelining career experts, undermining inconvenient intelligence assessments, and allowing political considerations to override professional judgment.”

Senator Tom Cotton (R-Ark.), the chairman of the Senate Select Committee on Intelligence, however, welcomed the retractions. “The Obama and Biden administrations mixed intelligence analysis and politics far too often,” Cotton said in a post on X. “I commend Director Ratcliffe for correcting the record and ensuring that the CIA’s analysis is free of any political bias.”

He added, “I’ve been sending these kind of reports back to the CIA for years and observing that they contain no intelligence. Our intelligence agencies have too often missed critical national-security developments to waste time on, for instance, how ‘pandemic-related contraceptive shortfalls threaten economic development.’ Honestly.”

Tyler Durden Mon, 02/23/2026 - 05:45

Recent comments