H.R. 7036, Data Driven Diplomacy Act

As ordered reported by the House Committee on Foreign Affairs on January 21, 2026

Speak Your Mind 2 Cents at a Time

Authored by T.J.Muscaro via The Epoch Times,

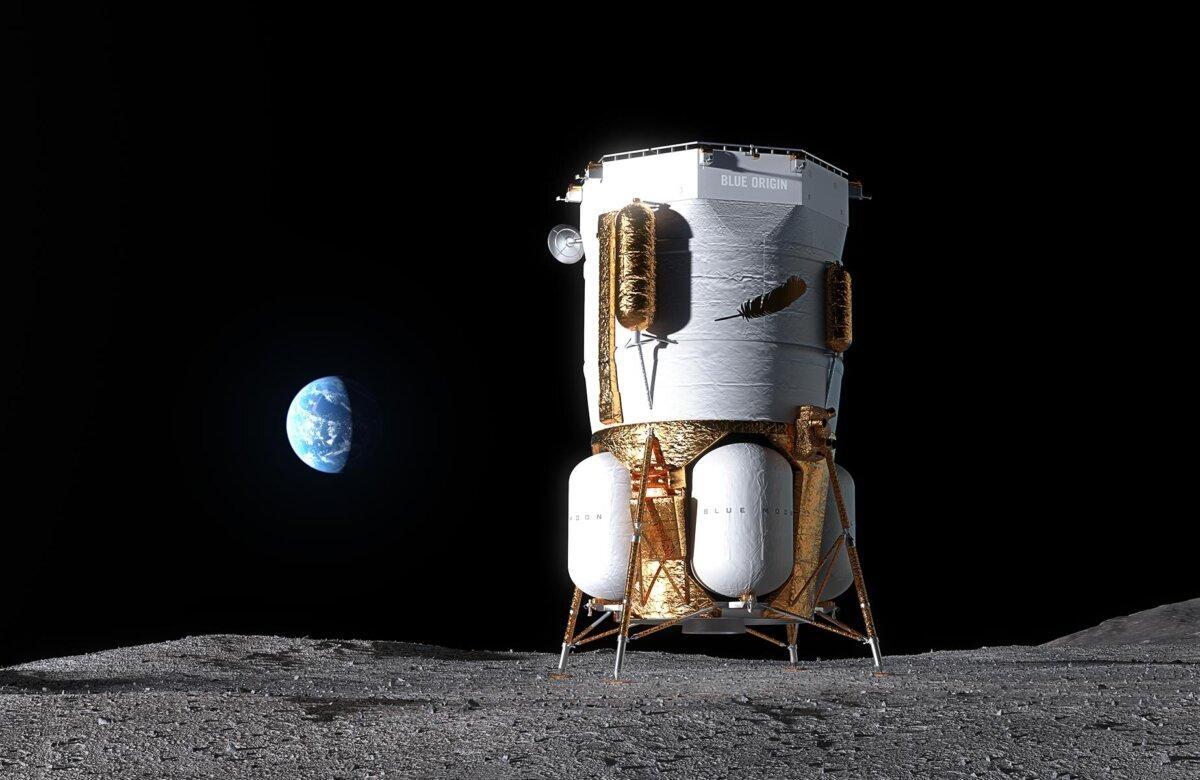

Blue Origin decided to shift its focus from the edge of space to the Moon.

The company announced on Jan. 30 that it was pausing all of its suborbital commercial flights on its reusable New Shepard rocket for no less than two years in order to focus more resources on delivering a crewed lunar lander to NASA in time to meet Congress’s set deadline to establish a permanent human presence on or around the moon by 2030.

“The decision reflects Blue Origin’s commitment to the nation’s goal of returning to the Moon and establishing a permanent, sustained lunar presence,” the company said in a statement.

January saw Blue Origin achieve successes on both fronts. Its Blue Moon MK-1 lander Endurance was shipped from its assembly facility at Cape Canaveral to Johnson Space Center in Houston on Jan. 20 to undergo critical testing.

“Named for Ernest Shackleton’s legendary ship that journeyed to Earth’s South Pole, MK1 honors resilience under pressure,” Blue Origin said on X. ”That same spirit of perseverance guides our mission to the lunar South Pole.”

The MK-1 lander is the first phase of Blue Origin’s plan. Designed as an unmanned cargo transport, the company explained on its website that this first one will be used for what it called the “Pathfinder Mission.”

That will be a demonstration mission that proves out the critical systems of both the lander and the New Glenn rocket that will carry it. Along with propulsion, communications, and avionics, this mission must also demonstrate a precision landing within 100 meters of a chosen site. This was intended to occur before NASA’s uncrewed Human Landing System mission for the Artemis Program.

In its full form, the MK-1 will enter commercial service as a lunar cargo lander designed to remain on the lunar surface and provide affordable, safe, and reliable access to the Moon.

Rendering of Blue Origin’s Blue Moon MK-1 Lander on the lunar surface. Blue Origin

MK-2 will be a crewed landing craft built and operated in accordance with NASA standards.

NASA previously had an agreement with Elon Musk’s SpaceX to provide the lunar lander that would return humans to the surface for the first time since 1972 during the Artemis III mission. However, acting NASA administrator Sean Duffy reopened the mission to competition.

“We are in a race against China, so we need the best companies to operate at a speed that gets us to the Moon FIRST,” Duffy said on X.

“SpaceX has the contract to build the [Human Landing System], which will get U.S. astronauts there on Artemis III. But, competition and innovation are the keys to our dominance in space so @NASA is opening up HLS production to Blue Origin and other great American companies.”

NASA’s new full-time administrator, Jared Isaacman, agreed with his predecessor’s decision and visited Blue Origin’s facilities on Jan. 15.

Meanwhile, the 38th New Shepard mission was successfully completed on Jan. 22, carrying another six humans on an autonomous ride from a launch site in West Texas to above the Karman Line—the internationally-recognized boundary of outer space—and back.

The operation has carried more than 90 individuals and more than 200 scientific and research payloads over those commercial ventures, including the first all-female multi-person crew to fly to space.

The company noted in its press release that it has built a multi-year customer backlog, which it attributes to the rocket’s consistent, reliable performance and customer experience.

“We’re focused on continuing to deliver transformational experiences for our customers through the proven capability and reliability of New Shepard,” New Shepard senior vice president Phil Joyce said after the latest mission.

Tyler Durden Mon, 02/02/2026 - 17:00Authored by James Howard Kunstler,

The political grandstanding started way back in 1973 when the irascible Marlon Brando stayed home from the Academy Awards but sent an Apache princess, one Sacheen Littlefeather, to the podium to decline his award (Best Actor for The Godfather) on account of the 71-day standoff at the Pine Ridge Indian Reservation in South Dakota between federal agents and Oglala Lakota activists who had seized the little town of Wounded Knee.

After that, political “statements” at awards ceremonies of all kinds became modish, then obligatory, and now in the age of Lefty-left Woke Jacobin activism, all you get is one denunciation after another of the monster who lives in their heads: ChrumpChrumpChrump. Cue the audience of fellow “stars” for the also obligatory standing-O, which is really a test to see if any among them dare not join in the hosannahs — so they can be anathemized.

You are seeing sheer ritual performance by performers, the highest perq of stardom being the approbation of their peers, fellow performers — nevermind the lowly gorks out in Flyover Land who “consume” the products of pop culture. This is cliché narcissism-on-parade, of course, and is now so completely institutionalized in the pop culture industries that seemingly all actors, musicians, dancers, mimes, comics, and literary figures must act-out an activist fantasy or face the pretty extreme punishment of being run out of their business.

It’s all fake and pathetic, and the more they do it, the more their various culture industries suffer — to the point now that feature production in Hollywood was down over 16-percent in 2025. It’s dying in a self-reinforcing doom-loop. The reason is no secret, but it is dangerous to speak of it: the management of our “sense-making” institutions — movies being an important one — has been taken over by women (and womanish men) acting out Cluster-B psychodrama fantasies obsessively attacking “the patriarchy” — by which they mean (but cannot say) civilization itself, the thing sedulously built by men.

The latest wrinkle in this tragic saga is the psychodrama over ICE, the men tasked with finding and deporting people who came into the country illegally. The Cluster-B women mis-direct their nurturing instincts to rescue this politically-designated “oppressed minority,” overlooking the fact that not a few of these illegal aliens turn out to be murderous psychopaths. Conveniently, too, the illegal aliens also happen to be a very useful device for the Democratic Party to pad the census and provide illicit votes, all to keep the party in power and sustain its rackets.

President Trump completes the doom-loop circle because he is the mythic figure who prompts all the anxiety behind the “mass formation” phenomenon we are witnessing. Mr. Trump is patriarchy-in-action, so he must be destroyed by the goddess-heroines of show business. The goddess-heroines seem to believe they are ushering-in a Utopia of Nurture in which no oppressed minority will be left behind. That fantasy happens to intersect with the leveling fantasies of Karl Marx and his apostles, the mentors of the obscenely-rich denizens of Hollywood so eager to abolish obscene riches. So, you see how either stupid, or mentally-ill, or both, the people in show business can be.

Last night’s awards extravaganza was the Grammys, for music.

The anti-ICE ritual flared in full effulgence with Song of the Year winner Billie Eilish - costumed not to look as a woman but rather like a piece of luggage - bathed in applause for heroically muttering, “Fuck ICE,” after picking up her little golden gramophone statuette. Perfect.

Few musicians can make a dime anymore, and a very few of those few make billions while the rest starve. The record album was the supreme art-form of my generation, and it is long gone. Record labels don’t continue to exist when there are no records. Musical acts don’t get contracts and don’t get paid. Nobody listens to FM radio anymore and so nobody is introduced to new musical talent. Live music on the small club scale is dying because the drinks cost too much. Does anyone still have a quaint old home stereo, a gigantic wall-of-sound, with four-foot-high speakers? All I’ve got is a seven-inch Bluetooth speaker.

The lively arts are dying and the remaining lively artists are assisting with the suicide.

Not far in the future, the motion picture might be a dead letter. Technology marches on.

Immersion in human experience depicted on a silver screen, using the techniques of dramaturgy, will be supplanted, we’re told, by video games that put you immersively into “a world” where a story is spinning that you can now act-out a role in.

You might see how that would entice an awful lot of people to check-out of reality altogether — and if that happens, you might well ask: who is left to run civilization?

The answer you get will be: artificial intelligence, AI. Oh, great.

But then, is it running civilization for all those pathetic people losing themselves in immersive video games? Or just for AI itself? And where does that take the human race?

Personally, I don’t expect it to work out that way. If I were disposed to investing money in the entertainment business, I’d build a theater for puppet shows.

That’s the level our civilization-destroying antics are taking us to, with the Democratic Party leading the way.

Tyler Durden Mon, 02/02/2026 - 16:20A Detroit judge, her attorney father, and two other individuals were charged by federal prosecutors in an alleged "years-long scheme" to embezzle nearly $300,000 from individuals deemed incapacitated or otherwise vulnerable.

Judge Andrea Bradley-Baskin, 46, is alleged - among other things, "to have used $70,000 in a ward’s funds to purchase an ownership stake in a local bar," and "money embezzled from the estate of a ward to pay a two-year lease on a new Ford Expedition for herself."

In addition to Bradley-Baskin, her father, Avery Bradly, 72, Nancy Williams, 59, and Dwight Rashad, 69, were charged with conspiracy to commit wire fraud and several counts of money laundering. The judge was also hit with a single count for making a false statement to a federal law enforcement agent.

Bradley-Baskin and her father Avery represented a firm that was appointed to manage the estates of incapacitated wards of over 1,000 cases, the DOJ claims. The firm, Guardian & Associates, was run by indicted co-conspirator Nancy Williams, and would siphon funds from the estates of vulnerable individuals to the judge and her father - along with to a group home operator, Dwight Rashad, officials allege.

Bradley, Rashad, and Williams are accused of stealing $203,000 from one ward's legal settlement, while spending nothing on the individual.

Guardian and Associates is further accused of paying out sums to Rashad for individuals who weren't even living in his facilities, the indictment claims.

According to the indictment, probate courts regularly appoint guardians and conservators to manage the personal and financial affairs of adults, known as wards, who have been found by the court to lack the capacity to do so themselves. Guardians and conservators are fiduciaries who are obligated to act in the best interests of their wards. The indictment alleges that Nancy Williams owned Guardian and Associates, an agency that was appointed as a fiduciary by the Wayne County Probate Court for incapacitated wards in over 1,000 cases.

...

Avery Bradley is an attorney, who, along with his daughter (and fellow attorney) Andrea Bradley-Baskin, operated a law firm that often represented Guardian and Associates in Wayne County Probate Court and otherwise practiced regularly in that court. Bradley-Baskin is currently a district judge on Michigan’s 36th District Court. Dwight Rashad operated a series of group homes and residential facilities for elderly individuals, including wards, who needed support and care. -DOJ

They also claim Williams paid Rashad rent for wards who never lived in his facilities. Lawyers for Bradley-Baskin have not responded to requests for comment. The case is being investigated by the FBI and IRS Criminal Investigation.

"We respect the authority that covers a black robe. This state judge and her cronies allegedly abused that high honor for personal gain by preying on the needy protected by the court," said U.S. Attorney Jerome Gorgon in a statement. "This would be a grievous abuse of our public trust."

FBI Detroit Field Office chief Jennifer Runyan said, “Regardless of a person’s position in society, no one is above the law,” and accused the defendants of exploiting their authority to profit from vulnerable people.

Tyler Durden Mon, 02/02/2026 - 15:45Authored by Matthew Piepenberg via VonGreyerz.gold,

On Friday, January 30, 2026, the world learned (or rediscovered) just how grotesquely rigged the paper gold and silver markets truly are.

Despite no change whatsoever in global supply and demand forces, silver went from a $120 near-high on Thursday to a $78 low on Friday, marking this as the largest single-day crash (35%) in the silver market in 44 years.

It goes without saying that such price moves don’t happen naturally.

Something far more engineered was in play, a trick which many investors may not immediately recognize, but which anyone familiar with the nefarious insider mechanics of banking, the Chicago Mercantile Exchange, the COMEX and the London Bullion Market Association can see as plainly as a dentist sees a cavity.

So, what happened?

Look No Further than a Banker’s RescueAs usual, whenever something so openly rigged, insider and market-distorting occurs, the very first place to look for a smoking gun, guilty child and a liar’s grin is among the banks, most of whom are and were drowning in levered silver short positions by Thursday night’s $120 silver price.

This meant that with each passing day of rising silver, the banks were getting squeezed to the point of self-destruction.

This is not fable but fact. Rising silver was literally strangling the big banks. They needed to exit their short squeeze as soon as possible, but preferably at a lower rather than higher silver price.

And then, almost by magic, silver conveniently fell like a rock to save their collectively levered @$$es.

Coincidences Galore…But was it really any “magical” coincidence that JP Morgan was able to exit its massive (and fatally stupid) short exposure at the absolute bottom/floor of the silver price on Friday? That is, at the perfect moment?

Was it also any coincidence that the London Metals Exchange went completely dark on that very same day?

And was it just an equal coincidence that HSBC, the second largest silver short holder on the LBMA, went completely offline as the choreographed Friday massacre in silver took place?

Or do you think it may also be just another coincidence that the self-regulated COMEX raised its margin requirements yet again on that same Friday to shake out even more of the levered longs, which were otherwise pummeling the short-exposed bankers?

And finally, do you think it was just a coincidence that the announcement of a new Fed Sheriff came that very same day, on the eve of a weekend, and well after the Asian markets had closed?

Engineered CarnageFolks, let’s be very clear. What happened on “Silver Friday” was neither normal market action nor a convergence of statistically impossible coincidences.

It was an entirely engineered flushing of the silver price to save a fatally trapped cabal of bankers caught behind the grassy knoll in the mother of all short-squeezes.

But as I had warned as recently as a month ago, such desperate measures are nothing new, especially in the more volatile silver trade. Or stated otherwise: “We’ve seen this movie before.”

Same Tricks, Different DatesIn 1980, for example, when the Hunt brothers famously sought to corner the silver market, they had caught the attention and fear of the market manipulators in the US and UK, who, for obvious reasons, feared a rising silver price.

The self-regulated US exchanges have the luxury of changing the rules in the middle of a chess match, which means they effectively always win (i.e., cheat).

As the Hunt brothers helped take silver toward an alarming $50.00 in 1980, the CME simply changed the rules mid-game by making the exchange a sell-only platform, which naturally crushed not only natural price discovery, but also took 80% off the silver price with a single rule change.

How’s that for a rigged game?

But the highlights don’t end there.

In the post 2008 crisis era, silver began to make positive strides north yet again. By 2011, silver hit the spooky $49.00 level, and so the equally spooked CME proceeded to raise the margin costs for silver trades five times in two weeks.

By effectively raising the “buy-in” to play poker with the silver exchanges, the new rules (i.e., the “House”) forced most of the silver longs to sell at mass, which directly precipitated a 48% fall in an otherwise naturally bullish silver market.

Of course, we just saw similar games played in December of 2025, when the COMEX imposed margin hikes yet again in the silver markets. As I warned just weeks ago, this was a sign of desperation but not capitulation.

The rigged game against silver would not end so easily.

Silver Friday…Which brings us to Silver Friday, one of the greatest price spoofs ever witnessed in the totally rigged, and now totally desperate paper metals markets.

As silver hit $120, the levered bankers and the incestuous system they rigged went into open panic and cheat mode against that otherwise revered notion of dying capitalism, which the rest of us call “free price discovery.”

By adding more margin hikes on Friday, the insiders forced a sell-off in the paper silver markets and covered their embarrassing shorts at a 35% discount off natural price action.

This was the market equivalent of Lance Armstrong conducting his own drug tests…

What’s Next?If some of you are glad to understand the twisted plumbing behind the manipulation of silver (and gold) in the COMEX cesspool, a theme we’ve covered numerous times elsewhere, you may nevertheless be concerned.

That is, you may be glad to see how the game is rigged, but your next question, naturally, is how does that help you as a silver or gold investor if the House always wins?

After all, it may be nice to call out a dirty cop, but that doesn’t mean it’s easy to beat one.

Or stated even more simply, if the game is so openly rigged, how does one ever win? What can you do with your gold and silver in such a corrupt backdrop?

Fair QuestionIn fact, the disconcerting tricks behind Silver Friday are by no means the end of the longer story for silver in particular or precious metals in general, as the exchanges are clearly terrified of silver and gold’s inevitable direction northwards.

They see what we see.

If anything, the desperation behind this headline move only signals a stronger silver and gold market ahead.

Why?

Supply & Demand Gets the Last LaughBecause the crash of Silver Friday did not solve the much larger problem (or more powerful forces) of basic supply and demand.

Silver has seen five consecutive years of 200M ounces/year of supply deficits, totaling over 1B ounces in collective silver supply deficits.

All Silver Friday achieved was a flushing out of uber-levered speculators and a classic butt-saving of those ever-so-stupid commercial banks who found themselves trapped (and now rescued) from the mother of all short-squeezes.

A rigged system which favors insider bankers is nothing new. We’ve written about their staggering games for years.

But here’s the rub.

Rock Now Beats PaperWhat we just witnessed on Silver Friday is pure confirmation that the silver (and gold) paper markets are dying before our watering yet wide-open eyes.

In October, for example, the London exchange effectively seized up. They were out of physical silver. In the summer of 2025, the COMEX saw 100% delivery of gold, leaving an exchange whose typical delivery percentage was 1%.

In short: The world wants physical metals, not paper tricks.

The CME and COMEX cheaters may be able to brazenly manipulate the paper price of silver, but they have yet to find an alchemist’s ability to create actual silver.

Moving forward, actual buyers of real silver will move further and further away from the now discredited and increasingly desperate and openly rigged paper markets in the US and UK.

The physical metals will be in greater demand, and the once-powerful paper exchanges will lose their leverage and influence.

Industrial as well as monetary demand for silver will continue to push demand and physical pricing higher.

As for gold, the rising demand for real money (physical gold) over paper currencies will continue its secular and historical momentum north for all the reasons we’ve already covered.

This rising preeminence of physical gold and silver over levered paper gold and silver will steadily outpace the increasingly desperate and disclosed mechanizations on the paper exchanges.

Or stated more simply: The CME may have won a paper battle on Silver Friday, but rising demand for physical silver and gold will win the war on paper systems losing credibility, power and options with each tick of a global debt bubble and currency timebomb.

For those who hold physical gold and silver as part of a long game of wealth preservation against the short game of desperate yet dying paper money, Friday’s speedbump was nothing more than that: A bump in an otherwise wide-open road forward.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of ZeroHedge.

Tyler Durden Mon, 02/02/2026 - 15:05We have repeatedly warned about the "Great Memory Crunch," driven by AI data center buildouts absorbing a growing share of global memory supply, and industry insiders now telling consumers and enterprises (read here) should accelerate purchases of electronics that use high-bandwidth memory before prices accelerate further, as supply shortages are expected through 2027.

One key signal that the memory shortage is worsening is that Apple, one of the world's most valuable companies, is having to prioritize the production and shipment of its three most premium new iPhone models due to the memory crunch, according to a new report by Nikkei Asia.

Not even Apple can mitigate the threat of the HBM shortage.

Here's more from the report based on industry insiders:

The U.S. tech giant will focus on delivering its first-ever foldable iPhone as well as two non-folding models with higher-end cameras and larger displays for its flagship launch in the second half of the year, said four people with knowledge of the matter. The standard iPhone 18 model will be scheduled for shipment in the first half of 2027, they said.

The move is intended to optimize resources and maximize revenue and profits from premium models amid surging prices for memory chips and other materials, multiple sources told Nikkei Asia. It is also critical for Apple to minimize any potential production hiccups while mass producing its first-ever foldable iPhone, which requires more complicated industrial techniques and new materials that could require more time to reach required levels of production quality, according to the people.

Choosing to focus on premium models in the second half of this year and targeting sales for its relatively standard models in the first half of 2027 could help the company better manage supply chain resources and develop a better and clear marketing strategy, one of the people said.

. . .

Apple has at least five new iPhone models in the pipeline: a revamped iPhone Air, its thinnest-ever model; the standard new iPhone; and three premium models. It is not yet clear when shipments of the Air will start, but they are not expected this year.

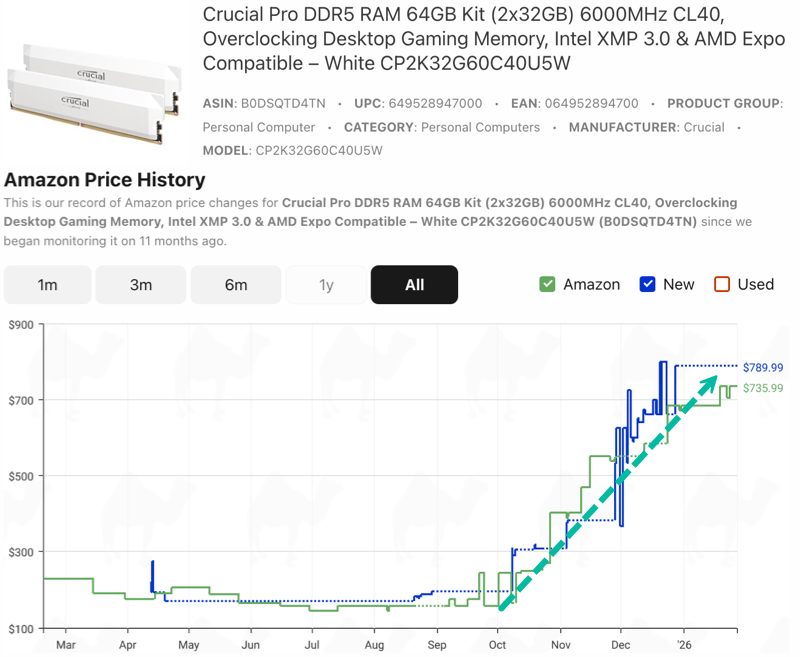

To visualize the HBM memory crunch, Amazon price-tracking website CamelCamelCamel shows a parabolic surge in the price of Crucial Pro DDR5 64GB RAM, rising from $145 to $790 in just six months.

More than one month ago, we cited Goldman analyst Maho Kamiya, who told clients that concerns about rising memory prices and the absence of top-down tailwinds had sent Nintendo shares spiraling.

TrendForce expects 70% of HBM chips produced this year will be consumed by data centers.

The list of memory-crunch victims has continued to grow.

Last week, we noted that smartphones, PCs, and other consumer electronics dependent on HBM were set to come under pressure. Goldman then followed with another note, warning that it had slashed global PC shipment forecasts due to soaring memory prices. That list continues to expand:

In addition to the Nikkei Asia report, Apple CEO Tim Cook told investors during an earnings call this past week that "We do continue to see market pricing for memory increasing significantly. As always, we’ll look at a range of options to deal with that."

If even one of the world’s largest and most powerful companies is struggling to secure enough memory supply, the warning signs are flashing red: the Great Memory Crunch is rapidly accelerating and could impact product availability, while sending prices for popular electronics soaring.

Tyler Durden Mon, 02/02/2026 - 14:50Authored by Zachary Stieber via The Epoch Times,

Superintendents are keeping schools closed to students across multiple states on Feb. 2 as cold weather persists, leaving some roads and sidewalks difficult to navigate.

Officials in Montgomery County, Maryland; Fairfax County, Virginia; and Winston-Salem/Forsyth County, North Carolina were among those announcing canceled classes on Monday for the eighth day in the wake of a storm that dumped snow and ice along the East Coast.

“Snow and ice removal from this winter weather event has been slow, where Monday will be the first day above freezing in 9 days,” Montgomery County Public Schools said on the district’s website.

“We know we will not have perfect conditions any time soon, but many streets and sidewalks are NOT passable for buses or safe for student walkers,” officials added later.

They said they want to resume classes on Tuesday, but doing so would be partially contingent on people clearing sidewalks around them.

Fairfax County Public Schools said on its website that classes were canceled because of “continued concerns about safe travel for students and staff to and from school.” The district did not commit to opening on Tuesday.

At least some employees in both counties are expected to report to work on Feb. 2, officials said.

Winston-Salem/Forsyth County Schools said on its website that schools were closed Monday “due to unsafe road conditions.”

Those three districts were among those not holding remote classes or instruction over the Internet.

Other districts, such as Randolph County Schools in North Carolina, were having a remote learning day rather than holding classes as normal in person.

Still others, including schools in Baltimore County in Maryland and the District of Columbia, opened for in-person instruction, but two hours later than usual.

A number of states are dealing with snow and ice brought by a January storm. Some areas reported multiple feet of snow. Many recorded at least eight inches.

Since then, freezing temperatures have persisted, keeping the snow and ice in place unless it is removed by hand or machine.

The National Weather Service issued a winter weather advisory for portions of Michigan and North Carolina on Monday due to freezing temperatures and additional accumulations of ice.

Forecasters also warned residents across Florida that temperatures as low as 30 degrees, with cold wind chills, were expected late Monday into early Tuesday.

The cold temperatures atypically affected the Southeast, including Alabama and Florida.

More snow is projected to fall in Delaware, Maryland, and New Jersey, among other states, in the coming days, although the total would likely be no more than 1 inch in most areas and a maximum of 5 inches, the weather service said.

Tyler Durden Mon, 02/02/2026 - 14:20With roughly 50% of the S&P 500's market capitalization having reported results so far this earnings season, we are focusing on what companies are saying about artificial intelligence on earnings calls.

To do that, we lean on Goldman analysts led by Ben Snider, who track executive commentary focused on AI adoption.

"AI adoption has remained a popular topic on earnings calls this quarter, but only a handful of companies have quantified their productivity gains from AI use," Snider said.

Those companies include:

Bank of America (BAC):

"We have 18,000 people on the company's payroll who code - using the AI techniques, we've taken 30% out of the coding technique - the coding part of the stream of introducing a new product or service or change, that saves us about 2,000 people... And I use an example, our audit team has built a capability they think a series of prompts around doing audits and stuff to allow them to shape the head count back down that they had to grow during the regulatory onslaught over the last few years."

C.H. Robinson Worldwide (CHRW):

"Our fleet of AI agents is growing quickly as we continue to pioneer new ways to automate manual tasks and supercharge our industry-leading freight experts to solve for complexity and deliver high-quality service to our customers and carriers… This includes an expectation that we will generate double-digit productivity improvements in both NAST and Global Forwarding in 2026, as we continue to implement agentic AI across our quote-to-cash lifecycle of an order... These digital capabilities also enabled us to continue delivering double-digit productivity increases in NAST in 2025. Since the end of 2022, we have delivered a more than 40% increase in shipments per person per day, and this is measured across the entirety of our NAST organization... Additionally, 95% of our checks on missed LTL pickups are now automated, saving over 350 hours of outsourced manual work a day… Take the example we give often around our request for freight quote operation... Previously, we were only getting to 60% of those requests; today, we get to 100%. Previously, it was taking a cycle time of 17 to 20 minutes; today, it takes less than 32 seconds... These new AI agents are tracking down missed pickups and using advanced reasoning to determine how to keep freight moving... As a result, shippers' freight moves up to a day faster and return trips to pick up missed freight have been reduced by 42%... the growing automation across our quote-to-cash lifecycle enables us to decouple head count growth from volume growth and to create greater operating leverage and operating margin expansion... Our average head count was down 12.9% year-over-year in Q4 and was down 3.8% sequentially..."

Costco Wholesale (COST):

"An early use case has involved integrating AI into our pharmacy inventory system... autonomously and predictably reorders inventory, improving our end stocks to more than 98%. This change has played an important role in helping us achieve mid-teens growth in pharmacy scripts filled and has improved margins while lowering prices to our members. We are now in the process of deploying AI tools in our gas business, which we expect will improve inventory management and drive incremental sales by ensuring we're always delivering the best value to our members."

Meta Platforms (META):

"Since the beginning of 2025, we've seen a 30% increase in output per engineer with the majority of that growth coming from the adoption of agentic coding, which saw a big jump in Q4. We're seeing even stronger gains with power users of AI coding tools, whose output has increased 80% year-over-year. We expect this growth to accelerate through the next half."

Northern Trust (NTRS):

"You heard me mention our productivity for 2025 was about 4% of our expense base. And this year, we bumped that up. It's going to be closer to 5%. And a lot of that is because of the impact we're seeing of AI... we are simplifying processes, upgrading platforms, and applying AI to reduce friction in service delivery."

Paychex (PAYX):

"We are excited to share that our first agentic AI pilots were a success this quarter. They autonomously handled thousands of payroll calls and emails with nearly 100% accuracy, decreasing payroll processing time and enabling our service teams to focus on higher value strategic advisory support."

ServiceNow (NOW):

"AI is also driving significant cost efficiencies that have resulted in full-year profitability beats on top of our recently raised guidance... We expect an operating margin of 32%, up 100 basis points year-over-year driven by OpEx savings enabled by AI efficiencies."

Travelers Companies (TRV):

"We've recently rolled out Gen AI agents to efficiently mine both internal and external data sources to better understand and synthesize the risk characteristics and ensure appropriate business classification. This capability both accelerates the underwriting process and results in improved risk classification and segmented pricing... In extensive testing, we achieve significantly improved engineering output and meaningful productivity gains... the efficiency gains in our claim organization come through loss adjustment expense, benefiting the loss ratio. As just one example, our claim call center population is down by a third. And this year, we'll be consolidating four claim call centers down to two... Our AI investments to automate submission intake for new business reduced our time to ingest submissions from hours to just minutes… our renewal underwriting platform leverages generative AI… with early results showing more than a 30% reduction in average handle time."

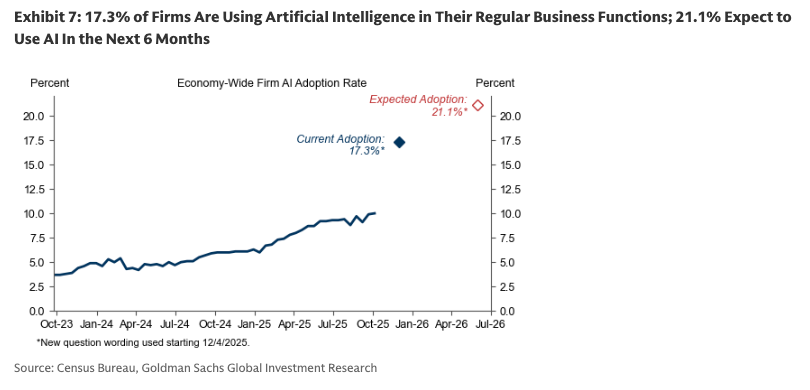

In a separate note, Goldman analyst Sarah Dong reported that the AI adoption tracker through December stood at 17.3%, with an expected target of 21.1% over the next six months.

Related:

What To Know About Corporate America's Double-Digit AI Adoption Boom

October Layoffs Surge Most Since 2003 Amid Cost-Cutting, AI Adoption, Challenger Data Shows

We expect 2026 to be a year when AI-related layoffs accelerate as AI adoption gains traction across corporate America.

Tyler Durden Mon, 02/02/2026 - 14:05By Tsvetana Paraskova of OilPrice.com

Devon Energy and Coterra Energy announced on Monday a definitive agreement to merge and create a premier shale operator in an all-stock transaction, implying a combined enterprise value of about $58 billion.

The deal, announced today after weeks of speculation, would create a company with a significantly increased position in the premier part of the Permian Basin and operations in the Marcellus Shale and Anadarko Basin.

The deal will create one of the top shale producers with pro-forma third quarter 2025 production exceeding 1.6 million barrels of oil equivalent (Boe) per day, including over 550,000 barrels of oil per day and 4.3 billion cubic feet of gas per day, the companies said.

The combined company will be named Devon Energy and will be headquartered in Houston while maintaining a significant presence in Oklahoma City.

Devon and Coterra expect to realize $1 billion in annual pre-tax synergies with the deal.

Lower oil prices have shale producers considering how they can boost investor returns when expanding drilling at $60 a barrel oil or lower is eating the margins.

In terms of drilling opportunities, the combined company will have the largest inventory in the Delaware basin with a breakeven of below $40 per barrel, according to Devon’s presentation of the merger deal.

The combined company will also have top-tier capital efficiency in each basin, with operations in the Permian, Anadarko, Eagle Ford, Marcellus, and the Rockies regions.

Under the terms of the agreement, Coterra shareholders will receive a fixed exchange ratio of 0.70 share of Devon common stock for each share of Coterra common stock. Upon completion of the deal, Devon shareholders will own about 54% of the go-forward company and Coterra shareholders will own approximately 46%.

The transaction, which was unanimously approved by the boards of directors of both companies, is expected to close in the second quarter of 2026, subject to regulatory approvals and customary closing conditions, including approvals by Devon and Coterra shareholders.

Tyler Durden Mon, 02/02/2026 - 13:45By Benjamin Picton, Senior Market Strategist at Rabobank

The DXY is dealing firmer this morning and precious metals continue to be flogged like the family silver after Donald Trump confirmed the nomination of Kevin Warsh as incoming Fed Chair. In defiance of the President’s oft-stated preference, markets are convinced that Warsh is a hawk. Consequently, zero-yield risk is taking a beating (bitcoin, ouch), equities are offered and US 5y5y inflation swaps have fallen by ~2bps since Wednesday of last week.

The Financial Times marked the occasion of Warsh’s nomination by saying ‘Arise, Shadow Fed Chair Stan Druckenmiller’, suggesting that the legendary hedge fund manager who counts both Kevin Warsh and Treasury Secretary Scott Bessent among his proteges is now the most powerful person in the global economy. The FT references ‘people familiar with the matter’ as describing Druck’s relationship with Warsh and Bessent as “akin to father-son relationships”, with Warsh in particular sometimes speaking with Druckenmiller “more than a dozen times a day”. Needless to say, markets will now be hanging off of Druck’s every utterance for direction on monetary policy.

While that will doubtless be the case, it seems absurd that much divination is actually required to determine where monetary policy in the United States is likely to go. The national debt burden is immense – soon to hit $39 trillion in dollar terms and now above 121% of GDP – and more than 3% of GDP is already dedicated to servicing interest expense. That – as Fed Chair Powell pointed out last week – comes at a time of healthy economic expansion with a labor market close to full employment.

With all the understatement of a career central banker, Powell described this cocktail as “unsustainable”. If something is ‘unsustainable’, logically it will not be sustained. So what is likely to change?

It won’t be the spending, as the largely futile efforts of DOGE and the fact that ‘mandatory spending’ (social programs, farm subsidies, student loan subsidies etc) plus interest expense plus defence spending accounts for almost 87% of US fiscal outlays. Interest expense will go up, not down, Trump wants to increase the defence budget by 50% and cutting entitlements is a practical impossibility that often gets talked about but never seems to happen. Besides, Trump campaigned on opposing cuts to programs like social security and Medicare.

What about the income side of the ledger? The Trump administration has already taken steps to increase taxes by introducing sweeping import tariffs, but if those tariffs prove effective over time in driving import substitution for domestically-produced alternatives it stands to reason that tariffs will become less and less effective as a revenue tool. Outright rises in direct taxation also seems unlikely given that Trump permanently extended his 2017 tax cuts that had been due to expire via the One Big Beautiful Bill in May of this year.

That leaves interest rates and growth as the only remaining levers to right the fiscal ship. Politicians always think that they are going to grow their way out of trouble, but in Trump’s case it seems likely that an inflationary boom is genuinely part of the fiscal strategy. All of the signs so far point to a willingness to ‘run it hot’ when it comes to the economy.

We have written previously about the strategy of driving adoption of US dollar stablecoins as a means to lower borrowing costs at the front end of the yield curve. Coupled with a sympathetic Fed Governor who is likely to reflect the President’s wish for a lower Fed Funds rate, this might be the best shot of the administration to move the fiscal needle. Indeed, in an era of fiscal dominance, the incoming Fed Chair may have little choice but to keep short rates low.

Along with moves to pressure mortgage relates lower through MBS purchases, threats of price caps (on credit card interest, for instance) and attempts to use tariffs as leverage to extract investment pledges from other countries, these sorts of measures veer into the realm of financial repression, where real interest rates are held negative and private savers carry the can for the government largesse.

Of course, some of these policy options are only available to the United States due to its status as the issuer of the global reserve currency. Abusing the “exorbitant privilege” of being the reserve currency issuer through erratic trade practices, financial repression and strategic currency devaluation is a high stakes gamble that could backfire spectacularly.

Xi Jinping is evidently well aware of the contradictions faced by the United States in attempting to leverage its position as reserve currency issuer without losing it. The FT yesterday reported on comments from Xi calling for the Chinese renminbi to become a global reserve currency by creating a “powerful (read: politicized) central bank” that would ensure a “strong currency” used widely in international trade, investment and foreign exchange markets.

The renminbi has been steadily strengthening against the dollar since Liberation Day last year, and the PBOC has accelerated its run stronger daily fixings from late November onwards. Xi was clear at the Shanghai Cooperation Organization summit last year that he wished to internationalize the role of the CNY and China has begun using its monopsony market power in commodities like iron ore to drive wider acceptance of its currency for trade settlement. Expect more of this in markets where China is the only buyer, or the only buyer of scale.

CNY is starting from a low base and still faces the Triffin Dilemma of not meeting the requirements of a reserve currency so long as China insists on running trade surpluses (there’s no sign of a change of heart on that score), but by boosting its adoption Xi could chip away at the reserve currency status of the dollar right at the moment when many other players in financial markets and the world economy are openly questioning whether the dollar’s writ still runs.

Though it still seems unlikely at this stage, if the reserve status of the dollar was genuinely threatened it would dramatically reduce the freedom to manoeuvre of US policy makers grappling with that “unsustainable” fiscal trajectory.

For the public finances of the United States, that might be the Warsh that could happen.

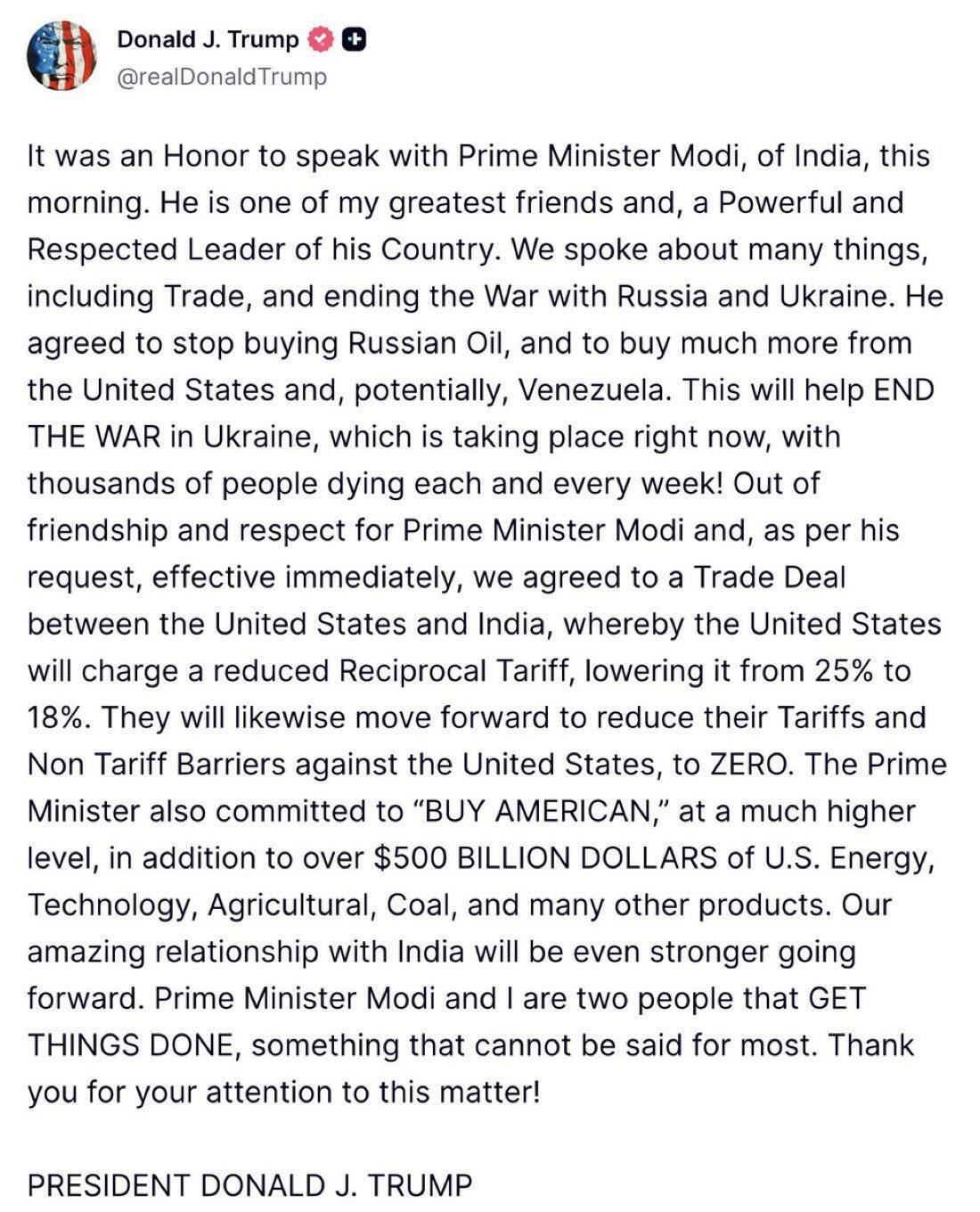

Tyler Durden Mon, 02/02/2026 - 13:05In a huge Monday development, President Trump has announced the US will trim its punitive 25% tariff on Indian imports to 18% after striking what he hailed as a new "trade deal” with Indian Prime Minister Narendra Modi. Crucially it hinges on New Delhi having reportedly ended its purchases of Russian crude and swapping them for massive US energy and goods buys.

In a Truth Social post, Trump portrayed the agreement as a major geopolitical win, saying that India "agreed to stop buying Russian oil, and to buy much more from the United States and, potentially, Venezuela," and crucially framing the move as helping "END THE WAR in Ukraine."

via AP

via AP

Under the newly touted deal, according to breaking details.:

The United States will cut its "reciprocal tariff" on Indian goods from 25% to 18%, effective immediately.

India will slash its tariffs and non-tariff barriers on American products to zero.

Modi has pledged a gargantuan "BUY AMERICAN" commitment, including upwards of $500 billion in U.S. energy, technology, farm, coal, and other exports.

Trump cast the concessions as evidence of deep bilateral "friendship and respect," insisting the deal marks a new chapter in US–India trade and energy ties. This will of course also be a blow to Moscow's oil lifeline.

Bloomberg notes:

The White House did not immediately respond to a request for comment on if Trump was lowering the reciprocal tariff and eliminating the extra penalty over Russian oil purchases, or simply reducing one of the rates. India’s benchmark stock index Nifty 50’s futures traded at the Gujarat International Fin-Tec City surged as much as 3.8% in thin trading, while the US-listed iShares MSCI India ETF hit session highs and rose as much as 2.4%. The rupee rallied in ofshore trading, gaining 1% against the dollar.

The shift represents a dramatic retreat from the brash tariff escalation of 2025, when Washington first slapped India with steep levies, including a 25% penalty linked explicitly to Russian energy imports, in a bid to choke Delhi's crude trade with Moscow. The pressure appears to be working, to say the least.

"Out of friendship and respect for Prime Minister Modi and, as per his request, effective immediately, we agreed to a Trade Deal between the United States and India, whereby the United States will charge a reduced Reciprocal Tariff, lowering it from 25% to 18%," Trump posted. "Our amazing relationship with India will be even stronger going forward."

Tyler Durden Mon, 02/02/2026 - 12:50Authored by Lance Roberts via RealInvestmentAdvice.com,

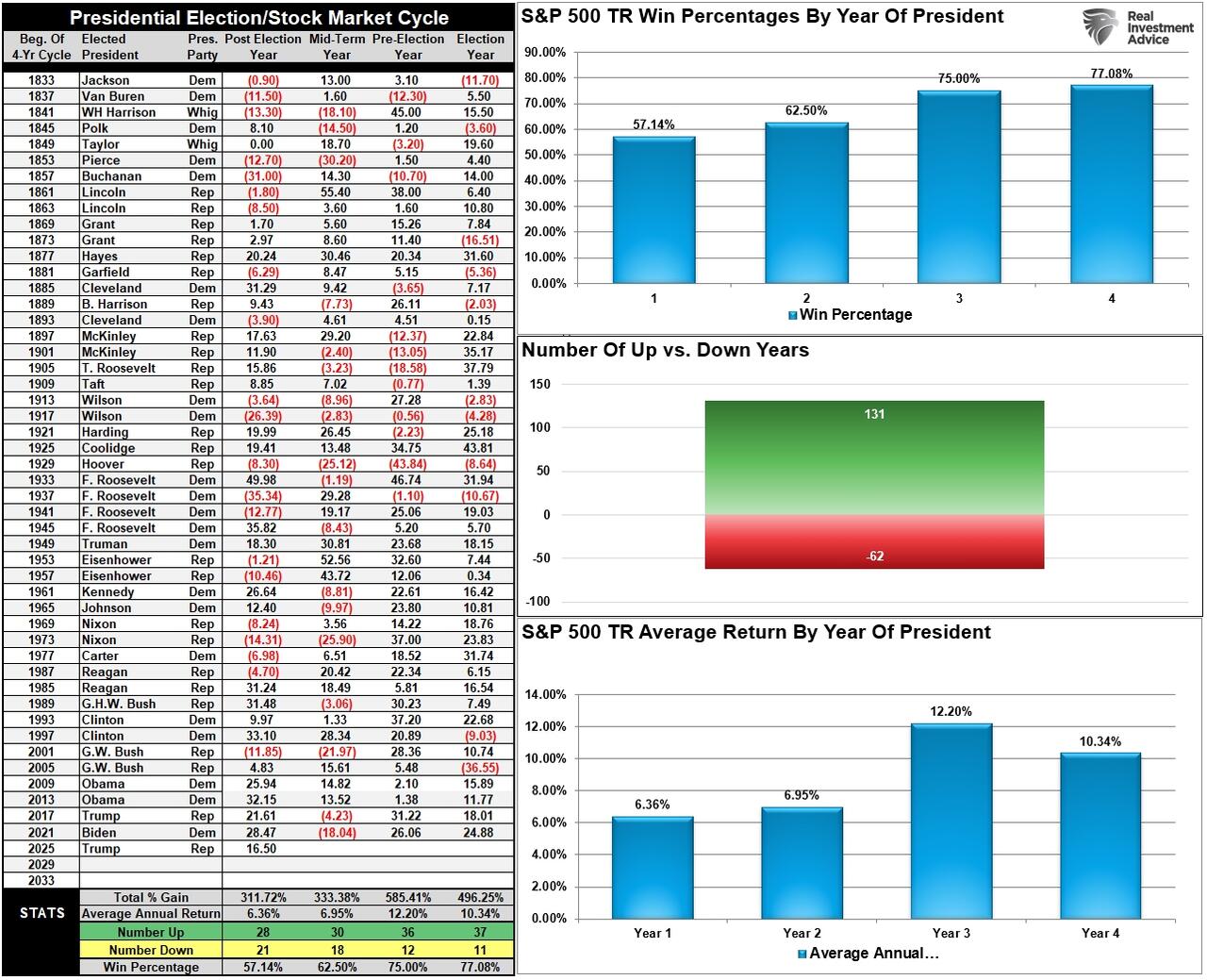

Market cycles are once again at the center of the investment narrative as we head into 2026. The optimism is familiar as earnings held up in 2025, the economy avoided recession, and big tech lifted the indexes. However, those victories are already reflected in the price. As we head into 2026, with valuations extended, the margin for error has narrowed. However, while analysts are very optimistic for this year, the case for another strong year leans heavily on historical patterns.

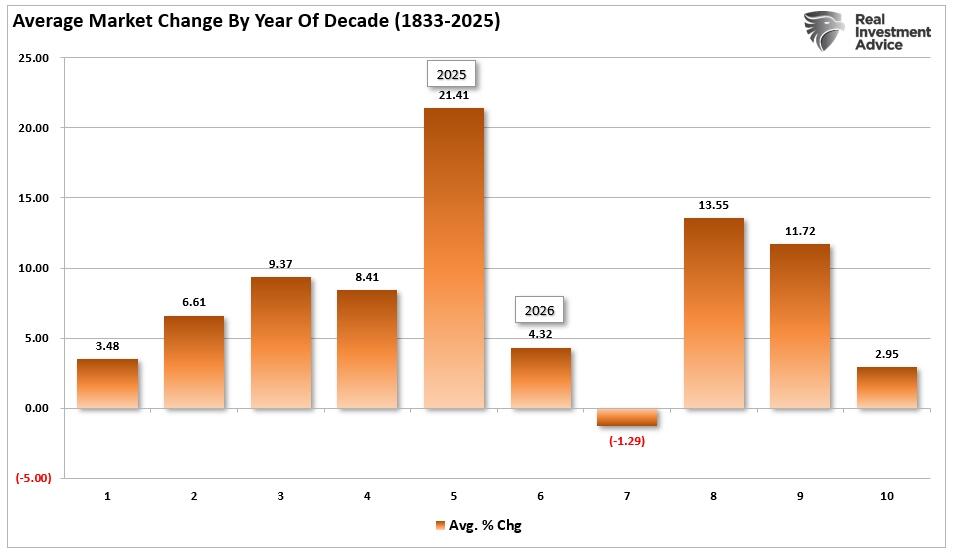

Let’s start with the Presidential Cycle. Market cycles tied to the presidential calendar suggest the second year of a new administration is often slower. Since 1948, years three and four of a presidential term have yielded the most substantial returns, while year two, or the post-election year, has shown weaker performance, with modest gains and lower win rates. The data is shown below, and while 2025 traded above historical norms, 2026 may not be as fortunate.

Since 1871, markets have gained in 30 of those years, with losses in only 18, resulting in a win rate of approximately 62%. While better than a “coin toss,” it falls well short of the win rate in years three and four. Another potential headwind to the markets in 2026 is the midterm elections, which could potentially result in a change of control in the House or Senate, leading to increased gridlock in Washington.

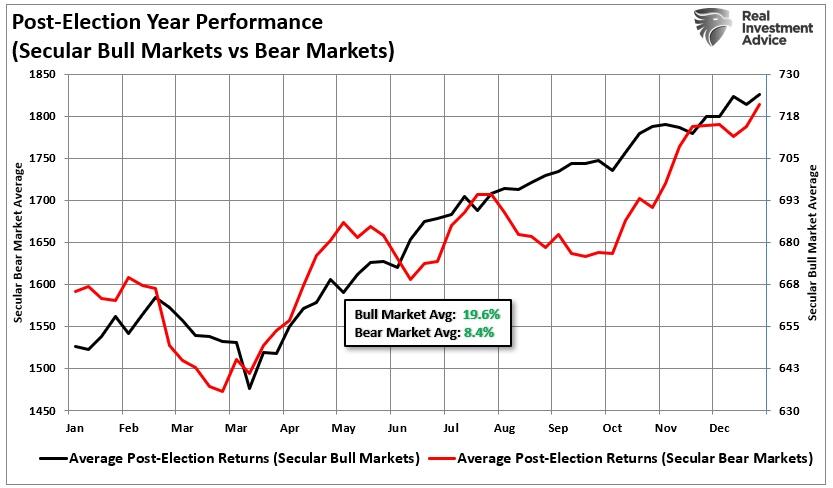

It is worth noting that since 1948, there have been seven instances of loss during the second year of the presidential cycle. Two of those losses occurred sequentially during the last two administrations, in 2018 and 2022. However, stocks have, on average, performed better during bull market cycles versus bear market cycles. The chart below illustrates the average market return during both bullish and bearish market cycles during the second year of a Presidential term.

With a “win ratio” of 62%, the media has been quick to assume the bull market will continue unabated. However, there is a 38% chance that a bear market will occur, which is not to be taken lightly. Furthermore, given the current duration, magnitude, and valuation issues associated with the market, a “Vegas handicapper” might increase those odds slightly.

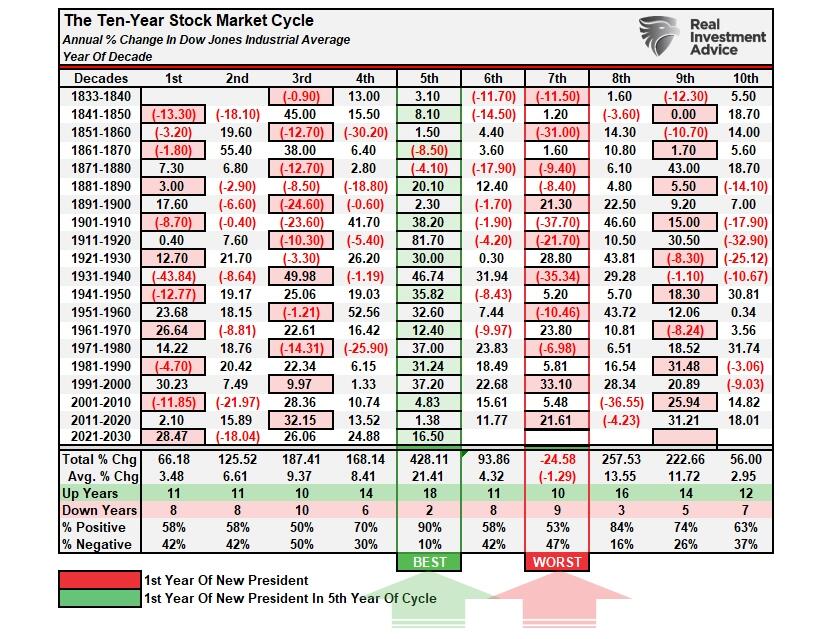

Year 6 Of The Decennial CycleThen there’s the decennial trend. Market cycles built around decade shifts show the sixth year of each decade tends to underperform. In fact, only the 7th and 10th years have weaker returns. While 2025, the 5th year of the cycle, performed in line with historical averages, years 6 and 7 (2026 and 2027) suggest some caution. Average returns are 4% and -1.2% respectively, with the win/loss ratio barely better than a “coin toss.”

We can further assess the potential risk by examining the average market change by year of the decennial cycle. As noted while 2025 performed near historical norms, the risk of a lower return year in 2026 seems to be elevated.

While the Presidential and Decennial cycles are not guarantees of lower to negative returns in 2026, the analysis suggests that investors should at least exercise caution when it comes to risk management. With valuations elevated, risk-taking and speculation high, and sentiment very bullish, there seems to be a higher risk of disappointment than not.

A resurgence of interest rates that impact corporate profitability

Inflation rises, causing the Federal Reserve to halt rate cuts.

An economic slowdown, or mild recession, that results in a decline in forward earnings.

A financial or credit-related event that causes a repricing of market valuations.

You get the idea. The current setup reflects that with earnings growth rates slowing, the consumer is leveraged, and while inflation is lower, it remains sticky. The Federal Reserve is caught between weak growth and elevated prices. Betting on another strong year without acknowledging the weight of these market cycles is a dangerous assumption.

Cycles don’t dictate market direction. But they shape investor psychology, and when both primary market cycles suggest caution, it’s not the time to get aggressive.

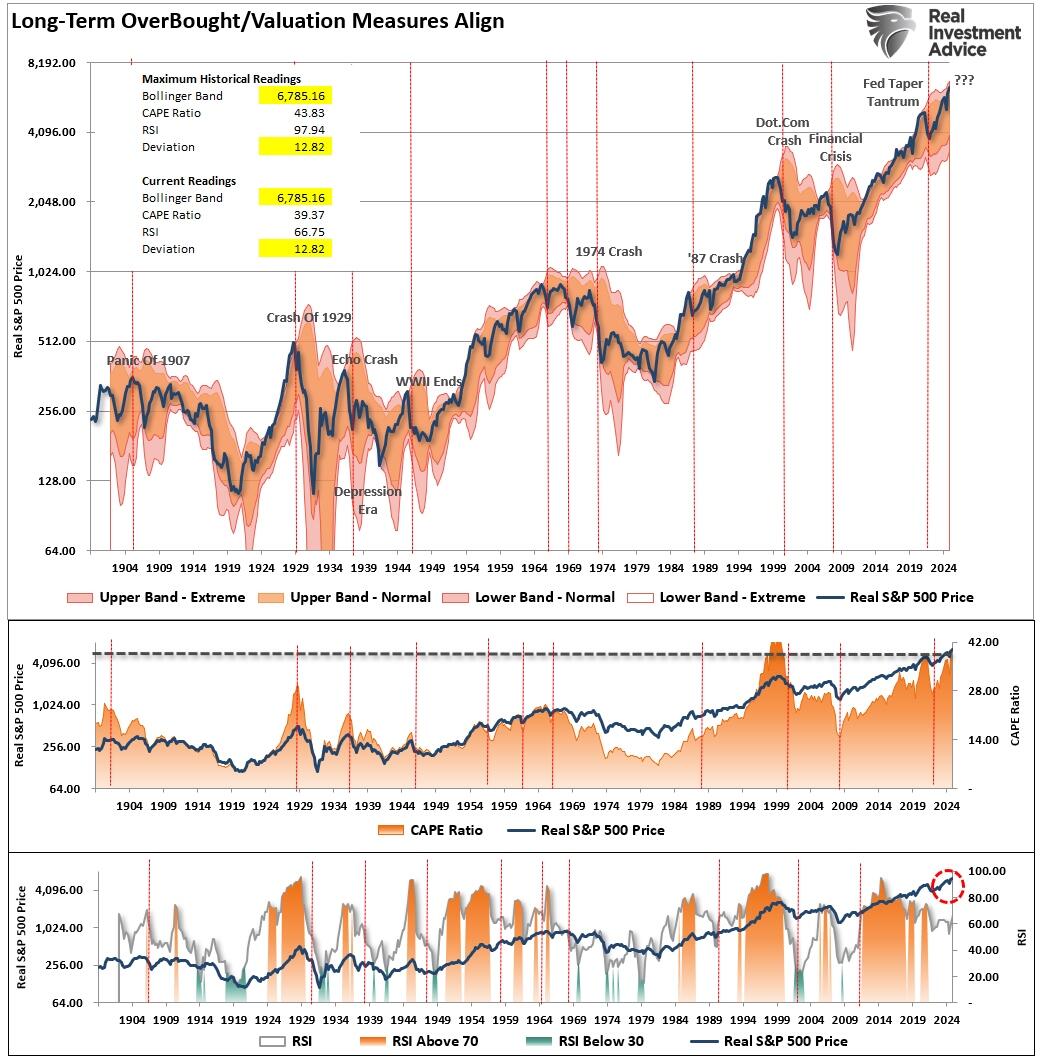

The “Technical” Risk of ReversionMarket cycles work because they reveal investor behavior. Bull phases are driven by optimism, liquidity, and earnings growth. Bear phases follow when expectations exceed reality. Right now, we’re on the edge of that shift. The Shiller CAPE ratio is trading well above its long-term average, and market prices are outpacing profits by a wide margin. That’s a signal, not noise. Market cycles have always corrected this type of divergence. In 1999, the last time we saw a similar disconnect, the result was a steep and painful correction.

What’s worse is that earnings growth in 2025 leaned on familiar crutches: cost cuts, financial engineering, and suppressed wages. Margins held up, but revenue growth did not. Now, consumer wages are declining, resulting in slower spending, and forward guidance is being revised lower. That’s not a setup that aligns with the optimism baked into current prices. For example, Bank of America’s 2026 outlook clearly sees this. Their analysts project weaker consumer demand and downside risk to earnings. However, BNP Paribas is more bullish, projecting the S&P 500 at 7,500, but even they admit that it depends on strong economic momentum and falling rates.

This is where market cycles come back into focus. Every long-term chart illustrates the same lesson: when valuations outpace fundamentals, reversion is inevitable. It’s not always immediate. It’s rarely obvious. But it’s consistent. And 2026 is shaping up as a test of whether this time is different—or not.

In September 2021, I produced the following chart stating:

“A market melting-up is exciting while it lasts. During melt-ups, investors rationalize why ‘this time is different.’ They start taking on excess leverage to try and capitalize on the rapid advance in prices, and fundamentals take a back seat to price momentum. Market melt-ups are all about ‘psychology.’ Historically, whatever has been the catalyst to spark the disregard of risk is readily witnessed in the corresponding surge in price and valuations. The chart below shows the long-term deviations in relative strength, deviations, and valuations. The previous ‘melt-up’ periods should be easy to spot when compared with the current advance.”

Of course, just three months later, the market began a nine-month correction that clipped roughly 25% off asset prices before bottoming in October 2022.

The chart has been updated through the end of 2025. It is worth noting that prices are again deviating from the long-term mean, valuations are extended, and relative strength is declining. Furthermore, investors are taking on increasing speculative risk and leverage, much like they did in 2021. Expectations for corporate earnings, the lifeblood of market performance, appear overly ambitious, and analysts are projecting another high double-digit increase in earnings for the year, a figure well above historical trends. However, these projections may not align with economic realities, particularly if consumer demand softens, the global economy slows further, or cost pressures persist.

The chart below uses quarterly data, so it is slow to move. It is worth noting that the current market is significantly deviated from its long-term mean, with the second-highest levels of valuation on record. While many claim that “this time is different,” long-term analysis suggests that it likely isn’t.

In 2025, actual earnings growth fell short of the original forecasts but remained decently strong overall. However, much of the market’s performance in 2025 was driven by valuation expansion rather than fundamental earnings growth. If this pattern continues, the risk of a correction increases. With all “experts” currently expecting above-average economic growth and earnings rates in 2026, investors should consider remaining more risk-conscious. As discussed in “Bob Farrell’s 10-Illustrated Rules:”

“Rule #9: When all experts and forecasts agree, something else will happen.”

Such certainly seems a risk to consider as we head into the new year.

Investors would be wise to treat this phase of the market cycle with discipline. The choice is yours.

How to Position for Market Cycles in 2026“Chase returns, and you’ll likely end up paying for it. Manage risk, and you’ll still be around when the next true bull leg begins.“

I am always reticent to discuss taking a more “risk-averse” approach to the markets. This is because investors typically interpret such commentary as “sell everything and go to cash.”

While 2026 presents its share of challenges, the solution is not to abandon the market altogether. Instead, investors can take practical steps to navigate these uncertainties.

None of this means the next “bear market” is lurking. The data suggest that being overly aggressive, taking excessive risk, and increasing leverage may not yield the desired outcome. Since exceedingly bullish markets are primarily a function of psychology, they can persist longer and extend further than logic predicts. The requirement to “end” such a phase is an exogenous event that changes psychology from bullish to bearish. Such is when the stampede for the exits occurs, and prices can decline very quickly. As such, investors need guidelines to participate in the market advance. However, the real challenge is maintaining those gains when corrections inevitably occur.

Positioning for 2026 means respecting our current market position. This is not a time to lean into high-beta names or speculative stories. This is a time to manage risk, preserve capital, and focus on quality. With both the presidential and decennial market cycles signaling below-average returns, prudence is more valuable than prediction.

Tighten up stop-loss levels to current support levels for each position. (Provides identifiable exit points when the market reverses.)

Hedge portfolios against significant market declines. (Non-correlated assets, short-market positions, index put options)

Take profits in positions that have been big winners. (Rebalancing overbought or extended positions to capture gains but continuing to participate in the advance).

Sell laggards and losers. (If something isn’t working in a market melt-up, it most likely won’t work during a broad decline. It is better to eliminate the risk early.)

Raise cash and rebalance portfolios to target weightings. (Rebalancing risk regularly keeps hidden risks somewhat mitigated.)

Notice, nothing in there says, “Sell everything and go to cash.”

Investing in 2026 will require a blend of optimism and caution. With slowing economic growth, fiscal policy uncertainties, global challenges, overconfident sentiment, and ambitious earnings expectations, investors have numerous reasons to approach the markets with caution. There will be a time to raise significant cash levels. A good portfolio management strategy will ensure that exposure decreases and cash levels rise when the selling begins.

The most important thing to remember is that market cycles are not about exact timing. They’re about understanding the rhythm of investor psychology, capital flows, and fundamental trends. In 2026, that rhythm suggests caution. Stay liquid. Stay hedged. And don’t forget—every market cycle eventually resets. Your job is to be still standing when it does.

Remember, as Larry David might say,

Tyler Durden Mon, 02/02/2026 - 12:40“You don’t have to be a genius—just don’t be a schmuck.”

Here we go again.

The government shutdown, which should be lifted in 24-48 hours once the House votes (we reported yesterday that Mike Johnson allegedly has the votes to pass the vote), is again jamming the machinery of government data reporting.

The BLS has pushed back the January 2026 jobs report, originally set for Feb 6, along with December’s Job Openings and Labor Turnover Survey and Metropolitan Area Employment data.

“The release will be rescheduled upon the resumption of government funding,” Emily Liddel, an associate commissioner at BLS, said in a statement. “Due to the partial federal government shutdown, the Bureau of Labor Statistics will suspend data collection, processing, and dissemination.”

The Bureau of Labor Statistics will announce new release dates once funding is restored.

Tyler Durden Mon, 02/02/2026 - 12:27We reported earlier that the last major nuclear arms control treaty between superpower rivals Russia and the United States is set to expire this week.

Former Russian president Dmitry Medvedev, now deputy chairman of the country's Security Council, has throughout the Ukraine war been the top official issuing the Kremlin's 'unofficial' nuclear warnings and threats. But now the outspoken Russian hawk is urgently offering an olive branch, arguing that the New Strategic Arms Reduction Treaty (New START) must be quickly extended.

Source: Roscongress Photobank

Source: Roscongress Photobank

The Kremlin has made clear Russia is willing to extend it for another year, to allow more robust negotiations and for a longer deal to be finalized. Unless it is renewed, the landmark treaty will expire on Thursday, February 5.

But with just days away, the Trump White House has yet to issue anything official. Of course, President Trump is also known for making key decisions at the last moment, building suspense and leverage, based on also on his notorious unpredictable decision-making style.

Medvedev on Monday made clear that Russia's offer to quickly extend "remains on the table, and the treaty has not even expired yet, and if the American side wants to extend it, then this can be done."

He also confirmed that Moscow has received no response on this offer from Washington:

Medvedev told the newspaper Kommersant that Moscow might have to wait until the expiry of the treaty on February 5 for a U.S. response to the Russian initiative.

When contacted for comment, a White House official told Newsweek Monday: "The president will decide the path forward on nuclear arms control, which he will clarify on his own timeline."

Medvedev explained Russia's point of view, as summarized in Newsweek:

Medvedev said the New START treaty had played a positive role in curbing the nuclear arms race, and that both Russia and the U.S. had stuck to its main restrictions.

However, the most important thing was for ties between the U.S. and Russia to be restored, with relations at their lowest since the Cuban missile crisis of 1962, Medvedev said. He said Trump's "Golden Dome" and statements about resuming nuclear testing complicated any potential strategic dialogue between Russia and the United States.

He further warned that letting the treaty expire would mark the first time since 1972 that there are no legal limitations on strategic weapons between the two rivals, which are both well-armed with atomic warheads.

Medvedev is predicting that more countries will join the nuclear club if New START's safeguards aren't in place by the world's two foremost nuclear powers.

Former President Obama chimes in...

If Congress doesn’t act, the last nuclear arms control treaty between the U.S. and Russia will expire. It would pointlessly wipe out decades of diplomacy, and could spark another arms race that makes the world less safe. This piece is worth the read. https://t.co/NPtKyjYRml

— Barack Obama (@BarackObama) February 2, 2026

According to Monica Duffy Toft, professor of international politics and director of the Center for Strategic Studies at The Fletcher School, "By providing transparency into the world’s two largest nuclear arsenals, New START has lowered the risk that either side will misinterpret normal military activity as preparation for a nuclear strike."

It was signed in 2010 by Presidents Barack Obama and Dmitry Medvedev, and limits the number of deployed strategic warheads to 1,550 per side, and caps deployed delivery systems - including of missiles, bombers, and submarines - at 700. There's also a mutual inspection regimen, allowing each side to monitor the other's sites.

Tyler Durden Mon, 02/02/2026 - 12:20Authored by Tom Ozimek via The Epoch Times,

Federal Aviation Administration (FAA) Administrator Bryan Bedford said on Feb. 1 that the agency accepts the findings of the National Transportation Safety Board (NTSB) that a series of systemic failures by the FAA led to a January 2025 midair collision, the deadliest U.S. aviation disaster in more than two decades.

Speaking to reporters on the sidelines of an aviation conference in Singapore, Bedford said the FAA did not dispute the NTSB’s conclusions on the collision between an American Airlines regional jet and a U.S. Army Black Hawk helicopter near Ronald Reagan Washington National Airport, which killed all 67 people aboard both aircraft.

“We don’t disagree with anything that the NTSB has concluded from their investigations,” Bedford said. “Many of the recommendations have already been put into action. Those that haven’t, we’re going to evaluate.”

The NTSB revealed the probable cause of the crash on Jan. 27, citing the FAA’s decision to allow a helicopter route to operate close to a runway approach path at Reagan National, along with multiple other “systemic failures” at the agency.

“This was 100 percent preventable,” NTSB Chair Jennifer Homendy said during the agency’s nine-hour probable-cause hearing, which capped a year-long investigation.

The NTSB said that the executive branch’s decision to permit helicopter traffic so close to commercial aircraft operations created unacceptable risk.

“Number one, this helicopter route shouldn’t have been there in the first place. This was terrible design of the airspace,” Homendy said toward the end of the Jan. 27 hearing.

Data and Procedural LapsesInvestigators also faulted the FAA for failing to adequately review its own data indicating elevated midair-collision risk around the Potomac airspace and for allowing controllers to rely heavily on “visual separation”—a practice in which pilots are responsible for seeing and avoiding other aircraft—to maintain traffic flow.

“The question is, should the FAA have known there was a problem, and should something have been done? Absolutely, the data was there. The data was in their own systems,” Homendy said, adding that the NTSB had worked with the FAA to flag more than 15,000 close-proximity events over several years, including 85 classified as serious.

Salvage crews work on recovering wreckage near the site in the Potomac River of a midair collision between an American Airlines jet and a Black Hawk helicopter at Ronald Reagan Washington National Airport, in Arlington, Va., on Feb. 6, 2025. Jose Luis Magana/AP Photo

The NTSB also cited staffing and human factor issues at the Reagan National control tower, noting that a single controller was handling both helicopter and airplane frequencies on the night of the crash. While the board concluded that staffing levels technically met FAA requirements, it said extended shifts likely reduced alertness and vigilance, increasing operational risk.

The safety board also criticized what it described as the FAA’s long-standing resistance to safety recommendations under previous administrations.

A visitor walks toward flowers and a letter left in memorial to the victims of a midair collision of an American Airlines jet and a Black Hawk helicopter near the Potomac River at the base of the Titanic Memorial in Washington, on Feb. 1, 2025. Carolyn Kaster/AP Photo

The U.S. Army was also cited for failing to fully implement a safety management system that could have addressed altitude risks on Washington helicopter routes. Investigators said the Black Hawk’s altimeter likely misreported altitude by about 100 feet, contributing to the crew’s belief that they were flying within authorized limits.

Federal ResponseThe FAA said in a Jan. 27 statement that it “values and appreciates the NTSB’s expertise and input” and that it has acted on urgent safety recommendations issued in March 2025, adding it would carefully consider additional measures outlined in last week’s findings.

Amid the fallout from the 2025 crash, U.S. Transportation Secretary Sean P. Duffy recently announced that the FAA had formalized permanent restrictions on helicopters operating near Reagan National unless they are carrying out essential operations.

The rules move helicopter routes farther away from Reagan National and require all military aircraft to broadcast their locations during flight, and prevent air traffic controllers from relying on visual separation.

“After that horrific night in January, this Administration made a promise to do whatever it takes to secure the skies over our nation’s capital and ensure such a tragedy would never happen again. Today’s announcement reaffirms that commitment,” Duffy said in a Jan. 22 statement. “The safety of the American people will always be our top priority. I look forward to continuing to collaborate with the NTSB on any additional actions.”

The Trump administration on Jan. 26 unveiled a major overhaul of the FAA to bolster modernization efforts and enhance safety, including the installation of a new air traffic control system and advanced aviation technologies.

Tyler Durden Mon, 02/02/2026 - 12:05Authored by Steve Watson via Modernity.news,

Arizona is ground zero in the fight to reclaim U.S. borders, with ICE shelling out a whopping $70 million for a 418,000-square-foot warehouse in Surprise—the size of seven football fields—to process and detain illegal aliens targeted for deportation. The acquisition under the Trump administration marks a long-overdue shift from the chaos of unchecked migration that flooded communities under previous Democrat-led policies.

The Department of Homeland Security snapped up the sprawling industrial site near Dysart and Cactus roads in a cash deal completed January 23, as property records confirm. ICE plans to convert it into a 1,500-bed processing center, part of a broader push to expand detention capacity amid renewed focus on mass deportations.

Local officials in Surprise distanced themselves, stating they “do not participate in ICE operations” but can’t block federal authority. Yet the move has ignited fury from Arizona Democrats, who see it as a direct threat to their sanctuary-state dreams.

ICE just purchased a massive 418,000 sq ft warehouse in Arizona and the Democrats are LOSING THEIR MINDS

— Libs of TikTok (@libsoftiktok) January 30, 2026

Cry harder, Libs.

ICE is here to stay! pic.twitter.com/hKlZhcYscG

State Senator Analise Ortiz slammed the purchase as “abhorrent,” adding “It really should chill all of us because ICE is violating the US Constitution, which means none of us are safe, including United States citizens.”

The warehouse buy comes hot on the heels of Arizona Attorney General Kris Mayes’ inflammatory warnings to ICE agents, where she suggested citizens could legally shoot masked feds under the state’s Stand Your Ground law.

In a brazen display of anti-enforcement bias, Mayes told local media: “You have these masked Federal officers with very little identification, sometimes no identification, wearing plain clothes and masks. And we have a stand your ground law that says that if you reasonably believe that your life is in danger, and you’re in your house or your car or on your property, that you can defend yourself with lethal force.”

She doubled down, questioning how people would know if masked intruders are legitimate officers: “But how do you know they’re a peace officer? It becomes, did they reasonably know that they were a peace officer?” Mayes even boasted of her own gun ownership, implying she’d react the same way.

Republicans blasted her comments as dangerously irresponsible, with calls for resignation pouring in. Senate Majority Leader John Kavanagh demanded she retract and step down, while Congressman Abe Hamadeh accused her of justifying murder against federal agents. It’s classic leftist hypocrisy: championing gun rights only when it suits their agenda to sabotage border security.

Mayes also launched a webpage urging citizens to report and film alleged ICE misconduct, vowing to prosecute agents for “assault, murder, unlawful imprisonment” if they step out of line. She warned ICE to “keep your hands off of our tribal members,” positioning herself as a defender against federal overreach while ignoring the real victims—American communities ravaged by illegal immigration.

The new Arizona facility is just one piece of ICE’s aggressive warehouse-buying spree across the U.S., with the agency acquiring sites in at least eight states to ramp up detention networks. Recent purchases include a $102 million warehouse in Maryland and plans for an 8,500-bed mega-jail in El Paso, Texas, as part of a $45 billion effort to enforce immigration laws long ignored by deep-state bureaucrats.

While open-borders advocates howl in protest, this facility promises to bolster enforcement efforts, ensuring criminals and overstays are swiftly removed to protect American families and sovereignty.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

Tyler Durden Mon, 02/02/2026 - 11:25

Recent comments